CA - Peyto Exploration: Insiders Still Making Acquisitions

Summary

- The spate of acquisitions by a management that usually does not acquire is significant to investors.

- I usually do not have a sell price goal until I see a lot of industry insiders selling. Right now, they are clearly on the buy side with Peyto Exploration & Development Corp.

- Finances are conservative enough for Peyto Exploration & Development Corp. to acquire, grow production, and repay debt.

- The move into rich gas should continue conservatively with an eye on increasing profitability and tight cost controls.

- Peyto has only lost money one time since it went public. For a cyclical company, that speaks volumes about profitability.

(Note: This is a Canadian company that reports in Canadian dollars unless otherwise stated.)

Peyto Exploration & Development Corp. (PEYUF) (PEY:CA) is the latest of a long list of managements that I follow that are still making acquisitions or gaining control of companies because they believe that their industry is cheap. What is particularly significant about Peyto is that management usually does not make acquisitions. Yet this time around they have made several. That is a huge insider vote that this management believes (along with a lot of others) that the industry is cheap.

People often ask me about a price goal. But as long as I see insiders getting into the industry along with others buying, there is no reason to consider selling. Just as industry insiders are voting by a wide margin to get in, there will come a time when you see a lot of insiders getting out. That is the time to think about a sales price goal and consider getting out of all but potential core positions that you want to keep for a long time.

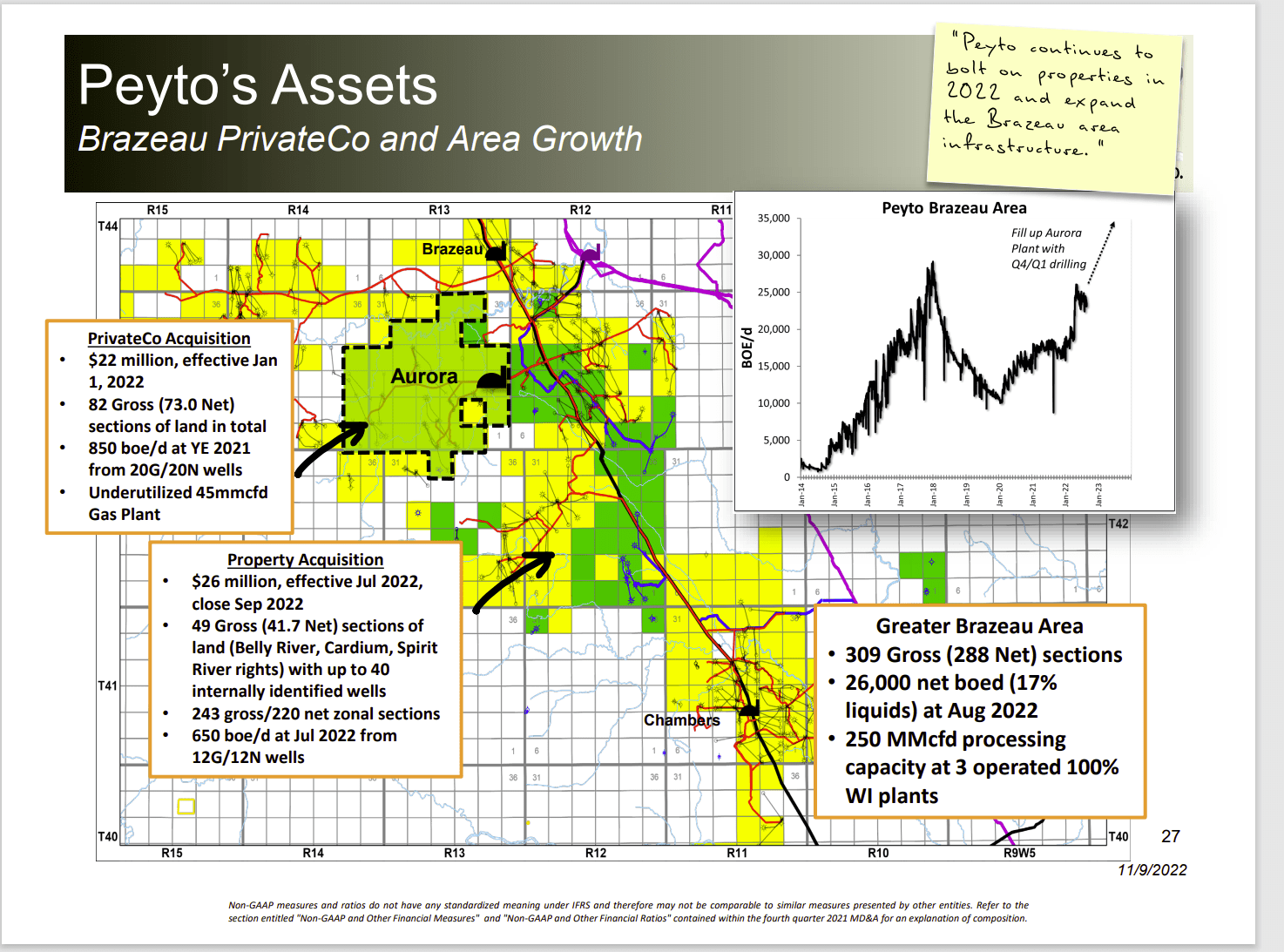

Peyto Presentation Of Latest Acquisitions (Peyto Corporate Presentation November 2022)

{kind=link}

Peyto began the year with the Cecilia acquisition and now has added more to the company holdings. This is not a company known for growing by acquisitions at all. The fact that management has now considerably varied from history is extremely significant to investors.

Management also mentions farm-in arrangements as well. This has long been a company that has bid on sections to add to its holdings and then built the supporting infrastructure itself as well as developing the acreage.

Bolt-on acquisitions have a long history of being safer than average. Small acquisitions like the ones shown above are also considered lower risk. So, the company is not really varying from the conservative strategies it is known for. Rather, management is taking advantage of low prices caused by owners of smaller holdings who "want out" after the experience of the last several years.

Peyto management knows the area and the operators rather well due to the proximity of the acquired land to Peyto's own operations. So, there are very likely not going to be many "surprises" that often come with acquisitions.

Investors can likely suspect that management will soon revert to an organic growth strategy that has predominated throughout the history of the company.

Conservative Move To Liquids

Management a few years back had decided that a move into liquids was justified after years of natural gas price declines. This formerly dry gas producer has been slow to produce more liquids because technology advances and natural gas price increases have made the move less pressing than was the case in the past.

The very low costs of Peyto made the business unusually profitable. Therefore, the need to diversify was not as strong here as was the case with other producers. There has also been a management goal that liquids production operations successfully compete for capital. While that has slowed the diversification effort, it has also kept profitability decent.

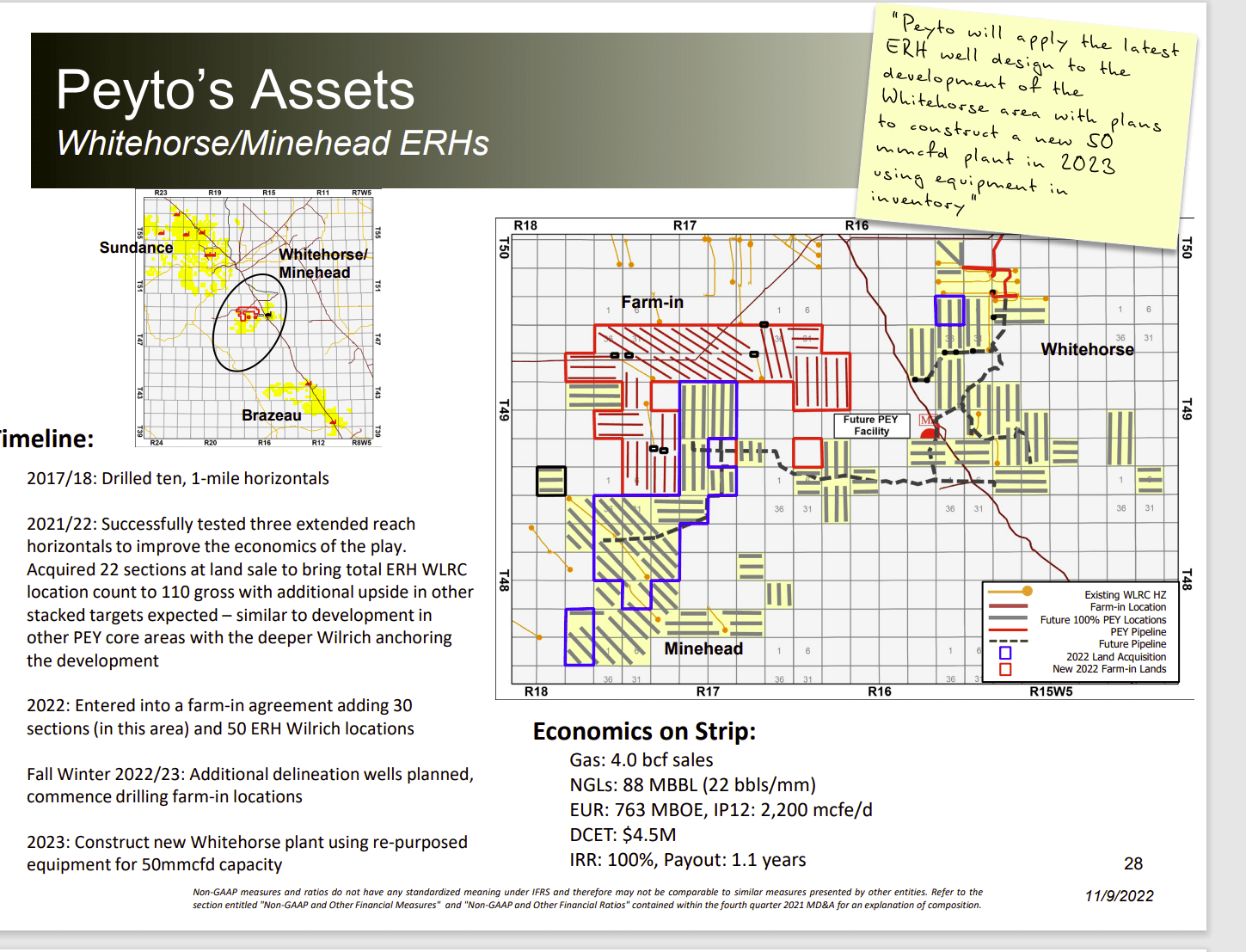

Peyto Description Of More Liquids Production Example (Peyto Corporate Presentation November 2022)

{kind=link}

Much of the industry would call this "rich gas" production. What is making this move competitive with the dry gas operation is longer horizontal wells (known as extended reach). This new technology is being "tried out" by management. Management has enough faith that the company is now clearly moving into this part of the industry after years of solely dry gas production.

But it also clear that management wants more data before they go into full development mode. Also, many of the processing plants owned by management were modified to handle the liquids being produced.

The "name of the game" is to keep costs as low as they were with the dry gas production while pocketing the increased value of rich gas production. This is actually spreading throughout the oil and liquids part of the industry which is leading to lower costs and of course lower corporate breakeven points. Of course, superior geology still wins out. But the public may be in for a generation of lower prices than anyone thought possible due to the cost progress being made.

Cost Control

Peyto Exploration & Development Corp. management constantly notes that this company only ever lost money in one year. The impairment charges that were incurred for the first time have come back, as Canadian accounting allows the recovery of impairment charges once an industry recovery is underway enough to determine that the impairment charges should be reversed.

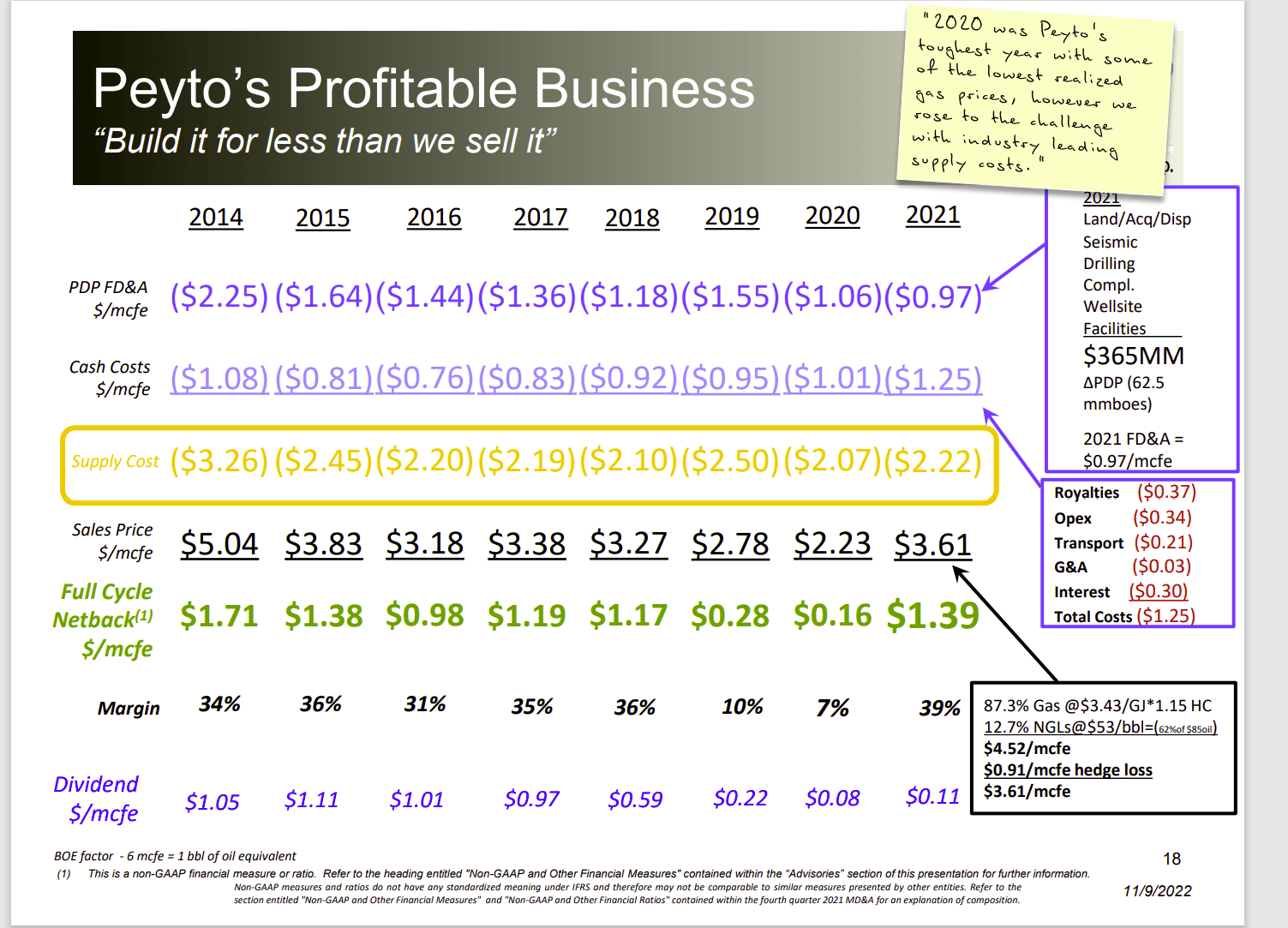

Peyto Full Cycle Netback Monitoring (Peyto Corporate Presentation November 2022)

{kind=link}

Notice that the continuing trend for PDP FD&A is down. This is a cost leader that intends to maintain that cost leadership. Not many investors are aware that many commodity industries face the prospect of reducing costs every year to maintain competitiveness. Few companies are as blunt about that prospect as Peyto Exploration & Development Corp.

The next line about cash costs for production and transportation (mainly) will bounce up during times of robust commodity prices because royalties and transportation tend to move up. In the current case, the increase in liquids in the product mix will push both up more than expected because the costs for both are higher.

What is declining is the interest cost, because this company is able to repay debt and grow at the same time. There were arguments during the cyclical downturn that the debt was too high. That is clearly not the case when management can make cash acquisitions, grow production, and repay debt. The companies I follow with "too much debt" are solely repaying debt. If they make acquisitions at all, they use stock so that the acquisition lowers key debt ratios.

Takeaways

It is important to look back to review whether management made the right steps about debt, dividends, and growth during the downturn. There will be another cyclical downturn in the future. Investors can learn a lot from conservative situations when compared to the risk-taking situations. Peyto Exploration & Development Corp. clearly was a conservative company.

The brisk acquisition pace engaged in by management is likely to cool off in the future. In the meantime, it is clear that there were a lot of discouraged small owners throughout the industry that want out in the current environment. This is a management in position to take advantage of that trend while growing production.

The dividend was recently increased again. This is a variable distribution entity that can have a place in an income portfolio for those that can afford it. Management has also grown the company considerably since the company went public.

A capable management can usually conduct business so that the stock price at a minimum will exceed the old cyclical high price of the last cycle plus inflation. This management is likely to do a lot better. That may mean that the future income received on these shares could well be worth the effort for investors that have to pay withholding.

Recovery parts of the business cycle are often very underestimated by investors that just got through a brutal downcycle. That makes this still a contrarian opportunity to invest while many still remember the last few years and "want out." The finances and the low stock price currently make Peyto Exploration & Development Corp. attractive even for more conservative investors.

For further details see:

Peyto Exploration: Insiders Still Making Acquisitions