CA - Pine Cliff Energy: Buy This Natural Gas Stock For Its Sustainable 9% Dividend Yield

2023-12-22 17:59:04 ET

Summary

- Pine Cliff Energy, a small-cap Canadian natural gas producer, pays high-yield dividends supported by its low decline rate and robust balance sheet.

- Will the investment thesis remain valid, particularly in light of its acquisition of Certus Oil & Gas and the recent weakness in natural gas prices?

- In this article, I analyze Pine Cliff's operations and assess the safety of its dividends.

Pine Cliff Energy Ltd . ( OTCPK:PIFYF ) is a small-cap natural gas producer in Canada. With a 7% corporate natural decline rate and low demand for capital expenditures, Pine Cliff has consistently rewarded its shareholders through regular dividend payments, currently yielding 9.5%.

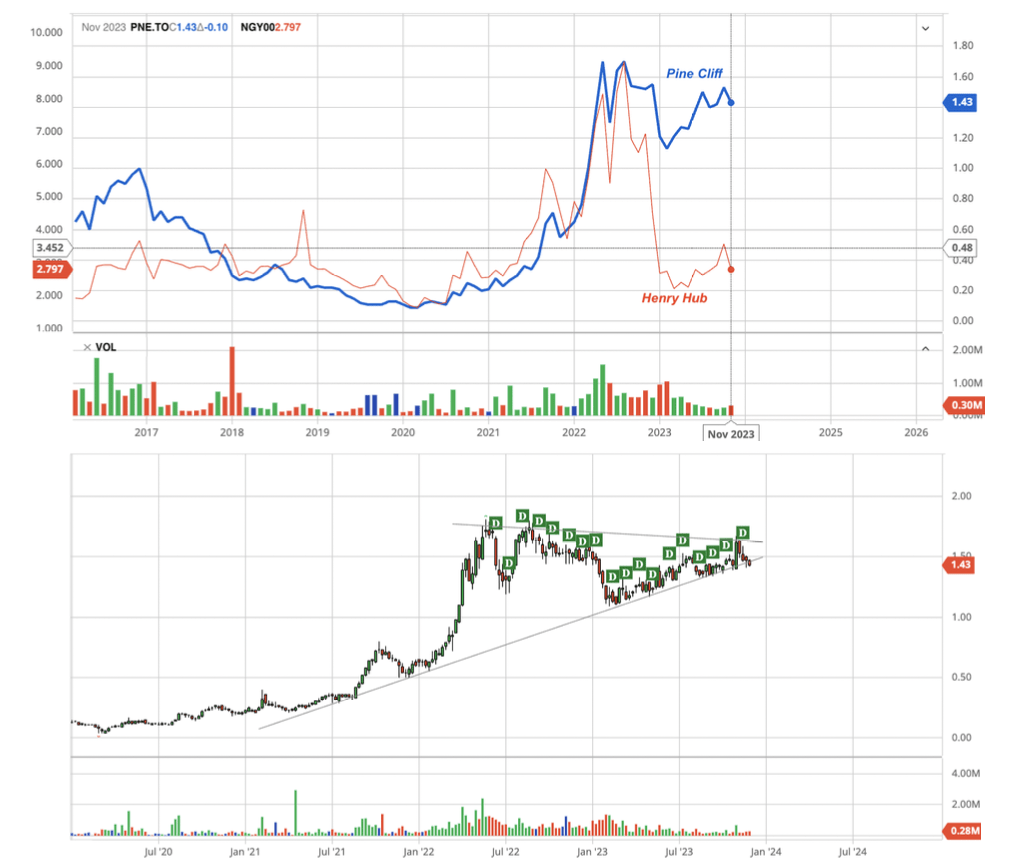

Since I first presented the stock as a high-yield income idea in February 2023, Pine Cliff has appreciated by 3.6% and paid ten monthly dividends, resulting in a total return of 14.6%, as illustrated in Figure 1. As a comparison, the S&P 500 index returned approximately 14.5% during the same period.

{kind=link}

Fig. 1. Stock chart of Pine Cliff Energy, dividend back-adjusted, as compared with Henry Hub benchmark natural gas price. Dividend payments are shown as "D" (modified from Barchart and Seeking Alpha)

Since February 2023, Pine Cliff Energy has released its 2022 annual report and three quarterly results. Additionally, the company acquired Certus Oil & Gas Inc., resuming merger and acquisition activity after a two-year hiatus. The stock has also followed natural gas prices downward lately. It is thus a good time to reexamine the business and review the investment thesis.

A review of the business

Pine Cliff Energy is a small-cap natural gas producer with operations in three main areas in the western Canadian provinces of Alberta and Saskatchewan, as shown in Figure 2.

{kind=link}

Fig. 2. Main operating areas of Pine Cliff Energy, before and after the acquisition of Certus Oil & Gas Inc. (modified after Pine Cliff Energy)

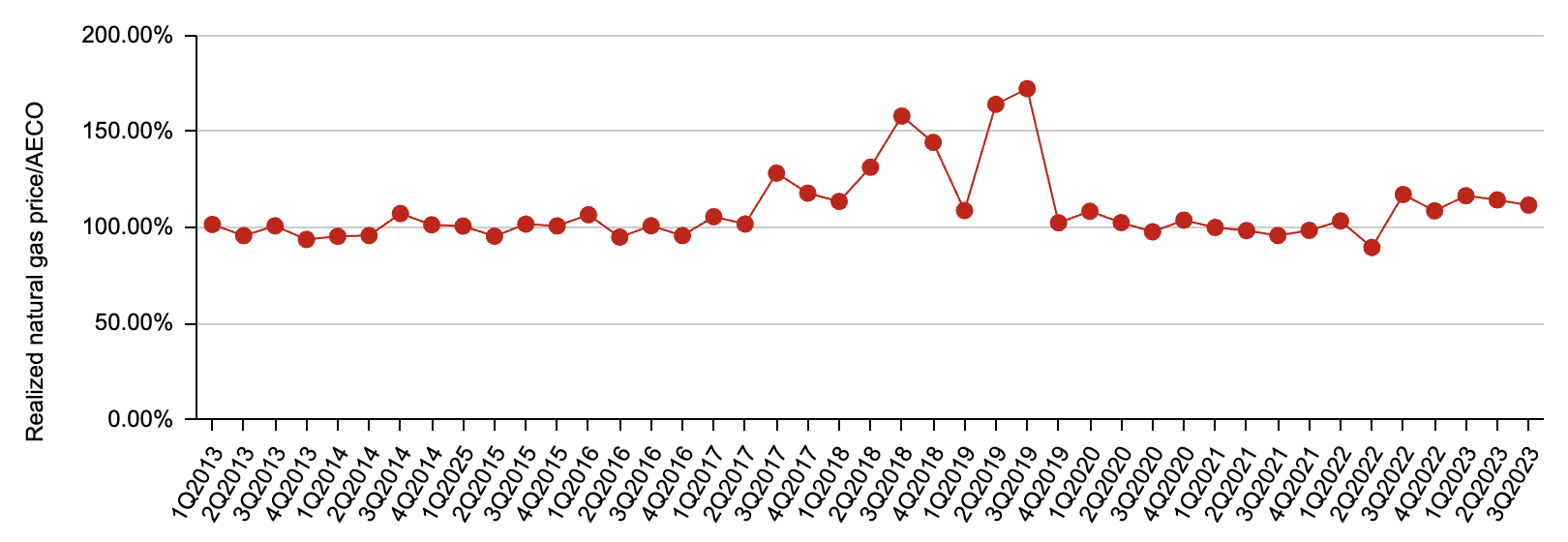

Over the period from 2013 to the third quarter of 2023, natural gas has consistently constituted the vast majority of Pine Cliff's total production, ranging from 86.1% to 96.5%. Pine Cliff sells its natural gas to five markets in Canada and the U.S. It owns three Canadian Energy Regulators - regulated export pipelines to Montana and Saskatchewan, providing natural gas market pricing diversity. While Pine Cliff has usually sold natural gas at prices comparable to the Canadian benchmark AECO, it has indeed realized a premium in, for example, 2017-2019 and recent quarters, as shown in Figure 3. Since the third quarter of 2022, Pine Cliff has achieved an average premium of 13.7% over AECO.

{kind=link}

Fig. 3. A comparison of Pine Cliff realized natural gas price with Canadian benchmark AECO before hedging in percentage (compiled by Laurentian Research for The Natural Resources Hub, based on data sourced from the financial filings of Pine Cliff Energy)

The lowest decline rate in Canada

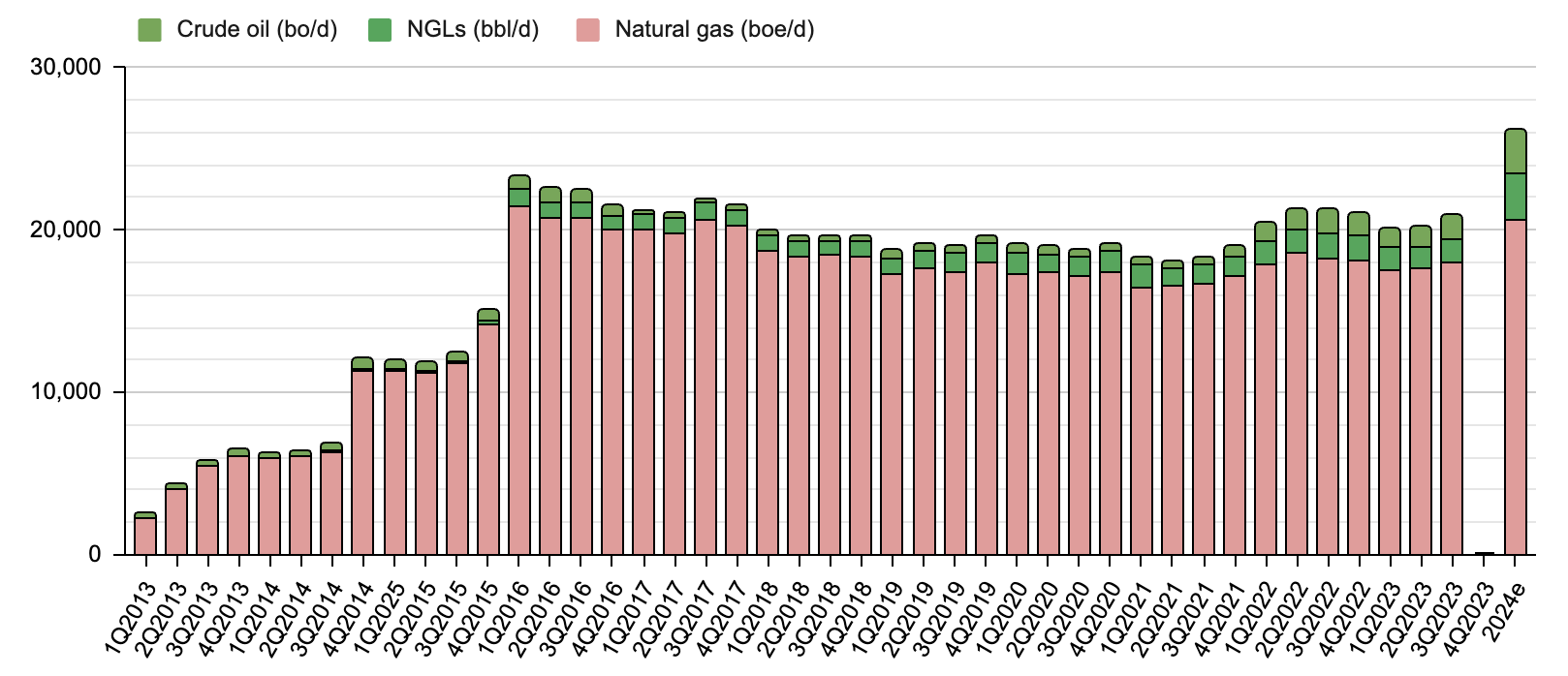

Since George Fink and Phil Hodge assumed control of the company in December 2011, Pine Cliff made as many as 20 acquisitions, particularly in the first five years, resulting in rapid production growth from approximately 100 boe/d in 2012 to 23,297 boe/d in the first quarter of 2016, as shown in Figure 4.

{kind=link}

Fig. 4. Production profile of Pine Cliff Energy, 2013 to date, shown with estimated pro forma production for 2024 following the Certus transaction (compiled by Laurentian Research for The Natural Resources Hub, based on data sourced from Pine Cliff financial filings)

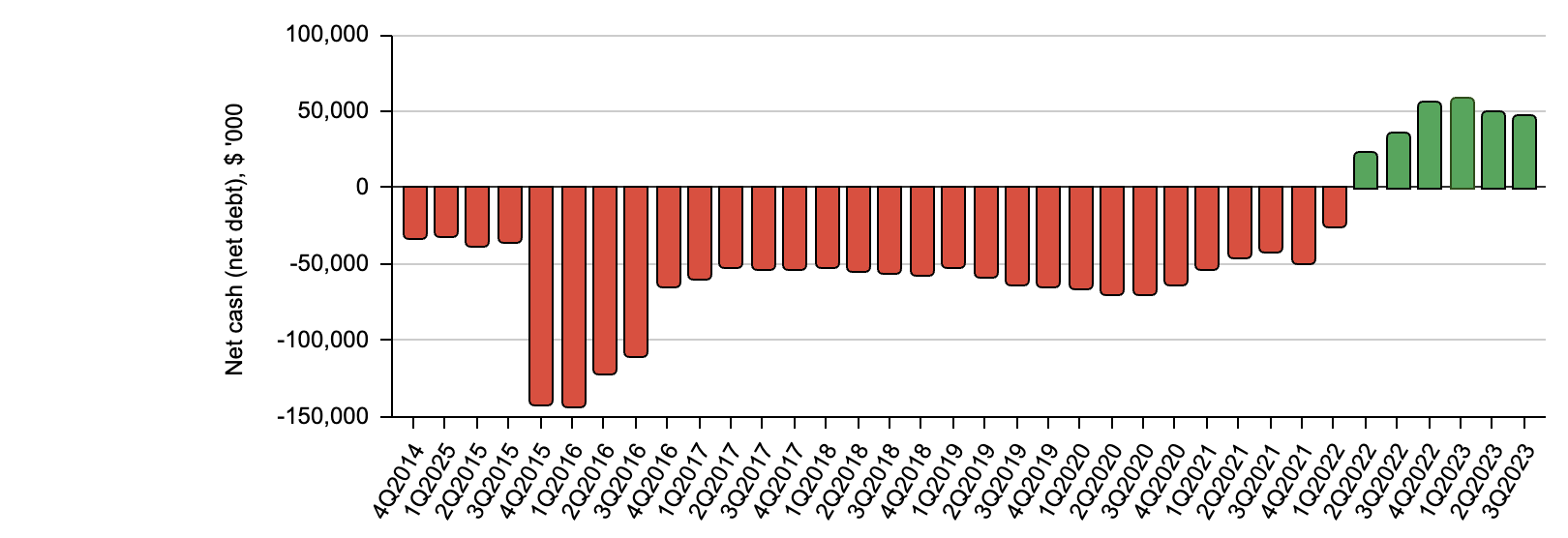

From 2016 to early 2021, Pine Cliff Energy focused on reducing debt accumulated during the 2012-2015 acquisition spree (Figure 5). During this period, the company kept capital expenditures to a minimum, as illustrated in Figure 6. Despite limited capital spending, Pine Cliff managed to maintain production above 18,000 boe/d, thanks to its 7% decline rate—the lowest among all Canadian public producers, which have an industry average production decline rate of 25%. The surge in natural gas prices in late 2021 and 2022, demonstrated in Figure 7, propelled Pine Cliff to a positive net cash position. Consequently, the company began increasing capital spending to counter natural decline, address a two-year acquisition drought, and drive production growth.

{kind=link}

Fig. 5. Net debt of Pine Cliff Energy by quarter (compiled by Laurentian Research for The Natural Resources Hub, based on data sourced from Pine Cliff financial filings)

{kind=link}

Fig. 6. Quarterly capital expenditures of Pine Cliff Energy (compiled by Laurentian Research for The Natural Resources Hub, based on data sourced from Pine Cliff financial filings)

{kind=link}

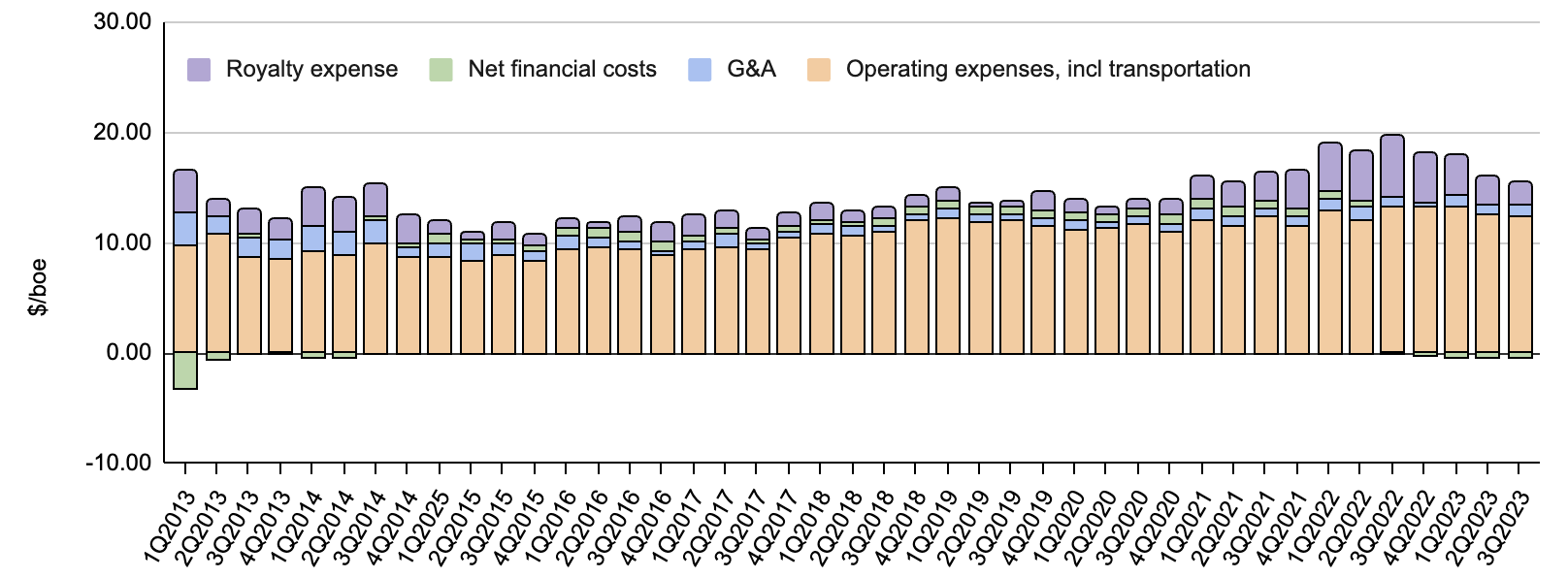

Fig. 7. Quarterly average total price realized by Pine Cliff Energy, as compared with the unit cash cost (compiled by Laurentian Research for The Natural Resources Hub, based on data sourced from Pine Cliff financial filings)

The cash cost of Pine Cliff Energy was C$15.29/boe in the third quarter of 2023, down from the recent high of C$19.66/boe reached in the same quarter one year ago, as illustrated in Figure 8. Over the last ten years, Pine Cliff lost money on a full-cycle basis only in five quarters, never in any full year, as evidenced in Figure 7.

{kind=link}

Fig. 8. Cash costs per boe for Pine Cliff Energy (compiled by Laurentian Research for The Natural Resources Hub, based on data sourced from Pine Cliff financial filings)

Financial performance

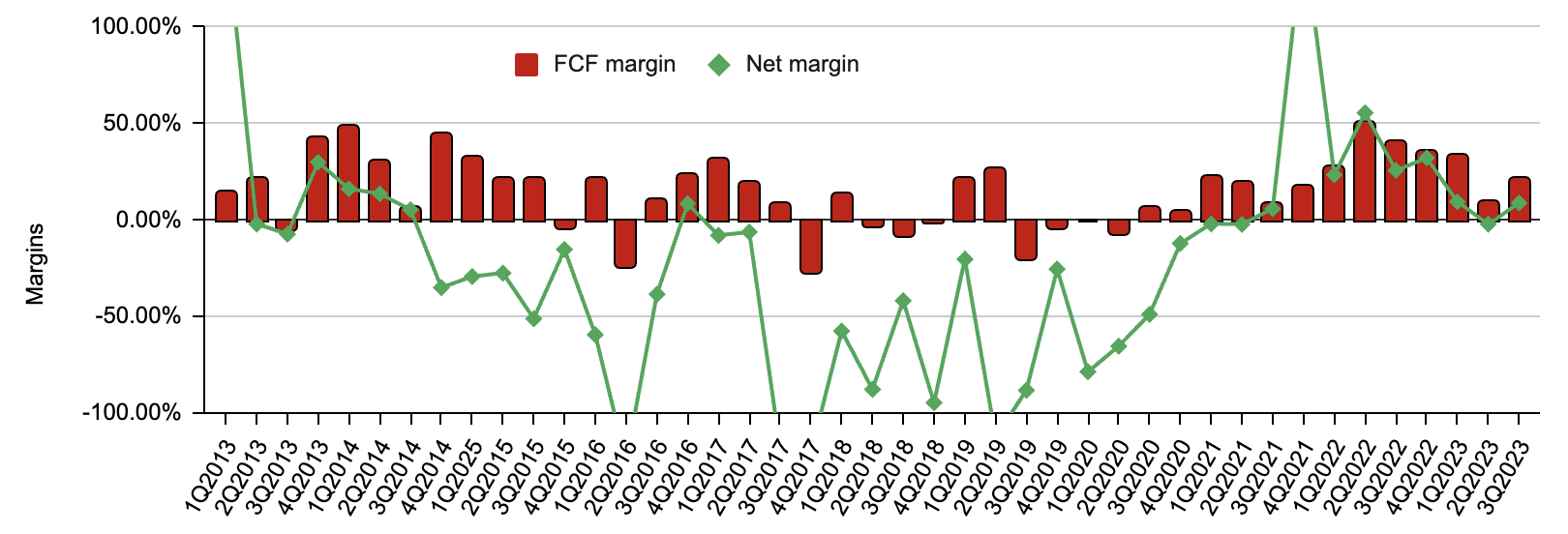

Thanks to the low cash cost and low decline characteristic of the asset portfolio and prudent capital spending by the management, Pine Cliff Energy managed to generate positive free cash flow in each of the last ten years, even between 2015 and 2020 when commodity prices were low, as evident in Figure 9. However, as I pointed out previously, the net margin of Pine Cliff fluctuated significantly more than its free cash flow margin. This is where general investors new to oil and gas companies tend to get confused.

{kind=link}

Fig. 9. Net margin and free cash flow margin of Pine Cliff Energy (compiled by Laurentian Research for The Natural Resources Hub, based on data sourced from Pine Cliff financial filings)

From the first quarter of 2016 to 2020, quarterly revenue fluctuated around C$27 +/- 5 million due to production being in a holding pattern (Figure 4), and the total realized price ranged between C$10/boe and C$20/boe (Figure 7). From the first quarter of 2021 to the second quarter of 2022, quarterly revenue rose to a record high of C$90 million, driven by strong natural gas prices and a slight increase in production. Since then, a softening total realized price has resulted in a gradual decrease in quarterly revenue to C$48 million by the third quarter of 2023. However, as evidenced in Figure 10, Pine Cliff still pulled in more revenue in that quarter than in any other quarter prior to the third quarter of 2021. This is because the cash margin is still healthy, as illustrated in Figure 7.

{kind=link}

Fig. 10. Revenue before royalties, adjusted funds flow, net earnings and FCF of Pine Cliff Energy (compiled by Laurentian Research for The Natural Resources Hub, based on data sourced from Pine Cliff financial filings)

Dividend safety

Supported by robust cash flow, Pine Cliff initiated a monthly dividend in June 2022 and has since increased it twice. The current monthly dividend stands at C$0.01083 per share , resulting in an impressive dividend yield of 9.51%.

Previously, Pine Cliff indicated that, as long as the benchmark AECO remains above C$2.62/Mcf, the funds flow will be sufficient to cover cash expenses, capital expenditures, corporate taxes, and dividends. In the second and third quarters of 2023, AECO averaged C$2.44/Mcf and C$2.58/Mcf, both below the C$2.62/Mcf threshold. The net cash position indeed dropped from C$58 million in the first quarter of 2023 to C$49 million in the second quarter and C$47 million in the third quarter, as shown in Figure 5. This raises the question of whether the current monthly dividend is sustainable.

As we assess Pine Cliff's dividend safety, let us not forget that AECO has dropped to the support band that has been operative for three decades, as shown in Figure 11, suggesting limited downside risk. Even if AECO remains sub-C$2.62/Mcf for an extended period, Pine Cliff carries no debt on its books and has C$47 million of net cash to support the continued payment of dividends at the current level for several quarters. Additionally, Pine Cliff can opt to minimize capital spending for cash conservation, thanks to its exceptionally low rate of production decline.

{kind=link}

Fig. 11. The Henry Hub and AECO benchmark natural gas prices, measured in US$/MMbtu and C$/gigajoule, respectively (modified from Barchart and Alberta Economic Dashboard)

Additionally, the acquisition of Certus Oil & Gas, a transaction expected to be closed before the end of 2023, is anticipated to increase Pine Cliff's production by approximately 5,300 boe/d (Figure 4). The Certus production has a 49% liquids cut, which is expected to strengthen Pine Cliff's operating netback through increased exposure to crude oil and natural gas liquids production. Dividend safety will benefit from Pine Cliff's 25.4% greater production at a higher operating netback.

Valuation and risks

The recent decline in AFFO may give the appearance of the Pine Cliff stock trading near its historical average EV/AFFO; however, as shown in Figure 12, the stock trades significantly below the historical multiples, pro forma the Certus acquisition.

{kind=link}

Fig. 12. Enterprise value to adjusted funds flow multiple, from 2013 to date, with the EV/AFFO for 2024 estimated pro forma the Certus acquisition (modified after Pine Cliff Energy)

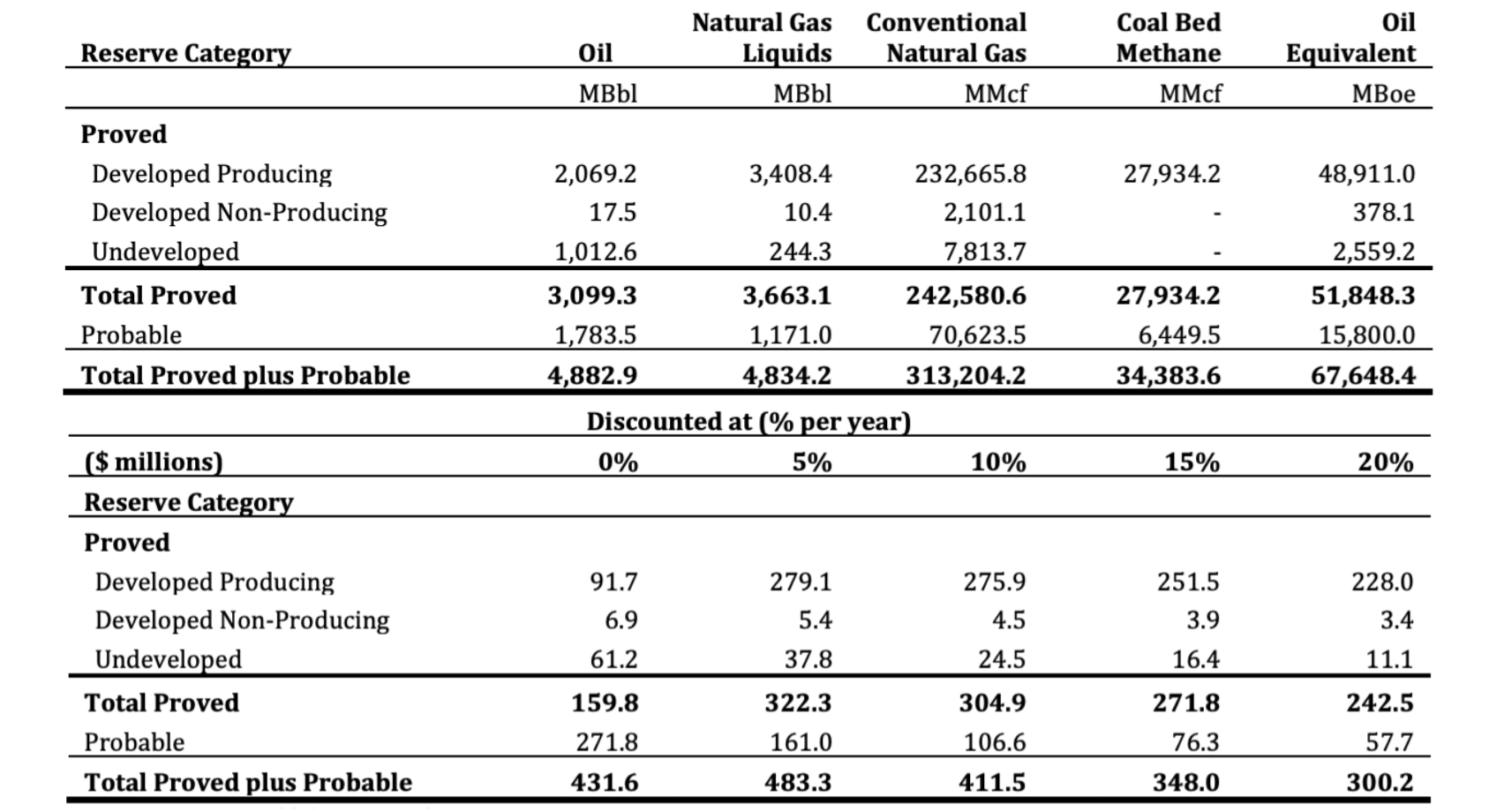

Pine Cliff is currently trading at US$6.8 per barrel of oil equivalent of proved developed producing reserves, using the end-2022 reserve data as shown in Table 1, with Certus' 12.3 MMboe PDP reserves considered. In terms of the price-to-net-asset-value (P/NAV) multiple, it is valued at 1.43 times for proved reserves or 1.09 times for proved and probable reserves, or 1.38 times for proved reserves or 1.06 times for proved and probable reserves, pro forma the Certus acquisition. These metrics indicate that Pine Cliff is inexpensive at this time.

{kind=link}

Table 1. Reserves and before-tax NPV-10 of Pine Cliff Energy as of December 31, 2022 (modified after Pine Cliff Energy)

To Pine Cliff shareholders, the greatest risk is probably the volatile natural gas prices. However, as discussed above, the downside risk is limited in the near term. Looking further ahead, the LNG Canada project at Kitimat is scheduled to come on stream in 2025. The Coastal Gaslink pipeline of TC Energy ( TRP ), now complete and capable of transporting 2.1 Bcf/d, will feed to the 14 Mtpa LNG Canada. The start-up of LNG Canada is supposed to be extremely bullish for Canadian natural gas producers, Pine Cliff Energy included.

Pine Cliff boasts a 7% decline rate, the lowest among Canadian E&P companies. The low decline rate allows Pine Cliff to reduce capital expenditures during times of low natural gas prices. Additional acquisitions may result in a rise in the decline rate, threatening the business model of Pine Cliff. Fortunately, Certus' corporate decline is only at 16%. Pine Cliff's pro forma base production decline rate is expected to be less than 10%, still ranking among the lowest for publicly-traded Canadian upstream companies, as illustrated in Figure 13.

{kind=link}

Fig. 13. Base decline rates for Canadian E&P companies (modified after Pine Cliff Energy)

As with other operators of mature wells, Pine Cliff has liabilities associated with the abandonment of wells at the end of their productive life. At this time, some 91% of its wells are still active.

For further details see:

Pine Cliff Energy: Buy This Natural Gas Stock For Its Sustainable 9% Dividend Yield