PCTY - Paylocity: Not Expensive When Checking Recurring Revenue And Innovation

2023-04-12 11:35:01 ET

Summary

- Paylocity Holding Corporation is a leading provider of cloud-based payroll and human capital management software solutions.

- In my view, it is quite ideal that Paylocity does not really need a lot of debt financing to operate. The company appears to receive financing from clients and providers.

- Further plans to continue to innovate on its cloud-based software platform to improve the user experience as well as to grow its sales organization could enhance FCF growth.

- Recurring and other revenue accounted for 99% and 94% of our total revenues for the three months ended December 31, 2021 and 2022, respectively.

Paylocity Holding Corporation ( PCTY ) expects sales growth to exceed 30% in 2023. With significant recurrent revenue, I believe that FCF will likely trend north driven by innovation. Besides, I believe that further increases in the product offering and more personnel will likely bring significant economies of scale. Even considering risks from competition or lack of sufficient innovation, I believe that the fair price should be close to $250 per share. Hence, in my view, the current stock price appears too low.

Paylocity Reports 92% Revenue Retention

Paylocity Holding Corporation is a leading provider of cloud-based payroll and human capital management software solutions.

Its SaaS platform offers a full range of products that help companies attract and retain talent, improve employee’s culture and engagement, and streamline and automate HR and payroll processes. With a unified platform, Paylocity provides a comprehensive solution for the modern workforce, helping companies improve efficiency and productivity in their human capital operations.

In my view, large organizations like Automatic Data Processing ( ADP ) or Paychex, Inc. ( PAYX ) use Paylocity mainly because of its technology, which appears to explain why the company reports 92% revenue retention. In my view, further improvements in technology will likely lead to more clients willing to use the services of Paylocity.

Source: Investor Presentation

Besides, the company appears to receive significant benefits from relationships with channel partners. It is also worth noting that Paylocity offers a lot of services for partners, including a partner portal, which enhances client retention and integrations with open APIs from other software.

Paylocity offers comprehensive HCM and payroll software solutions that deliver key benefits to clients such as a centralized platform, employee experience, insights and referrals, leading customer service, and seamless integration with an extensive ecosystem of partners. The company markets and sells the product suite through a direct sales force, and generates revenue based on the solutions purchased by the customer, the number of customer employees, and the number, type, and timing of services provided.

Source: Investor Presentation

Whether we appreciate the business model or not, in my view, it is worth having a look at it because of the recent financial stats. We are talking about double digit revenue growth, 15%-20% FCF growth, and 30%-35% EBITDA growth.

Source: Investor Presentation

Finally, it is also worth noting that the recent guidance given for 2023 includes 36% y/y revenue growth for 2023. The numbers were given in a recent presentation given to investors.

Source: Investor Presentation

Balance Sheet

Paylocity reports a considerable amount of cash, but most assets are represented by funds given by clients. In my view, it is quite ideal that Paylocity does not really need a lot of debt financing to operate. The company appears to receive financing from clients and providers.

As of December 31, 2022, management reported cash and cash equivalents of $120 million, accounts receivable close to $24 million, deferred contract costs of $68 million, and prepaid expenses of around $30 million. Funds held for clients were equal to $3.065 billion with total current assets of $3309 million, below the total amount of current amount of liabilities.

Non-current assets include capitalized internal-use software of $71 million, property and equipment close to $59 million, and goodwill of $102 million. Besides, long-term deferred contract costs stood at $262 million with long?term prepaid expenses of $6 million and total assets close to $3.937 billion, more than 1x the total amount of liabilities.

Source: Quarterly Report

Among the liabilities I did not really find a lot of financial debt. Most relevant liabilities are accounts payable worth $7 million, accrued expenses of $115 million, client fund obligations of $3.065 billion, and total current liabilities of $3.189 million. Finally, long-term operating lease liabilities are equal to $65 million, and total liabilities stand at $3.260 billion.

Source: Quarterly Report

It is worth noting that very recently we saw a significant decrease in the client funds obligations and funds held for clients. I hope that the company successfully stops the decline in funds from clients because Paylocity appears to receive some money thanks to interest income on these funds.

We earn interest income on funds held for clients. We collect funds for employee payroll payments and related taxes in advance of remittance to employees and taxing authorities. Prior to remittance to employees and taxing authorities, we earn interest on these funds through demand deposit accounts with financial institutions with which we have automated clearing house, or ACH, arrangements. We also earn interest by investing a portion of funds held for clients in highly liquid, investment-grade marketable securities. Source: Quarterly Report

My Assumptions Include Increases In Technology, More Personnel, Economies Of Scale, And More Communication About The Total Amount Of Recurring Revenue

In my business model, I assumed sufficient investment in technology leadership, which will likely enhance customer growth, and may bring economies of scale. More clients may enhance both EBITDA margins and FCF margins, which could bring stock valuation increases. In this regard, I believe that investors will likely appreciate the following commentary from management.

These investments include increasing the number of personnel across all functional areas, along with improving our solutions and infrastructure to support our growth. The timing and amount of these investments vary based on the rate at which we add new clients and personnel and scale our application development and other activities. Source: Quarterly Report

We expect these investments to increase our costs on an absolute basis, but as we grow our number of clients and our related revenues, we anticipate that we will gain economies of scale and increased operating leverage. As a result, we expect our gross and operating margins will improve over the long term. Source: Quarterly Report

Besides, I expect further expansion of product offerings and further development of the referral network. I believe that further plans to continue to innovate on its cloud-based software platform to improve the user experience as well as to grow its sales organization could also enhance sales growth. In particular, lowering customer acquisition costs thanks to partners will most likely be appreciated by the market.

I also believe that management will do good by highlighting the amount of recurring revenue obtained from clients. Recurrent revenue is highly appreciated by financial advisors because it facilitates running discounted cash flow models. More information about the recurrent revenue will likely enhance the demand for the stock.

We derive the majority of our revenues from recurring fees attributable to our cloud-based HCM and payroll software solutions. Source: Quarterly Report

Recurring and other revenue accounted for 99% and 94% of our total revenues for the three months ended December 31, 2021 and 2022, respectively, and 99% and 95% for the six months ended December 31, 2021 and 2022, respectively. Source: Quarterly Report

My DCF Model Implies A Target Price Of $250 Per Share

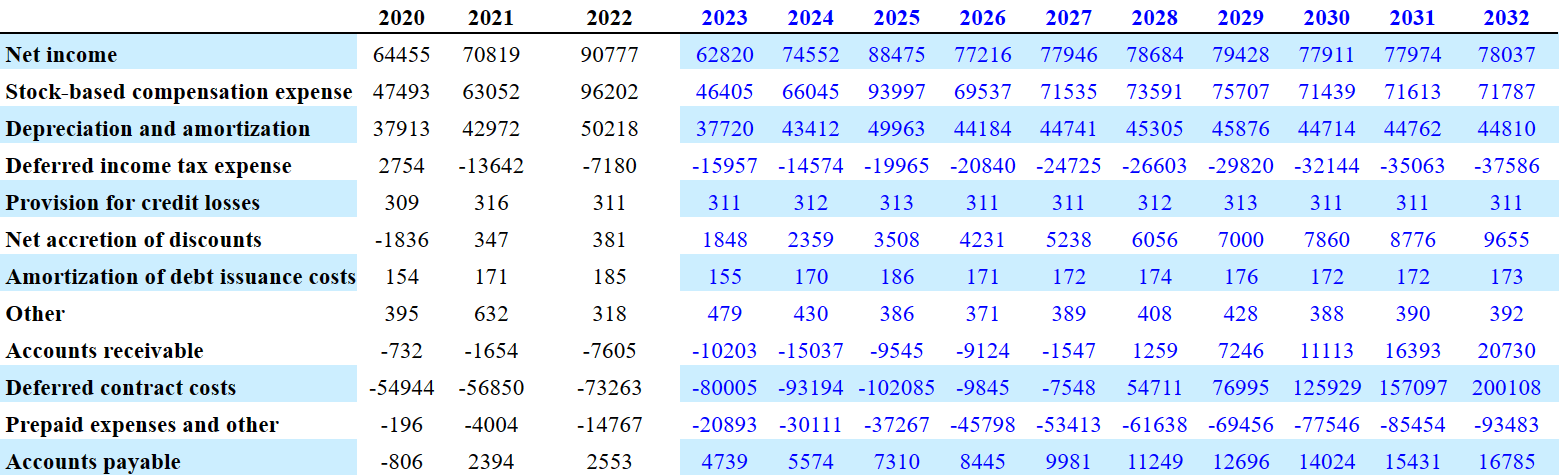

The numbers in my model include net income growth, moderate increases of D&A, increases in accounts payables, some provision for credit losses, and stock-based compensation expenses. The FCF would also increase considerably. The average FCF growth would be close to 20.5%. I believe that my figures are conservative and in line with the figures reported in 2020, 2021, and 2022.

My DCF model included 2032 net income of $78.5 million, 2032 stock-based compensation expenses of $71.5 million, depreciation and amortization close to $44.5 million, and deferred income tax expenses of -$38.5 million. Also, with changes in accounts receivable of $20.5 million, changes in deferred contract costs of $200.5 million, and prepaid expenses close to -$94.5 million, the CFO would stand at $319.5 million. If we also assume 2032 capex of -$3 million, the implied 2032 FCF would stand at $317.5 million.

{kind=link}

{kind=link}

With a WACC of 9% and an EV/FCF multiple of 95.5x, the implied enterprise value would be $13.810 billion. Adding cash and cash equivalents of $120 million and other long-term liabilities of $3.5 million, equity would be close to $13.955 million. Besides, the implied price would stand at $250 per share.

Source: My DCF Model

Many Competitors

Paylocity Holding operates in a highly competitive and fragmented market, where its competition varies for each of its solutions. Its competitors primarily include HR and payroll services and software providers, such as Automatic Data Processing, Inc., Paychex, Inc., Paycom Software, Inc. (PAYC), Paycor, Inc. (PYCR), Ultimate Kronos Group, and other local and regional providers.

In my view, the main competitive factors on which they compete include the ability to connect with the modern workforce, a comprehensive suite of payroll and HCM products on a single platform, breadth and depth of product functionality, configurability and ease of use of solutions, modern, mobile, intuitive, and consumer-oriented user experience, benefits of a cloud-based technology platform, and the ability to innovate and respond quickly to customer needs.

Risks

The company faces several risks that could affect its ability to operate and maintain its profitability. Volatility in operating results, competition in the markets in which it operates, lack of innovation, and the inability to manage growth effectively are some of the main risks.

The market for our solutions is characterized by rapid technological advancements, changes in client requirements, frequent new product introductions and enhancements and changing industry standards. The life cycles of our products are difficult to estimate. Rapid technological changes and the introduction of new products and enhancements by new or existing competitors, or development of entirely new technologies to replace existing offerings could limit the demand for our existing or future solutions and undermine our current market position. Source: Annual Report

Besides, technical problems such as interruptions in the operations infrastructure or software glitches could also damage the company's reputation. In addition, the acquisition of other companies or technologies could distract management attention, and result in additional dilution for shareholders. Finally, data security and the protection of intellectual property rights are also important concerns that need to be addressed. Paylocity holds relevant information about employees, bank accounts, and money flow. If some information becomes public, I believe that many clients and market participants will be upset, which may lead to stock price declines.

Conclusion

Paylocity Holding Corporation has a solid business model and a business strategy focused on innovation and significant revenue growth. Its unified cloud-based software platform and comprehensive payroll and human capital management product offerings position it as a leader in a highly competitive market. Although there are risks, such as competition and volatility in operating results as well as risks from lack of innovation, in my view, the stock is undervalued. I believe that future free cash flow growth and revenue growth would justify a valuation of $250 per share.

For further details see:

Paylocity: Not Expensive When Checking Recurring Revenue And Innovation