CA - Peyto: Pedal To The Medal

Summary

- Stock repurchases will not happen.

- The aim is to be the most profitable primarily natural gas producer.

- Management will pay a dividend that appears to be reasonably maintainable. It will be increased using the same considerations.

- The expansion into Brazeau appears to offer a profit improvement opportunity.

- The full cycle netback may be the best in a long time (or even ever) in fiscal year 2023.

(Note: This is a Canadian company reporting in Canadian Dollars unless otherwise noted.)

Peyto ( PEYUF ) is a company where being the best, growth, and more profits come first. Management stated d uring the latest conference call that there will not be stock repurchases at this company. Management firmly believes that the shareholders pay them to be the best they can be, and the goal is to grow that best to the extent possible.

In line with management's thinking is that they will establish a dividend that grows over time. But they avoid the idea of a "base dividend" because they saw commodity prices head to zero and less. As management put it, if you don't have commodity prices then you also do not have a dividend. So, there is no sense going out on a limb to state that there will be a "base dividend".

The other thing about a dividend is a management resoluteness to grow the business. While a return to shareholders is important, this management believes that the return should be from profits. The CEO and others have long noted that they do not want their capital back (as long as it makes money) because then they have to find another way to make that capital earn a decent return.

So, this company is very much against the market demand of return of capital in the form of variable dividends and stock repurchases. That puts the company in a very small minority. But for any investor looking for a management that is very good at what it does, then this is probably the place to look.

Costs

The costs of this company are among the best in North America. This is especially true since the costs are reported in Canadian dollars which are generally worth less than United States dollars.

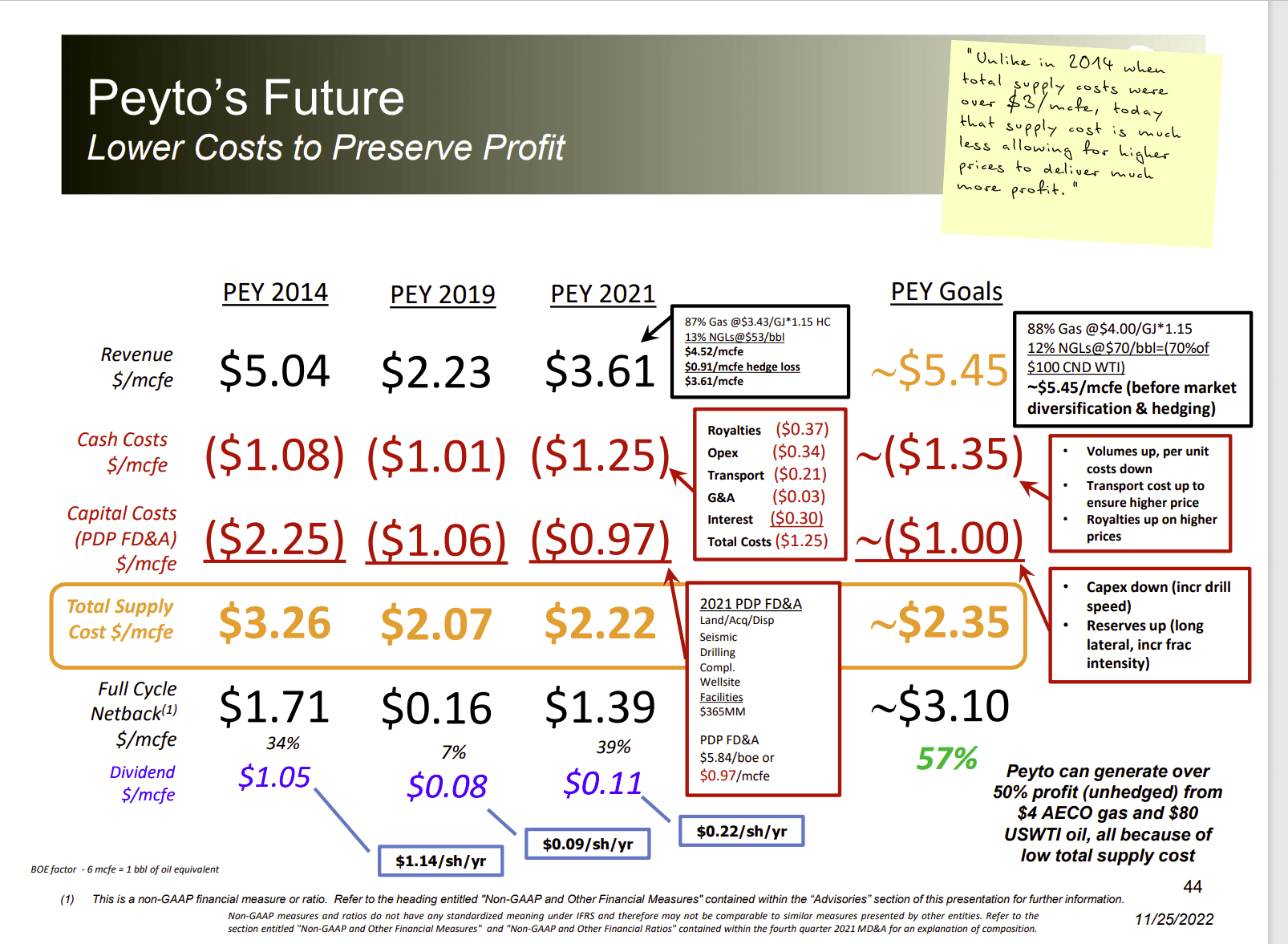

Peyto Historical Per MCFE Costs And 2023 Goals (Peyto November 2022, Corporate Presentation)

{kind=link}

The low costs should lead to a historically high margin for the company in the coming fiscal year. Management will hedge production to get away from some of the daily volatility of cash prices as well as to develop a reasonably predictable cash flow for both budgeting and dividend purposes.

This management made a lot of money from the hedging program in the past. That may not happen with prices generally in a volatile uptrend. But at least management "nails down" some of the robust cash flow.

Growth

Management will snap up bolt-on bargains when they are available. This is yet another insider taking advantage of a lot of sellers to increase profitable operations.

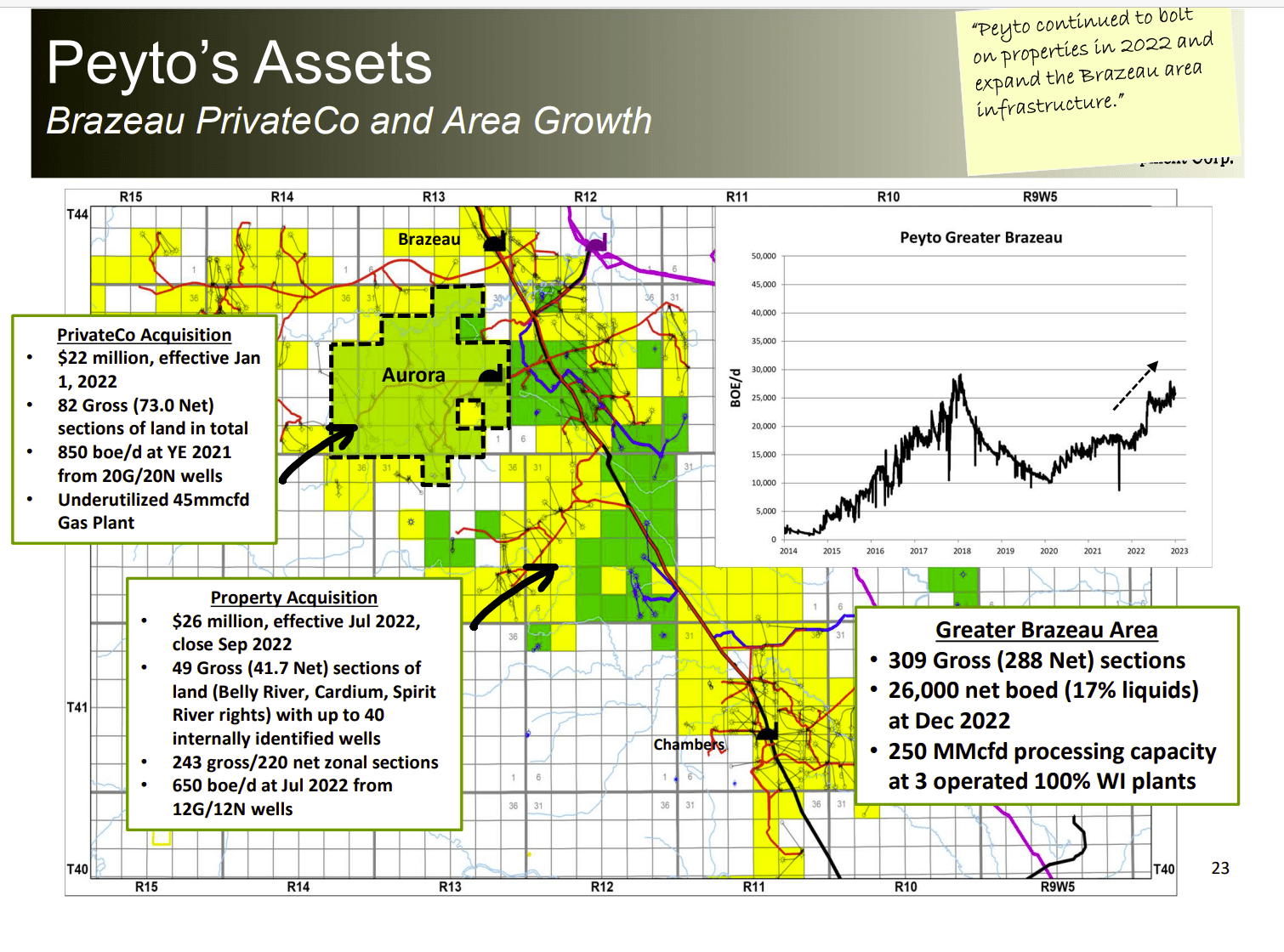

Peyto Growth In Brazeau Area Of Alberta Canada (Peyto January 2023, Corporate Presentation)

{kind=link}

The company has purchased a lot of land in the very profitable Brazeau area of operations. As you can see, Canadian land is relatively cheap when compared to the American basins. In many cases, there is considerable infrastructure sold along with the acreage (as shown above). The end result was that management significantly increased the company presence in this area and gained valuable infrastructure with excess capacity in the process.

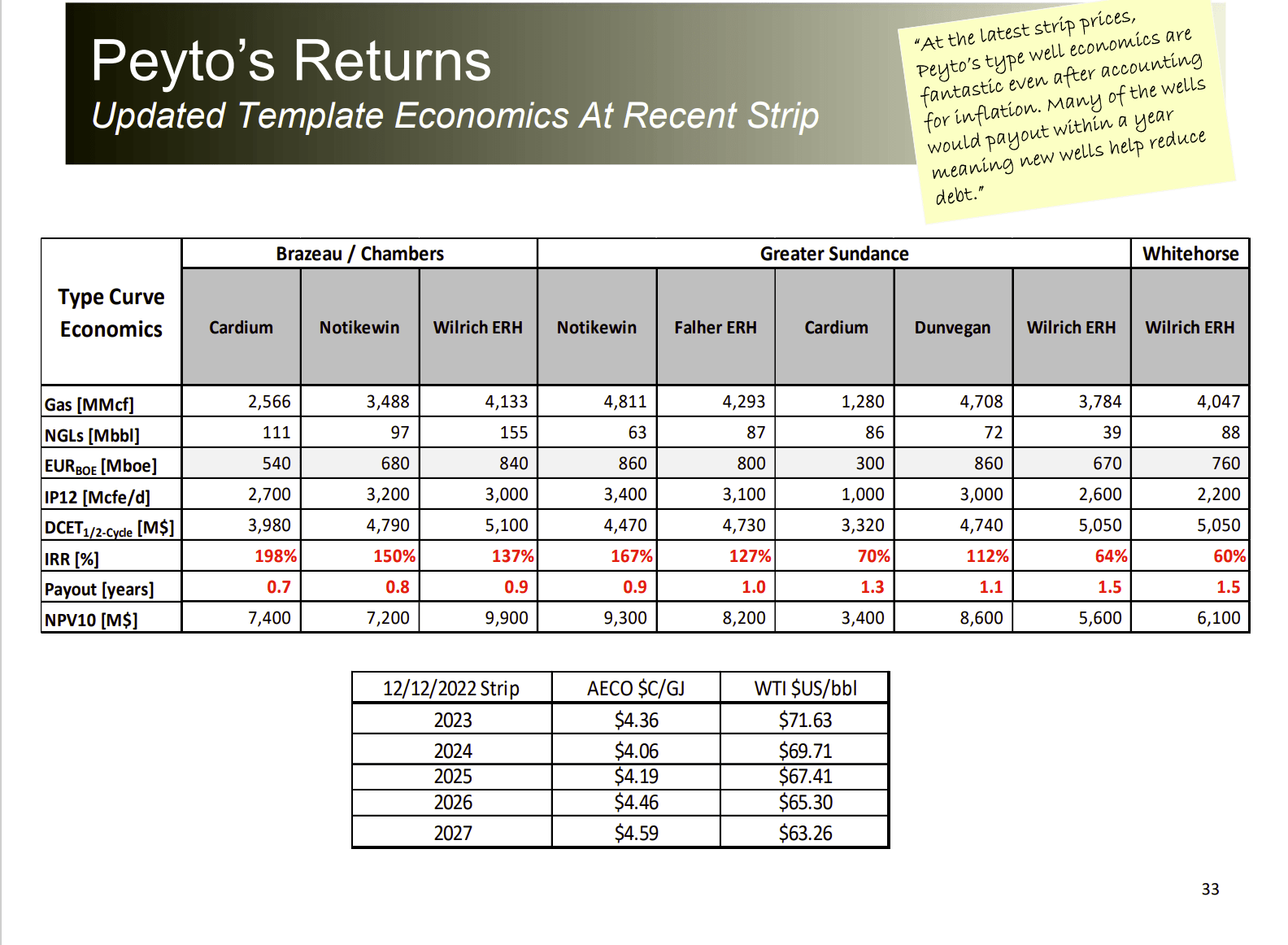

Peyto Well Profitability Table For Various Leasing Areas (Peyto January 2023, Corporate Presentation To Investors)

{kind=link}

The importance of expanding in the Brazeau area is shown above. Not only are the prices dirt cheap, but the returns rival the best in North America at current commodity prices. That means it would be hard to find a better deal in competing basins.

This formerly dry gas producer is slowly adding liquids production for profit flexibility. Natural gas is still roughly 88% of production. But that is down about seven points from a few years back when dry gas was around 95% or more of total production.

The result is that the more valuable condensate, other liquids, and oil now significantly influence the average selling price whereas in the past that was not always the case. This strategy will ensure decent profitability well into the future under a wider variety of commodity price scenarios.

Paybacks are fast enough that management can drill two wells with the same capital money in one fiscal year (sometimes more). That allows for a rapid cash flow expansion.

This management will usually try to initiate well production during the strong heating season because natural gas prices tend to be stronger then. So the initial production then receives higher seasonal prices. This helps to raise the return on capital invested in the well.

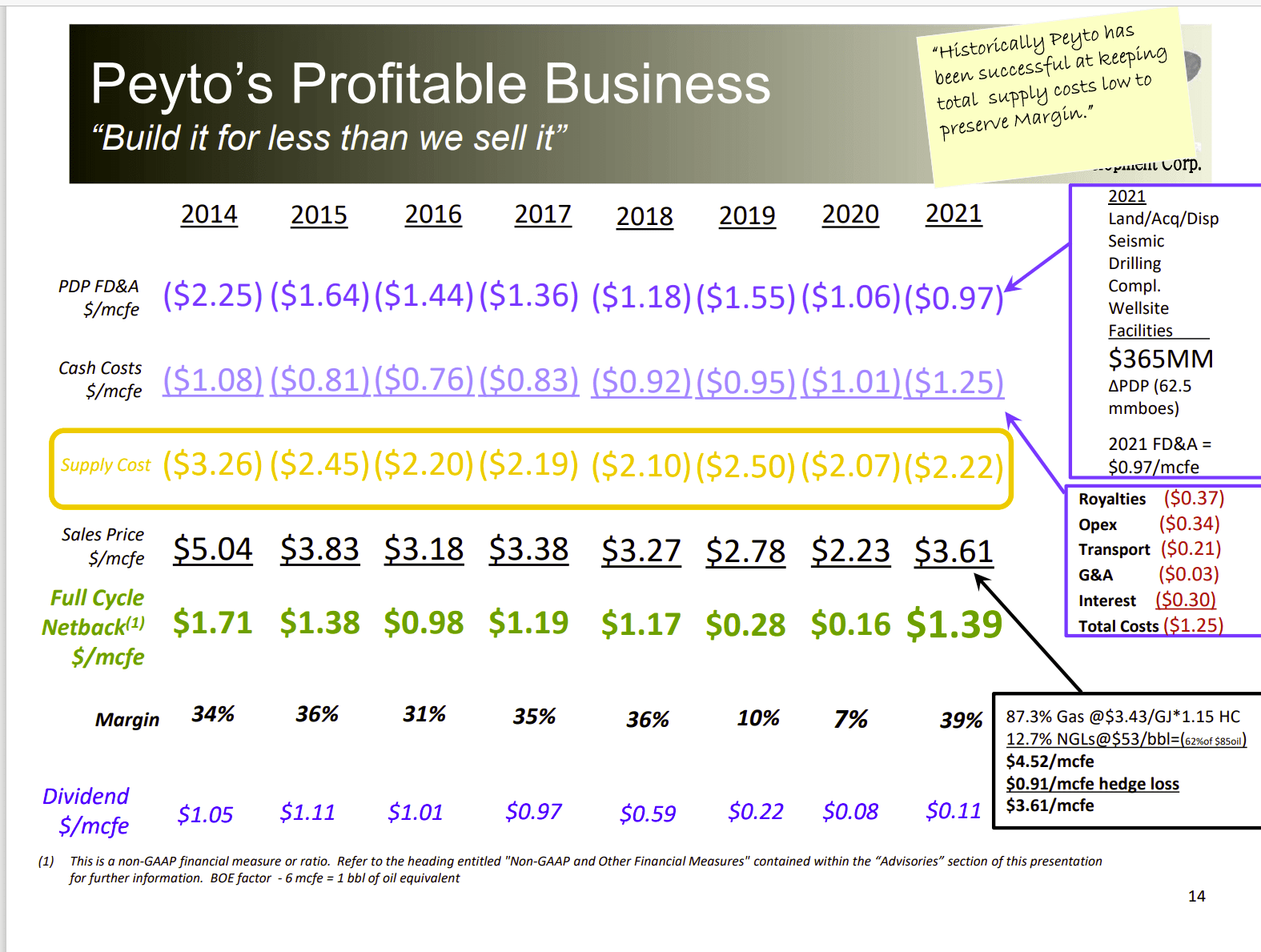

Peyto Cost and Profit History Through 2021 So Far (Peyto January 2023, Corporate Presentation To Investors)

{kind=link}

Management has long had a goal of a profitable netback throughout the industry cycle. As shown above, they come far closer to meeting that goal than does much of the industry. Fiscal year 2020 was the first time the company ever had to take an impairment charge. That is a sign of just how low the costs are for this company.

Fiscal year 2021 is on track to have one of the best netbacks in some years. The netback next year will be even better. The last few years have had uncharacteristic hedging losses due to the rising commodity prices that happen in any recovery period. Next year the hedges will be at better prices.

The expansion into the more profitable Brazeau area may lead to some margin expansion depending upon how management wants to grow production in this area. Many times, it pays to "not go out on a limb" because the profitability of basins often changes as technology marches forward. Therefore, keeping all decently profitable areas moving forward is often indicated.

The Future

Peyto was one of the last natural gas producers to decide to develop some liquids rich areas of production. The low costs of production enabled this producer to remain a dry gas producer long after many competitors added liquids to increase profitability. At the time, no one thought the decline in natural gas production would last as long as it did.

Now the move into rich natural gas production has been with the aim of decreasing controllable costs even though some liquids costs are inherently higher than dry gas. The result is a very tight maintenance on costs so that much of the added value to the average selling price heads to the bottom line.

This management intends to repay debt while growing production and taking advantage of any bargain acquisitions that appear. By management's own admission, acquisitions are relatively rare. So, investors should take that as a sign that the industry overall is still cheap enough to consider buying. The time to sell is when these insiders are selling (usually the whole company) in decent numbers. Right now, is clearly therefore the time to consider investing.

For further details see:

Peyto: Pedal To The Medal