CA - Parkland: Debt Reduction And Shareholder Activism Could Make For An Interesting 2023

2023-03-24 11:30:00 ET

Summary

- Parkland is a large fuel retailer, operating its own refinery in British Columbia.

- A recent acquisition helps to diversify away from being a fuel distributor.

- The focus will be on debt reduction. Thanks to the majority of the debt consisting of fixed rate debt, I do not anticipate any issues despite the high debt level.

- The net debt will decrease to just around C$4B by the end of 2025.

Introduction

Parkland ( PKIUF ) ( PKI:CA ) is a major fuel refiner, supplier and marketer in Western Canada where it operates the 55,000 barrel per day refinery in Burnaby, British Columbia. The company has been trying to diversify its operations and acquired a frozen food chain in 2022. This will be a welcome diversification for the fuel-focused business.

Parkland's primary listing is in Canada, where it's trading with PKI as its ticker symbol. The average daily volume on the TSX is almost 600,000 shares , making the TSX by far more liquid than any of the secondary listings. The current market capitalization of Parkland is just over C$5.6B, considering there are just over 175 million shares outstanding.

FY 2022 wasn't so bad at all and the DCF increased substantially

As this article is focusing on the financial results of 2022, the outlook for 2023 and the debt situation, I would recommend you to read up on the business model and Parkland's strategy in this 2022 article .

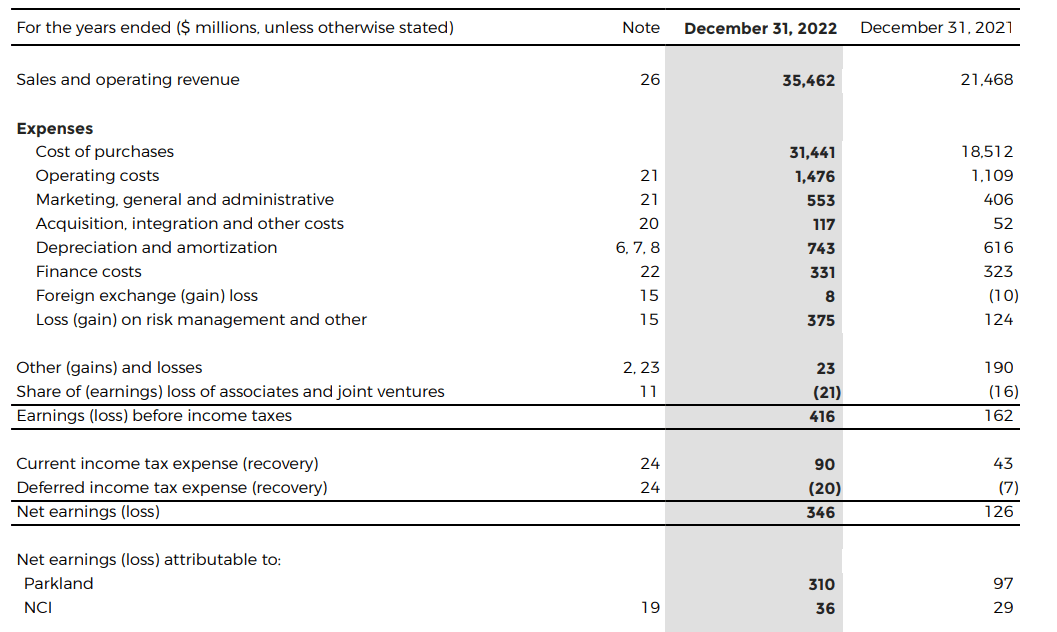

During the entire financial year, Parkland reported a total revenue of approximately C$35.5B , which is an increase of almost 70% compared to FY 2021. Not in the least because fuel got more expensive (which we also see in a similar increase in the cost of goods sold) but also because the frozen food retail division is contributing as well. The bottom line showed a net income of C$346M , of which C$310M was attributable to the shareholders of Parkland. This resulted in an EPS of C$1.94 based on the average share count of just under 160M shares but keep in mind the current share count is almost 10% higher.

{kind=link}

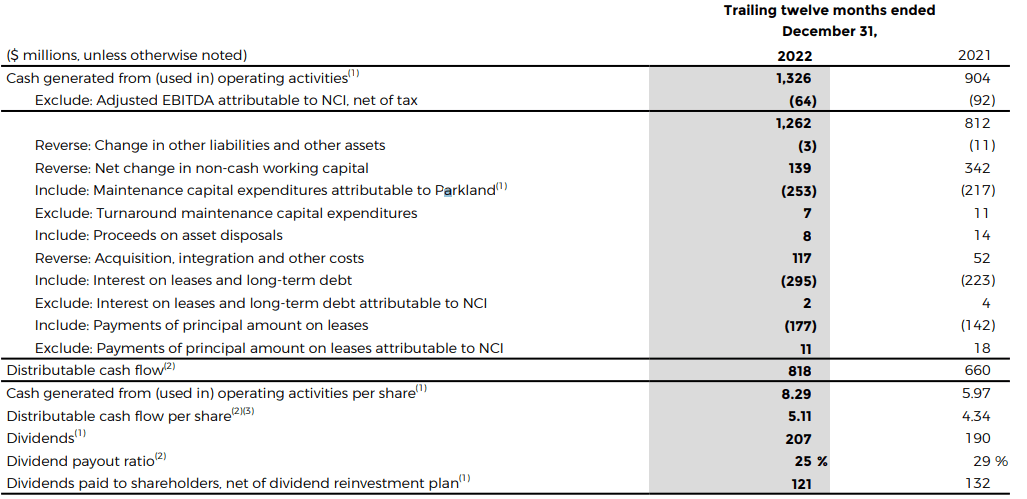

What's important to fully understand Parkland and its performance is the sustaining free cash flow generated by the company. And fortunately, Parkland does an excellent job in disclosing its distributable cash flow: the free cash flow generated by the company including tax and interest payments as well as sustaining capex but excluding growth initiatives.

{kind=link}

As the image above shows, the adjusted operating cash flow was C$1.26B and after including the lease payments, interest payments and the sustaining capex, the distributable cash flow was C$818M which is approximately C$4.66 per share (using the current share count instead of the average weighted share count which is why the DCF per share comes in at C$5.11 in the image above). That is an excellent result as it indicates the stock is still trading at a free cash flow yield of almost 15%.

Looking forward to 2023 and a closer look at the debt on the balance sheet

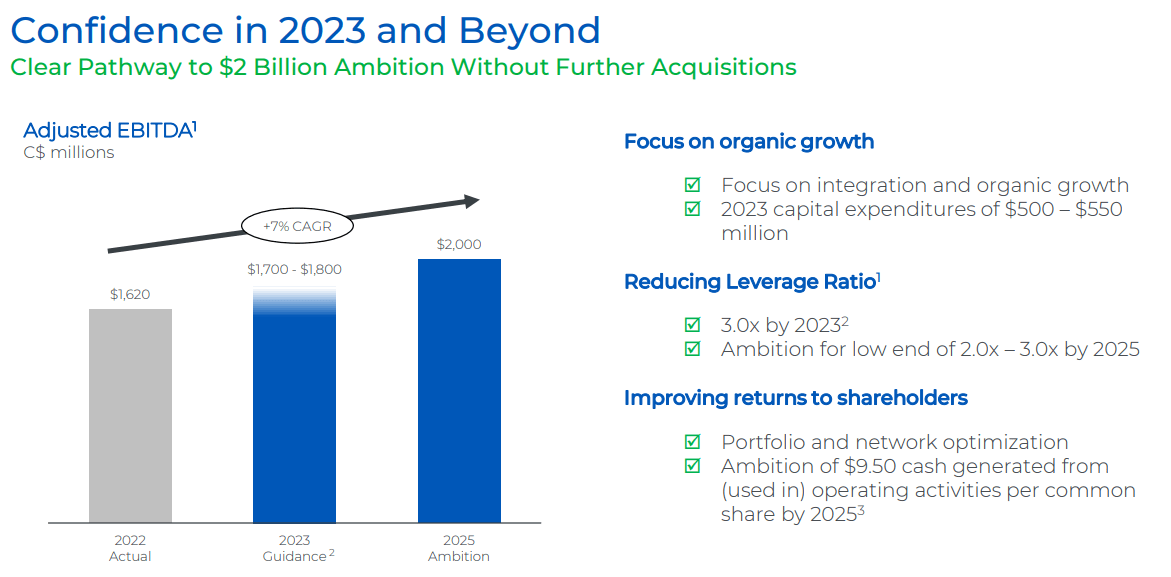

After completing a pretty successful 2022, Parkland plans to further increase its EBITDA in 2023. The official guidance calls for a full-year EBITDA of C$1.7-1.8B, which would be an increase of 5-11% compared to 2022. The mid-term plan is still to generate C$2B in EBITDA by 2025 which should result in an operating cash flow of C$9.50 per share.

{kind=link}

One of the most important elements of the image above is the commitment to reduce the leverage ratio. Parkland commits to reduce the net debt to just 3 times EBITDA by the end of this year (implying a year-end net debt of C$5.1-5.4B) but what I am particularly pleased with is the 2025 debt ratio guidance. Parkland wants to reach the 'low end' of its targeted EBITDA multiple of 2-3 which means the net debt will drop down to around C$4B based on that guidance, which means Parkland anticipates to reduce its net debt by about C$500M per year in both 2024 and 2025.

That's music to my ears because although Parkland's M&A strategy has clearly paid off, times are changing and as debt is getting more expensive, Parkland for sure doesn't want to get caught in the vicious circle in having to borrow at much higher rates.

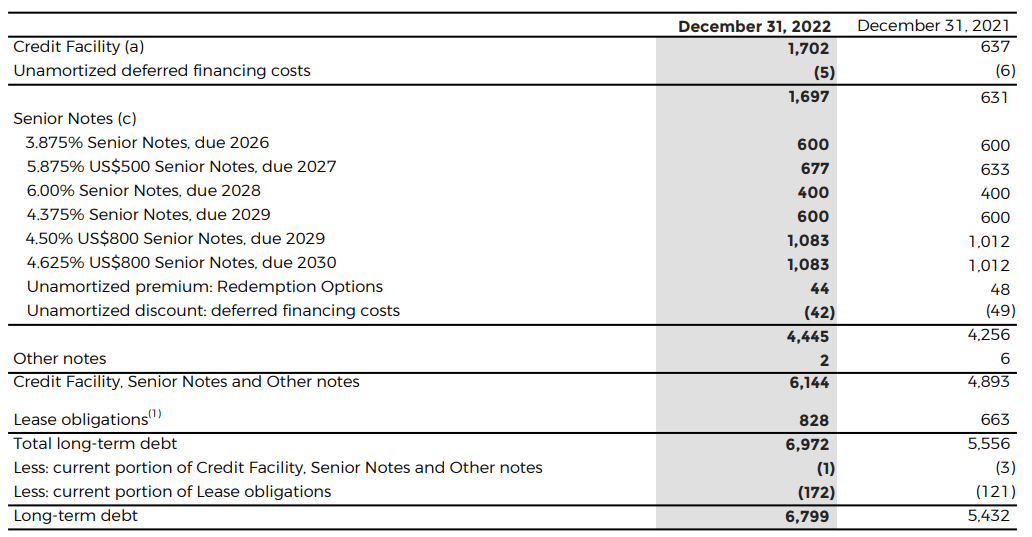

And that brings us to one of the elements I appreciate the most about Parkland. Its CEO has locked in the cost of debt for the vast majority of the outstanding debt. As you can see below, of the C$6.1B in gross debt, almost C$4.5B has a fixed interest rate, which means the income statement (and free cash flow result) will only get hit by increasing interest rates on the credit facility. But as there's no fixed-rate debt maturing before 2026, you can be sure that credit facility will be sharply reduced by using the incoming free cash flow.

{kind=link}

Investment thesis

While yes, Parkland has a substantial amount of debt on its balance sheet, the vast majority has a fixed interest rate, so the company should not be dragged into a vicious circle of expensive refinancings or interest expenses increasing month after month. Sure the average cost of debt on the credit facility will increase but even if there is an average increase of 400 basis points (this is an arbitrary number and not the interest rate increase the company is guiding for), the C$65M in additional interest expenses (which is less than C$50M in free cash flow difference in an after-tax basis) won't have a major impact on the health of the company. And as Parkland will pay off some of that debt, the total impact of increasing interest rates will be even lower.

As Parkland is guiding for the EBITDA to increase to C$2B without any M&A, the C$380M in additional EBITDA will likely result in at least C$250M in additional free cash flow, which will further boost the distributable cash flow per share from C$4.66 to in excess of C$6 (assuming the current share count remains unchanged).

I was worried about the debt, but I shouldn't be as Parkland should have no issues to deal with the current maturity schedule. An activist shareholder recently urged Parkland to look at scenarios wherein the refinery would be spun off or sold, so perhaps this will help the company to start trading at higher multiples.

I have a small long position in Parkland as I was unable to take advantage of the dip in Q4 2022, but the company for sure still is on my shortlist to perhaps increase my position.

For further details see:

Parkland: Debt Reduction And Shareholder Activism Could Make For An Interesting 2023