PDSB - PDS Biotechnology's PDS0101 Shows Potential In HPV-Positive Head And Neck Cancers

2023-04-05 06:57:49 ET

Summary

- PDS0101, an innovative immunotherapy, targets HPV-positive cancers, including recurrent or metastatic head and neck cancer with high-risk HPV16 infection.

- VERSATILE-002 Phase 2 clinical trial demonstrates improved efficacy and a favorable safety profile compared to historical data for this patient population.

- A combination of PDS0101 and KEYTRUDA shows a response rate of 41.2%, more than double the 19% observed with approved ICI monotherapy.

- The upcoming VERSATILE-003 Phase 3 clinical trial aims to provide further insight into the combination therapy's efficacy and safety.

- My recommendation for PDS Biotechnology is to view it as a "Buy" option, though as a speculative, high-risk investment within a well-diversified portfolio.

Introduction

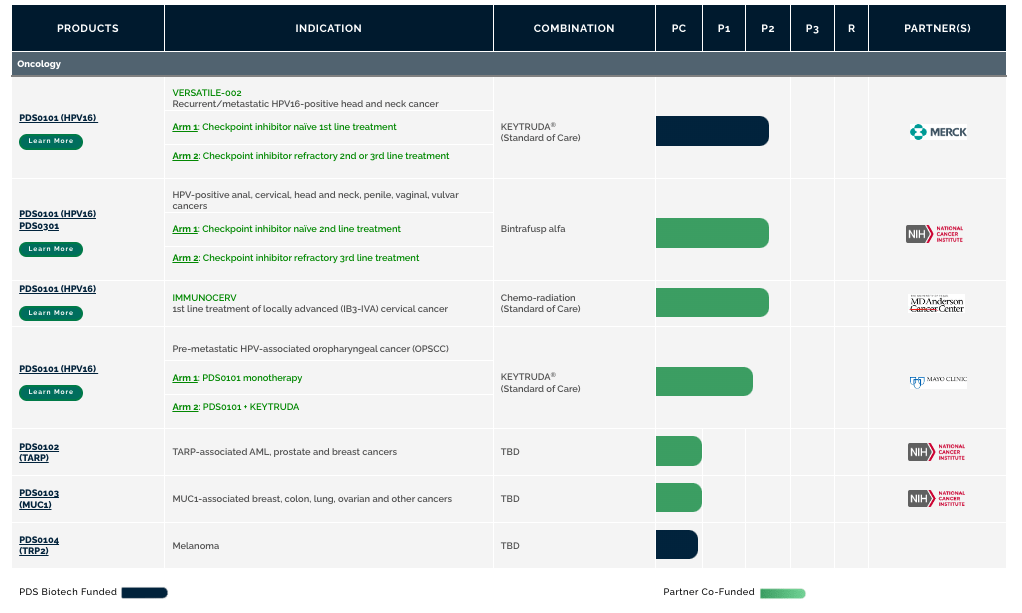

PDS Biotechnology ( PDSB ) is a biotech company that focuses on developing immunotherapies for targeted cancer and infectious diseases. The company uses its proprietary technology platforms, including Versamune, Versamune plus IL-12, and Infectimune, to create T cell activating therapies. These therapies induce large amounts of potent CD4 helper and CD8 killer T cells in vivo, potentially overcoming the limitations of current immunotherapies. PDS Biotech combines Versamune with disease-specific antigens to design these therapies, enabling the immune system to recognize and eliminate diseased cells. The company's pipeline targets various cancers, including HPV-positive cancers and common forms like breast, colon, lung, prostate, and ovarian cancers. Additionally, Infectimune-based vaccines can produce durable neutralizing antibody responses and potent T cell responses, making them suitable for universal influenza vaccine applications.

PDS Biotech pipeline (PDS Biotechnology)

{kind=link}

Recent events: A National Cancer Institute-led Phase 2 trial for advanced HPV-positive cancers is also underway, and a successful meeting with the FDA discussed the regulatory pathway for a triple combination therapy. The reported median overall survival was 21 months for advanced, immune checkpoint inhibitor [ICI] refractory HPV-positive cancer patients. Additionally, the IMMUNOCERV Phase 2 trial of PDS0101 with chemoradiotherapy showed a 100% clinical response and 89% complete response in locally advanced cervical cancer patients.

The following article will ruminate on PDS0101 for the treatment of recurrent or metastatic head and neck cancer with high-risk HPV16 infection.

Financials

In 2022, PDS Biotech experienced a net loss of roughly $40.9 million ($1.43 per share), a significant increase from the $16.9 million net loss ($0.66 per share) in 2021. This higher net loss is primarily due to investments in research and development, clinical programs, and the acquisition of PDS0301. R&D expenses rose to about $29.4 million in 2022, compared to $11.3 million in 2021, with the majority of the increase attributed to personnel costs, clinical costs, quality and manufacturing costs, and the $10 million acquisition of PDS0301 rights from Merck KGaA. General and administrative expenses also increased to roughly $12.2 million in 2022, up from $10.2 million in 2021, mainly due to higher personnel costs and professional fees. Total operating expenses reached approximately $41.7 million in 2022, a 94% increase from the previous year's $21.4 million. As of December 31, 2022, the company had a cash balance of $73.8 million, which is projected to fund operations and R&D programs until the third quarter of 2024, considering the anticipated initiation of a registrational trial in 2023.

The Growing Concern of HPV-Positive Head and Neck Cancers: Understanding Prevalence, Risk Factors, and Treatment Options

Despite vaccination efforts, HPV-positive head and neck cancers, especially oropharyngeal cancers, are a growing concern due to their increasing prevalence in recent years. According to the CDC, around 70% of oropharyngeal cancers are caused by high-risk HPV strains, with HPV16 being the most common. The prevalence of recurrent or metastatic head and neck cancer with high-risk HPV16 infection is influenced by various factors such as stage at diagnosis, treatment modalities, and patient demographics.

Treatment options for HPV-positive head and neck cancer depend on the stage and location of the tumor, as well as the patient's overall health. Common treatment modalities include:

- Surgery: Surgical removal of the tumor, sometimes along with the surrounding tissue, is often the first step in treating head and neck cancers.

- Radiation therapy: High-energy rays or particles are used to destroy cancer cells. This can be administered as external beam radiation therapy, intensity-modulated radiation therapy (IMRT), or brachytherapy.

- Chemotherapy: Systemic treatment using drugs to kill cancer cells or stop their growth. Chemotherapy can be administered alone or in combination with radiation therapy (chemoradiation).

- Immunotherapy: A type of treatment that utilizes the patient's immune system to fight cancer. For example, immune checkpoint inhibitors such as pembrolizumab (Keytruda) or nivolumab (Opdivo) can be used to treat advanced or recurrent head and neck cancers.

- Targeted therapy: Drugs that specifically target cancer cells or their environment, with less harm to healthy cells. Cetuximab (Erbitux) is a targeted therapy used for head and neck cancers.

PDS0101: A Promising Immunotherapy for HPV-Positive Cancers with Enhanced Efficacy and Favorable Safety Profile

PDS0101 is an innovative molecularly targeted immunotherapy designed to treat HPV-positive cancers. It is based on an enantiospecific cationic lipid nanoparticle platform containing HPV16 neoantigens. This therapy works in conjunction with checkpoint inhibitors (CPIs) to enhance anti-tumor activity. PDS0101 achieves this by increasing the production of Type I interferons and promoting antigen processing and cross-presentation. As a result, the therapy generates high levels of polyfunctional HPV16-specific CD8 and CD4 T cells in vivo, as well as fostering immune memory.

The data from the VERSATILE-002 Phase 2 clinical trial shows promising results compared to historical data for patients with recurrent or metastatic head and neck cancer and high-risk HPV16 infection. The trial evaluates the combination of PDS0101 and Keytruda (pembrolizumab) as a first-line treatment for these patients.

According to management, the response rate (tumor shrinkage greater than 30%) of 41.2% is more than double the 19% observed with approved ICI monotherapy, indicating a potentially significant improvement in treatment effectiveness. Additionally, clinical efficacy, which includes both ORR and stable disease, was observed in 76.5% of patients, demonstrating that a majority of patients experienced positive outcomes with this combination therapy.

Furthermore, the safety profile of the treatment is notable, with no treatment-related adverse events greater than or equal to Grade 3 reported (n=19). This suggests that the combination of PDS0101 and Keytruda could provide a more tolerable treatment option for patients with recurrent or metastatic head and neck cancer and high-risk HPV16 infection.

Lastly, the 9-month follow-up data (n=17) showed a progression-free survival rate of 55.2% and an overall survival rate of 87.2%. These figures, although preliminary, suggest that the combination therapy may offer improved survival outcomes for this patient population when compared to historical data.

The data from the VERSATILE-002 Phase 2 clinical trial presents promising results for patients with recurrent or metastatic head and neck cancer and high-risk HPV16 infection. The reported response rate and clinical efficacy suggest an improvement in treatment effectiveness, and the safety profile appears favorable. However, it is important to note that the data is preliminary and subject to further analysis. The trial's sample size is relatively small, and the results may not be representative of the broader patient population.

This year, the company anticipates a Phase 3 clinical trial called VERSATILE-003 will be initiated, building on the data from the ongoing VERSATILE-002 trial. The new randomized, controlled trial will investigate the combination of PDS0101 and Keytruda compared to Keytruda alone in ICI-naïve patients with recurrent or metastatic HPV16-positive head and neck cancer.

My Analysis & Recommendation

In conclusion, PDS Biotechnology has shown promise in its development of PDS0101, an innovative immunotherapy designed to treat HPV-positive cancers. The VERSATILE-002 Phase 2 clinical trial results indicate a potentially significant improvement in treatment effectiveness for patients with recurrent or metastatic head and neck cancer and high-risk HPV16 infection, as well as a favorable safety profile. While these preliminary results are encouraging, it is important to await the completion of the trial and further data analysis for definitive conclusions.

Investors should closely monitor the progress of PDS Biotechnology's pipeline, particularly the upcoming VERSATILE-003 Phase 3 clinical trial, which may provide more insight into the combination therapy's efficacy and safety. It is worth noting that the company's cash balance of $73.8 million is expected to fund operations and R&D programs until the third quarter of 2024, which provides a stable financial foundation for the company to continue its research endeavors.

Based on the current data, PDS Biotechnology appears to be a potentially attractive investment opportunity for investors with a high risk tolerance and a long-term investment horizon, considering the inherent uncertainties and lengthy timelines associated with clinical-stage biotech companies. Investors should keep in mind the risks involved and carefully weigh the potential rewards against the uncertainties before making any investment decisions. My recommendation for PDS Biotechnology is to view it as a "Buy" option, though only as a speculative, high-risk investment within a well-diversified portfolio.

Risks to Thesis

"When the facts change, I change my mind." - Paul Samuelson

While my article presents a bullish thesis for PDS Biotechnology, there are several risks that investors should consider:

- Clinical trial delays: Various factors can lead to delays in clinical trials, which in turn can impact the development and approval of therapies like PDS0101. Delays can occur due to issues with patient enrollment, manufacturing or supply chain problems, unexpected adverse events, or changes in regulatory requirements. These delays can result in increased costs, prolonged timelines, and jeopardize the chances of a therapy reaching the market.

- Clinical trial failures: Clinical trials carry inherent risks, and there is no guarantee that PDS0101 or other pipeline products will demonstrate the efficacy and safety required for regulatory approval. Failure in clinical trials can lead to substantial financial losses and damage the company's reputation.

- Regulatory hurdles: Even if clinical trials are successful, PDS Biotechnology may face challenges in obtaining regulatory approvals from agencies such as the FDA. Delays or rejections in the approval process can negatively impact the company's prospects and financial position.

- Improved vaccination efforts: The market for HPV-associated cancer treatments may shrink if vaccination efforts, particularly among men, become more successful. Widespread adoption of HPV vaccines can potentially reduce the prevalence of HPV infections and subsequently decrease the number of HPV-positive cancers. This reduction in the patient population may impact the demand for therapies like PDS0101, resulting in a smaller market and affecting the revenue and growth potential for PDS Biotechnology.

- Competition: PDS Biotechnology faces competition from other biotech and pharmaceutical companies working on similar immunotherapies and treatments for HPV-positive cancers. New or improved treatments entering the market can reduce the demand for PDS Biotechnology's products, impacting the company's revenue and growth potential.

- Market adoption: If PDS Biotechnology's products receive regulatory approval, there is no guarantee that they will gain widespread market adoption. Factors such as pricing, reimbursement policies, and physician and patient preferences can influence the commercial success of the company's products.

- Intellectual property risks: PDS Biotechnology relies on patents and other intellectual property protections to maintain a competitive advantage. The company may face challenges in obtaining or maintaining these protections, or they may become involved in costly legal disputes to defend their intellectual property rights.

- Financial risks: PDS Biotechnology is a clinical-stage company with a history of net losses. The company's ability to continue its research and development efforts depends on its ability to secure additional funding, either through equity or debt financing, partnerships, or other means. There is a risk that the company may not be able to obtain the necessary funding, which could impact its operations and growth potential.

For further details see:

PDS Biotechnology's PDS0101 Shows Potential In HPV-Positive Head And Neck Cancers