PINS - PayPal: Macro Headwinds For Fintech

- Following weakening performance and a poor takeover attempt, PayPal's shares have plummeted over 50%.

- Macro conditions are deteriorating and we feel they are bearish for PayPal, the business is not in a position to take advantage.

- The financials are good and long term the business will be fine, but management do not give us confidence in their ability.

- The valuation means we are not rating the stock a sell, it has been heavily beaten down and is now about right.

Investment thesis

PayPal (PYPL) has been quietly growing well and generating great free cash flow but in Q4-22 things changed. Since then, the stock has fallen sharply and sentiment around the business has changed sharply. The share price looks to have stabilized and so it is a great time for us to assess the business.

We will look at PayPal mainly from a macroeconomic perspective, to consider how PayPal will perform during the tough times ahead. We are not a fan of recent decisions by management and have found many issues with past decisions. We still feel there are areas to exploit in the Fintech space and PayPal from a financial perspective is in a good place to take advantage.

Company description

PayPal is a global financial technology (Fintech) business which specializes in online payments, payment processing and money transfers. PayPal initially listed all the way back in 2002 but was quickly taken over by eBay, who subsequently spun the business off in 2015 .

The PayPal group has 11 businesses, including Venmo (a payments business popular among young people), Zettle (PoS payment system) and Honey (Browser extension).

PayPal was a market favorite, at one point reaching 750% returns since its spin-off from eBay. Since then, however, the stock has fallen 76% and is attracting criticism from many.

The reason for the fall is complicated. Unlike many stocks, it was not due solely to the economic factors which have driven most of the market down. As the below graph shows, PayPal began trading sideways in Q2 2021 before falling quite aggressively in Q4. Contrast this with the S&P 500 which was shaky in Q4 and fell harshly for the first time in 2022.

Firstly, PayPal attempted a bizarre takeover of Pinterest ( PINS ), which many investors could not rationalize either (Purchase price was allegedly $45BN, PINS is currently trading at $13BN). Secondly, Fintech businesses began to post shaky results, with the sign of things potentially slowing . At the time, it was attributed to the Omicron variant. Looking back however, after a quarter of negative US GDP growth , it was likely the beginning of weakening consumer spending.

After cratering to c.$80-a-share, we will now consider if this is now when PayPal will reverse course, or if more pain is to come.

Macroeconomic conditions

As a (predominantly) payment-driven business, PayPal is highly sensitive to economic conditions. When things are good, more money is exchanged and so PayPal generates greater fees for its services and vice versa. Economic conditions are however complex, they are rarely just 'good' and 'bad'. We will thus dissect each major aspect we feel appropriate and consider the short-to-medium term impact on PayPal.

Inflation

Inflation is driving prices of all things up, with US inflation at 8.6%. In theory, this would be good for PayPal as it earns a fee on the transaction amount. This being said, life is not so simple. We are seeing demand cooling due to a deterioration in people's income, as necessities are increasing in cost faster than wage growth. Energy being one of the key examples. This results in less discretionary income available for spending online, the area in which PayPal operates. People do not really pay their bills or groceries with PayPal which is why the business cannot benefit from this. The impact on PayPal has been a dip in performance during Q1 2022. The number of payment transactions fell 3.4% and their take-rate fell 0.03%. Mastercard ( MA ) by contrast saw flat revenue growth in Q1 2022 . With inflation unabating, it is not out of the question that we see further deterioration in payment transactions.

Interest rates

With interest rates increasing around the globe, interest-bearing services can now earn greater returns, depending on how the funds are sourced. This is good news for PayPal as they have launched a range of credit services in the last few years, including credit cards and buy-now-pay-later services. The risk here is protecting the downside, as delinquencies may increase if interest becomes overbearing. PayPal's credit loss rate increased 1 bps in Q1-22 which is clearly not material yet, but we should keep an eye on how this develops into H2 2022.

Consumer Sentiment/Confidence/Spending

There are many data sources which could be seen as leading indicators for a change in economic conditions, one we like to look at is consumer sentiment. The reason for this is that we are all acting in our selfish best interest, based on the knowledge and feelings we have. If we expect times to worsen, we will act accordingly to protect ourselves.

Survey of Consumers (Uni of Michigan)

As the table above shows, there has been a sharp deterioration since June and is still falling further since May 2022. We note the following quotes from the report:

About 79% of consumers expected bad times in the year ahead for business conditions, the highest since 2009.

Inflation continued to be of paramount concern to consumers; 47% of consumers blamed inflation for eroding their living standards, just one point shy of the all-time high last reached during the Great Recession

It is clear that many are fearing worsening conditions and site inflation to be a key problem. We have already established that this is sucking spending away from PayPal and so we think this is a serious issue for the business.

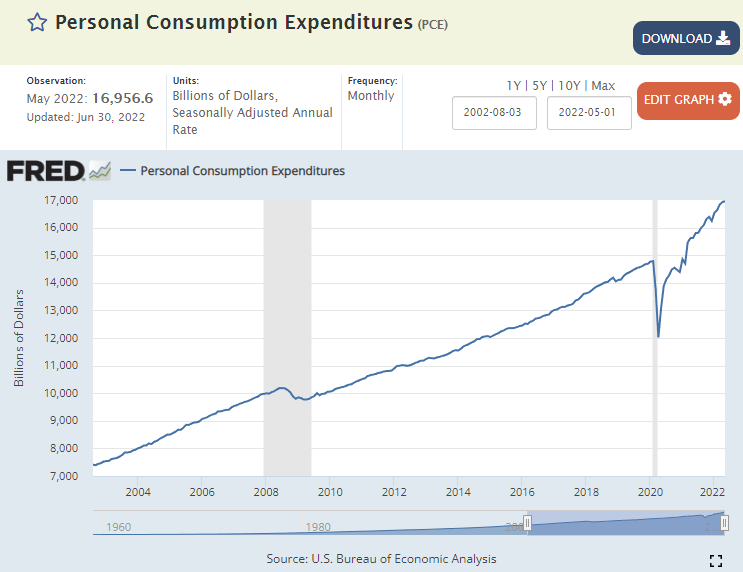

To provide a counter argument, personal consumption remains strong. Although this indicator is less valuable for predicting short-term trend changes, it is showing that the economy is not weak by any stretch.

Personal Consumption Expenditures ((FRED))

{kind=link}

GDP growth

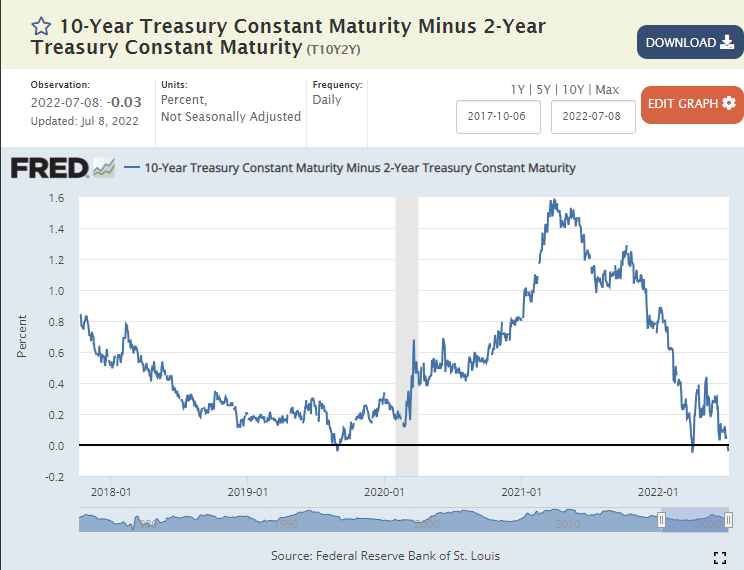

It is no secret that GDP growth is beginning to slow quite considerably. This is driven by many factors, inflation and consumer behavior being two of them. Our concern is that we are not seeing any bullish signals yet, just some evidence to suggest things are not as bad as some are making it out to be. The M&A market remains strong and personal consumption has yet to dip. This said, you cannot fight sentiment. Goldman Sachs ( GS ) are attributing a high chance to a recession by 2024, JPMorgan ( JPM ) also and even CFOs . This could be a self-fulfilling prophecy or it could be that they also do not see anything causing a bounce back from this slow decline we are experiencing. Our belief is that a recession will come and with 2 recent inversions in the yield curve, this is slowly feeling like a certainty. The yield curve is seen as a leading indicator for a recession, and is the difference in the yield between a long dated and short dated bond. The intention is to show the confidence within the market. If the yield of long-dated bonds fall, it is because investors are piling money into them, likely due to fears around the near term.

{kind=link}

Disrupting and being disrupted

The payments industry is at a funny crossroads currently, it is both disrupting and being disrupted.

Disruption

Payment companies, including PayPal, have caused much disruption to the traditional players as they have targeted younger audiences and improved upon archaic technologies. For example, one would think that sending money between two people's bank accounts should be extremely easy for the Bank's to organize and yet Venmo and Cash App ( SQ ) have exploded into prominence to offer such a service. The same is the case for being a payment facilitator, PayPal has been providing consumers a way of paying for things online easily and safely and that is not going to change. The disruption has occurred and the innovation is already in place, it is unlikely that many will attempt to join the market for a c.2% take-rate, the market is PayPal's and it is not worth trying to get in.

Disrupting

On the other end of the scale, the market is being disrupted by the emergence of buy-now-pay-later businesses. Those include Klarna, Affirm ( AFRM ) and Afterpay ( AFTPF ). These businesses allow consumers to buy an item through their services and pay for them on a monthly basis. In many countries, these businesses have managed to avoid credit regulations and so these "loans" do not hit an individual's credit history. PayPal has been late to joining this market but is also a service it offers. For those who can afford it, these services have allowed them to bring forward consumption, but the reality has left many with debt they cannot service. Similar to the boom in pay-day loans a decade earlier.

A third of UK 'buy now, pay later' users say they can't handle payments.

In Indonesia , 'pay later' services leave some drowning in debt.

It is likely that regulation will quickly move to stop these businesses from operating as they are, the UK is already far down this process and many more may follow. This is bad news for PayPal's credit business but the reality is it is probably a net benefit as these other businesses were infinitely larger than PayPal in this space and so were taking business from PayPal's core business.

Financials

PayPal recently announced its Q1 2022 financial performance and we note the following highlights:

| Q4'20 - Q1'21 change |

| Q1'21 - Q1'20 change |

| Active Accounts |

| -0.7% |

| 14% |

| New Active Accounts |

| -76% |

| -83% |

| No. of Payment Transactions |

| -3% |

| 18% |

| Take Rate |

| -0.03% |

| -0.1% |

| Transaction Margin |

| -1.4% |

| -6.9% |

| Source: |

| Q1-22 Deck |

What we see is a general decay in the business. Much of this has happened in the last quarter but it is certainly a continuing trend since 2020. The impact on the bottom line is a 6.9% fall in transaction margin over the course of a year. This is far too high for an established business such as PayPal. What is most concerning for us however, and what has spooked many investors, is the new active accounts. This has remained above 9M since Q2'18 and has only been below 5M once since 2017 (Source: PayPal's historic investor decks). This is nothing short of a disaster. We are struggling to rationalize why it has fallen by such an extreme amount. Even when some retail markets struggled in 2017, new customers did not fall by such an amount. If PayPal is no longer growing at such a rate, we really struggle to see how the business will grow. It cannot increase its take rate and can only bolt-on so many types of Fintech businesses. The first thing investors should do when the Q2 numbers are released is see what they have achieved.

M&A/Organic expansion

The reality is that the payments business is slowing and it is likely PayPal's management knew this when they attempted the takeover of Pinterest. Although the choice of response to their reality was not good, they acted along the correct lines. They do need to expand beyond their core operations. They have been launching new services constantly as the following shows.

PayPal new services (Q1 22 Deck)

We have an issue with this however, nothing is really working at a large scale. Yes they are winning customers, yes they are generating more profits, but these endeavors are probably not enough if payments start slowing aggressively. We see this in the ROCE, which has fallen from 22.8% in 2020 to 17.9% in 2022 (Source: Tikr Terminal). A perfect example of this is their Crypto services, they completely missed the boat (It was very obvious in 2017 that Crypto was going to be something revolutionary). The reality is, we do not have confidence in management to execute a growth strategy beyond payments.

The good

PayPal is not all bad, far from it. The business has a very impressive 7.4% FCF Margin and an EBITDA margin of 17.1% (Source: Tikr Terminal). It is a cash flow monster objectively, but at its current price, the yield is impressive. This can be returned in part to shareholders through buybacks, but also used to reinvest and improve the business.

Further, as Terry Smith and Charlie Munger like to say, in the long-term a stock can only generate returns in line with its ROCE. At a level of 17.9%, investors can still make a handsome return, should PayPal allocate resources appropriately (a big if!).

Finally, with a debt/equity ratio of 48.7%, PayPal has the capacity to invest heavily. This is not a large bloated business that is chugging along with no ability to pivot. The onus is on management to allocate resources effectively and turn this business around.

Valuation

PayPal's valuation is very attractive. It is trading at a 14.75x NTM EV/EBITDA multiple v. its historic average of 27.12x (Source: Tikr Terminal). This suggests it could double, if they can return to their relative market position historically. However, that is far from easy. With new customers growing at an average of just under 10M, PayPal is currently far from there. Additionally, they have significantly more competition than they did historically. Zelle, for example, is owned by several of the world's largest Banks. It is too early to know where PayPal is currently positioned until we get a few more quarters of information, but our belief is that the business will normalize in the region of 11x-17x in the short-term, with the potential for c.20x in the medium-term once things pick up.

Final thoughts

PayPal is not a bad business but it has had a bad quarter. Markets have naturally taken this as PayPal's new reality and is pricing in little-to-no growth. Although markets overreact a lot, we certainly understand this uncertainty from a macro perspective. Our belief is that PayPal will continue to struggle in the coming quarters.

The payment space is getting very competitive and so far, PayPal has not shown the ability to innovate. We are not giving up on the business but management certainly needs to refine its strategy.

Given the valuation of the business, we are not assigning a sell rating. It has fallen so sharply that we believe it is in and around its fair value. If it were to fall by 10% tomorrow, we would not be surprised but at a FCF% of 7.4%, PayPal is earning a nice return. Investors should be warned however, when/if the recession comes, a demand-driven business like PayPal will take a hit.

For further details see:

PayPal: Macro Headwinds For Fintech