CA - Peyto Exploration & Development: Offers An 11% Dividend Yield With Natural Gas

2024-01-02 10:30:00 ET

Summary

- Peyto Exploration has hedged a substantial portion of its near-term natural gas production while offering exposure to higher average prices in US markets.

- The company's quarterly production has been declining due to reduced capex and extended downtime at a gas plant.

- The recent acquisition of Repsol's acreage is expected to be accretive in the long term, with lower decline rates and increased processing capacity and capital efficiencies.

Introduction

After the first quarter of the year, I thought Peyto Exploration ( PEY:CA ) (PEYUF) offers good exposure to the natural gas price . Unfortunately, the natgas price hasn't really been cooperating in 2023 and although Peyto's share price performed pretty well up to November, it has recently come down again.

Navigating through an era of lower natural gas prices

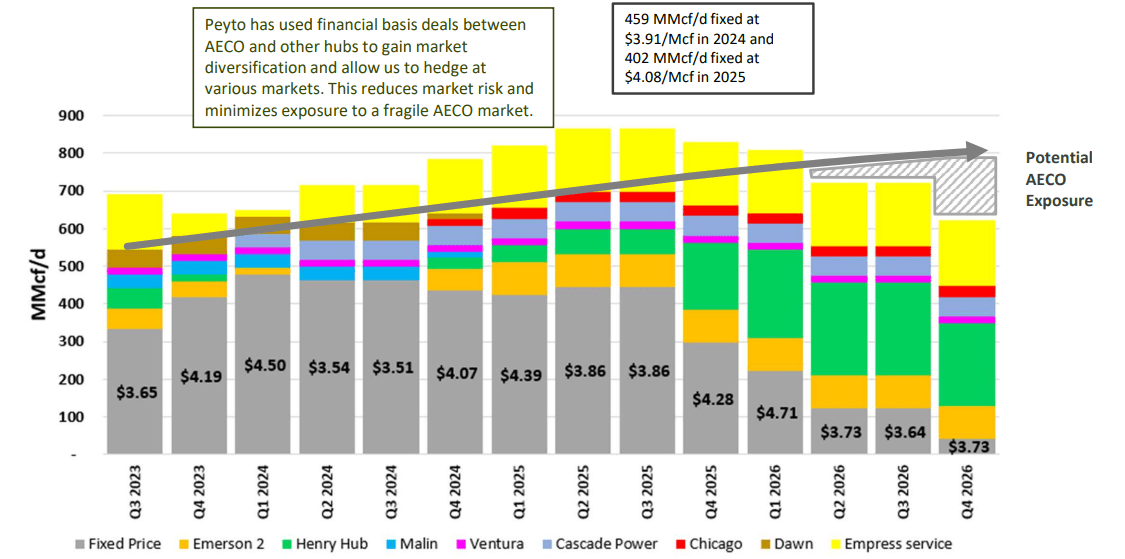

Before discussing the most recent financial results in greater detail, one of the reasons why I like Peyto a lot is its diversification as to where it sells its natural gas . While a lot of Canadian producers are being held hostage by the usually weaker AECO natural gas price, Peyto has hedged a substantial portion of its near-term natural gas production and offers exposure to several other end markets, including plenty of US-based selling points where its output commands a higher average price.

{kind=link}

As the image above shows, the company has no exposure to AECO based price fluctuations until 2026 where after a small portion of its production may be exposed to AECO prices - although I expect the company will address this closer to 2026.

During the third quarter, Peyto produced an average of almost 98,000 boe/day , of which about 88% was natural gas with the remainder of the oil-equivalent production consisting of NGLs.

{kind=link}

As you notice in the image above, Peyto's quarterly production has been declining and that's due to the reduced capex program by the company due to the lower commodity prices. Additionally, there was some extended downtime at a gas plant during Q3 which had a negative impact of approximately 1,000 boe/day on the average daily production rate.

The average natural gas price during the quarter was approximately C$2.57 but thanks to the aforementioned hedges and access to diversified markets, there was a hedging and diversification gain of approximately C$0.76 per Mcf which resulted in a net realized natural gas price of C$3.33 per Mcf.

{kind=link}

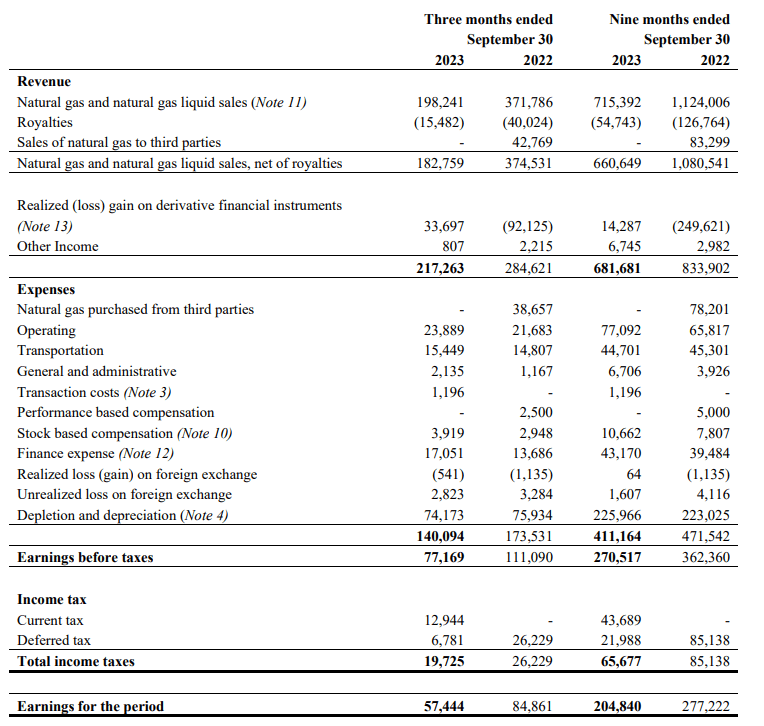

The company reported a total revenue of C$198M before royalties and hedges and a net revenue of C$217M after taking almost C$34M in hedging gains into account. The income statement below shows the exceptionally low-cost nature of Peyto's operations and despite its access to US markets, even the transportation costs are very reasonable.

{kind=link}

The pre-tax income was approximately C$77M which resulted in a net profit of C$57.4M resulting in an EPS of C$0.33.

The cash flow result shows a similar strong result. The reported operating cash flow was C$139M and after taking the working capital changes and lease payments into consideration, the adjusted operating cash flow was C$145M. Plenty of cash to cover the C$98M in capital expenditures.

{kind=link}

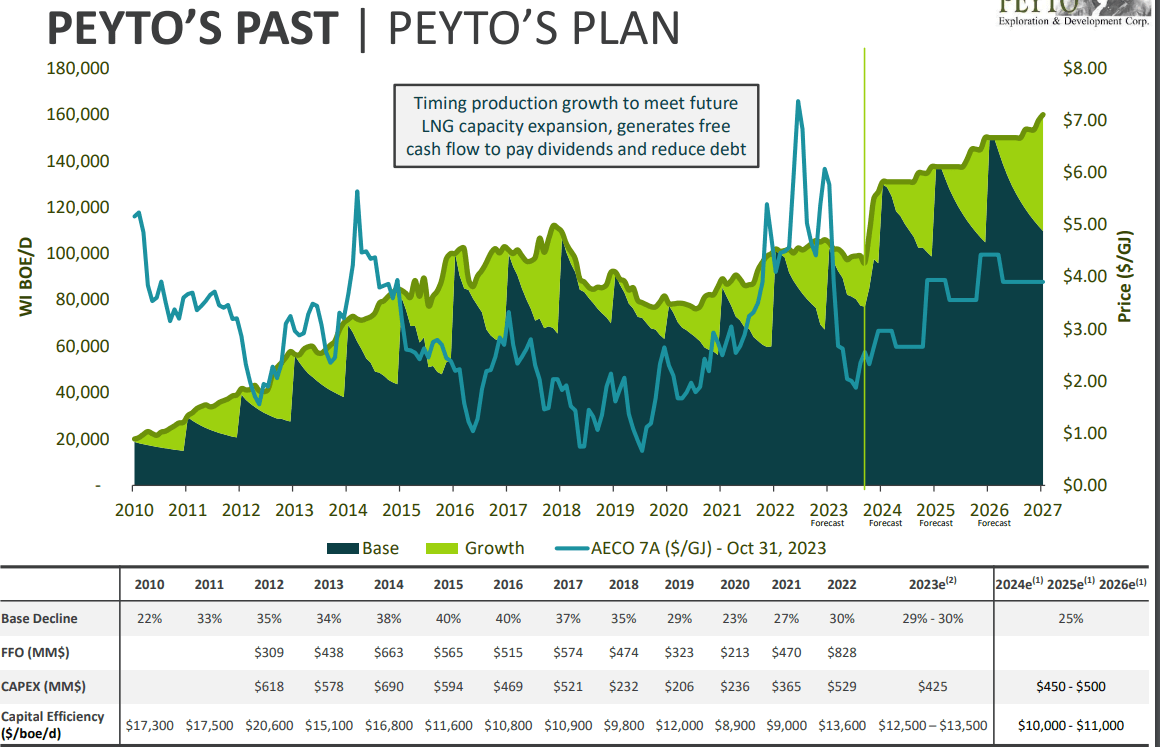

This means there was an underlying free cash flow of C$47M for a result of approximately C$0.27 per share. While that's not sufficient to cover the monthly dividend payments of C$0.11 per share, Peyto is investing in growth again and it expects to be able to increase its production rate using a capex budget of C$450-500M per year, going forward.

{kind=link}

The image above also shows an anticipated decline rate of 25% which is substantially lower than the high-20% rate it has been experiencing lately. This is due to the recently closed acquisition of Repsol's acreage bordering the existing acreage of Peyto.

The Repsol acquisition: accretive in the long term

Subsequent to the end of the third quarter, Peyto closed the US$468M acquisition of Repsol's 455,000 acres of land in the Edson area. The acreage has an existing production of 23,000 boe/day of which 75% consists of natural gas. This will result in a slightly reduced natural gas ratio in the output expressed in barrels of oil-equivalent, which will decrease from 88% to 86%.

{kind=link}

The acquisition includes approximately 306MMboe of reserves in the 2P categories (indicating an RLI of approximately 36 years) and five gas processing plants with an utilization of just 35% which means the consolidated area now has an utilization of 52% providing plenty of processing capacity for future production increases. As the acquisition comes with 2,200 kilometers of pipelines, the acquisition provides Peyto with some low-cost growth opportunities.

And equally important: the decline rate of the acquired assets is just 12% and that's what's reducing the consolidated decline rate on the current production basis of 123,000 boe/day.

{kind=link}

The Repsol assets haven't been drilled in a while, and it will be interesting to see how efficient Peyto can increase its production rate. The company expects an efficiency of C$10,000-11,000 per flowing barrel of oil-equivalent which means the sustaining capex to keep the production at 123,000 boe/day will be just C$325M (25% of 123,000 multiplied by the midpoint of the efficiency guidance).

Investment thesis

This means the current generous dividend of C$0.11 per share per month is actually covered by the sustaining free cash flow while the Repsol acquisition will even improve the efficiencies. If we would ignore the Repsol acquisition, the 30% decline rate on the pre-Repsol production rate of 100,000 boe/day indicated the company had to replace about 30,000 boe/day of production, at a cost of C$13,000 per flowing barrel resulting in a sustaining capex need of C$390M. Thanks to the additional efficiencies, the total sustaining capex may even decrease as Peyto can focus on the lower hanging fruit.

The company currently has a net debt position of C$1.3B which is pretty high but still manageable in the low natural gas price environment. The dividend will cost the company approximately C$256M per year and while the dividend will likely be fully covered in 2024, Peyto may prefer to reduce its dividend and pay off debt.

I currently have no position in Peyto, but I am considering to go long as I like the acquisition and the anticipated capital efficiency improvement. It is too bad none of the senior notes are listed on any exchange as I definitely would have liked to be a creditor of Peyto as well.

For further details see:

Peyto Exploration & Development: Offers An 11% Dividend Yield With Natural Gas