S - Peabody Energy: Shareholder Returns Should Ultimately Follow At These Prices

Summary

- Peabody Energy is one of the cheapest coal producers out there.

- It's trading at very low multiples, although coal prices and earnings are likely not sustainable in the long term.

- One of the reasons for its low valuation are restrictions to buybacks and dividends.

- As earnings hang in there, these restrictions should be able to be eased and ultimately disappear.

- At that point Peabody should look quite enticing to investors willing to venture into this hated sector.

In a bearish energy tape, Peabody Energy ( BTU ) fell nearly 10% yesterday . A good time to revisit a company I've found to be one of the cheaper coal producers. The company is now trading at a share price that translates into a ~$3.5 billion market cap and similar enterprise value. Shortly after my previous update, the company reported earnings of $2.81 per share, quarterly free cash flow of $340 million, and adjusted EBITDA of 578 million. A free cash flow multiple of 10x or an EV/EBITDA of 6x are OK, but they're astounding given these are quarterly figures. The company is using the current windfall to reduce debt. Here's what CEO Grech said about the global outlook for coal:

Now turning to global coal markets - across the globe, all coal price indices remain at elevated levels, representing a dynamic demand that continues to test the ability of supply in most of our market segments. The outlook for all our operating segments continue to be favorable with the constrained base serving a market that is reallocating the scarce availability of coal. Seaborne coal markets are currently facing disruption resulting from the Russia-Ukraine conflict. Our coal supply in Australia continues to be challenged by weather and staff absenteeism primarily as a result of continued COVID impacts.

How are things holding up fast-forward a couple of months. Well, just a few days ago, peer Whitehaven reported earnings and it turns out prices and the outlook are still quite favorable:

Whitehaven chief executive officer Paul Flynn said the longer-term under-investment in energy sources needed to supply baseload capacity to growing populations and economies had contributed to a widening gap between supply and demand.

“In FY22, we saw global energy shortages intensify as a result of the tragic conflict in Ukraine and associated sanctions against Russian coal and gas,” he said.

“Coal prices are at record levels and customers are focused on energy security now more than ever before. We have worked hard to position ourselves to maximize the opportunity arising from historically high prices.

On Aug. 11 the European ban on Russian coal went into effect, which is likely favorable to all non-Russian producers. Overall, prices appear to hang in there across the globe. This is especially true for thermal coal which is a rare occurrence. Peabody has exposure to both and benefits as long as coal prices are strong.

The U.S.-based LNG export facility Freeport should return to service in mid November . That will help Europe with its energy needs and may be beneficial to U.S. producers of coal and gas as prices should move somewhat in the direction of European price levels.

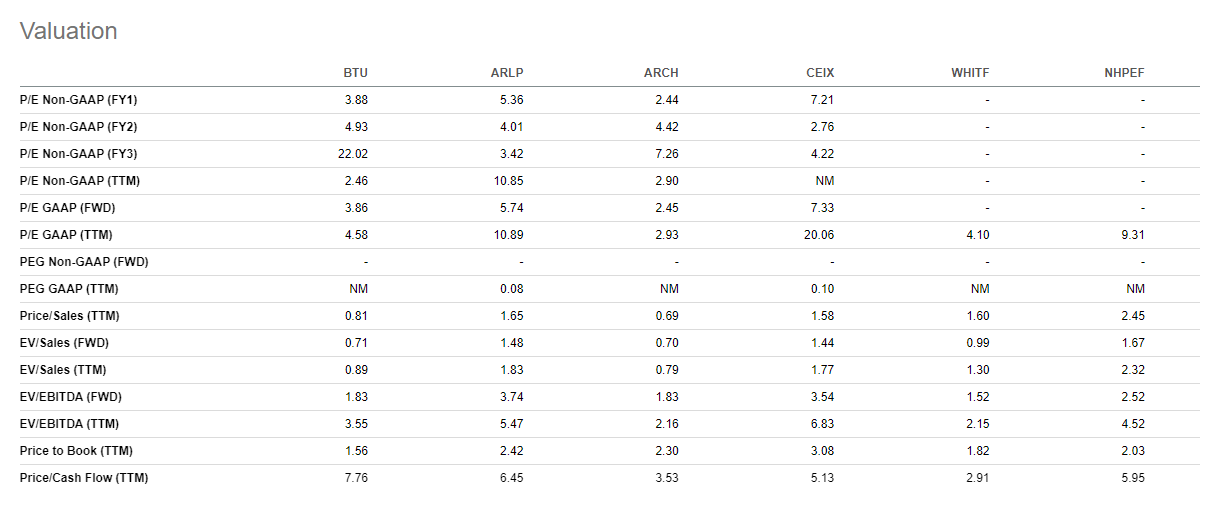

I pulled up valuations on Seeking Alpha for several peers, including Alliance Resource Partners ( ARLP ), Arch Resources ( ARCH ) and Whitehaven Coal (WHITF), among others.

{kind=link}

BTU continues to trade on the lower end of the range for this peer group. In particular, it trades at 1.83x forward EBITDA, 3.6x forward P/E and 1.56x book. Generally speaking, the valuations seem too low given the current profitability and outlook. This could be a function of coal being something of a toxic industry in terms of institutional investing. As I wrote in my previous article:

It's helpful to the profitability of the existing that there's essentially no long-term future for these companies. It's a very speculative endeavor to make long-term investments in this industry. Commodity industries tend to be poor investments because whenever the going is good, returns are driven down by new investments in capacity. The end of the coal industry may finally free it from that dynamic. Coal will likely disappear as a fuel over the next decade((S)), but these could potentially be very profitable. Meanwhile, the shares are priced as if it's game over in ~2025.

It seems very likely to me, given the macro backdrop and peer results, BTU will have a strong second half of 2022. BTU isn't exactly a market darling because its capital allocation isn't yet geared very much toward dividends and buybacks. Currently, the company is restricted here because of covenants in its debt documents and surety agreements. As much as I'd love my dividend and buybacks right now, I understand the company is working toward bringing the debt down and will try to address these restrictions as that happens. The company is actually already in a slight net cash position. I'm of the mind end of 2022/2023 is likely to be a profitable time period for BTU. There's the possibility (for geopolitical reasons) that these will be highly profitable time periods. At some point, shareholder returns become a reality and BTU should trade closer to peers(and that's not a very high bar, to begin with).

For further details see:

Peabody Energy: Shareholder Returns Should Ultimately Follow At These Prices