SHEL - Petrobras Q1'23: Strong Performance Dividends And Possible Buybacks On The Way

2023-05-12 08:29:48 ET

Summary

- Petrobras reported strong Q1’23 results, beating market expectations.

- The BoD proposed Q1’23 dividend of US$0.381/share (US$0.762/ADR), sticking to its generous dividend policy.

- However, changes in the shareholder return policy were hinted, possibly including buybacks.

- So far, investors’ fears of the Lula’s government impact on Petrobras seem largely exaggerated.

- Petrobras remains the cheapest oil major by far, presenting an attractive opportunity.

Petrobras (PBR)(PBR.A) has been amongst the most discussed companies, due to its large dividend and the possible radical changes in policy, following the election of Lula as president. The stock has been trading at large discount to its peers, primarily due to political risk. I've discussed the political risk in an article before, highlighting that a repeat of the car wash scandal type of developments as well as elimination of the dividend are quite unlikely. Now that Petrobras, under a newly appointed CEO, has reported its Q1'23 results and announced shareholder return plans, it's worth taking a look at the company again. It appears that another large dividend distribution of US$0.381/share* is proposed for Q1'23. However, the company signaled intentions to make changes to its shareholder return policy, possibly including a buyback procedure. On the balance sheet, debt seems manageable and net debt continues to melt. So far, the fears of the Lula's government ripping-off shareholders seem largely exaggerated and the market may start reducing the political risk discount. The current market value of Petrobras makes it the most undervalued oil major, relative to its peers, by far.

*Note that 1 ADR=2 shares

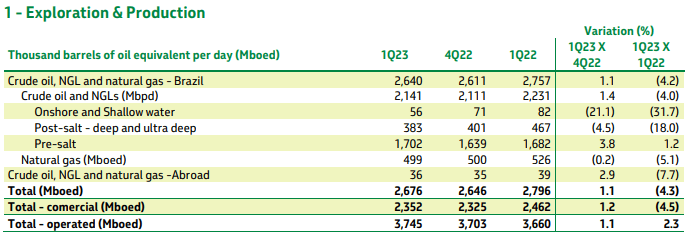

Petrobras operational overview

Q1'23 production numbers (Petrobras)

{kind=link}

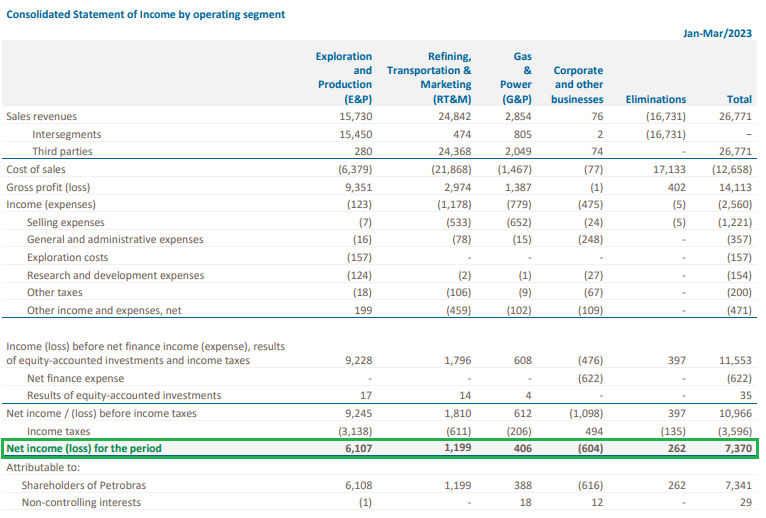

Petrobras released its Q1'23 results . Despite total commercial production being down a bit by 4.5% YoY to 2,352Mboe/day, the company managed to beat market expectations. Total revenue was down 1.5% YoY to US$26.8B, while gross profit declined by 2.1% YoY to US$14.1B, resulting in a slight decline in the respective margin to 52.7% from 53.0% a year ago. Inflation didn't spare the company as OPEX rose to US$2.6B (+19.5% YoY). The bottom line came at US$7.3B, which is 14.8% lower, but 19.4% higher than market expectations . This translates into EPS of US$0.56/share.

Q1'23 segment performance (Petrobras)

{kind=link}

Note, that the biggest contributor to the bottom line was the Exploration and Production (E&P) segment with net income of US$6.1B (US$8.0B in Q1'22), while the Refining, Transportation and Marketing (RT&M) segment added US$1.2B (US$1.9B in Q1'22) to earnings. However, the two smaller segments - Gas and Power (G&P) and Eliminations reported positive earnings, compared to negative last year, which partially offset the lower performance of the two main segments - E&P and RT&M.

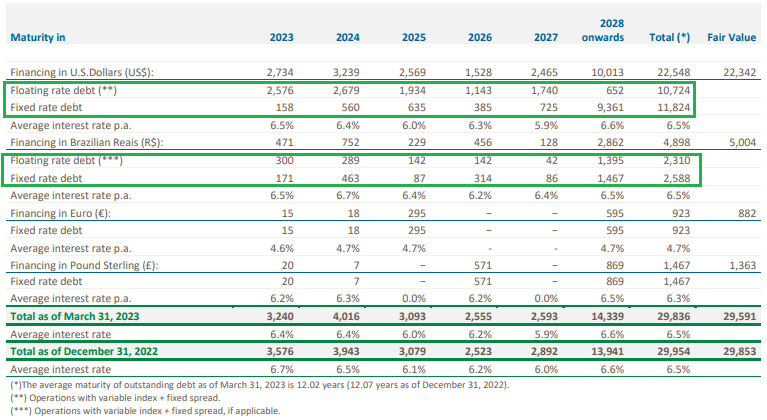

Debt under control

Looking at the balance sheet, Petrobras has financial debt of US$29.8B with 56.3% of it being at fixed rates. Looking at the maturity schedule, in every of the next three years between US$3B and US$4B of debt is due, making it relatively easy for the company to service it. In addition, there are lease liabilities of about US$23.5B, which when considering the US$10.3B of cash and equivalents, brings the net debt of the company to a bit below US$43.1B, down 6.0% YtD.

Financial debt profile (Petrobras)

{kind=link}

Overall, despite the rising interest rates environment, while Petrobras will experience higher interest expenses on its floating debt component, the situation is manageable. With the cash flow generating abilities of the company, the financial condition seems healthy. For reference, the annualized cash provided by operating activities (US$41.4B using Q1'23 figures as a starting point) is almost equal to total net debt.

Shareholder returns

One of the biggest fears of investors related to Petrobras is that, following Lula's election as president, the distribution policy of Petrobras will be radically changed, as the politician has been criticizing the massive dividends. As the company is majority state-owned, the government has the decisive role in its corporate governance. After the elections, the management team of the company was indeed changed, but the new BoD proposed another large dividend, sticking to the previous policy of 60% of operating cash flows minus investments. The proposal is for the total distribution of nearly US$5B or US$0.381/share (US$0.762/ADR), resulting in annualized dividend yield of 26.9% for the ordinary PBR share and 29.7% for the preferred PBR.A share.

Q1'23 dividend proposal (Petrobras)

{kind=link}

It has to be noted, that management signaled intentions to make changes to its shareholder return policy, aiming to "improve" it and eventually add share-buybacks. While I doubt that many shareholders want "improvements" in the current policy, the inclusion of share repurchases seems like a good idea, given the large discount of Petrobras to other oil majors. Also, reducing the dividend payout seems likely, but I still expect the dividend yield to remain in double-digit territory, amongst the highest in the sector.

Political risk

In light of the memories from the famous Car Wash scandal and Lula's criticism over Petrobras' generous dividend policy, it's normal that some investors fear of radical changes in the company's governance to the worse. That being said, the newly appointed management team seems to maintain a shareholder-friendly stance, maintaining high dividends and hinting at buybacks.

On 11 May, Lula has hinted that the government will seek lower fuel prices from Petrobras. While initially, some investors may be spooked by such comments, looking at the broader picture gives an important context. As oil prices have recently fallen, it's normal to expect lower fuel prices. Of course, an elected official will hardly pass on the opportunity to take credit for market changes that benefit the population at large. So as of now, Lula's policy towards Petrobras seems to be a lot of talk, but at the same time maintaining the shareholder profile of the company.

PBR stock valuation

Looking at Petrobras' valuation through peers comparison with other oil majors through the Forward EV/EBITDA multiple, the company appears to be deeply undervalued. I think that the discount is unjustified - after all it's not Brazil that has windfall taxes on oil profits, but the EU and Colombia, yet oil majors from those places are trading at large premium to Petrobras. As the maintenance of shareholder-friendly distribution policy seems more and more likely, the market could start repricing the risks and shares of Petrobras could appreciate as a result, reducing the discount to peers.

Conclusion

Petrobras reported strong Q1'23 results and the BoD proposed another solid dividend to be distributed to shareholders. While the distribution policy will be changed soon, management mentioned the possibility of the inclusion of share repurchases, which makes sense, given the large discount to peers. Overall, Petrobras remains the cheapest oil major, presenting an attractive entry point for those willing to bear the risks.

For further details see:

Petrobras Q1'23: Strong Performance, Dividends And Possible Buybacks On The Way