CA - Peyto: Mud Slinging

Summary

- Flying mud in July means that activity will be minimal until things dry out.

- This condition may weaken some ROEs of wells that are usually hooked to production faster.

- Whether management can completely overcome the weather challenge remains to be seen.

- Costs have declined and are likely to continue to decline. The slow move into more liquids production is likely to slowly continue.

- The margin in fiscal year 2021 was the best in some time on lower average selling prices (than was the case in 2015).

(Note: This article appeared in the newsletter on July 16, 2022 and has been updated as needed.)

(Note: This is a Canadian company that reports in Canadian dollars unless otherwise noted.)

The presidential report of Peyto (PEYUF) for July is out and the first thing that mattered is all the mud that has kept activity at a crawl. Spring Breakup has been unusually muddy and long. Thank you June rains. The equipment obviously has issues when the roads are mud as that mud flies everywhere while the equipment sinks. So, the second half of the fiscal year will get off to a slow start. Any possible weak volume comparisons will be due to the weather that hindered completion activities.

Sure enough, by the time the August presidential report came out, then management was dealing with bottlenecks as they were trying to get things back in shape for the very important winter heating season.

Management is concerned because they try to bring as many wells as possible online in time for the important heating season. Good prices obtained when the wells initially have that high (and rapidly declining production) can add an important percent or two (sometimes more) to the ROI of the well. In an industry where every extra penny generally gets to the bottom line with minimal deductions, such considerations matter a great deal.

Afterall, profits in the industry are a relatively small percentage of revenue (usually). So, that extra penny or so often makes a decent difference between a fair quarter and a great quarter.

The net effect of the weather will be to transfer some starting volumes from the third to the fourth quarter. Now whether the company can completely overcome the mud issue will remain to be seen. Mother Nature obviously does not have the same timetable as management. So, the mud issue could (and did) last longer than desired. Then came even more challenges. This is nothing new for the Canadian industry. But it does help understand the unpredictability of challenges on the way to profits.

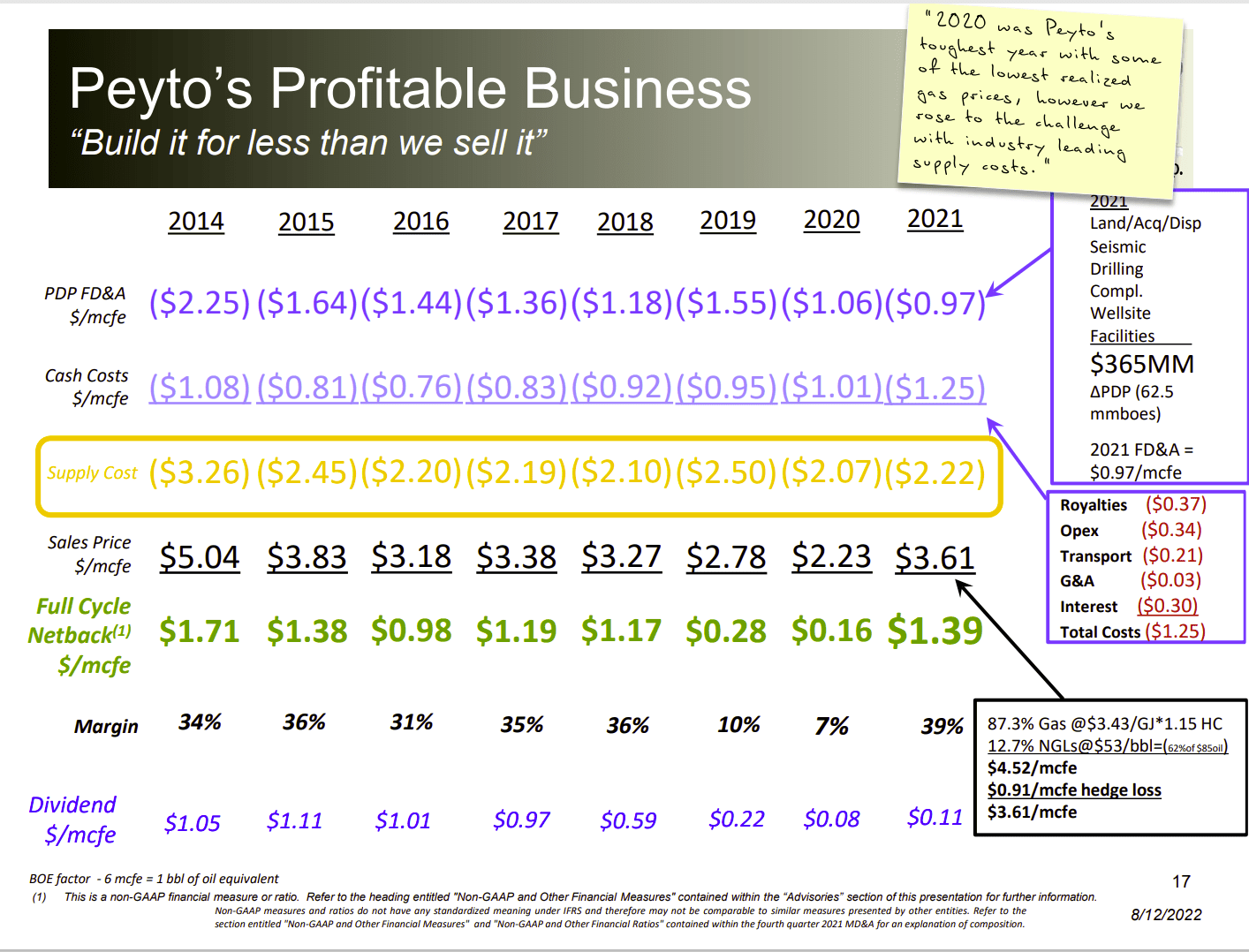

Peyto Cost History

The Canadian dollar advantage gives this company some of the lowest cost North America of any basin.

{kind=link}

Peyto Margin HIstory Before Impairments (Peyto August 2022, Corporate Presentation)

The company has had its best margin year in 2021 since 2015. That was accomplished with a lower average selling price. Any commodity business has to continually lower costs to remain competitive. Peyto has maintained some industry leading costs despite a conservative venture into high liquids production.

This dry gas producer was squeezed in fiscal years 2019 and 2020 when gas prices were extremely weak in Canada. The venture into liquids production has not been very fast because costs are so low that the coming industry recovery returned cash flows to robust levels that have lasted to the current time.

Furthermore, this management plays the same "game" or as the same strategy as many dry gas producers that ventured into more liquids. That objective is to keep costs at dry gas levels to pick up the benefits of liquids in the margins. As shown above, management is largely succeeding in keeping costs down.

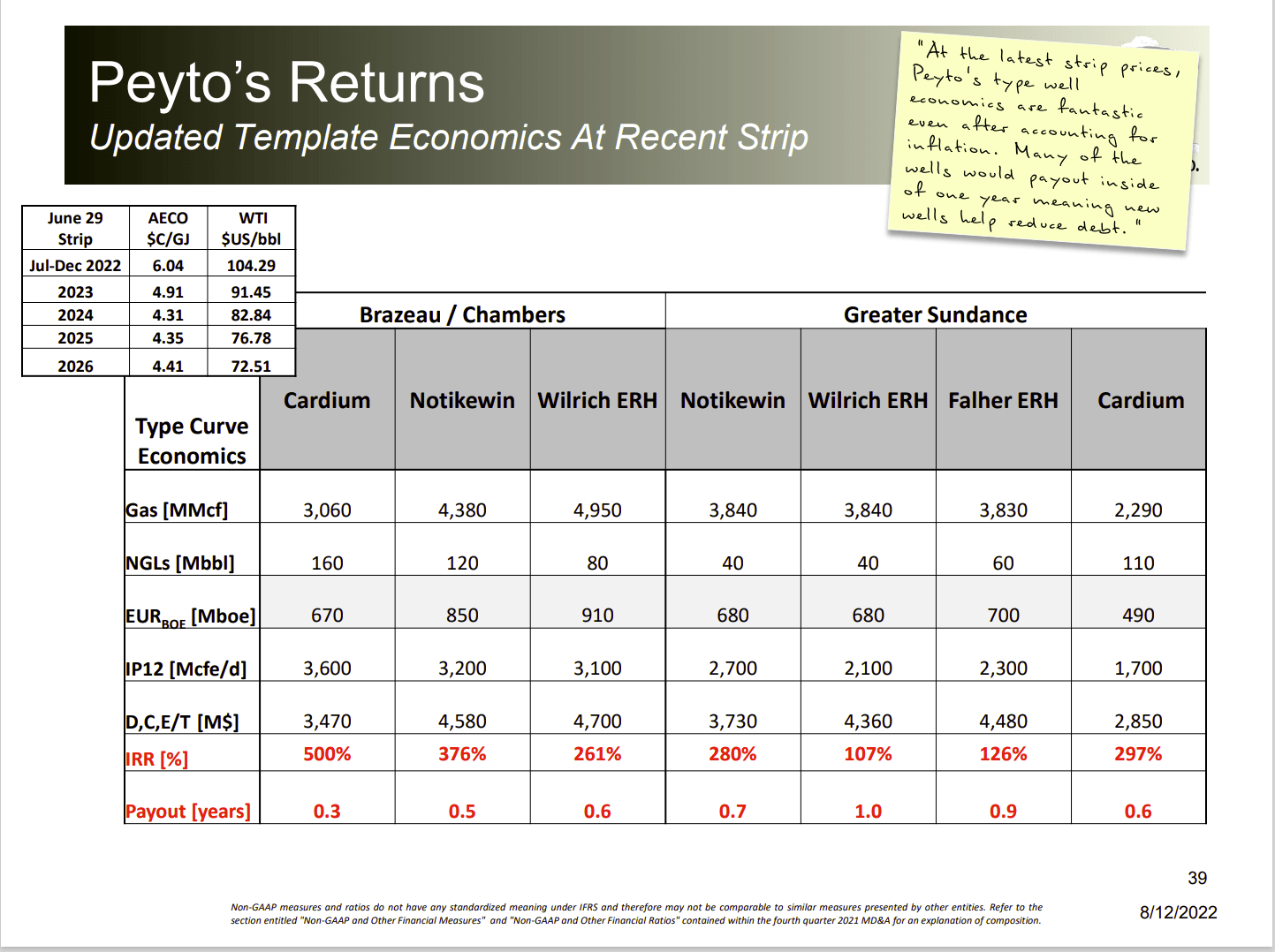

ROI Leadership

A quick survey of areas of operations is definitely encouraging.

{kind=link}

Peyto Well Profitability At Different Location (Peyto August 2022, Corporate Investor Presentation)

A whole lot of companies like this one are experiencing an unusual amount of profitability. As exporting ability increases in the United States, the natural gas pricing cycle probably will join the world pricing cycle in the future. That world pricing cycle is a good deal higher than is the case in North America.

In the meantime, the current environment has wells paying out in record short time periods. Many of these companies can report a satisfactory minimum well profitability with all costs recovered in less than a year.

Now the industry emphasis is on shareholder returns and lower debt levels. But the increasing emphasis on cost reduction means that more wells can be drilled with the same capital. Peyto management has reported in the past from time to time, the ability to add some wells to the capital budget because cost savings were significant enough.

As debt levels decline, less cash will be needed to service the remaining debt. That lower debt service costs will also free more money to potentially spend to expand production. The industry has never been able to resist high prices for long. On the other hand, fiscal year 2020 did do a fair amount of damage to a lot of balance sheets and it also caused the debt market to become more conservative. Therefore, an initial financial adjustment should be expected by investors (and consumers). But if the past is any guide, robust growth will resume at some point to bring about the next cyclical downturn.

Probably one of the biggest discussions brought in the presidential newsletter is that the industry discussion should be about maximizing return " ON " capital not return " Of " capital. This because a lot of professional investors do not want their capital back. Instead, they want it to continue to build wealth. That is why they invested in the first place.

Many investors lost money in past business cycles because they did not do their due diligence or properly monitor their investments in this very low visibility industry (fast moving too). The result is they want their money back before they can fear losing it. However, wealth building in the industry is a very different ballgame where you accept aborted cycles like the last one as part of the risks in this industry. Planning for it to happen again as Mr. Market tends to do is counter-productive even if it is predictable. Simply put, you cannot move forward in this industry by constantly fearing ghosts of the past. All you can do is your best as the future unfolds.

Profits

The result of everything is that this company is a profit leader that usually (but not always) avoids impairment charges. There are a lot of companies in the industry that report decent profits during the good times because they conservatively wrote-off as much as possible during the downturn (while blaming it largely on the lower of cost or market calculation).

Here, in Canada, the accounting rules allow those impairments to reverse as the industry recovers. That is not the case in the United States. Therefore, in the United States, the "accounting game" is to write off as much as possible so the coming recovery makes the company look as profitable as possible. Canada largely eliminated that game through the reversals of impairment charges.

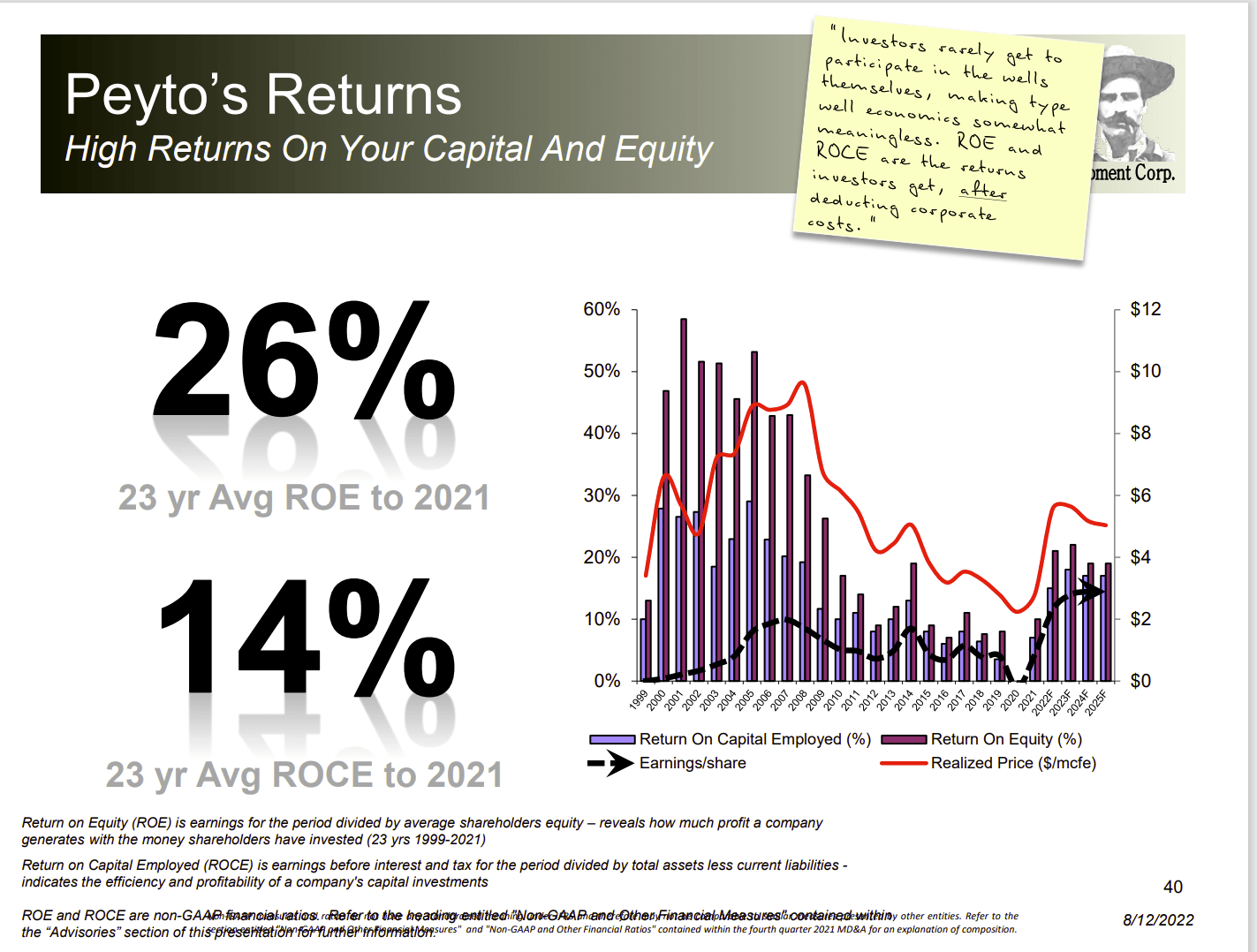

{kind=link}

Peyto Profitability History And ROCE History (Peyto August 2022, Corporate Presentation)

The first thing I look for in any cyclical industry is average profitability. This company has an average profitability that is hard to beat no matter the measure.

The profitability comes from a relentless focus on costs along with considerable midstream integration. This company owns most of its gas plants and the corresponding pipelines up to the connection to long haul pipelines that get the product to market.

The ownership of midstream assets helps to shield the company from some of the upstream volatility. A focus on costs "every step of the way" also protects the combined corporate profitability. Many times, diversification fails because management does not keep all parts of the diversification sufficiently profitable. That is typically when spinoffs happen.

The Future

Management will continue to focus on decreasing costs while increasing average revenue through a continued slow transition to more liquids. Management did purchase some liquids rich acreage awhile back. But a lot of areas in Canada already had liquids rich intervals that just were not profitable to produce until recently.

There is talk about the Tier 1 acreage being used up. But investors need to remember that Tier one acreage when I grew up was a 3,000 foot vertical well that flowed at least 200 BOD (and did not unexpectedly dry up). We have come a long way since then. It is very reasonable to assume that improving technology will continue to unlock previously non-commercial intervals and leases while moving locations into Tier 1.

Most oil and gas companies report increasing reserves and increasing locations to drill every year. It can be lumpy as innovations are not predictable. But the long-term outlook still appears to be favorable for growing reserves.

Similarly, the long-term outlook for petroleum products is still very positive. Many are used to produce products used in the green revolution. Natural gas itself is the preferred source for hydrogen (currently).

That makes a company like this a very good long-term consideration. Note that Canadian companies tend to be far less wedded to a dividend level. So, the dividend definitely needs to be considered as variable.

But as a profitable natural gas producer, this is one of the better companies to consider for investment.

For further details see:

Peyto: Mud Slinging