FVRR - Payoneer: Transforming Cross-Border Payments With Its Comprehensive Range Of Offerings

2023-06-22 02:28:02 ET

Summary

- Payoneer Global Inc. is well-positioned to become the top choice for cross-border payment solutions in the commercial sector.

- The company has a strong presence in over 190 countries and offers a comprehensive range of payment solutions, targeting the expanding e-commerce and cross-border payments markets.

- PAYO's shares are trading at a significant discount, with an EV/Sales revenue multiple of approximately 1.4x.

Thesis

With its extensive global network and comprehensive range of products, I believe Payoneer Global Inc. ( PAYO ) is well-equipped to establish itself as the top choice for businesses and freelance/gig-workers seeking cross-border payment solutions in the commercial sector. Compared to its peers, PAYO's shares are trading at a significant discount on an EV/Sales revenue multiple of approximately 1.4x. This presents an appealing risk-reward opportunity, in my view, for small-cap investors looking to capitalize on the favorable trends in B2B cross-border payments. I view the stock as a buy and have an end-of-year price target of $5.6 on the stock.

Company Overview

PAYO was founded in 2005 with the goal of helping small businesses thrive in an age where technology and the internet were changing the world of commerce. Since its founding, PAYO has created and built out a global payment and commerce-enabling platform to facilitate payments in multi-currencies, specifically geared towards SMBs that sell through marketplaces from over 190 countries.

Strong Quarter with Higher Float Income

PAYO had a strong start to the fiscal year 2023, surpassing revenue and EBITDA expectations. This was mainly driven by higher interest income and sustained growth in their high-take-rate products. Consequently, management increased their guidance for the year and also announced an $80 million share repurchase program. The revised outlook given by the management for FY23 includes projected revenue of $810-$820 million (30% YoY growth at the midpoint) and adjusted EBITDA of $140-$150 million. The revenue forecast incorporates $200 million in interest income from customer balances, while adjusted EBITDA factors in a $15 million technology investment headwind and a $15 million headwind from incentive payments from a large enterprise client, as previously anticipated. I have a positive outlook on the shares, given the ongoing momentum in PAYO's core business, long growth runway, and tailwinds from higher interest rates.

Long growth runway given the massive TAM

PAYO has established a substantial presence in the cross-border payments sector, operating in over 190 countries and territories. The company has built an extensive network of global bank partnerships and payment solutions, catering to both payers and receivers of payments. On the receiver side, PAYO enables businesses to receive payments locally, handle billing and invoicing globally, and streamline operations with popular marketplaces like Upwork Inc. ( UPWK ), Fiverr International Ltd. ( FVRR ), and Airbnb, Inc. ( ABNB ). On the payer side, PAYO facilitates payments to vendors, employees, and also handles EU and UK VAT taxes. Additionally, users can transfer funds to their bank accounts and withdraw cash from ATMs. I view PAYO's comprehensive range of offerings positively, as it allows the company to target the expanding e-commerce and cross-border payments markets effectively. A study by Vantage Market Research projects a 10% compound annual growth rate in B2B cross-border payment volumes until 2030, estimating the market to be worth $21 trillion. Given the sizable and growing market, I believe that PAYO's robust cross-border payments platform is well-positioned to achieve organic revenue growth of over 20% in the coming years.

{kind=link}

Valuation

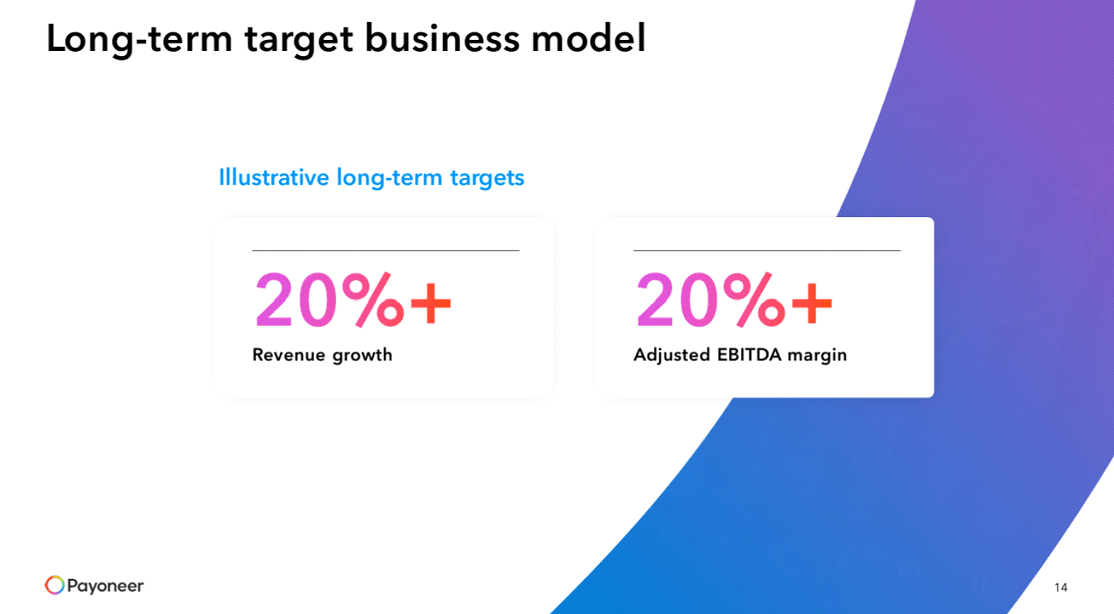

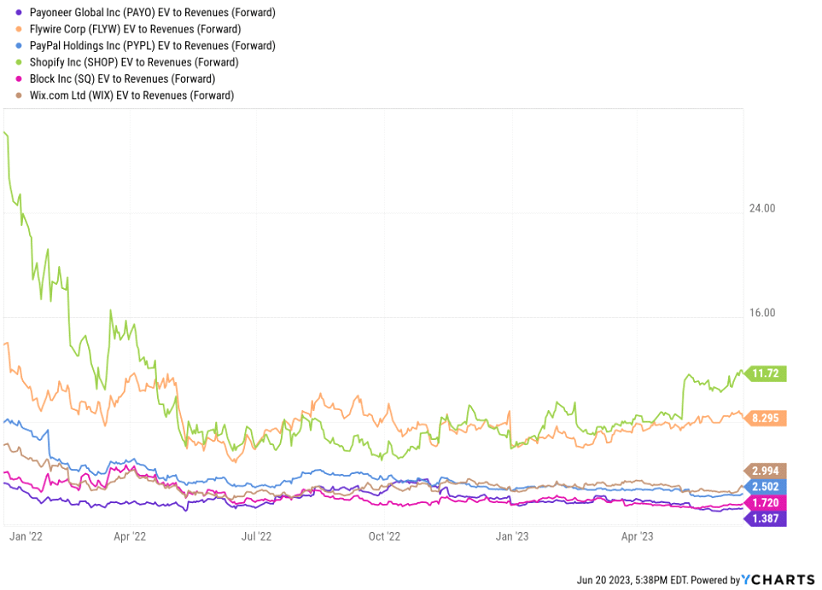

PAYO stock currently trades at an EV/revenue multiple of ~1.4x to FY23 estimate, a discount to a diverse group of business/cross-border payments peers, and a significant discount to that of high-growth, modern payments providers that have entered the public markets over the past few years, similar to PAYO. In addition, PAYO has a significantly better margin profile than nearly every other payments provider, which is largely due to the attractive margin profile on PAYO's newer products that are scaling at a rapid pace and being adopted in all of PAYO's markets across the globe. I view the risk-reward as favorable and believe that the shares can re-rate higher as PAYO continues tracking towards its LT operating targets that include 20% + organic growth and 20%+ EBITDA margins. My end-of-year price target of $5.6 is based on a forward EV/Sales multiple of 2x applied to 2024 revenue estimate .

{kind=link}

Risks To Target

PAYO may face challenges in its growth trajectory and market share due to intensified competition resulting from the promising growth opportunities in cross-border payments. Moreover, the regulatory landscape surrounding cross-border payments is stringent, and any alterations in regulations or compliance issues among PAYO's end-users could potentially impact the company's financial performance negatively.

Conclusion

PAYO is a cross-border payments platform that specializes in commercial payments and has a presence in more than 190 countries. I am impressed by PAYO's broad range of cross-border payment offerings, including the issuance of physical and virtual cards, merchant services, tax solutions, compliance services, and foreign exchange solutions. In my view, PAYO stands out as a diverse provider of cross-border payments in a market that I believe is poised for disruption and significant expansion, driven by the growing popularity of online marketplaces. I view the stock as a buy and have an end-of-year price target of $5.6 on the stock.

For further details see:

Payoneer: Transforming Cross-Border Payments With Its Comprehensive Range Of Offerings