CA - Pembina Pipeline: Q3 Results Showcase The Company's Overall Financial Strength

2023-11-13 09:22:17 ET

Summary

- Pembina Pipeline Corporation reported lower revenue but increased cash flows in its Q3 2023 earnings results.

- The company's stock price has been performing well, outperforming the S&P 500 Index over the past month.

- Pembina Pipeline's financial stability and attractive dividend yield make it an attractive investment option, although its yield is lower than some peers in the midstream sector.

- The company is much less indebted than some peer companies, so it has not been as impacted by the rising interest rates as some other midstream firms.

- The company's current dividend appears to be very sustainable.

On Thursday, November 2, 2023, Canadian midstream giant Pembina Pipeline Corporation ( PBA ) announced its third quarter 2023 earnings results. The headline numbers generally represented a continuation of the trend that we have seen across the midstream sector, at least from those companies that have reported so far. Pembina Pipeline showed lower revenue than in the year-ago quarter, but otherwise, its financial stability is on clear display here.

In particular, Pembina Pipeline's cash flows were up significantly compared to the prior year quarter. This is ultimately the most important thing for us as income investors as it is ultimately cash flow that determines the ability of a company to pay its dividends. Pembina Pipeline is certainly an attractive dividend stock right now, as the company's 6.08% yield is higher than many other things in the market. With that said though, Pembina Pipeline's yield is lower than that of companies like Enbridge ( ENB ), MPLX ( MPLX ), Energy Transfer ( ET ), and numerous other peers in the midstream sector.

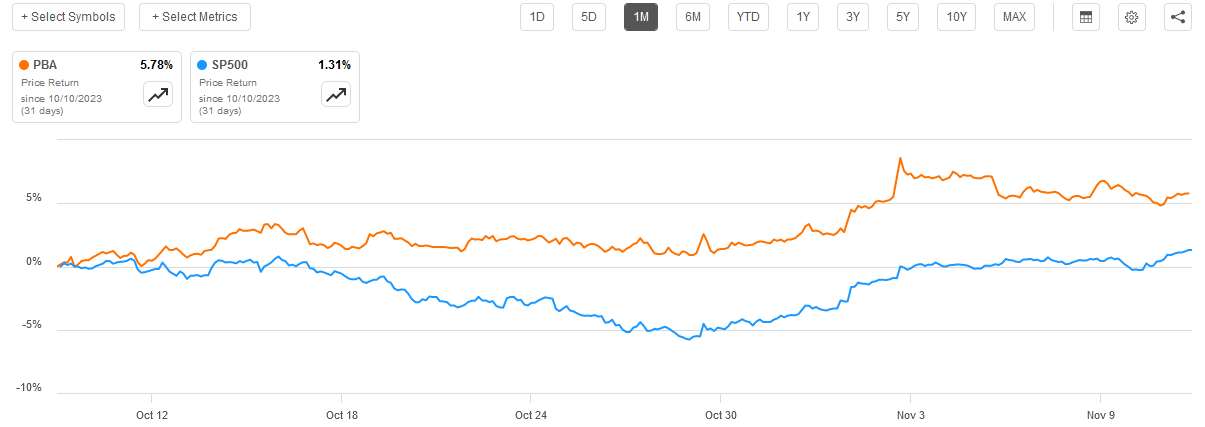

For its part, the market was generally favorable towards Pembina Pipeline's earnings results. The stock started going up on November 2 prior to the announcement and then jumped overnight to open on Friday at a higher level than the Thursday close. Over the past month, Pembina Pipeline's common stock is up 5.78%, significantly beating the S&P 500 Index (SP500) over the period:

{kind=link}

The fact that the company beat the broader market index over the past month is the same thing that we saw with Enbridge over the same period, which we discussed earlier today. Pembina outperformed its Canadian peer by a significant amount over the period, though. This could have something to do with Pembina Pipeline being much more conservative and focusing its efforts on developing its midstream business, rather than attempting to expand into other sectors of the economy.

Let us have a look at Pembina Pipeline's earnings results and determine if its recent market strength makes sense and if our thesis is still intact.

Earnings Results Analysis

As regular readers are no doubt well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Pembina Pipeline's third quarter 2023 earnings report:

- Pembina Pipeline brought in total revenue of C$2.292 billion during the third quarter of 2023. This represents a 17.52% decline over the C$2.779 billion that the company brought in during the prior-year quarter.

- The company reported an operating income of C$529.0 million in the most recent period. This represents an 18.36% decline over the C$648.0 million that the company reported in the year-ago quarter.

- Pembina Pipeline handled an average of 3.398 million barrels of oil equivalent per day in the reporting period. This represents a slight decline over the 3.424 million barrels of oil equivalent per day that the company handled in the corresponding quarter of last year.

- The company extended or signed new long-term contracts totaling 50,000 barrels per day that will be handled by the company's pipeline and facility assets. This shows that the demand for its services is rising, which is ultimately good for the forward growth of the business.

- Pembina Pipeline reported a net income of C$346.0 million during the third quarter of 2023. This represents an 81.08% decline over the C$1.829 billion that the company reported in the third quarter of 2022.

For the most part, the company's management appeared to be reasonably pleased with the company's performance in the third quarter of 2023. The earnings press release states :

Third quarter results reflect strong performance in the Pipelines and Facilities divisions as Pembina continues to benefit from growing volumes and higher tolls on certain systems. Notably, the conventional pipelines business delivered record quarterly volumes. Further, Pembina's marketing business delivered another solid contribution.

The company is clearly hyping up its rising volumes, but the highlights show that the company's volumes actually went down year-over-year. This was entirely due to the Facilities side of the business, which handles natural gas processing, natural gas liquids fractionation, and other operations that are not strictly related to getting hydrocarbon resources from one place to another. This unit reported average volumes of 803,000 barrels of oil equivalent per day during the most recent quarter compared to 893,000 barrels of oil equivalent per day on average during the equivalent period of last year. That more than offset the volume increase from the pipeline business. The company's pipelines transported an average of 2.595 million barrels of oil equivalent per day during the most recent quarter. The corresponding level during the year-ago quarter was 2.531 million barrels of oil equivalents per day. Thus, the pipeline business continues to fare pretty well, but the weakness on the facilities side more than offset the incremental improvements.

Fortunately, the volume decline in the Facilities division did not cause the business unit's cash flow to decline. In fact, the Facilities division reported an adjusted EBITDA of C$319 million during the quarter, which represents an increase of C$28 million year-over-year. The majority of this came from financial transactions though, and not really from an improvement in operational performance. Here is the earnings press release's version of why this unit's performance went up:

Pembina Pipeline - Earnings Press Release Posted to Seeking Alpha

I would have liked to see something like "improved profit margin" in these results, but that was not to be. Rather, all that we see here is that the company made a few financial transactions over the past twelve months that allowed it to credit more of the profit that is generated by some of the company's assets to its reportable results. As such, this is pretty much guaranteed to be a one-time transaction and the company will not be able to grow its cash flows by a similar amount next year. Fortunately, though, the company's cash flow should also not decline going forward because it should be able to continue to credit the additional cash flow to its adjusted EBITDA from now on.

Fortunately, the Pipelines business also delivered year-over-year growth, and this growth was driven by more than just accounting idiosyncrasies. The company reports that the Pipelines unit had an adjusted EBITDA of C$591 million, which represents a C$56 million increase compared to the year-ago quarter. The majority of this came from higher volumes of resources moving through the company's pipelines, which is exactly where we like to see growth coming from for a business such as this.

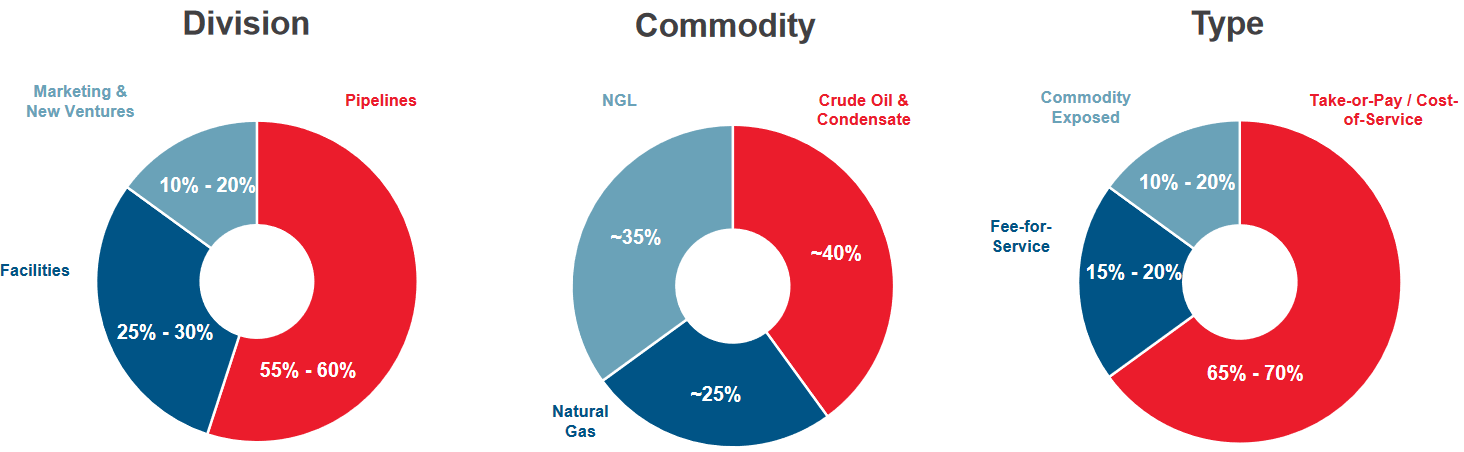

Fortunately, the majority of the company's cash flow comes from its Pipelines business. As shown here, the company expects that approximately 55% to 60% of its adjusted EBITDA is going to come from the Pipeline transportation unit over the full-year 2023 period:

{kind=link}

As such, the performance of the Pipeline division is perhaps the most important to the company's final results and its ability to cover the dividends. The fact that this business did pretty well during the third quarter is a good sign that Pembina Pipeline should be able to continue to reward its shareholders over the course of this year.

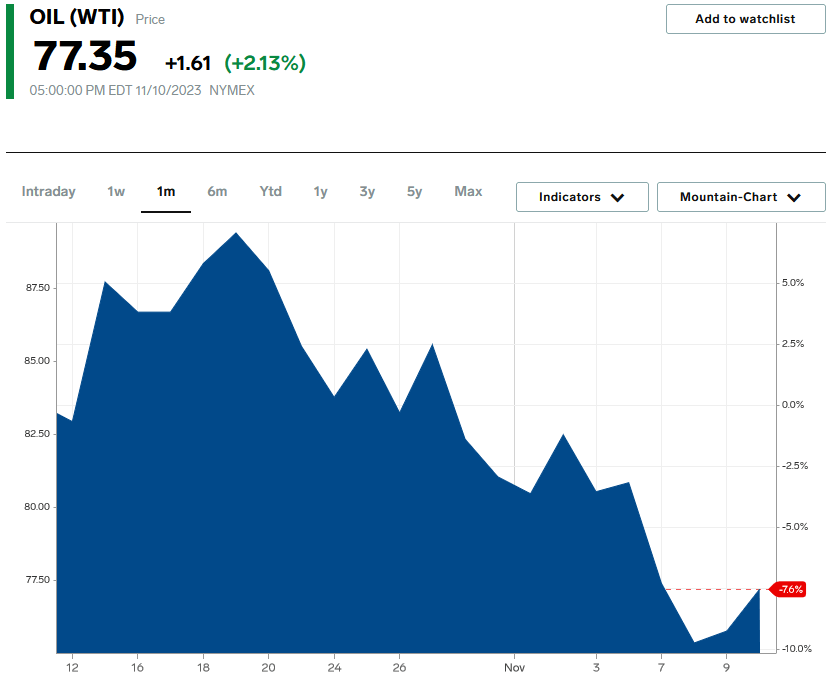

We can also see that very little (10% to 20%) of the company's cash flow is exposed to volatile commodity prices. This is a very good thing, especially right now. This is because commodity prices have not been doing very well lately. As we can see here, the price of West Texas Intermediate crude oil is down 7.6% over the past month:

{kind=link}

The less that is said about natural gas prices right now, the better. This is despite the fact that the fundamentals for both of these commodities are pointing to rising prices, not falling prices. After all, as I have pointed out in a few recent articles, there is a very real possibility of experiencing a crude oil shortage by mid-decade and a substantial global oil shortage by 2030.

Fortunately, Pembina Pipeline does not really have to worry about these fluctuations in commodity prices because most of its cash flow comes from sources that are not exposed to commodity prices. We certainly see that in the third quarter, as the company's cash flows were up despite the fact that both crude oil and natural gas prices were on average lower than in the year-ago quarter.

The overall stability in the face of weakening energy prices is something that we should be able to very much appreciate with Pembina Pipeline. After all, it is ultimately cash flows that determine the company's ability to pay its dividends and stable cash flows allow the company to budget a reasonably large percentage of its cash flow to be paid out to shareholders. This certainly appears to be the case here.

Financial Considerations

As I pointed out in a previous article on Pembina Pipeline,

It is always important to look at the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. As debt carries an interest rate that is based on the market rate at the time of issuance, a company's interest expenses might increase following the rollover in certain market conditions. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push the company into financial distress if it has too much debt. While midstream companies like Pembina Pipeline typically have remarkably stable cash flows, this is still a risk that we should not ignore.

As of the time of writing, interest rates in both the United States and Canada are very close to the highest levels that have been seen in the 21st century. This is due to the fact that the central banks of both nations have been actively working to reduce the high rate of inflation that has been dominating the post-pandemic period. Unfortunately, this means that any debt that Pembina Pipeline is forced to roll over will almost certainly increase the interest expenses that it has to pay to service the debt.

Fortunately, Pembina Pipeline has not been suffering as much from rising interest rates as some of its peers. As we can see here, the company's interest expenses have only increased by C$10 million per quarter since early 2021:

{kind=link}

Compare this to peer company Enbridge, which has seen its net interest expense increase by C$270 million over the same period. Of course, Pembina Pipeline has been much more conservative with respect to its finances over the past few years, which appears to be paying off here.

In short, so far at least, we are not seeing any real adverse impact of rising rates on the company's financial performance. This is good because the money that the company has to pay out in interest is money that cannot be used for more productive purposes, or returned to the shareholders via dividends.

In previous articles on Pembina Pipeline, we have seen that the company should not have any particular difficulty carrying its debt. However, those analyses were all performed using prior quarter numbers. We naturally want to update our analysis with the current quarter figures so that we know how financially solid the company is right now.

The usual way that we judge a midstream company's ability to carry its debt is by looking at its leverage ratio, which is calculated as debt-to-adjusted EBITDA. This figure theoretically tells us how many years it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task.

As of September 30, 2023, Pembina Pipeline has a leverage ratio of 3.4x based on its trailing twelve-month adjusted EBITDA. That is a very attractive figure that is significantly below the 5.0x that Wall Street analysts usually consider acceptable. It is also below the 4.0x figure that many of the most well-funded midstream companies in the sector are now running so Pembina Pipeline's leverage certainly does not look unattractive relative to its peers. Overall, we should not need to worry about the company's debt right now.

Dividend Analysis

One of the biggest reasons why investors purchase shares of midstream companies like Pembina Pipeline is that they normally have much higher yields than companies in other sectors. Pembina Pipeline is certainly no exception to this, as the company's 6.08% yield represents one of the few common stock yields that exceeds Treasury securities or money market funds right now. Although, as mentioned in the introduction, it is certainly nowhere near as attractive as some of the yields that we see in other midstream companies. That could make Pembina Pipeline a second-drawer choice for income investors, but the company's financial strength does help to explain why it trades with a lower yield than other companies that are deemed to be less desirable by the market.

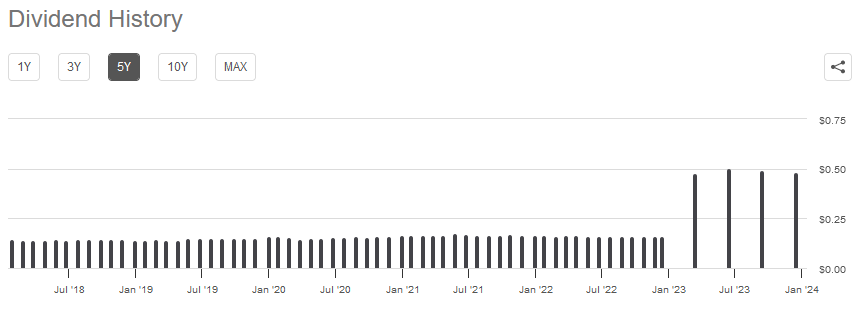

One thing that we can very much appreciate as income-focused investors is that Pembina Pipeline has a long history of raising its dividends over time:

{kind=link}

Admittedly, some readers might point out that the above chart shows that the dividend varies by a somewhat large degree from quarter to quarter and even month to month. However, that variance comes from the fact that Pembina Pipeline declares and pays its dividends in Canadian dollars. The dividends that are received by anyone who purchases the shares on the New York Stock Exchange, however, are in U.S. dollars. Thus, the exchange rate on the day that the dividends are paid determines the amount of money that the investor actually receives. This is why the dividends can vary even though the company is constantly raising the amount that it pays investors in its home currency.

The fact that the company raises its dividends on a regular basis works out very well for those investors who are dependent on their portfolios to provide the income that they need to pay their bills and finance their lifestyles. After all, inflation is constantly reducing the number of goods and services that can be purchased with the dividend so the dividend needs to keep rising just to maintain its purchasing power.

As is always the case, it is critical that we ensure that Pembina Pipeline can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our incomes and almost certainly causes the stock price to decline.

The usual way that we judge a company's ability to sustain its dividends is by looking at its free cash flow. During the twelve-month period that ended on September 30, 2023, Pembina Pipeline reported a levered free cash flow of C$1.0995 billion. That was, unfortunately, not enough to cover the C$1.6940 billion that the company paid out in dividends over the same period. This is likely to be concerning at first glance, since it shows that Pembina Pipeline is not generating enough cash internally to pay all its bills, cover its capital expenses, and pay out the current dividend to the shareholders.

However, we can treat Pembina Pipeline somewhat like a utility because of its overall cash flow stability. As I have pointed out in various previous articles, utilities usually finance their capital expenditures through the issuance of debt and equity while paying their dividends out of operating cash flow. During the trailing twelve-month period that ended on September 30, 2023, Pembina Pipeline reported an operating cash flow of C$2.7020 billion. That was more than sufficient to cover the C$1.6940 billion that was paid out in dividends and give the company a substantial amount of money that could be used for other purposes. Thus, Pembina Pipeline's dividend appears to be reasonably safe at the current level.

Conclusion

In conclusion, Pembina Pipeline Corporation's most recent Q3 earning report was quite solid despite the year-over-year revenue decline. The most important thing is cash flow, though, and this was up compared to the year-ago quarter. We also see that Pembina Pipeline is continuing to maintain its incredibly strong balance sheet and its attractive dividend yield. Unfortunately, though, the company's yield is not as good as some of its peers. This is almost certainly due to its generally stronger financial profile, as the market perceives that its risk is lower than the much more heavily indebted Enbridge.

For further details see:

Pembina Pipeline: Q3 Results Showcase The Company's Overall Financial Strength