PCTY - Paylocity: A Pullback Would Present A Better Risk/Reward Profile

2023-09-20 13:23:11 ET

Summary

- Paylocity's financials show a strong position with cash and no debt.

- The company's efficiency and profitability metrics are decent, but there is room for improvement.

- Paylocity has seen significant growth in the past, but future growth may be more challenging to sustain. Valuation suggests the company is slightly overvalued.

Investment Thesis

After Paylocity's ( PCTY ) 25% depreciation in 1 year, I wanted to take a look at the company's financials to see if it's a good time to start a position. With a decent yet conservative growth in revenues assumed, I believe the company is slightly overvalued and a further pullback in price would present a better risk/reward profile for me, therefore, I give the company a hold rating for now.

Financials

As of FY23 , the company had around $140m in cash and equivalents, against zero debt. This is a great position to be in as it allows the company the flexibility to expand further without any burden of annual interest expenses on its shoulders. It can deploy all the free cash available to further its growth.

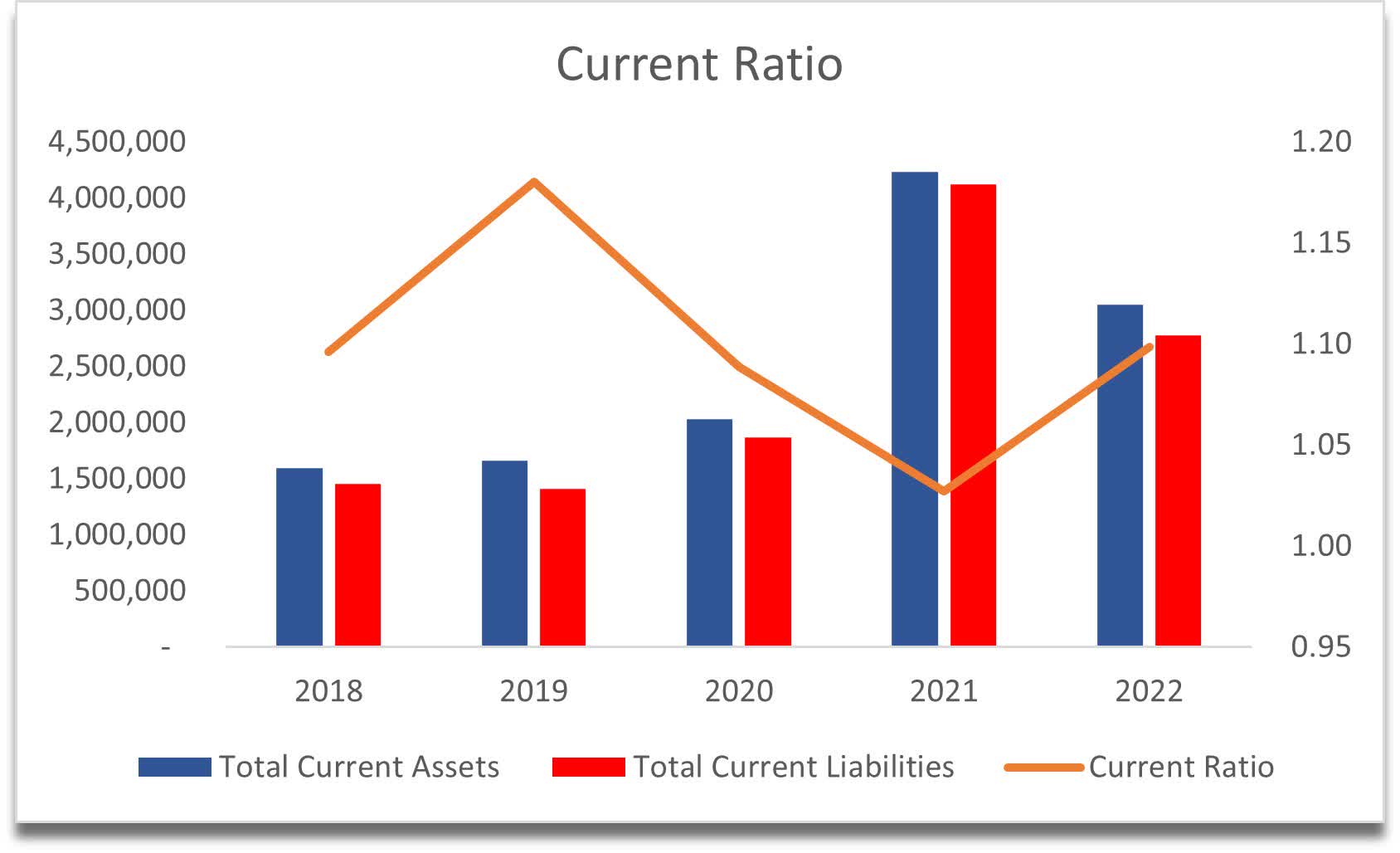

The company's current ratio is not ideal, however, as long as it's not under 1, I'm okay with it. I would like to see a ratio in the range of 1.5-2.0 as I believe that is an efficient ratio and a good balance between being able to pay off short-term obligations and deploying cash for growth initiatives. The company can pay off its ST obligations, therefore, it has no liquidity issues as of now.

{kind=link}

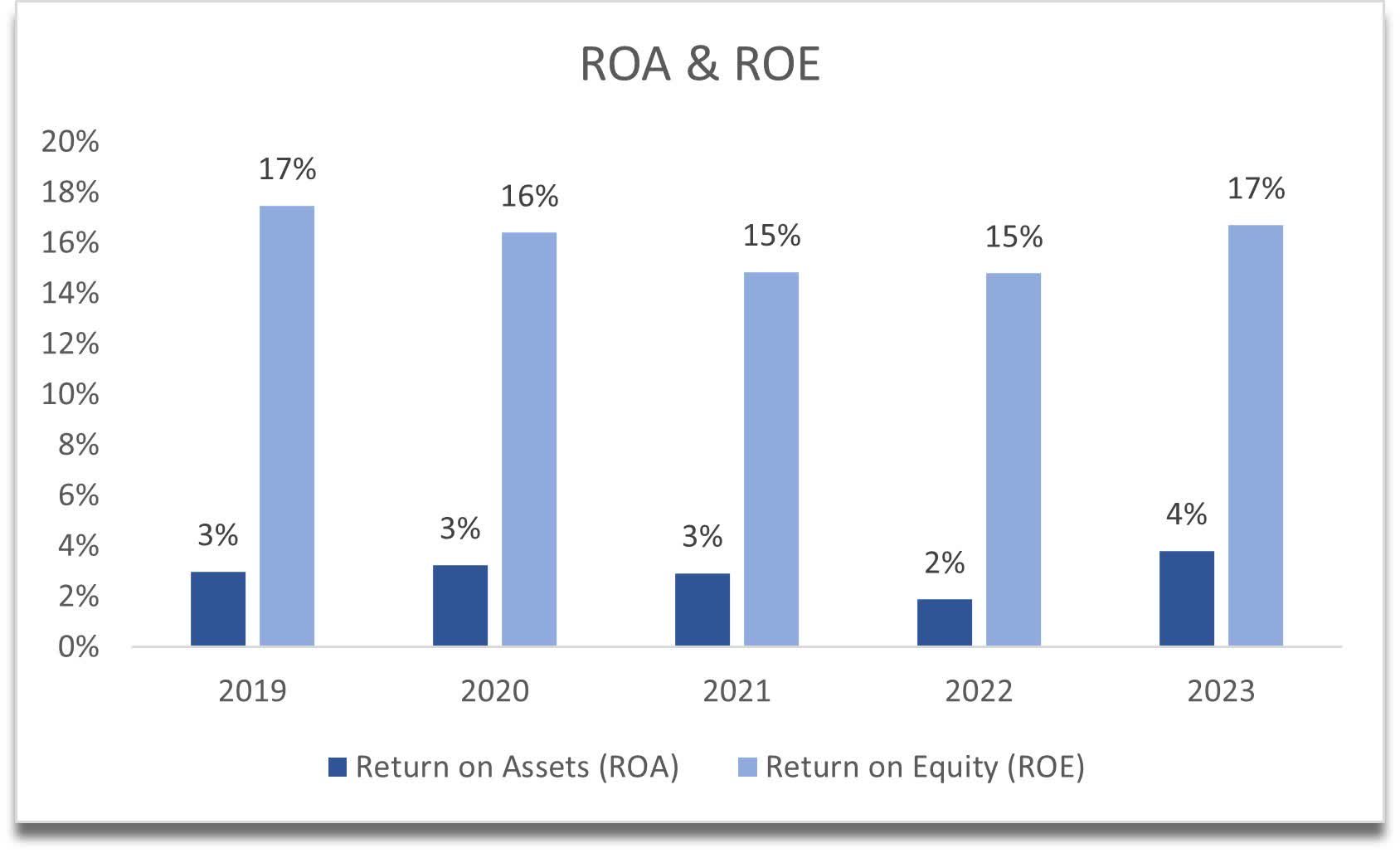

In terms of efficiency and profitability, the company's ROA and ROE have improved slightly, however, ROA is a little on the lower end, as I'd like to see at least 5% here, whereas ROE is pretty decent and is above my minimum of 10%. This tells me that the company could do a better job of utilizing its assets while creating value for shareholders as it seems to be using shareholder capital quite efficiently.

{kind=link}

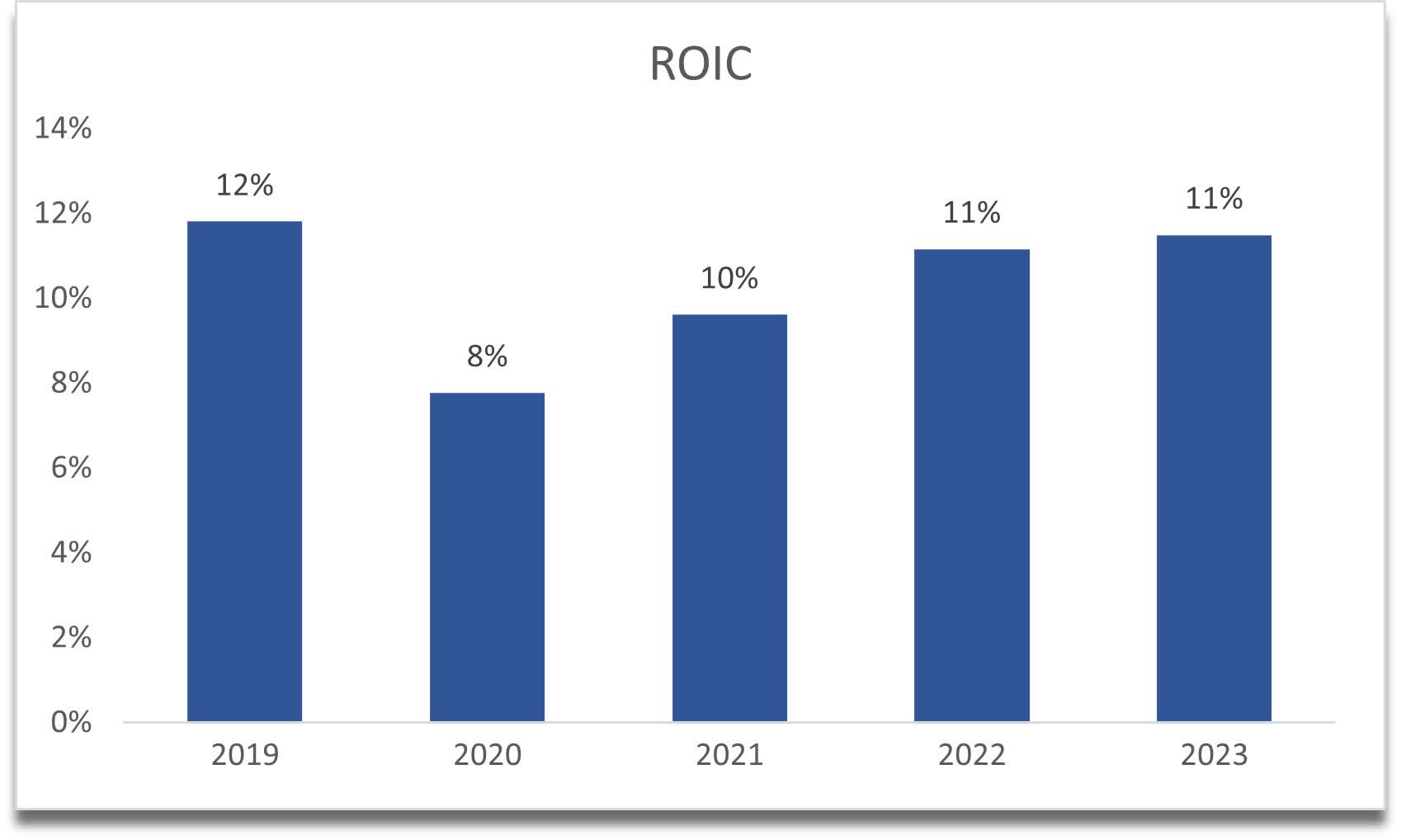

Paylocity's return on invested capital is also quite decent and above my minimum of 10%, which tells me that the company has a unique product that provides it with a competitive edge and a moat, which is exactly what I'm looking for in an investment.

{kind=link}

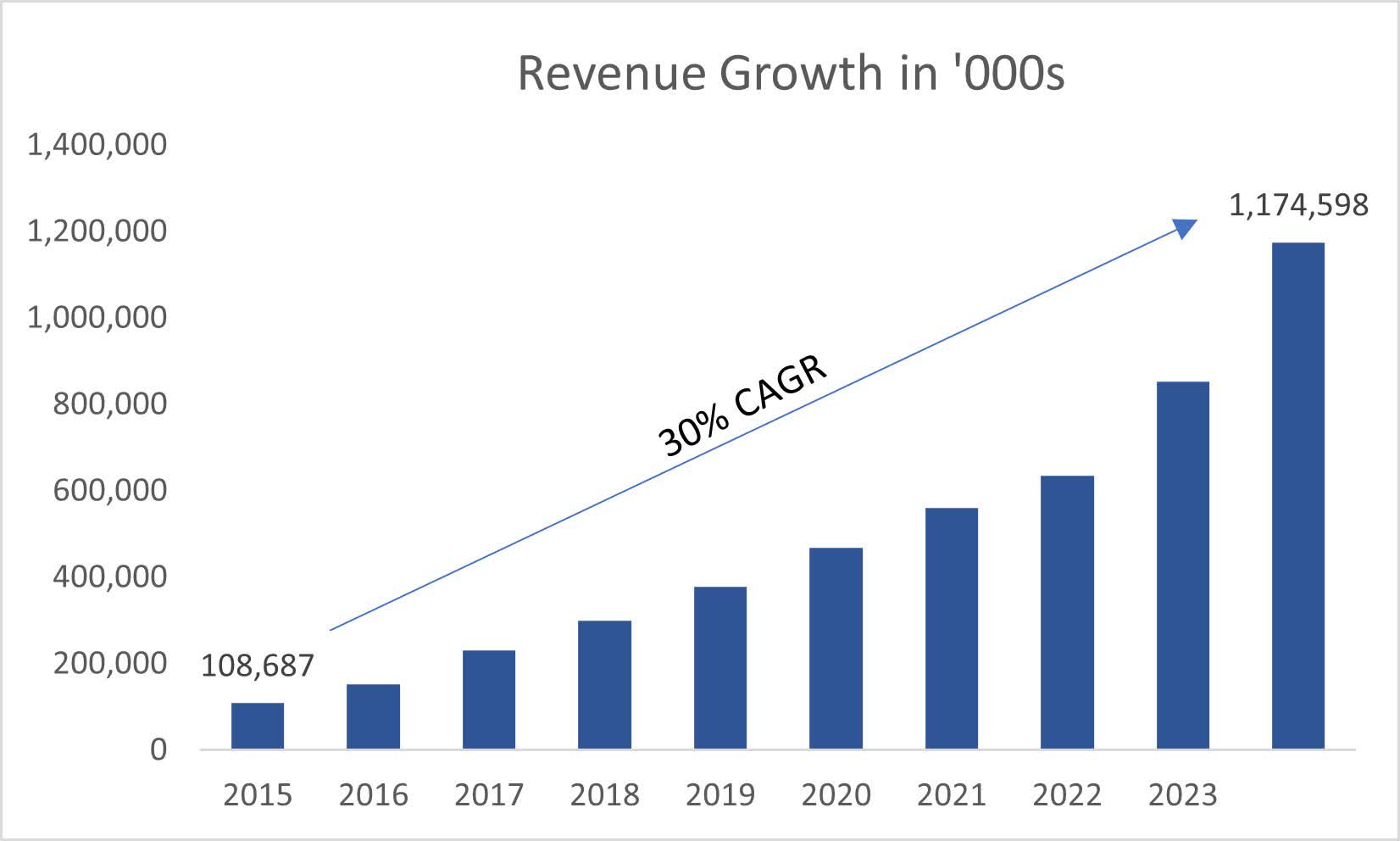

The company saw phenomenal growth in the previous decade, averaging 30% CAGR, which is fantastic. Can this be sustained going forward? It's hard to say, especially when analysts are estimating around 20% for the next year, which drops to 18.5% the year after. I will anchor my revenue assumptions to these numbers also. After that, the numbers become less reliable and will change over time as more information comes to light in the subsequent earnings calls.

{kind=link}

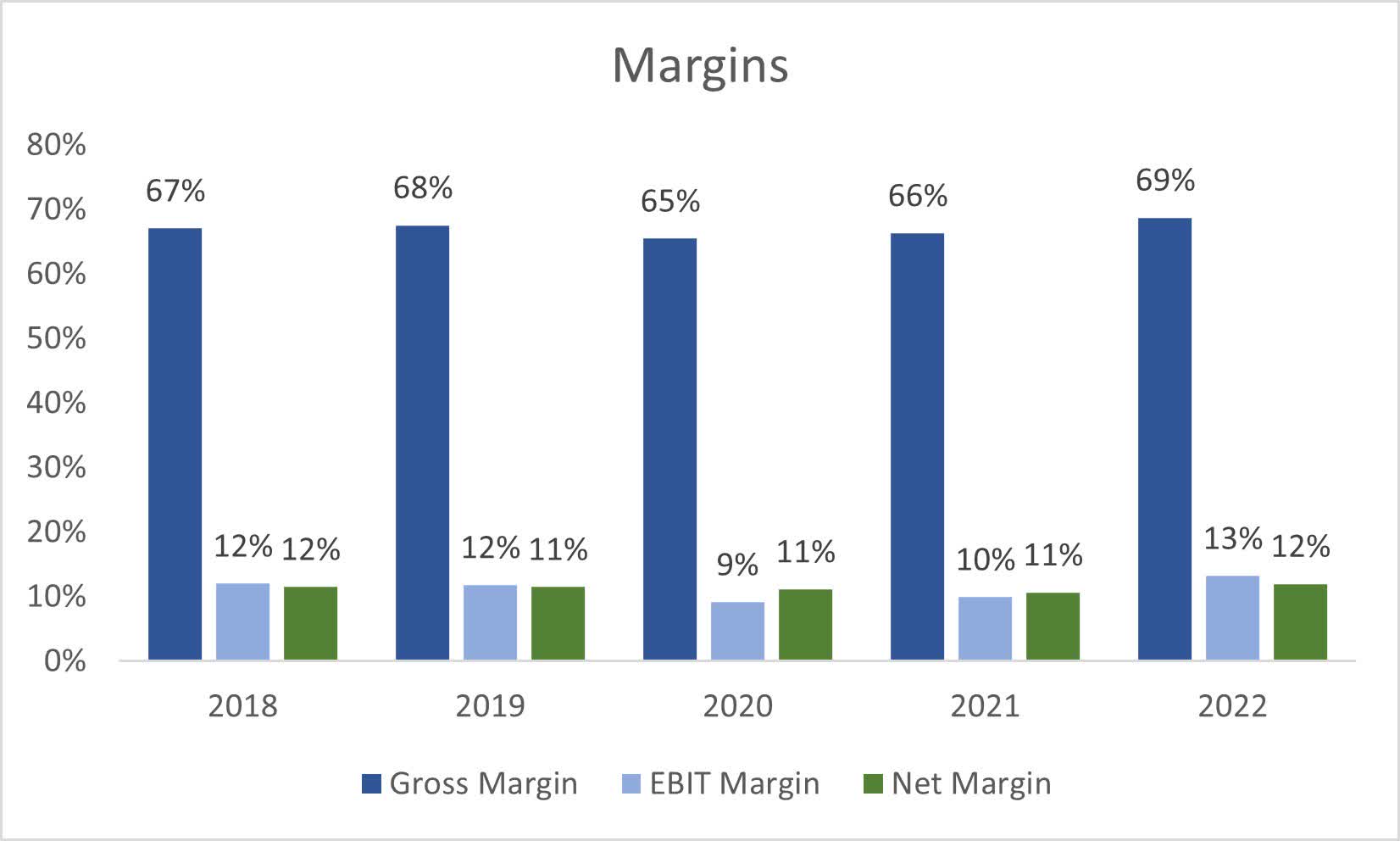

Over the last 5 years, the company has kept its GAAP margins relatively stable. The company likes to use its non-GAAP metrics to show its "true" value, therefore, I will stick with those also, otherwise, the company would be worth much less. Stock-based compensation is a big one for the company and distorts the figures quite a bit.

{kind=link}

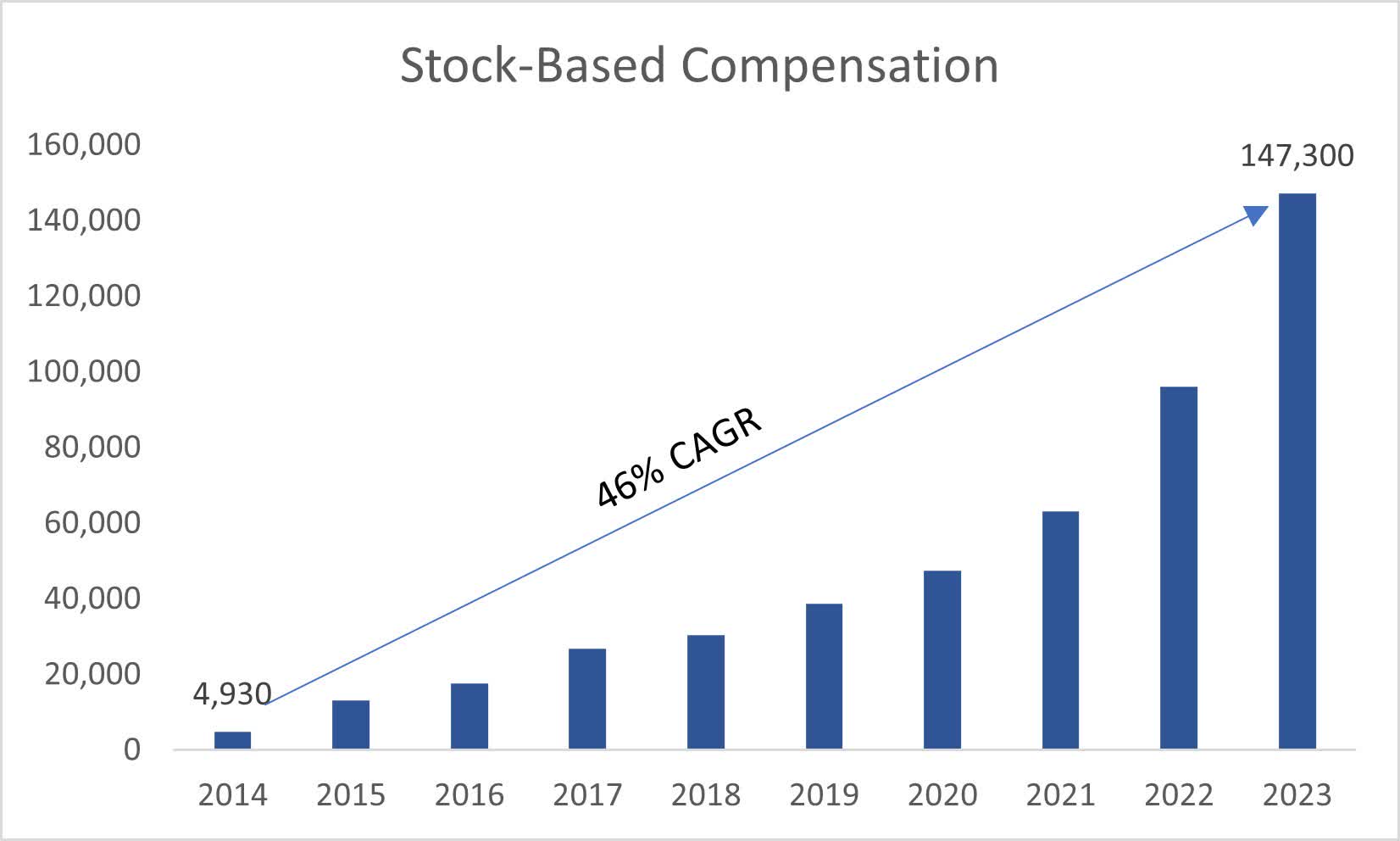

The company is hiring new staff in the mid-teens rate, which makes stock-based compensation go up also, and it doesn't seem to stop any time soon, as over the last decade, the company's SBC has increased by 46% CAGR. This may lead to share dilution or in some cases a drop in share price if the employees decide to sell their shares on the open market right after the shares have vested.

{kind=link}

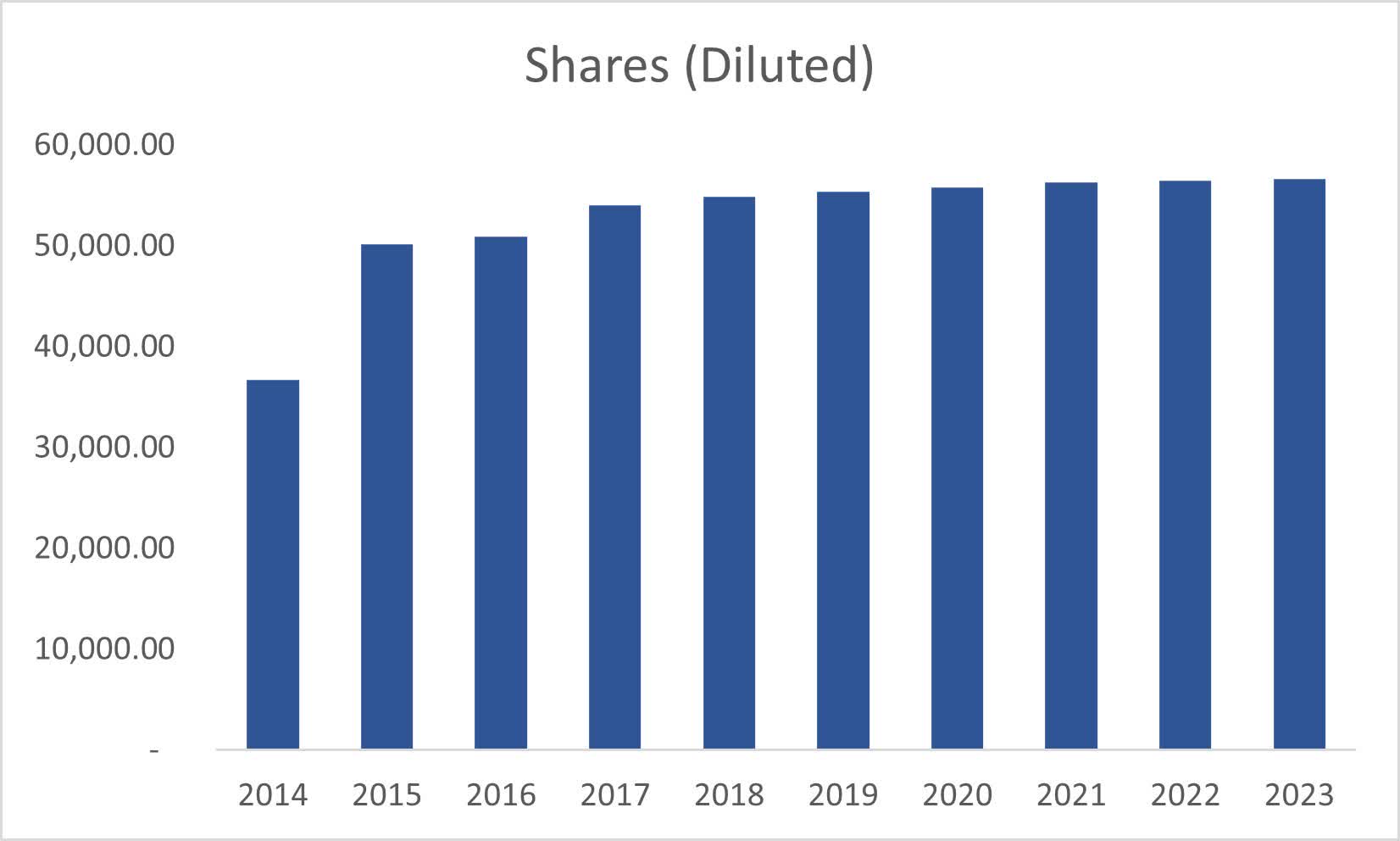

Speaking of share dilution, the company hasn't increased shares outstanding very dramatically since FY14, which means the company isn't diluting its shareholders.

{kind=link}

Overall, the company looks to be in decent shape and with a high probability of performing well in terms of revenue growth, which will be based on the company's ability to keep selling its product to more clients. The company seems to have a competitive edge and a decent moat, and that is something I wouldn't mind paying a premium for.

Valuation

So, I don't know how realistic it is to assume that the company is going to be able to achieve a 30% CAGR of revenue growth over the next decade, as it did in the last. I don't think it's out of the realm of possibility, however, I will lean towards the conservative assumptions, so for my base case, I will assume the company's going to grow at a respectable growth rate of around 14% CAGR over the next decade. It just makes sense that it won't grow as much as it did before because, when revenues were so low, it was much easier to grow, whereas now, revenues have already reached $1B and with a 14% CAGR over the next decade, revenues are going to reach $4.2B. That is a reasonable assumption in my opinion.

For the optimistic case, I went with an 18% CAGR, while for the conservative case, I went with a 10% CAGR to give myself a range of possible outcomes.

In terms of margins, I decided to keep the non-GAAP metrics as they are over the analysis period because if I had used GAAP metrics in operating margins, the company would have lost 1200bps of margins and would not be as valuable.

On top of these estimates, I will add a 15% margin of safety because the financials of the company are quite good with no apparent red flags in my opinion. With that said, Paylocity's intrinsic value is $157 a share, meaning the company is currently trading at a 16% premium to its fair value and does not provide an enticing risk/reward.

{kind=link}

Closing Comments

The company's growth prospects are outstanding, however, if I'm being on the more conservative side, I would like to see a further pullback in the share price of another 16% before I would consider jumping in, as long as the thesis hasn't changed with time and the company is still performing at a high caliber.

I just find it hard to believe that the company will be able to grow at such a pace as it did in the previous decade, now that revenues have increased 10-fold. But if you believe that the company is going to outperform and that the current 25% drop in share price in a year is sufficient for you to start a position, go ahead. As for me, I would rather be safe than sorry when it comes to investing. That means I may miss some opportunities because I was too conservative, but it also means I will not suffer if I start a position at the wrong time. This one goes on my price alerts with many others and will re-visit the company when it announces its next quarter results.

For further details see:

Paylocity: A Pullback Would Present A Better Risk/Reward Profile