PFGC - Performance Food Group: The Divergence Between Price And Fundamentals Is Bullish

2023-10-25 11:42:43 ET

Summary

- Performance Food Group has seen a decline in share price despite strong financial results and growth in revenue and profits.

- The company's Foodservice and Vistar segments have experienced significant revenue growth due to increased demand for eating out.

- Management remains optimistic about future growth, with projected revenue and EBITDA increases for the 2024 fiscal year.

During the past couple of years, most of the companies in the food market did quite well. Many of them were able to push inflationary pressures onto their customers. But it was only a matter of time before that trend ceased or even reversed. Earlier this year, the CEO of Conagra Brands (CAG), for instance, even said that, in response to continued inflation, Americans are buying less food. Naturally, that should not bode well for the companies involved in the gathering and transportation of food and other related products. And as a result, some companies in this space have seen downward pressure from a share price perspective in recent months.

A great example of this can be seen by looking at Performance Food Group Company (PFGC). For those who don't know, Performance Food Group is a rather large food and food products distributor that services over 300,000 customer locations in the food away-from-home industry using the 142 distribution centers in its network. Since I wrote a bullish article about the company back in May of this year, shares have seen a downside of 8.5%. By comparison, the S&P 500 has risen by 2.2%. This seems scary at first glance. And in the near term, it is certainly painful. However, when you dig underneath the hood and look at the most recent financial results provided by the management, you see that the fundamental picture for the enterprise is quite robust. The stock does look perhaps a tiny bit pricey compared to similar firms. But on an absolute basis, shares are still cheap enough to warrant some optimism moving forward.

The picture keeps looking sound

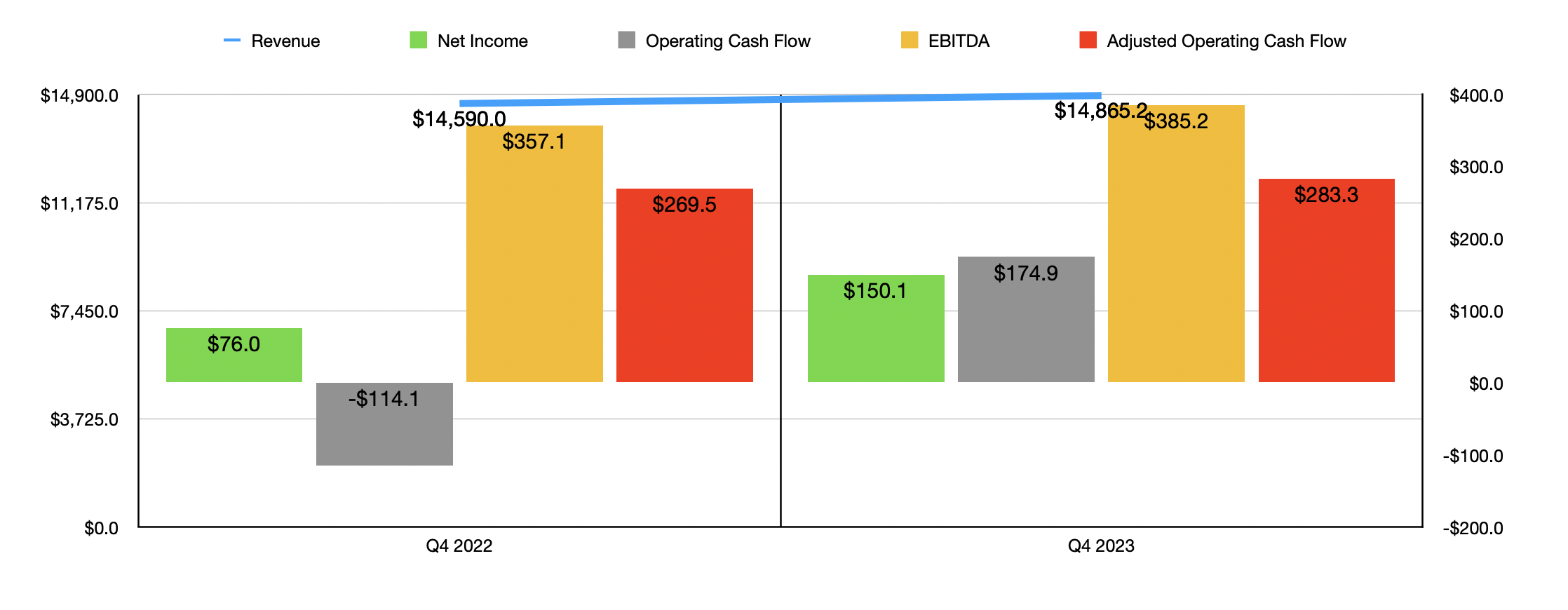

Although shares of Performance Food Group have been underperforming the market recently, the fundamentals of the company have been quite strong. To understand what I mean, we need only look at data covering the most recent quarter. This is the final quarter of the company's 2023 fiscal year . During that time, revenue came in at $14.87 billion. That's a decent increase over the $14.59 billion generated one year earlier. This increase of 1.9% was driven largely by a 1.8% increase in total organic case volume on a year-over-year basis.

{kind=link}

This rise in sales also brought with it higher profits as well. Net income almost doubled from $76 million in the final quarter of last year to $150.1 million in the same time in 2023. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, went from negative $114.1 million to positive $174.9 million. If we adjust for changes in working capital, we would get an increase from $269.5 million to $283.3 million. And finally, EBITDA for the company grew from $357.1 million to $385.2 million. It's worth noting that while the rise in revenue helped the company, another big contributor to the bottom line increase was expansion in its gross profit margin as a result of a favorable shift in the mix of cases sold, as well as by growth in the independent channel of operations that the company has.

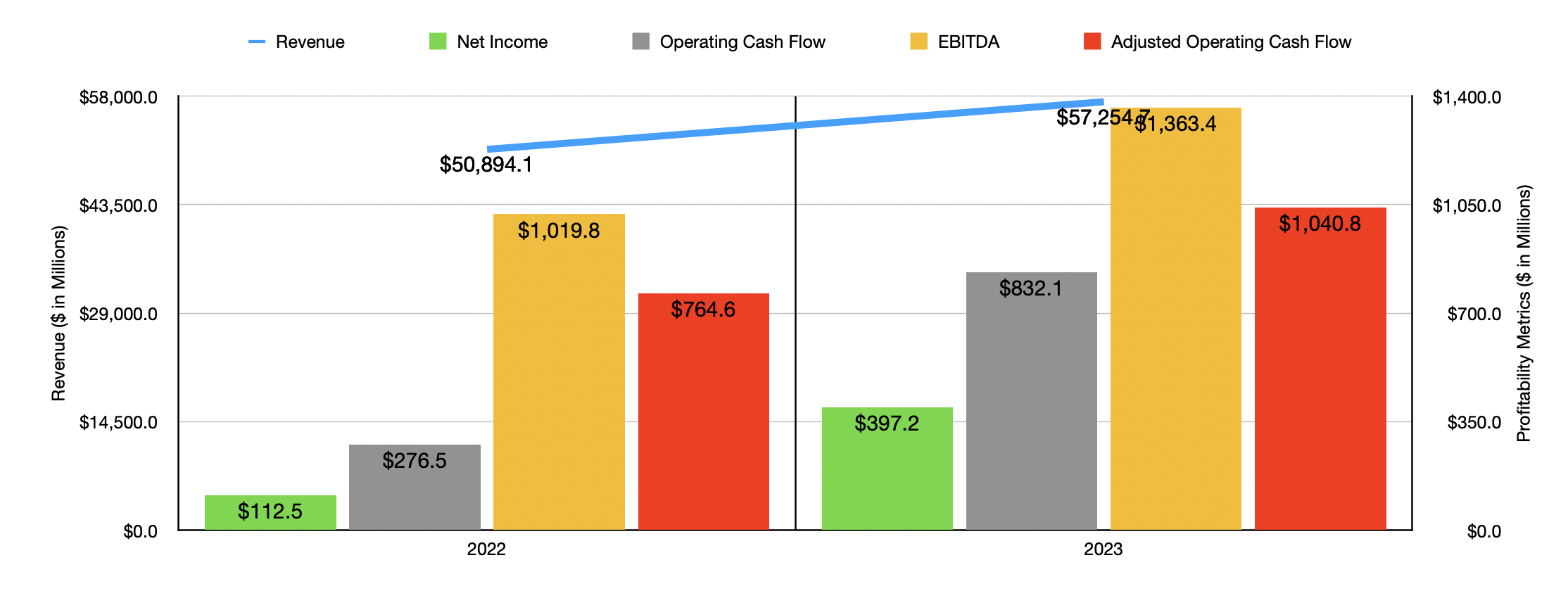

While the final quarter of the year might not have been the strongest, it does top off a rather robust year for the company. In 2023, revenue came in at $57.25 billion. That's 12.5% above the $50.89 billion generated one year earlier. A good part of this increase, however, came from the company's purchase of Core-Mark Holding Company, though it did benefit from product cost inflation of 8.6%. Even outside of this, the firm reported a 5.8% rise in total case volume on a year-over-year basis.

It's important to point out that Performance Food Group experienced upside across all three of its core operating segments. The Foodservice segment, which caters to around 175,000 restaurants and similar establishments, reported a 7.2% increase in revenue from $26.58 billion to $28.49 billion. An increase in selling price per case and a favorable shift in case mix were the two leading drivers of this growth.

Even though I mentioned earlier in this article that people are buying less food, they are actually spending more on out-to-eat food. And this is where Performance Food Group truly shines. You see, the COVID-19 pandemic brought with it some interesting changes. During that time, consumers were far more likely to make food at home. This caused some of the inflationary pressures in the food space since there was not the expectation of a major shake-up in where people eat. But as the pandemic has died down and is virtually gone, and frankly as boredom with home-cooked meals has set in, there has been a shift away from eating food at home to eating food elsewhere.

While Performance Food Group reported attractive growth for the Foodservice segment, Vistar performed even better. Revenue there skyrocketed 23.6% thanks to higher prices and volume growth in the vending, office coffee service, office supply, theater, value stores, hospitality, and travel channels. Again, all of this makes sense. As COVID-19 died down, all of these places were bound to experience additional traffic. This would be especially true of theaters, the travel industry, and hotels. And finally, we have the Convenience segment. Revenue here jumped 17.1%, though most of that increase was driven by the aforementioned acquisition.

{kind=link}

Just as was the case in the final quarter of the year, the year as a whole experienced attractive growth on the bottom line. Net income jumped from $112.5 million in 2022 to $397.2 million in 2023. Operating cash flow more than tripled from $276.5 million to $832.1 million on an adjusted basis. And finally, EBITDA grew from $1.02 billion to $1.36 billion.

When it comes to the future, management is still optimistic. For the 2024 fiscal year, they are expecting revenue of between $59 billion and $60 billion. At the midpoint, that would be 3.9% over what the company achieved in 2023. EBITDA, meanwhile, should be between $1.45 billion and $1.50 billion. Management also believes that they are well on their way to achieving their targets for 2025. That would call for revenue of between $62 billion and $64 billion and for EBITDA of between $1.50 billion and $1.70 billion.

{kind=link}

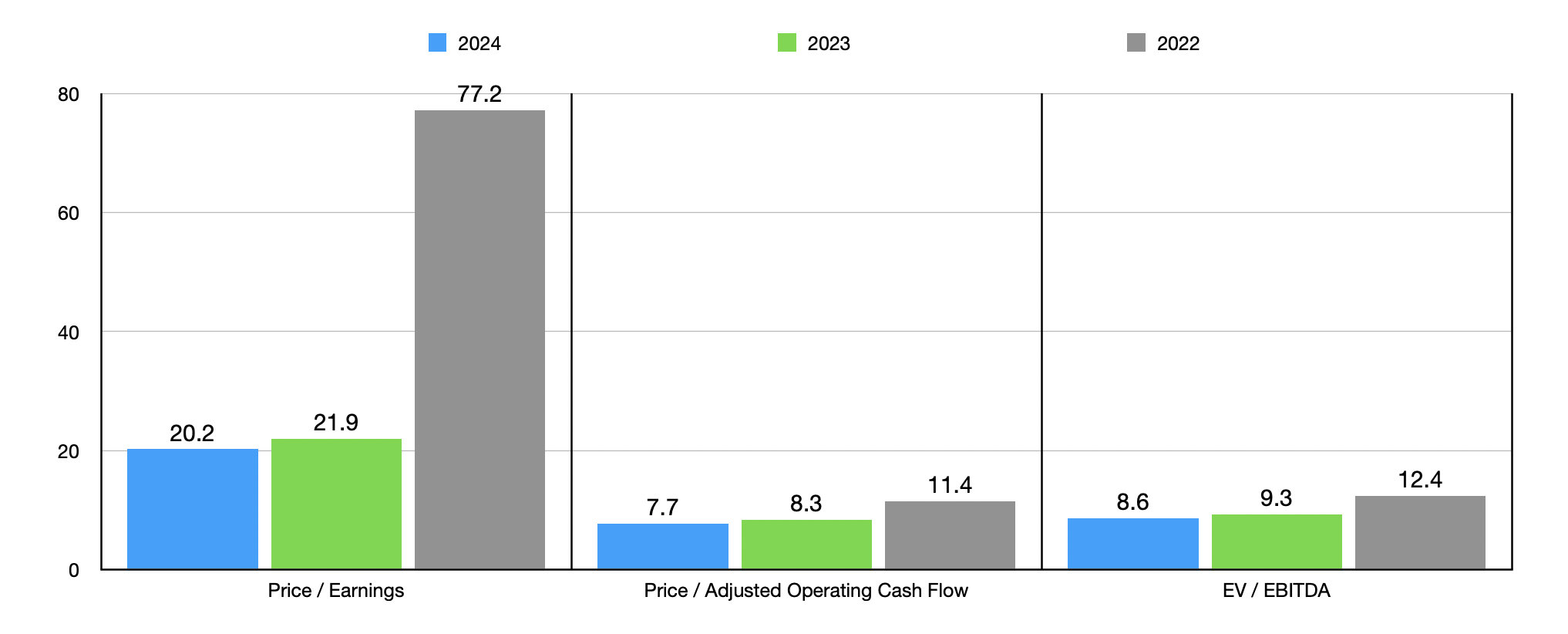

Using the estimate that we have for 2024, we can also get decent estimates for other profitability metrics. Net income, for instance, should be somewhere around $429.7 million. And adjusted operating cash flow should be $1.13 billion. Using these figures, I was then able to value the company as shown in the chart above. This includes not only the forward estimates for 2024 but also historical results for 2022 and 2023. In the table below, meanwhile, I compared the 2023 results to five similar firms. Using both the price-to-earnings approach and the EV to EBITDA approach, I found that three of the five companies ended up being cheaper than Performance Food Group. And when it comes to the price to operating cash flow approach, four of them were cheaper.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Performance Food Group Company |

| 21.9 |

| 8.3 |

| 9.3 |

| US Foods Holding Corp ( USFD ) |

| 20.1 |

| 7.8 |

| 10.4 |

| United Natural Foods ( UNFI ) |

| 41.4 |

| 1.4 |

| 6.4 |

| The Chefs' Warehouse ( CHEF ) |

| 36.0 |

| 55.0 |

| 10.5 |

| The Andersons ( ANDE ) |

| 19.6 |

| 1.4 |

| 8.4 |

| SpartanNash ( SPTN ) |

| 19.4 |

| 6.1 |

| 7.1 |

Takeaway

From all the data I see here, I have no reason to be anything other than bullish regarding Performance Food Group. While the stock might be pricey compared to similar firms, it looks cheap on an absolute basis. Growth continues even during these uncertain times and I see no reason why that should cease at any point ahead. Because of these factors, I have decided to keep the company rated a 'buy' for now.

For further details see:

Performance Food Group: The Divergence Between Price And Fundamentals Is Bullish