CA - Pembina Pipeline: Alliance Acquisition Strengthens The Thesis

2023-12-17 07:00:00 ET

Summary

- Pembina Pipeline Corporation acquires Enbridge's stakes in joint ventures, increasing its ownership and cash flow from existing infrastructure.

- The market reacts negatively to the news, possibly due to the issuance of subscription receipts and dilution of shares.

- The acquisition is expected to be immediately accretive to Pembina Pipeline's cash flow per share, but the acquisition multiple is not impressive compared to industry peers.

- The overall thesis does not change, and Pembina Pipeline continues to look like an excellent way to get a 5.96% yield today.

On Wednesday, December 13, 2023, Canadian pipeline giant Pembina Pipeline Corporation ( PBA ) announced the acquisition of Enbridge’s ( ENB ) stakes in the Alliance, Aux Sable, and NRGreen joint ventures. Pembina already owns a considerable stake in this joint venture, so this is simply going to result in it increasing the percentage of the cash flows generated by this infrastructure that it receives. This will not expand the company’s reach into new areas of the industry or outside of its existing footprint. There may be some investors out there who could be disappointed by this. After all, Pembina Pipeline does not have the scale of Enbridge, Enterprise Products Partners ( EPD ), or any of the other giants in the industry. It is still one of the largest midstream corporations around though, and this acquisition should still have a beneficial effect on the company’s cash flow. The fact that the company is not as large as some of its rivals is immaterial.

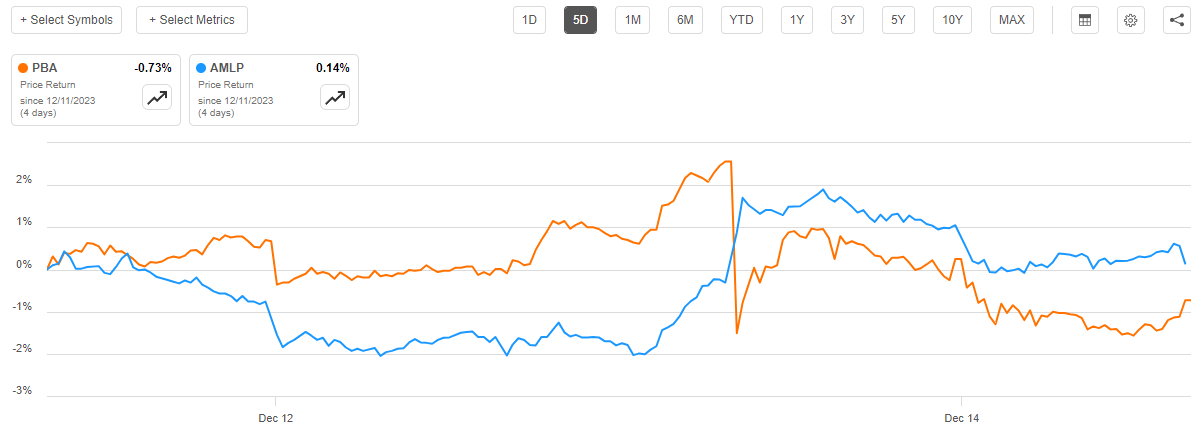

For its part, the market did not react at all well to this news. As we can see here, the company’s stock price dropped following the announcement of this acquisition on a day that the rest of the midstream sector as indicated by the Alerian MLP ETF ( AMLP ) was up:

{kind=link}

As such, it certainly appears that the market does not think very highly of this deal. This might be because one of the methods that is being used to finance this deal is the issuance of subscription receipts, which will increase the number of shares outstanding once the deal closes. Hopefully, the deal will still be accretive to the company’s cash flow on a per-share basis even once the new shares are issued. The market appears to expect that this may not be the case. As such, we want to investigate and determine what impact this deal will have on our thesis.

About The Deal

As stated in the introduction, as well as in Seeking Alpha’s bullet-point summary, Pembina Pipeline announced that it will be acquiring fellow Canadian midstream giant Enbridge’s stakes in the Alliance, Aux Sable, and NRGreen joint ventures. The company’s official press release provides more detail:

Pembina has entered into a purchase and sale agreement with Enbridge to acquire all of Enbridge’s interests in the Alliance, Aux Sable and NRGreen joint ventures and in the related operatorship contracts for an aggregated purchase price of $3.1 billion, including approximately $327 million of assumed debt, representing Enbridge’s proportionate share of the indebtedness of Alliance.

Pembina currently owns 50% of the equity interests in Alliance, Aux Sable’s Canadian operations, and NRGreen and approximately 42.7% of the equity interests in Aux Sable’s U.S. operations, and is the operator of certain assets pursuant to various operation services agreements (“COSAs”), with Enbridge being the operator of the remaining assets of the Acquired Business under other COSAs. Upon closing of the Acquisition, Pembina will hold 100% of the equity interests in Alliance, Aux Sable’s Canadian operations and NRGreen and approximately 85.4% of Aux Sable’s U.S. operations., and Pembina will become the operator of all of the Alliance, Aux Sable and NRGreen businesses. Pembina’s acquisition of Enbridge’s interests, including the additional interests in Aux Sable’s U.S. operations, is not subject to any rights of first refusal.

In short, Pembina Pipeline already owns a substantial stake in all of the entities that it is planning to acquire. This purchase will simply increase the company’s ownership stake, which will entitle it to a greater proportion of the cash flows that are generated by the assets of these joint ventures.

Curiously, Pembina Pipeline’s news announcement does not include any description of exactly what these purchased assets are. Fortunately, information can be found from other sources, including the presentation that the company recently released to its investors. Additionally, The Williams Companies ( WMB ) describes Aux Sable on its website:

Aux Sable is one of the largest NGL extraction and fractionation facilities in North America, processing liquids-rich gas at the terminus of the Alliance Pipeline, in Channahon, Illinois.

The Alliance Pipeline system is a massive pipeline system that extends from the Western Canadian Sedimentary Basin in British Columbia, Canada to Illinois, United States:

Canada Energy Regulator

NRGreen is a clean energy consulting firm based in Germany that has been involved in the construction of wind farms. In this case, the facility is a plant that uses waste heat to generate electricity:

Pembina Pipeline

NRGreen is a minor part of this acquisition, and its contribution to the company’s cash flow and EBITDA will be quite moderate compared to the other parts of this acquisition.

For the most part, though, it appears that Pembina Pipeline is not looking to expand into other businesses that it may not be familiar with. The company is clearly maintaining its focus on the midstream and hydrocarbon processing segments with which it has great familiarity and expertise. This is very nice to see as problems can sometimes arise whenever a business attempts to move into a new area via an acquisition.

Pembina Pipeline stated that it intends to finance this partially through the issuance of C$1.1 billion worth of subscriptions. This generally results in the issuance of new common stock, which dilutes the existing shareholders, although shareholders can keep their ownership stake relatively stable by buying new shares in the subscription offering. As a result, a company’s stock price does tend to drop somewhat when the subscription offering is announced, which is exactly what we saw in the company’s market action this week.

The big question then becomes how many new shares the company will need to issue in order to finance this acquisition. As of right now, the Toronto-traded shares are at C$44.32, so $1.1 billion would work out to about 24.82 million new shares. Pembina Pipeline currently has 549.0 million shares outstanding, so this issuance would increase the share count by about 4.5%. This is certainly a large enough increase in the outstanding share count that we should not ignore it.

At the same time, Pembina Pipeline claims in the news announcement that this acquisition will be immediately accretive to the company’s cash flow per share, and if its estimates of C$225 million to C$250 million are reasonably accurate then the math confirms that statement. The assets are all already active and have been operating under long-term contracts, so it seems likely that this estimate is reasonably accurate.

One major complaint that I have with this deal is that the acquisition multiple is not at all impressive. Pembina Pipeline claims a 9x adjusted EBITDA multiple in 2024 and an 8x multiple based on estimated 2025 cash flow:

Attractive acquisition multiple of approximately 9x 2023 and 2024 forecasted adjusted EBITDA, or approximately 8x 2023 and 2024 forecasted adjusted EBITDA, inclusive of $40 million to $65 million of annual synergies expected to be realized by 2025. Additional long-term synergy opportunities have been identified that would further reduce the transaction multiple.

In previous articles on midstream growth companies, I have pointed out that EBITDA multiples of 4x to 6x are not uncommon. In fact, this is the range that both Kinder Morgan ( KMI ) and The Williams Companies usually receive on their own growth projects. This is also the range that other peers usually advertise in investor presentations and similar material when discussing growth opportunities. As such, I have to disagree with Pembina Pipeline’s management. This is not as attractive of a multiple as I would really like to see, especially when we consider that interest rates are a lot higher than they used to be so payback periods should ideally be shorter than in the past.

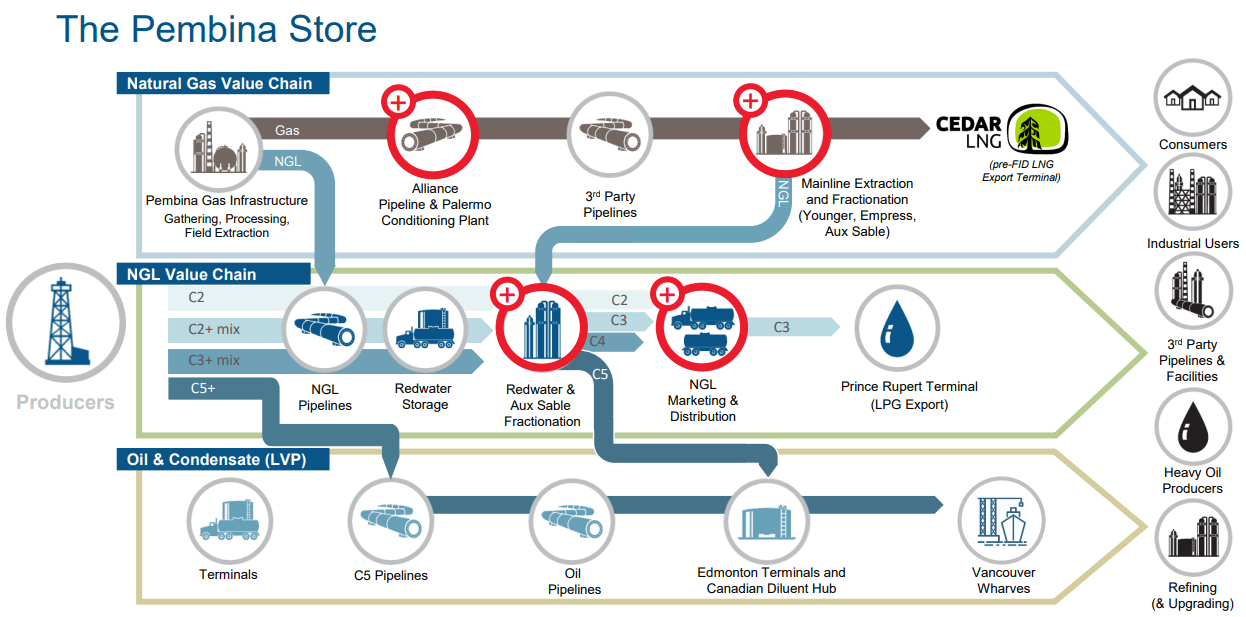

Value Chain Of The Combined Company

One of the things that we have always appreciated about Pembina Pipeline is the fact that the company has a presence all across the midstream value chain. The addition of the Alliance and Aux Sable Businesses expands it:

{kind=link}

In most cases, this acquisition simply increases the company’s presence in businesses that it was already involved in, as already noted earlier in this article. For example, Pembina Pipeline already owned the Redwater Fractionation plant, which was one of the largest fractionation facilities in North America, but the Aux Sable plant adds additional capacity in this area. The same is true for pipelines, as Pembina Pipeline has an extensive network of pipelines in central Canada today. As already mentioned, this acquisition appears to be simply an expansion of the company’s footprint in businesses in which it already had a presence.

The fact that Pembina Pipeline continues to have a presence all across the midstream value chain is something that could prove to be a competitive advantage for the company compared to those firms that do not have such a presence. After all, Pembina can essentially act as a single vendor performing the steps needed to get the product from the oil fields to the market where it can be sold. It could be more convenient for customers to work with a single vendor compared to many different ones.

Financial Considerations And Dividend Analysis

As I discussed in a previous article on Pembina Pipeline, the company’s balance sheet and dividend coverage is quite strong. There is nothing in this acquisition that changes things in a negative way, at least on a long-term basis. The fact that the company is financing quite a bit of this purchase with equity should prevent this transaction from having much of a negative impact on the company’s debt ratios, and the fact that it increases cash flow per share means that the dividend actually becomes a bit more affordable.

As the linked article includes very recent figures for the company, there is no reason to copy the analysis here.

Conclusion

In conclusion, there is nothing in this acquisition that appears to change our overall thesis about Pembina Pipeline in a negative way. The company’s balance sheet should still continue to be strong, and it should have adequate coverage of the dividend. In fact, it strengthens the company’s ability to grow its dividend going forward due to the per-share accretion. The only real complaint is that the payback period for this purchase seems rather weak, especially compared to the returns that its peers generate from organic growth projects. Overall though, the company continues to look like a reasonably solid way to earn a 5.96% yield today.

For further details see:

Pembina Pipeline: Alliance Acquisition Strengthens The Thesis