CA - Pine Cliff Energy: A Call Option On Natural Gas With A 9.3% Yield

2023-06-15 10:30:00 ET

Summary

- Pine Cliff Energy pays a generous dividend, which was fully backed in Q1.

- It may not be fully covered in Q2 as the natural gas price is now trading below C$2.50 on a spot basis.

- This means Pine Cliff is now more a trading vehicle than a long-term buy and hold (unless you have a very advantageous dividend tax regime).

Introduction

As my recent articles on Pine Cliff Energy ( PNE:CA ) ( OTCPK:PIFYF ) have shown, I have had a pretty bullish stance on Pine Cliff Energy as the company was printing cash in 2021 and the majority of 2022 thanks to its low-decline asset base. This allowed the company to take advantage of the strong prices and the balance sheet was cleaned up while the Canadian natural gas producer also started to pay a very generous dividend. But I recently sold my entire position, and in this article I will explain why.

The Q1 results were okay

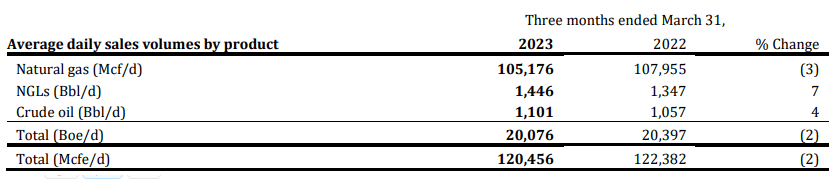

The total output of Pine Cliff was approximately 20,100 barrels of oil-equivalent per day in the first quarter and the vast majority (approximately 87%) of the oil-equivalent output consists of natural gas.

{kind=link}

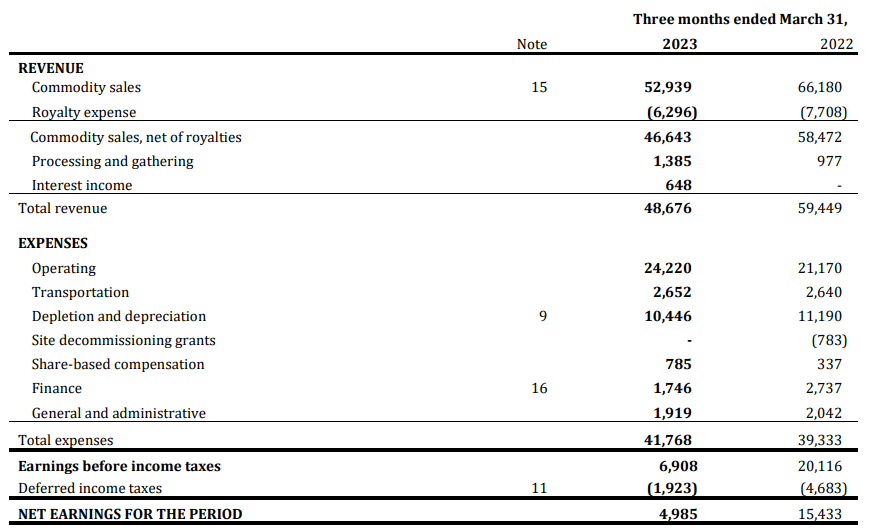

As the average realized price was approximately C$3.74 per Mcf for the natural gas sales in the first quarter, about 67% of the consolidated revenue was generated from selling the natural gas. The average realized oil price was just under C$92.5 per barrel. And combined, this resulted in a total revenue of just under C$53M. after deducting the C$6.3M in royalty expenses and adding the interest income and processing and gathering income, the net revenue was C$48.7M.

{kind=link}

The operating expenses remain relatively low although there clearly is an increase in the net operating expenses compared to the first quarter of that year, despite posting a lower production rate (the YoY output in the first quarter decreased by approximately 1.5%).

Pine Cliff was still profitable though, and the bottom line shows a net income of C$5M. This is approximately C$0.014 per share based on the current share count of just over 351 million shares.

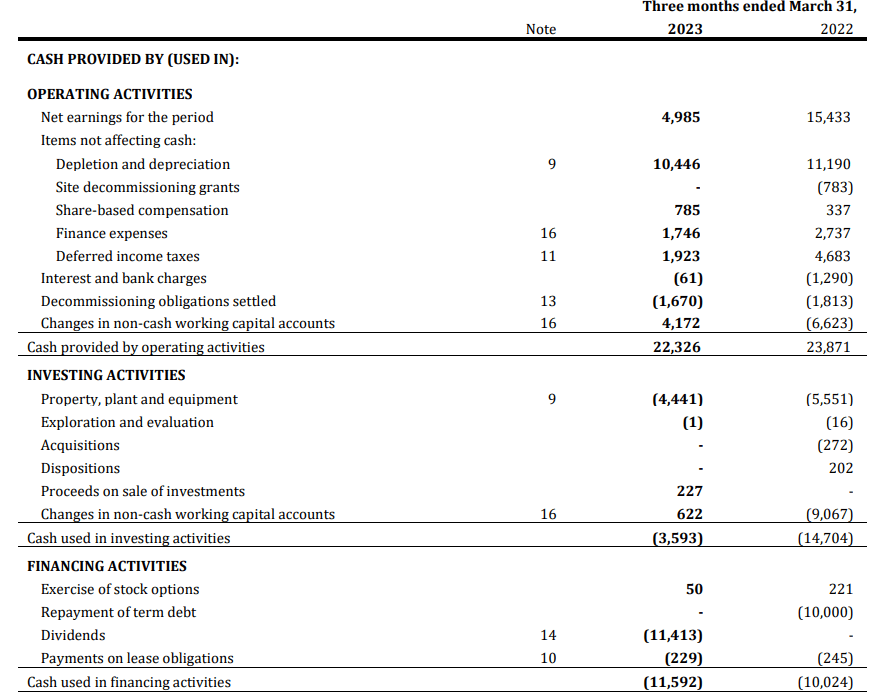

Not a great performance but let's not forget the Pine Cliff assets are pretty mature and there aren't a whole lot of capital expenditures needed. While the company reported a total depreciation, amortization and depletion expense of C$10.5M in Q1, the total capex was just C$4.4M. As you can see below, the total operating cash flow was C$22.3M and after deducting the C$4.2M contribution from working capital changes and deducting the C$0.2M in lease payments, the adjusted operating cash flow was C$17.9M.

{kind=link}

But as the total capex was just C$4.4M, the net free cash flow was C$13.5M during the first quarter. That's almost three times higher than the reported net income thanks to the big difference between depreciation expenses and actual capital expenditures. Additionally, all of the taxes that were calculated based on the pre-tax income were deferred and no cash taxes were owed in Q1. The free cash flow result of C$13.5M represents a free cash flow per share of C$0.038 which means the current monthly dividend of C$0.0108 is fully covered by the free cash flow result.

I'm still bothered by the low PV10 value

I bought the stock in the mid C$1.20 range at the beginning of the first quarter, and I sold out in the mid C$1.40 range a few weeks ago. Usually I am not too interested in a 15% share price swing but in Pine Cliff's case, I was willing to take some money off the table as I already have a long position in several other natural gas companies. Additionally, during the current low natural gas price era, I wanted to stick with producers that have a long reserve life index (preferably a few decades). Because although I am sure the natural gas price will - eventually- increase again, producers with a relatively small reserve are just losing valuable time.

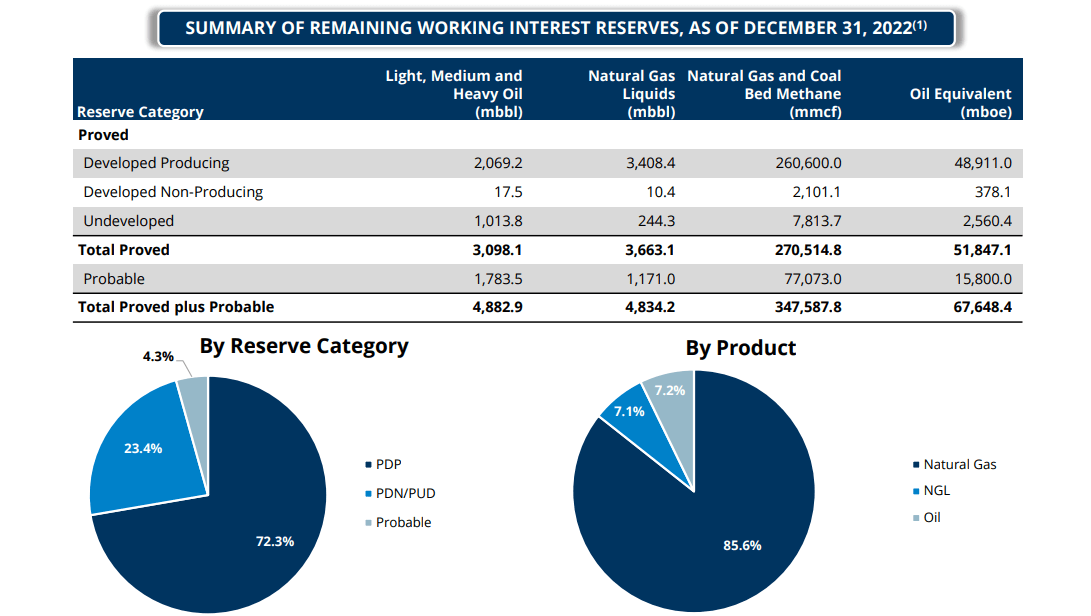

And the relatively constrained reserve estimate is one of my main reasons to sell. As of the end of 2022, the total 2P reserves contained about 67.7 million barrels of oil-equivalent. At a current production rate of about 7.3M barrels of oil-equivalent per year, the reserve life based on the 2P reserves is just over 9 years. The PDP reserves of 48.9 million barrels of oil-equivalent underpin a reserve life of about 6.5 years.

{kind=link}

And that's fine. The company is very upfront about this and for short term speculation purposes, this low-decline natural gas producer could be a good choice.

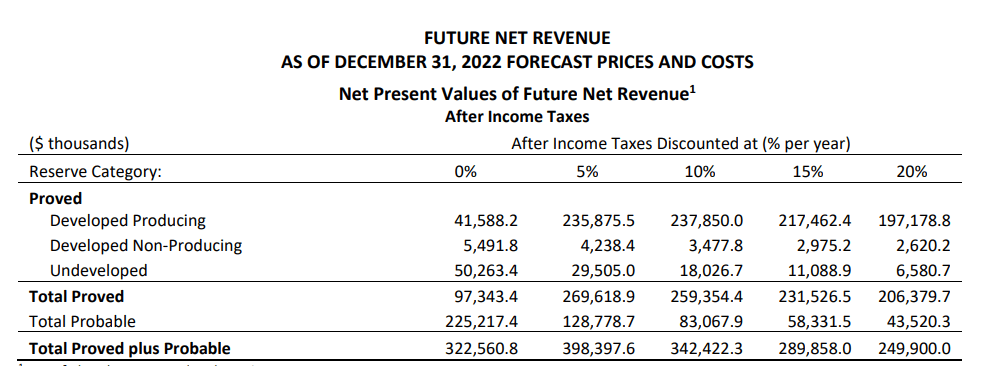

But I also wanted to make sure I wasn't overpaying for Pine Cliff, so the reserve update which provides an overview as of the end of each calendar year usually is a good read. As you can see below, the independent consultants calculated an after-tax PV10 value of C$342M. This includes the abandonment and reclamation costs.

{kind=link}

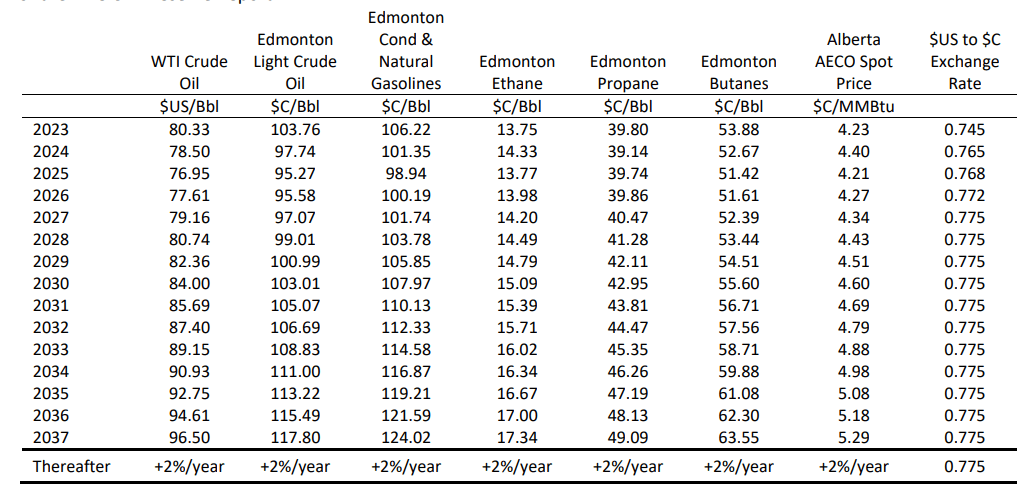

If we add the net cash position of C$61M, the total NAV of the company would be around C$403M. Divided over 351.2M shares outstanding, that's approximately C$1.15 per share. Sounds good as a potential bottom for the share price, but there is one caveat. As you can see below, the average natural gas price (AECO SPOT) used for the PV10 calculations uses pretty aggressive natural gas prices.

{kind=link}

While I don't dispute the natural gas price could increase again, let's keep in mind that every year the natural gas price trades below those base case scenarios, the PV10 value decreases as an Mcf of gas that gets sold at C$2.50 instead of C$4 is 'lost forever'. It's too bad these PV10 calculations don't provide a sensitivity analysis based on different natural gas prices as I would have loved to see how the PV10 holds up using C$3.5 or even C$3 natural gas (the current spot price is even below C$2.25 per GJ, so achieving an average of C$4.23 for this year is already pretty impossible).

And that means the PV10 value will likely be lower than the C$1.15 based on the base case scenario. If I would use the PV15 value for the PDP reserves and a 20% discount rate for the remainder of the reserves, I end up with a NAV of C$0.95 per share.

Investment thesis

I'm more than happy to sometimes speculate on the natural gas price, and I think that's how I should approach Pine Cliff Energy from here on. When the share price gets closer to the official NAV (perhaps adjusted for the high natural gas price used in the base case scenario) it could make sense to buy and rake in the C$0.0108 monthly dividend while waiting for the natural gas prices to recover, only to sell Pine Cliff on the pop.

Pine Cliff isn't the only natural gas position I trimmed, but for now, it is the only one I am keeping an eye on to define a re-entry point. If you are bullish on the natural gas price, Pine Cliff might be the perfect stock for you thanks to its low decline rate (less than 10%) and very robust balance sheet. I will likely use Pine Cliff as a trading vehicle going forward. If the share price slides back down to C$1.25, I'd likely buy the stock again. And, as I own several other natural gas producers, I have hedged my bets in case I'm wrong and the natural gas price suddenly rips higher.

For further details see:

Pine Cliff Energy: A Call Option On Natural Gas With A 9.3% Yield