CA - PetroTal: Navigating Through The Peruvian Turmoil

Summary

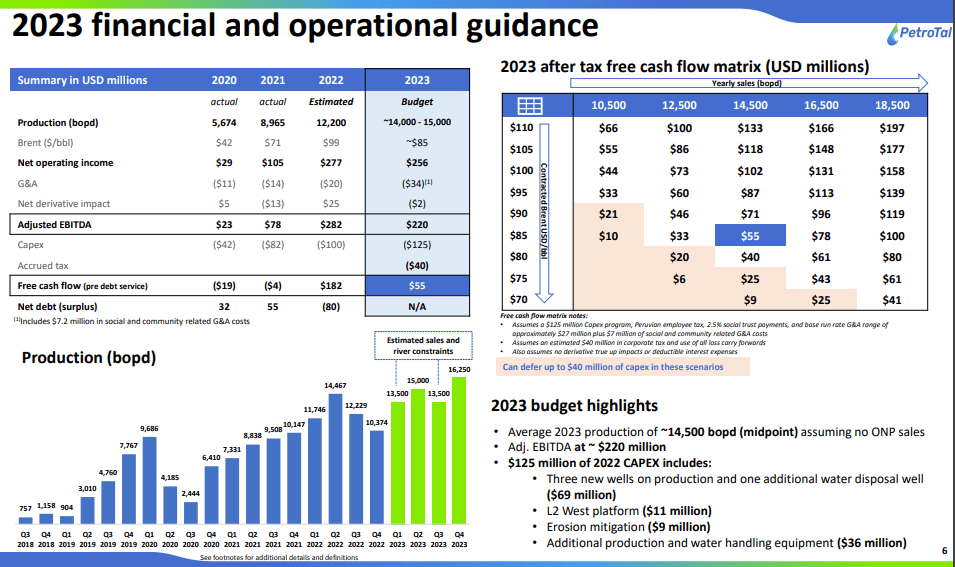

- PetroTal has released its 2023 budget and guidance, with expected production of 14.5kboe/day and EBITDA of US$220M.

- There has been progress on collecting the receivables from Petroperu as payments are being made under an established schedule.

- Management plans to retire the US$80M of outstanding debt in Q1’23 and subsequently initiate a shareholder return program.

- PetroTal remains one of the most undervalued oil plays as political and social turmoil is not seriously affecting the company yet, but the risk remains high.

In November, I wrote an article about PetroTal (PTALF)(TAL:CA) - small but rapidly growing oil producer from Peru. Now that Peru is shaken by social unrest and PetroTal's management released their 2023 budget and guidance, I decided to take a look at the new developments and their implications for shareholders. It seems that the company has been making progress with both its development activities as well as with collecting the considerable receivables from Petroperu. The 2023 guidance looks quite realistic to me, while management intends to initiate a shareholder return program in 2023. The company remains at a very attractive valuation, but there's the risk of the political turmoil in Peru deepening and social unrest affecting the company's operations. For that reason, I think that only high-risk tolerance investors should consider the stock.

2023 guidance and new developments

2023 budget and guidance (PetroTal)

{kind=link}

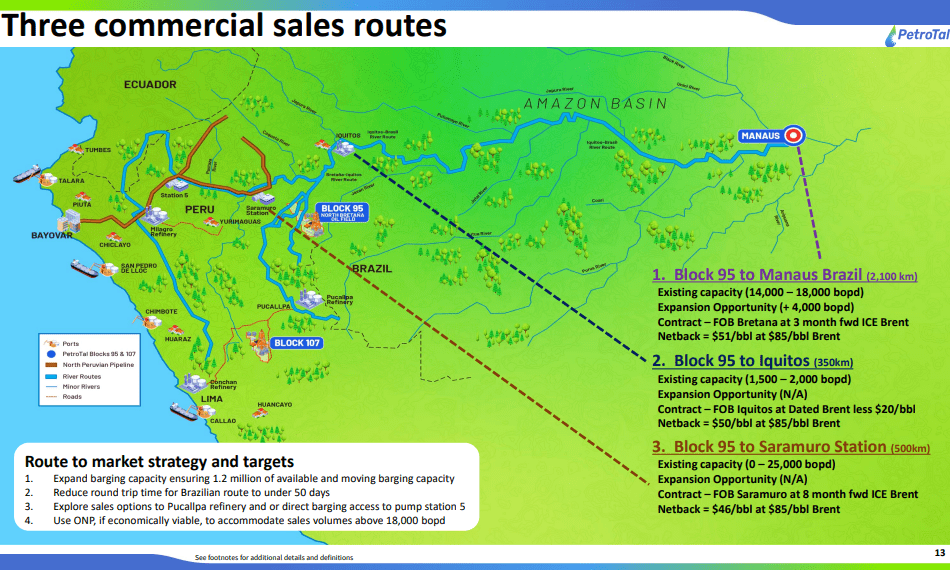

Management expects average daily production of 14.5kboe, which will be around 19% YoY increase. At the same time, PetroTal has much larger production capacity as it demonstrated by achieving an exit production rate of 23.7kboe on 31 December 2022. Unfortunately, logistical constraints are still preventing the company to operate at full capacity. In that regard, the 2023 guidance projects no sales through the North Peruvian Pipeline (ONP) during the year. Instead, all of the production will be sold via the Brazilian route and to the Iquitos refinery.

{kind=link}

The ONP is still being attacked and dealt intentional cuts, which creates oil spills and makes the locals hostile towards the oil industry. While repairs are underway, It's doubtful that given the current political crisis and social unrest in Peru, the issues with the pipeline will be resolved, so the decision of PetroTal not to use that route seems logical.

Routes capacity and economics (PetroTal)

{kind=link}

The Brazilian route also comes with risks as in late November a river blockade was established by a local indigenous group and a barge with PetroTal's oil has been detained with the crew taken hostage for 48 hours. The issue has been resolved since then and river access restored, but the risk of the situation repeating should not be crossed out. Also, low river levels could impact the loading capacity of the barges, so the company plans to ship 13.2kboe of daily production via that route, below its capacity of 14k-18k boe of daily production with the remaining 1.3kboe/day going to the Iquitos refinery. In the future, options for expanding the barge fleet and hence the capacity of the Brazilian route could be examined.

Liquidity and results guidance

The company reported on 9 Dec that it reached an agreement with Petroperu and established a schedule for the payment of a total of US$64M of receivables with US$10.9M of it paid shortly after. Despite the political turmoil in Peru, it appears that the state owned utility keeps making payments to PetroTal as the amount paid out reached US$16.1M as of 16 Jan, when the 2023 budget and guidance were released. The monthly installments are expected to continue up to 1 August, when the total of US$64M should be reached.

{kind=link}

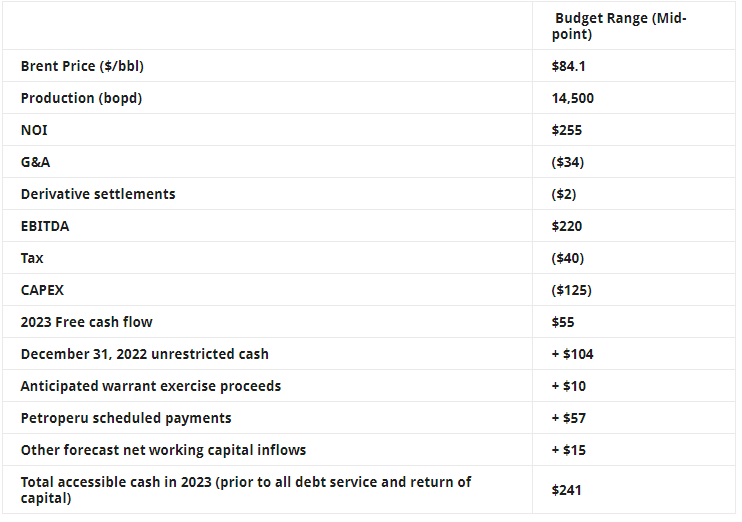

As far as results guidance goes, management projects EBITDA of US$220M in a US$84.1/barrel Brent price scenario. After accounting for taxes and US$125M of CAPEX, FCF is projected at US$55M. Under certain assumptions of warrant exercise and changes in net working capital, PetroTal may end up with US$241M of available cash (US$161M after accounting for the expected US$80M bond retirement). Given that, management intends to maintain a liquidity buffer of US$50M and distribute the available cash above that level in buybacks and dividends. Under the 2023 plan, this would imply over US$100M of shareholder returns.

Valuation

As of 30 Sept, PetroTal had 859.3M shares, which puts the market cap at around US$440M. For the net debt position, I'll take the unrestricted cash and equivalents of US$104M, add to them the scheduled receivables payments of US$57M and subtracts the US$80M of bonds and leases of US$20.2M. The resulting EV of PetroTal is US$380M.

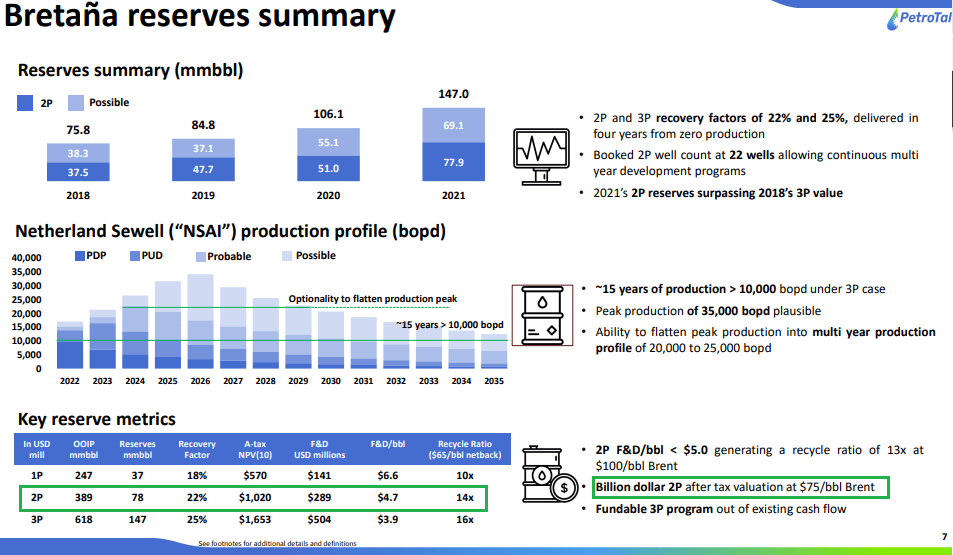

Bretana field economics (Petrotal)

{kind=link}

At the same time, the 2P reserves at the operating Bretana field are estimated to have indicated NPV of US$1,020M, discounted at 10% under a US$75/barrel Brent price scenario. Using this number as a proxy for the fair value of the EV gives a target share price of PetroTal of US$1.24 or 146% upside to the current price. Note, that the calculation doesn't assign any value to the highly prospective Osheki Kametza field of Block 107.

Looking at the Forward EV/EBITDA multiple in relation to other oil companies, operating in Colombia and Argentina, which have comparable political risk to Peru, PetroTal is on par with Parex Resources ( OTCPK:PARXF ) with the lowest multiple amongst the group. And this is despite the Colombian companies being subjected to some sort of a windfall tax, while there is no such policy in Peru.

The situation in Peru

Following the arrest of the president Pedro Castillo, Peru has been shaken by large protests and social unrest. The situation remains tense to this day. While the demonstrations are primarily concentrated in big cities, the capital Lima in particular, some mining operations have been disrupted . The last update from PetroTal didn't mention anything about disruption of operations, due to protest, so I would assume that as of now there are no issues. On the other hand, if the situation in Peru remains at its current state or even escalates further, the state owned Petroperu may not honor the established receivables payment schedule. Also, the chances of the ONP pipeline being repaired and its security strengthened are close to zero in such political and social environment. Without the ONP pipeline, reaching production at full capacity of 24kboe/day will not be possible in the foreseeable future.

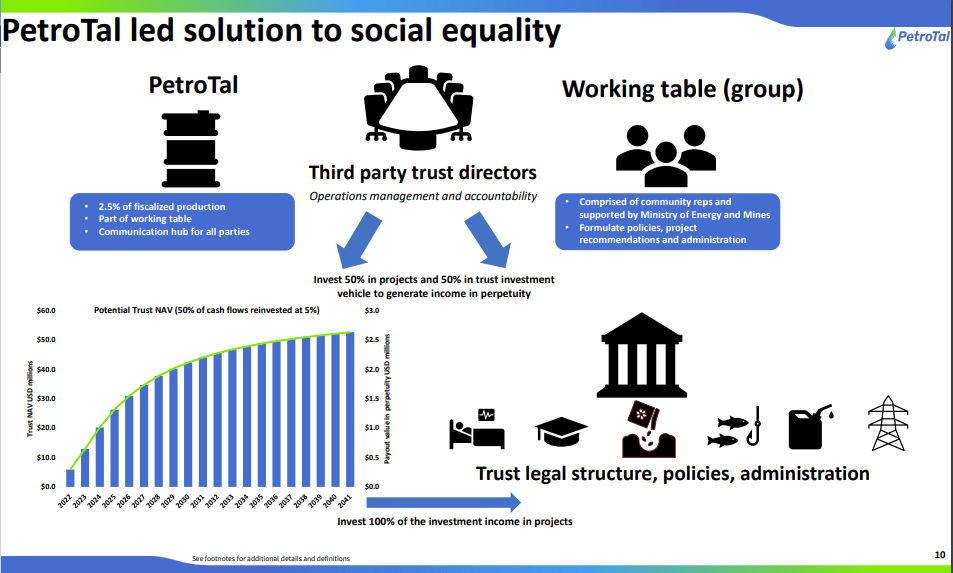

PetroTal's plan on community relations (PetroTal)

{kind=link}

The best that PetroTal could do is to keep good relations with the locals, which could reduce the risk of further river blockades on the export route to Brazil. In that regard, the company plans to spend US$18M for various social and community programs in 2023 alone.

Conclusion

PetroTal appears to be one of the most undervalued oil companies. When the company is valued at the estimated NPV of the 2P reserves of the operating Bretana field, the upside is 146%. At the same time, logistical issues persist, exacerbated by the worsening political climate in Peru. For that reason, while the potential reward looks very attractive, I think that only investors with high risk tolerance should consider the stock.

For further details see:

PetroTal: Navigating Through The Peruvian Turmoil