CA - Pfizer: Buy The Panic

2023-12-21 01:08:28 ET

Summary

- Pfizer stock has fallen 45% YTD as it has been impacted by the decline in revenue from COVID-19 products. The recent news about Danuglipron has added fuel to the fire.

- But is everything so bad when it comes to investing in the company for the long term? Let's figure it out together - read on.

- Pfizer is strategically positioning itself for long-term success by expanding its oncology capabilities and focusing on cost savings and acquisitions.

- I believe PFE stock looks oversold and undervalued due to likely underestimated EPS forecasts for FY2025 and beyond.

- So I suggest not buying this panic, but thinking about buying PFE instead.

Introduction

Pfizer, Inc. ( PFE ) is a leading global pharmaceutical and biotech company founded in 1849, and headquartered in New York. It specializes in discovering, developing, and manufacturing biopharmaceutical products, including oncology and immunology drugs, rare disease treatments, and vaccines. Notable products include Eliquis, Nurtec ODT/Vydura, Prevnar, Comirnaty, and Paxlovid.

Pfizer was actively involved in COVID-19 prevention and treatment, collaborating with various partners globally and having a strategic partnership in China for the local launch of the COVID-19 oral therapeutic treatment Nirmatrelvir/Ritonavir. This boosted PFE's financials when COVID-19 was a pressing problem in our society. I remember writing about PFE in November 2021 and claiming that the stock looked like a medium-term 'Strong Buy" at the time:

{kind=link}

But the pandemic became a thing of the past as quickly as it had emerged, taking the company's profit margins with it.

{kind=link}

The share price started to follow margins and management's weak guidance, which I will write about in more detail below. As a result, PFE is trading near its 10-year lows today:

But is everything so bad when it comes to investing in the company for the long term? Let's figure it out together.

Pfizer's Financials And Prospects

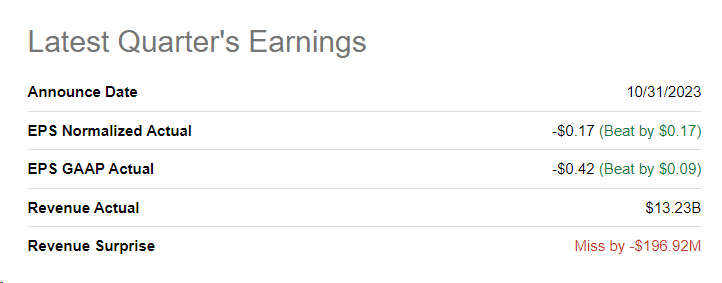

In Q3 FY2023 , Pfizer reported revenues of $13.2 billion, representing a 41% operational decrease primarily driven by the expected decline in revenues from Paxlovid and Comirnaty. However, revenues for Pfizer's non-COVID products demonstrated a 10% operational growth during the same period.

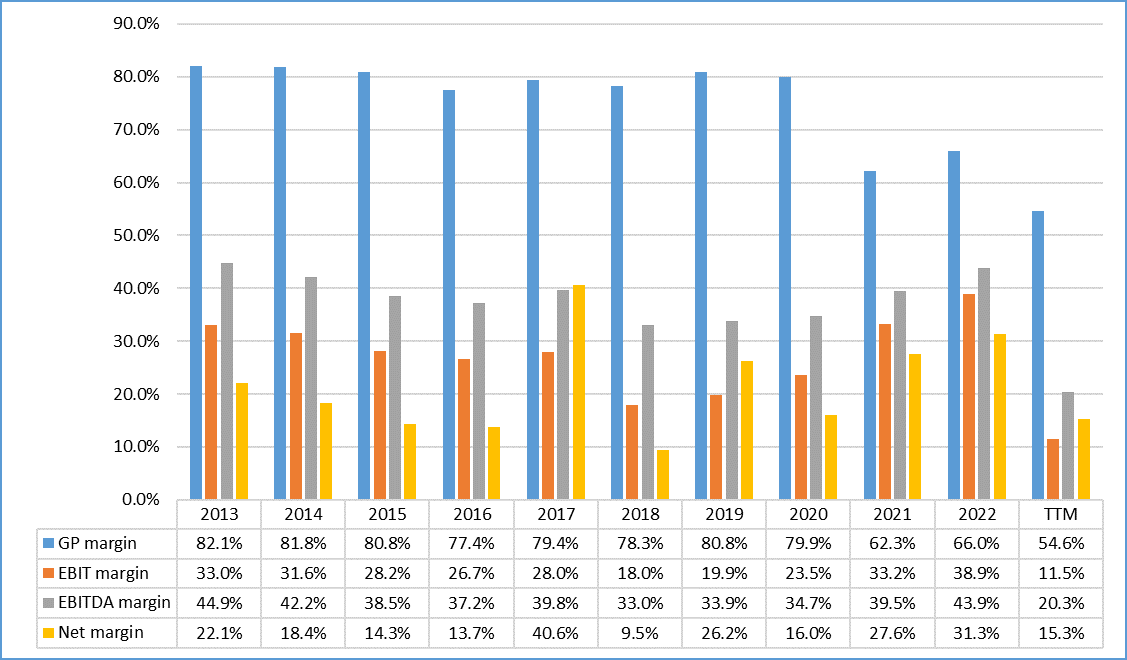

By measures of profitability, the 3Q adjusted gross margin was 32.7%, down from 63.3% a year earlier, again reflecting the Comirnaty and Paxlovid inventory write-offs and other charges.

The reported diluted loss per share for Q3 2023 was $0.42, significantly impacted by $5.6 billion in non-cash inventory write-offs and other charges, resulting in an adjusted diluted LPS of $0.17.

{kind=link}

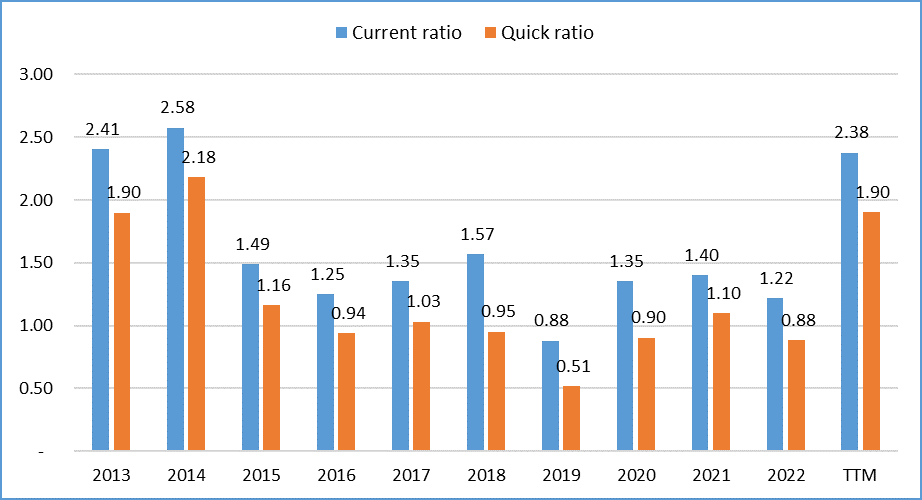

The company has increased its liquidity ratios this year, apparently to make M&A activities less risky.

{kind=link}

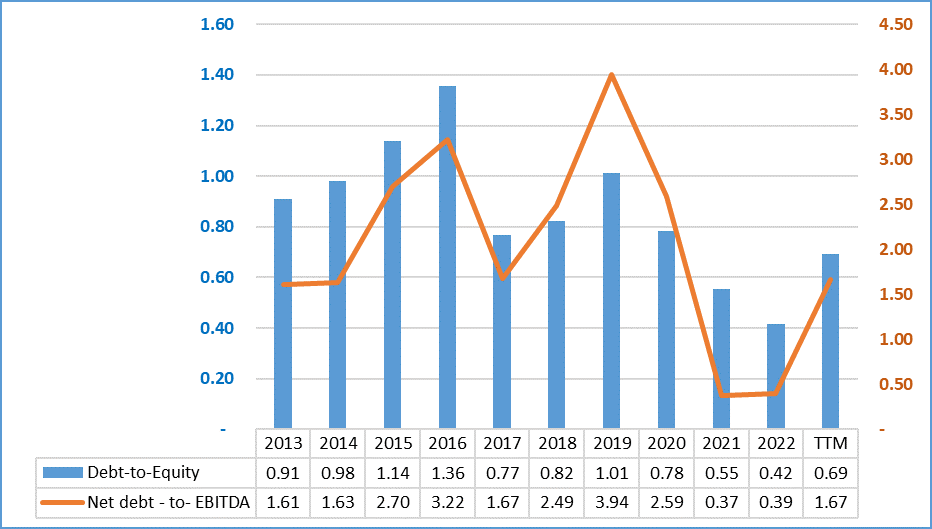

The debt burden has increased slightly on a TTM basis, but overall PFE's leverage is still at a relatively acceptable level in my opinion.

{kind=link}

At the time of the Q3 press release, Pfizer reaffirmed its FY2023 guidance, initially provided on October 13, 2023, which included revenues at $58-61 billion and an adjusted diluted EPS of $1.45-1.65. The company also maintained its expectation for non-COVID operational revenue growth of 6% to 8% compared to FY2022. The positive factors contributing to Pfizer's performance included the successful launch of new products and indications, such as Abrysvo for older adults and Prevnar 20 for pediatric use. Additionally, Pfizer launched an enterprise-wide cost realignment program aimed at achieving annual net cost savings of at least $3.5 billion, with $1.0 billion expected to be realized in FY2023 and an additional $2.5 billion in FY2024.

After the announcement of the Q3 results, Pfizer began a real losing streak that brought the share to where it is trading today.

On December 1 , PFE announced that its twice-daily oral weight loss candidate, danuglipron, will not proceed to late-stage development due to safety concerns flagged in a Phase 2 readout. This setback follows a similar outcome for Pfizer's first obesity candidate, lotiglipron, in June, where patients in early-stage trials experienced an increase in certain liver enzymes. Pfizer's development of GLP-1 drugs for diabetes and weight loss was of particular interest, with danuglipron holding a strategic advantage as an orally administered therapy.

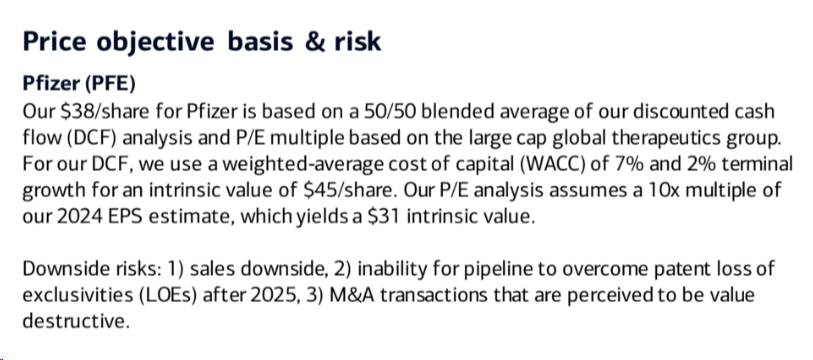

Some major investment banks started to evaluate this news and in almost all reports I could find, I saw PFE shares rated as 'Neutral', despite price targets of $34-38.

BofA's analysts wrote that they believe tolerability issues will continue to be a challenge for danuglipron, potentially delaying Pfizer's entry into the obesity treatment paradigm. Despite this setback, BofA remains bullish on the overall obesity treatment space, expecting a broader uptake of anti-obesity medications with improvements in reimbursement and competitive pricing pressure.

On December 13 , the company announced a forecast for the 2024 financial year that reflected the management's expectations following the acquisition of Seagen. They called for $ 58.5-61.5 billion in sales, roughly in line with expectations for FY2023. However, Wall Street was very disappointed by this forecast, as it had originally expected much higher growth rates.

Based on today's price action, we can assume that Mr. Market is now pricing in some risk that PFE will repeat the story of Organon ( OGN ), which has been suffering from its debt load for many quarters and remains dirt cheap.

But I don't think it's as bad as the Street fears.

It's because Pfizer is strategically positioning itself to return as a diversified healthcare leader, aiming to move beyond the challenges posed by the COVID-19 era. With a broad portfolio encompassing various therapeutic areas, the company seeks to reclaim its status as a comprehensive medical solutions provider. The recent acquisition of Seagen is poised to enhance Pfizer's oncology expertise, particularly in the realm of antibody-drug conjugates (ADCs), a pivotal component of targeted cancer therapies. This strategic move should strengthen Pfizer's position in oncology and help capitalize on Seagen's leadership in the ADC sector.

While Pfizer focuses on expanding its oncology capabilities, the company continues to benefit from robust contributors to top-line growth in internal medicine. Established products like Eliquis and Vyndaqel, alongside newer offerings such as Abrysvo and Prevnar 20, contribute significantly to Pfizer's overall performance. The acquisition of Seagen also brings a promising pipeline of potential FDA-approved drugs, adding the further potential for success and profitability. These initiatives align with Pfizer's focus on replacing sales from products losing exclusivity in 2025-2030.

Pfizer's recent restructuring program, unveiled in October, aims to achieve annual cost savings of at least $3.5 billion, with $1.0 billion anticipated in 2023 and $2.5 billion in 2024.

In terms of financial performance, Pfizer anticipates robust top-line growth in its core businesses (excluding COVID-19 therapies) over the coming years (though FY2024 is about to be flat as we now know). The company, backed by a substantial operating cash flow of $62 billion in 2021-2022, continues to leverage its financial strength to pursue acquisitions and advance drug development. The emphasis on its pipeline, featuring nearly 20 new products or indications over the next 18 months, reflects Pfizer's commitment to sustaining growth.

Therefore, over a longer investment horizon, I think PFE is still a strong company with a bunch of prospects that should positively impact the company's financials in one way or another.

But what about PFE's valuation?

Pfizer's Valuation Analysis

While I have a few reports in front of me, I cannot ignore the analysts' calculations of the fair value of PFE stocks. This is how the valuation picture for PFE looks like to the analysts at BofA:

{kind=link}

Argus Research analysts see the fair value of PFE $1 higher (as of November 24, 2023):

PFE trades at 9.3 times our 2024 EPS estimate, below the mean of 17.6 for our coverage universe of large-cap biopharma stocks. We believe that Pfizer is well positioned for post-pandemic recovery, and expect stronger top-line growth from the base businesses, excluding COVID-19 vaccines and treatments. The stock also carries an attractive dividend yield of about 5.4%. We are reaffirming our BUY rating on PFE with a revised price target of $39.

Source: Argus Research [proprietary source]

I usually look at the FCF yield, which is where you can best see the margin of safety that value investors are so desperately looking for. In the case of Pfizer, I don't see a clear margin of safety, as the company’s heavy spending on acquisitions and CAPEX has severely clouded the picture in recent quarters. The FCF yield has fallen from 8-11% to 5% today within a year:

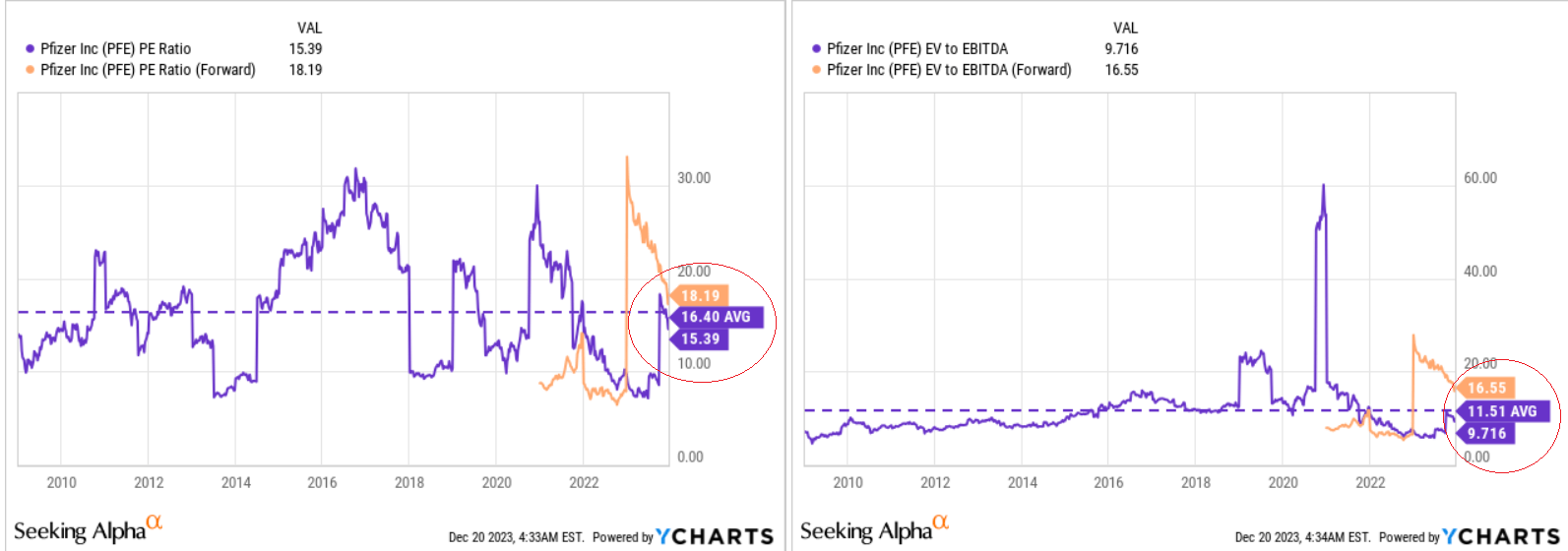

Although PFE's multiples are on average 15-20% below those of the industry medians, the stock doesn't look cheap by historical standards if we rewind to 2009:

{kind=link}

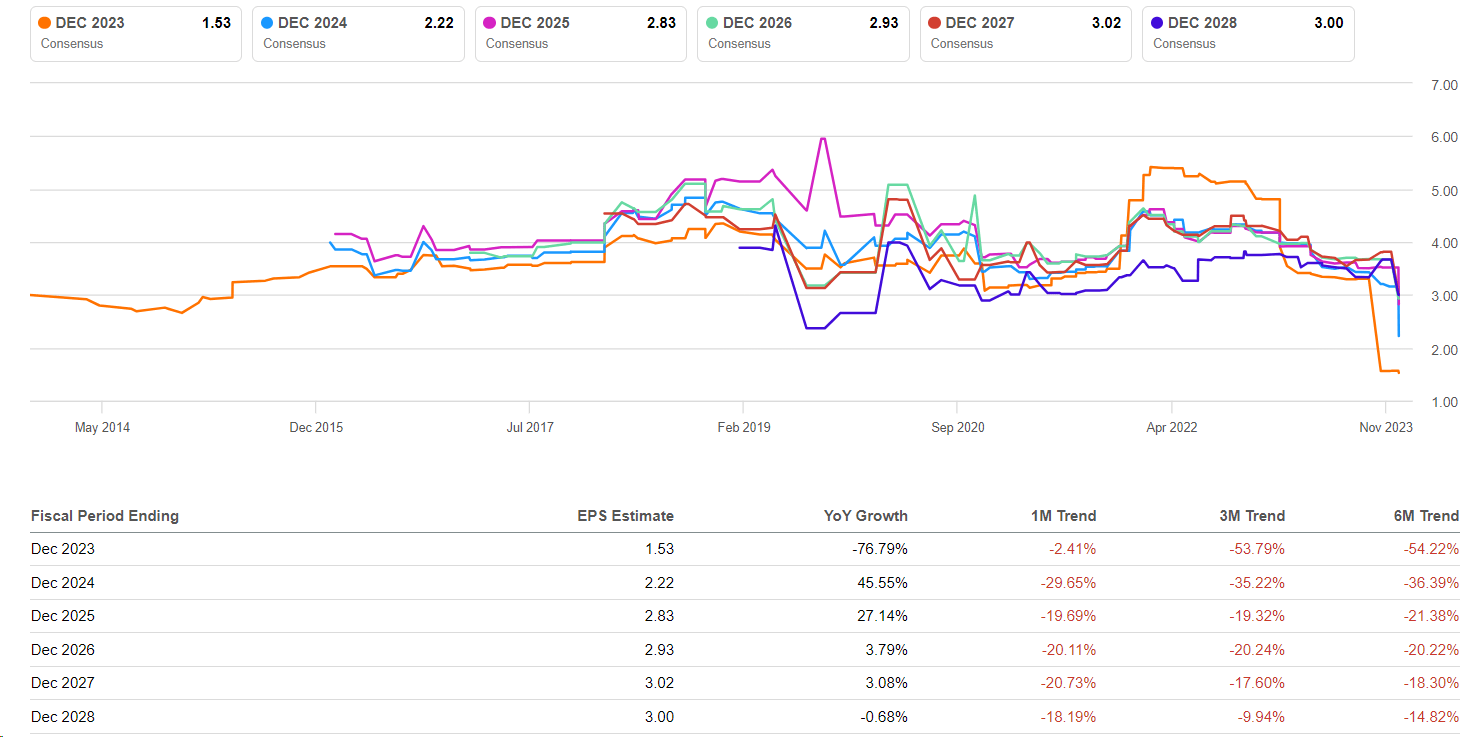

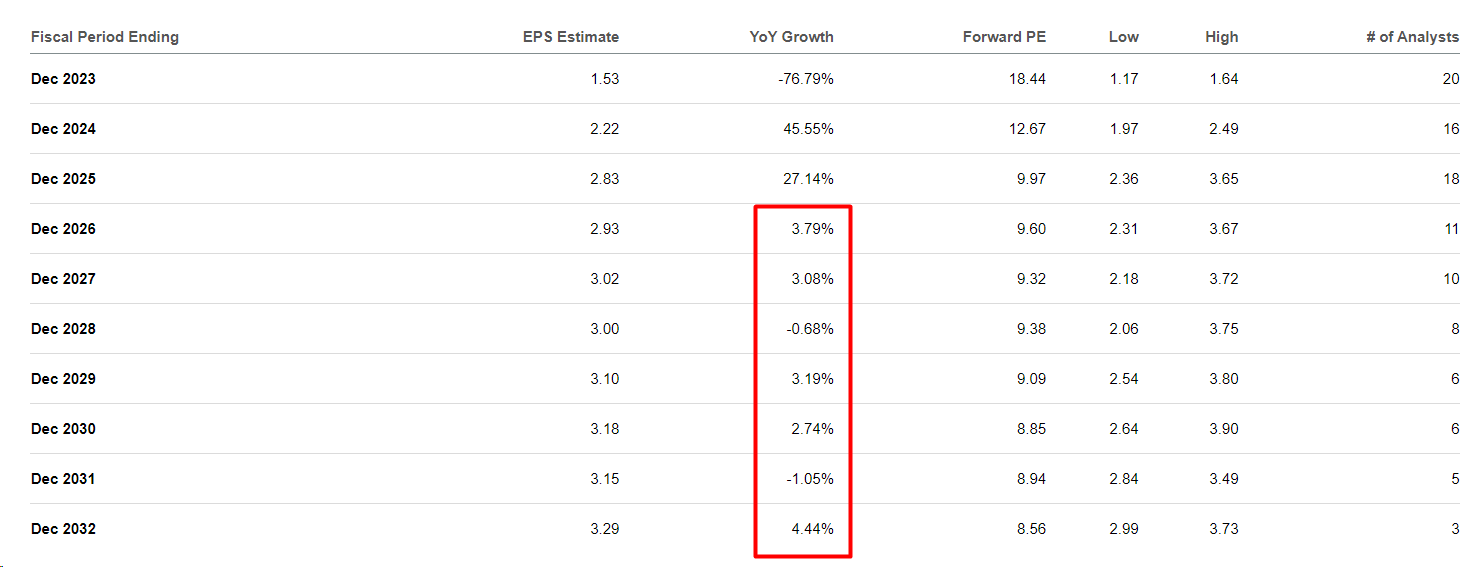

However, when we look at the P/E ratio and EV/EBITDA, we need to understand one very important thing: Wall Street's estimates for PFE's earnings have been slashed dramatically recently, and not just for FY2024 and FY2025:

{kind=link}

However, assuming that PFE's conservative forecasts only concern the 2024 financial year and that cost optimizations and synergy savings as well as an increase in sales by Seagen await us, I do not consider the current roughly flat growth rates for PFE's EPS in the years 2026-2030 to be realistic.

{kind=link}

Once the integration of Seagen is complete, PFE's EPS estimates are likely to rise again - to me that seems only a matter of time. But the market prices in such things quickly, so investors could miss the opportunity by standing aside.

The Bottom Line

Of course, my today's thesis comes with plenty of risks to consider; otherwise PFE stock would not have fallen by 45% YTD. Pfizer's reliance on key products, vulnerability to currency fluctuations, and sensitivity to healthcare policy changes and global health events add complexity to this 'potential recovery story'. Also, the recent news about the phase 2 results for Danuglipron should not be ignored by investors - it is indeed a big blow to future growth.

However, Danuglipron is only 1 of the company's products, which will most likely come to market in one form or another, albeit later than previously planned. But Mr. The Market seems to have forgotten to think about that possibility, focusing just on the panic. I suggest not buying this panic, but thinking about buying PFE instead.

Thanks for reading!

For further details see:

Pfizer: Buy The Panic