PDSB - PDS Biotechnology: PDS0101 Being Put To The Test

2023-11-01 04:02:35 ET

Summary

- PDSB provided updated interim data from its Versatile-002 study of PDS0101 in early October. While the survival data are strong, there were no responses in checkpoint inhibitor-refractory patients.

- Versatile-003 is set to get underway in Q4'23. The trial will put PDS0101 to the test, comparing it in combination with MRK's Keytruda, to Keytruda alone.

- Completion of Versatile-003 might seem like a while away, but interim analyses provide a possibility of early success.

PDS Biotechnology Corporation ( PDSB ) is getting underway with a phase 3 trial of its drug, PDS0101, in human papilloma virus 16 (HPV16)-positive head and neck squamous cell cancer (HNSCC). This trial, called Versatile-003, will compare PDS0101 Merck's ( MRK ) Keytruda (pembrolizumab), to Keytruda alone. The phase 3 thus allows PDS0101, which has looked promising in HNSCC, albeit by cross trial comparison, to show what benefit it actually offers. This article takes a look.

Figure 1: PDSB is down over 60% year-to-date.

Updated VERSATILE-002 interim data

Providing the rationale for PDSB's Versatile-003, is the phase 2 trial Versatile-002. Versatile-002 is a trial of PDSB's PDS0101, with MRK's Keytruda, in HPV16 positive HNSCC. PDS0101 itself is a vaccine that uses a lipid nanoparticle containing HPV neoantigens, to provoke an immune response against these HPV neoantigens, which should be useful in helping a patient immune system attack their HPV-positive cancer. While PDSB has provided encouraging data from the trial before, on October 3, 2023, PDSB provided updated interim data from Versatile-002.

Checkpoint inhibitor-naïve patients

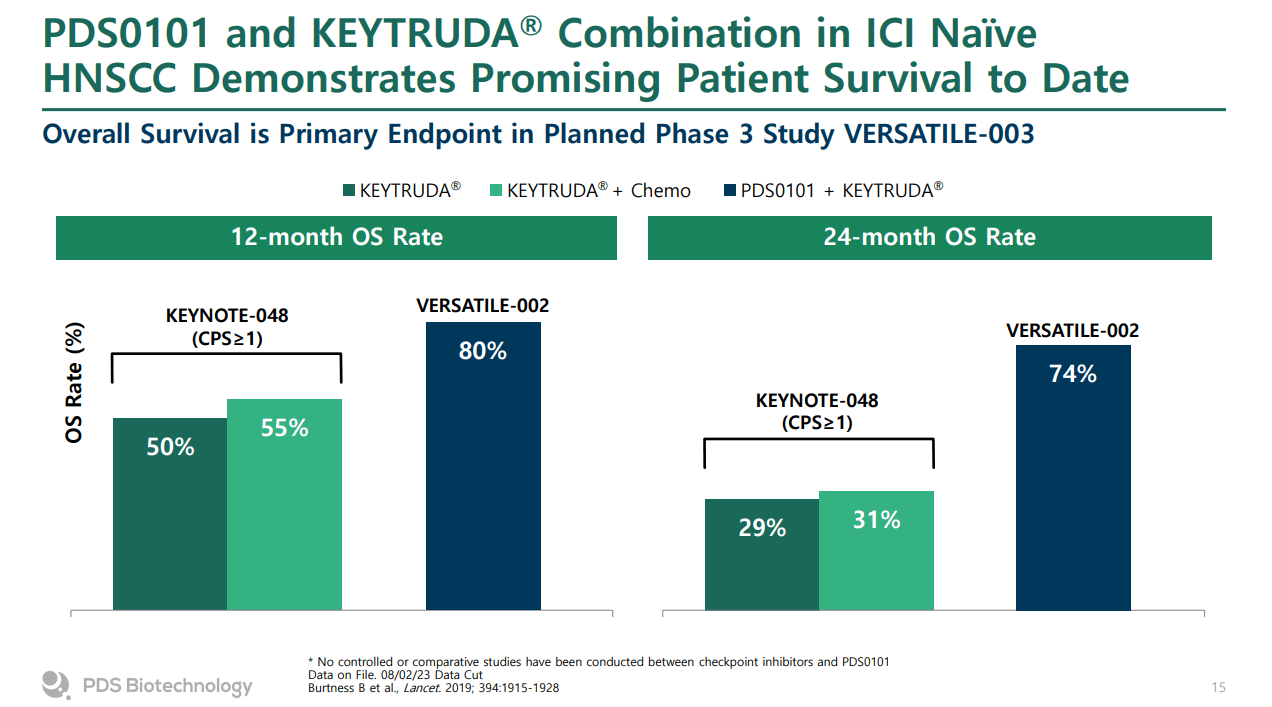

On the efficacy front, PDS0101 plus Keytruda produced compelling numbers in patients who had not previously been treated with a checkpoint inhibitor ((ICI)), such as MRK's Keytruda. A survival rate of 74% at 24 months, in patients treated with PDS0101 plus Keytruda, compares favorably to a literature value of less than 30% for approved checkpoint inhibitors.

Figure 2: Updated interim data from the checkpoint inhibitor (ICI) naive group in PDSB's Versatile-002 study. Note green columns represent literature values for comparison, not data from Versatile-002. (PDSB Corporate Presentation, October 2023.)

{kind=link}

The overall response rate (ORR; complete responses + partial responses) was 13/52 patients.

Checkpoint inhibitor refractory patients

In another cohort of patients in Versatile-002, patients who were refractory to a checkpoint inhibitor, the results were less clear - there were no confirmed responses (ORR = 0/21 patients). The 12 month survival rate of 56% however, compares favorably to a published value of 17% at 12 months for patients who have progressed on a checkpoint inhibitor and are not treated with salvage chemotherapy. PDSB did sell off during the day on October 3, with the updated interim data, so that explanation seems to only have been so satisfying to the market.

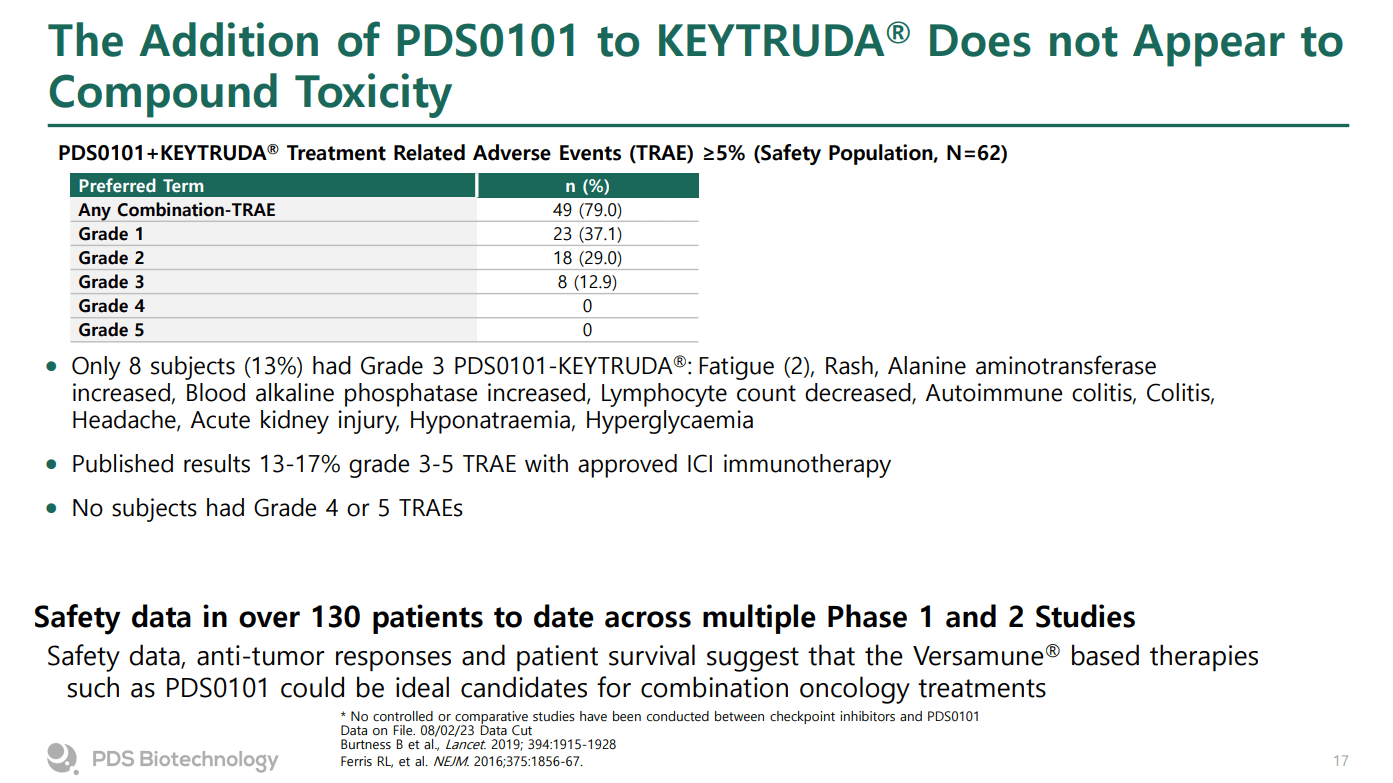

Results from Versatile-002 are compelling on the safety front. If PDS0101 offers even slightly better efficacy than Keytruda alone, it would likely be worth taking due to the fact that the rate of grade 3 adverse events doesn't seem to increase much adding PDS0101 into the mix.

Figure 3: Overview of adverse event data from Versatile-002. (PDSB Corporate Presentation, October 2023.)

{kind=link}

VERSATILE-003

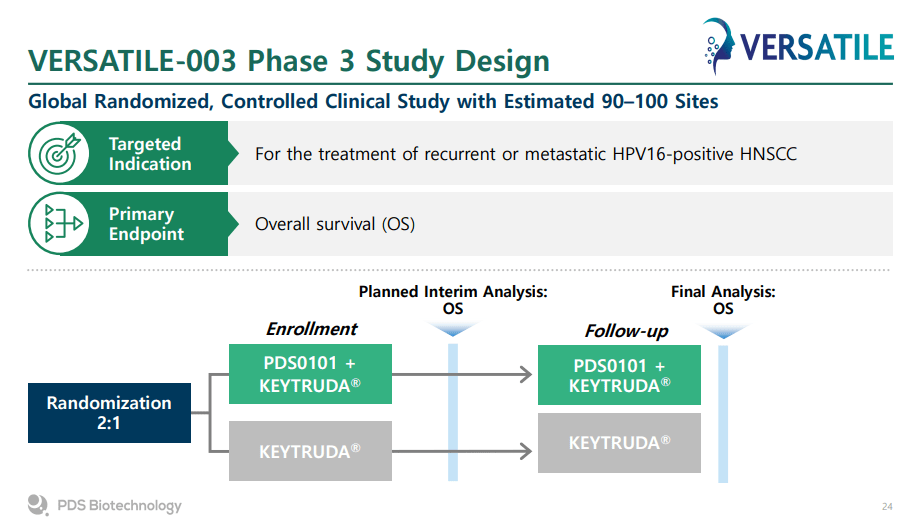

PDSB plans to initiate a phase 3 study of PDS0101 with Keytruda in HPV16 positive HNSCC, called Versatile-003, in Q4'23. That study could produce data allowing marketing approval. Importantly, the design of the trial will avoid the literature comparisons we've been engaging in up to now, so it will be obvious if PDS0101 is actually adding benefit to Keytruda.

Figure 4: Study design of Versatile-003. (PDSB Corporate Presentation, October 2023.)

{kind=link}

Financial Overview

PDSB had cash and cash equivalents of $60.6M as of June 30, 2023. R&D expenses were $8M in Q2'23 and G&A expenses were $4.7M in Q2'23. PDSB has $23.3M outstanding on its financing agreement with Horizon Technology Finance Corporation, with payments on the principal to begin in October, 2024. Net loss for Q2'23 was $11.5M and net cash used in operating activities was $18M in the first six months of 2023. At this rate then, has cash runway for 20 months from the end of Q2'23, or until February 2025. Cash burn should pick up however with the Versatile-003 trial getting underway while Versatile-002 is still ongoing. Indeed PDSB has only stated that its cash resources should be sufficient for 12 months from the end of Q2'23.

PDSB had 30,868,188 shares outstanding as of August 7, 2023, corresponding to a market cap of $124.1M. It should be noted as of June 30, 2023, there were 5,324,402 options to purchase PDSB's common stock outstanding (weighted average exercise price of $6.85) and 506,229 warrants.

Other shots on goal

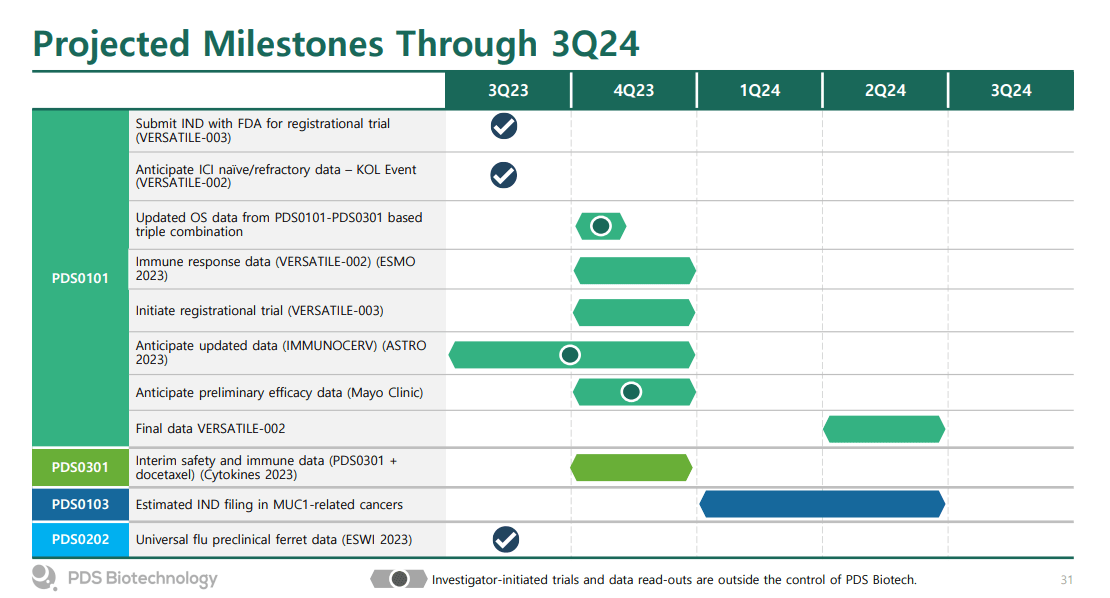

Looking at PDSB's catalyst slide allows us to see if there is anything on tap near-term that could move the stock.

Figure 5: PDSB anticipated milestones. (PDSB Corporate Presentation, October 2023.)

{kind=link}

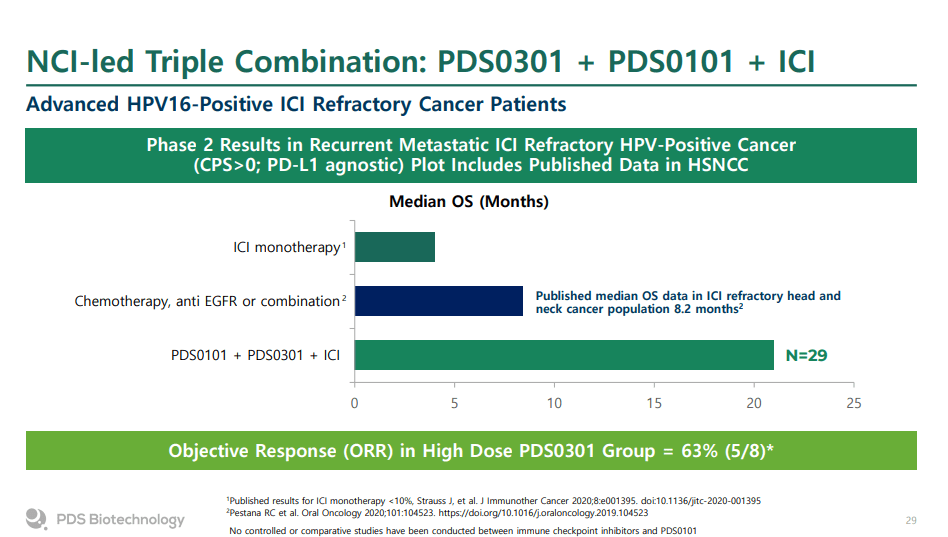

Firstly, PDSB is also developing PDS0301, which is a tumor targeting form of IL-12, that aids T cell function in the tumor microenvironment. The agent, in combination with PDS0101 and a checkpoint inhibitor has produced impressive data, at least in terms of comparison to historical data, in a National Cancer Institute ((NCI))-led study of various HPV16-positive cancers refractory to a checkpoint inhibitor.

Figure 6: Results from a trial of a triple combination of a checkpoint inhibitor with PDS0101 and PDS0301. Note comparisons to other therapies are cross-trial comparisons. (PDSB Corporate Presentation, October 2023.)

{kind=link}

The efficacy of PDS0101 in that trial however, isn't clear because the combination of a checkpoint inhibitor, PDS0101 and PDS0301, might only be working due to one of those drugs (PDS0101 or PDS0301) allowing checkpoint inhibitor refractory patients to respond again to therapy. As such even if additional data from this NCI-trial, expected in Q4'23, is positive, it still won't tell us if PDS0101 is an active cancer therapeutic and will work in the Versatile-003 study. I don't think updated data has the potential to move the stock hugely, because the high dose group already reported strong data (ORR of 63%) and the design of the trial doesn't seem to be aimed at looking what PDS0101 and PDS0301 are contributing.

What could be more useful is data from a Mayo Clinic-led study of PDS0101, that study looks at pre-metastatic HPV-positive oropharyngeal cancer. The trial includes an arm with PDS0101 monotherapy and also an arm with Keytruda plus PDS0101. The trial doesn't include an arm of Keytruda alone however, which is what would really allow us to make some conclusions on the efficacy of PDS0101. Nonetheless responses to PDS0101 monotherapy prior to surgery (study treatment is administered prior to transoral robotic surgery) could provide another hint that PDS0101 itself is an active anti-cancer agent, and the results seen in trials like Versatile-002 aren't just a lucky result in terms of comparison to literature values.

Conclusions

PDSB estimates that HPV16-positive HNSCC is a $2B-$3B market opportunity in the US alone. Even if peak sales were $1B, a biotech being bought out for a few times peak sales isn't unheard of, so PDSB trading with an enterprise value of $87M currently makes the name seem fairly cheap. To be fair, the share count is probably going to have to increase, because PDSB guiding for 12 months cash might not be enough to make it to a positive interim result from Versatile-003. There is the possibility of PDSB doing a non-dilutive deal, partnering one of its other pipeline members, but that is an uncertainty.

Right now I rate PDSB a hold. I think PDS0101 didn't just look good in the Versatile-002 trial due to a favorable set of patients, I think the drug is going to succeed in Versatile-003, but the share price is sliding and an interim readout from Versatile-003 isn't coming in Q4'23. I view updates from other catalysts like investigator-led trials, at least the near-term updates, to be unlikely to cause a huge move.

I also think PDSB could issue more shares to raise some cash soon, to help the company get further into 2024 and potential interim analyses from Versatile-003. That potential raise represents a near-term risk to the share price. Beyond that, if PDS0101 doesn't look special as monotherapy in the Mayo clinic-led study, it could lead to doubts about the efficacy of the drug, causing further selling. I'll revisit the PDSB thesis and potentially revise my rating as we get updates from the investigator-led trials, the timing of potential Versatile-003 interims, and updates on PDSB's cash situation.

For further details see:

PDS Biotechnology: PDS0101 Being Put To The Test