GOOGL - Pinterest: This Sell Decision Is Easy

Summary

- Shares of Pinterest have rallied in August, defying the broader market declines, owing to support from Elliot Management - one of its largest shareholders.

- Still, fundamentals were weak through Q2.

- Pinterest saw continued evaporation in users, while expenses rose tremendously - cutting into profits.

- Looking ahead, Pinterest doesn't have a well-defended niche in the social media space and is at risk of further deterioration.

The current volatility in the markets gives investors a really good opportunity to scrub through and really hone in on stock selection in their portfolios. I'm still of the mindset that current interest-rate dramas will settle by the end of the year and that markets should enjoy a modest lift through December - but that individual stock picks, especially within beaten-down tech plays, are the way to go from here on out.

Pinterest, Inc. ( PINS ), on the other hand, is a volatile name that I'd rather care not to buy into. Though Pinterest has lost nearly 40% of its value year to date, it has bucked the trend of recent tech decliners and actually rallied ~30% in August. The primary driver here is bullish commentary from its largest shareholder, Elliott Management - even though the company posted dismal Q2 results .

I remain soundly bearish on Pinterest. I think the entirety of the social media space is at risk at the moment. Look at the biggest of them all, Meta Platforms (META), which is undergoing leadership turmoil after the departure of COO Sheryl Sandberg and is struggling under the weight of ad-tracking/privacy changes. On top of that, user growth across the board is slowing as saturation kicks in and people spend less time idling online as they return to normal post-pandemic routines. Social media companies - especially the smaller ones - have had to invest tremendously into R&D (which is now increasingly expensive thanks to massive inflation in wages, especially in Silicon Valley) in order to bulk up their niches and continue appealing to users.

Pinterest's chief problem remains that it is bleeding users. Part of this is macro-driven (social media time seems to be on the decline) and part of it is company-driven (there are so many alternatives to Pinterest, and as social media companies age they tend to die slow deaths, with the exception of Facebook which has been able to reinvent itself through acquisitions like Instagram). Over the past few years, it has only been able to grow revenue by boosting ARPU, and it has only been able to do this through increasing ad load. Facebook also went through a period of chasing revenue growth through ad load, but this has its limits. In the long run, Pinterest will need to keep expanding its user base in order to continue reaping ad dollars - which is not something we have seen in a long time.

Valuation-wise, I don't find Pinterest cheap either. At current share prices near $23, Pinterest trades at a market cap of $15.32 billion. After we net off the $2.66 billion of cash on Pinterest's most recent balance sheet, the company's resulting enterprise value is $12.66 billion.

Versus current-year consensus revenue of $2.80 billion (data from Yahoo Finance ; representing 9% y/y growth), Pinterest trades at a 4.5x EV/FY22 revenue multiple. I find this quite expensive (especially in the current market where many high-quality software stocks with recurring revenue and a higher margin profile are trading at similar multiples) for a waning social media stock that is struggling to maintain single-digit revenue growth and has been shedding users for quite some time.

The bottom line here: the graveyard of social media stocks that have passed their fad eras is long, and I'm afraid Pinterest is on its way to joining them. Resist the temptation to buy Pinterest on its dip this year and sit on the sidelines. There are plenty better value plays to be had, especially in the SaaS sector: (DocuSign ( DOCU ), Okta ( OKTA ), Palantir ( PLTR ), and Appian ( APPN ) are some recent favorites of mine).

Q2 download

To me, Pinterest's Q2 print was exclusively a bad-news quarter with many red flags. Let's go through the highlights, starting with revenue growth:

{kind=link}

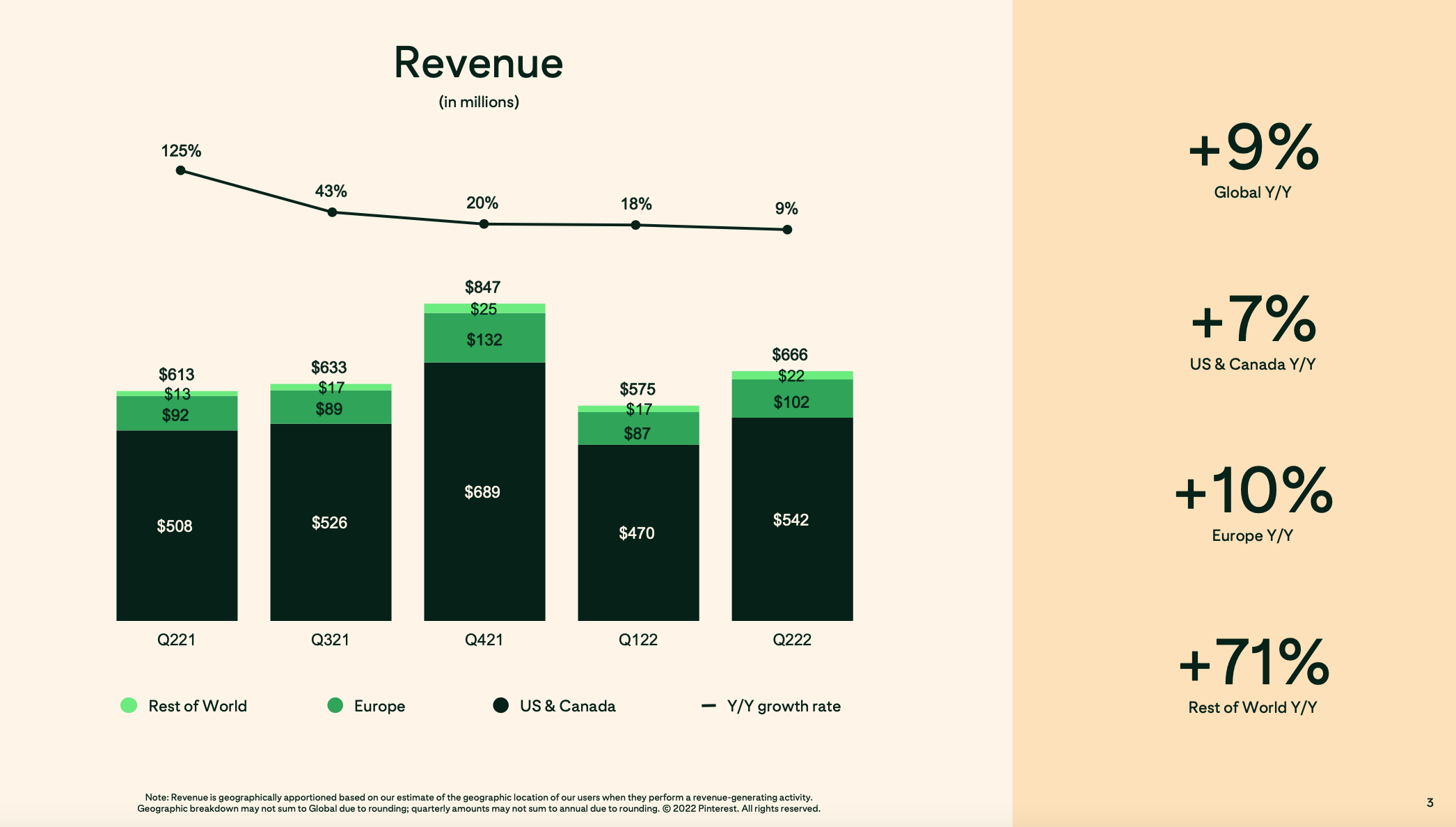

Pinterest grew revenue at a 9% y/y pace, decelerating seven points against 16% y/y growth in Q2. Again, the primary driver of revenue growth was ad load-driven ARPU expansion, as well as improved monetization in the company's rest of world segment (which still contributed to only a very small $22 million slice of the company's overall $665.9 million in revenue for the quarter). Pinterest, by the way, slightly missed Wall Street's expectations for $666.6 million in revenue for the quarter.

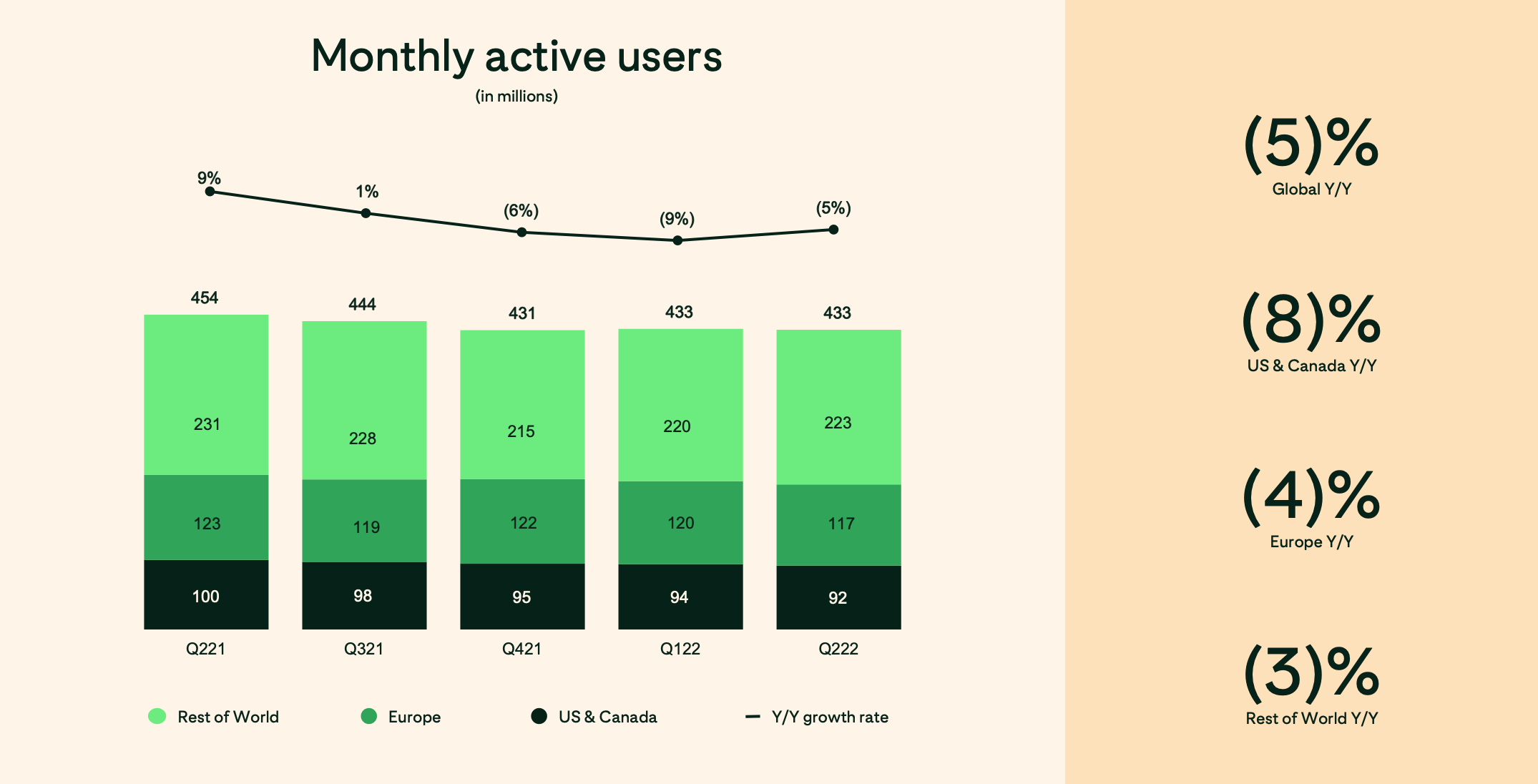

User trends continued to show steep declines. Globally, Pinterest maintained users flat to Q1, but sank -5% y/y. At a region level, the company lost 2 million users in the U.S. and 3 million in Europe, while adding 3 million users in other geographies.

{kind=link}

While net-users are flat sequentially, this is what we would consider a very unfavorable mix shift in users. In Q2, a U.S. user generated $5.82 in quarterly ARPU, versus just $0.10 in the rest of world. It's a clear message here: losing American users hurts, and it takes many more international users to make up for that loss.

There are a number of drivers behind the loss of users, including a change to Google's ( GOOG , [[GOOGL]]) search algorithm plus increased competition in short-form video from other social media outlets. Per new CEO Bill Ready's remarks on the Q2 earnings call:

Some of the factors contributing to our year-over-year MAU decline are easier to quantify such as lower search traffic, largely driven by Google's algorithm change in November of last year, which resulted in fewer new users and resurrections, and the last vestiges of the pandemic unwind, which we believe we largely lapped at the end of Q2.

We do also face increasing competition for time spent on competitive video-centric platforms, primarily in our mature markets, but it's challenging to quantify or measure the impact to our engagement on these platforms. These year-over-year declines were most pronounced for our web users, which dropped approximately 30% year-over-year, while our global mobile app users remain far more resilient, growing 8% year-over-year."

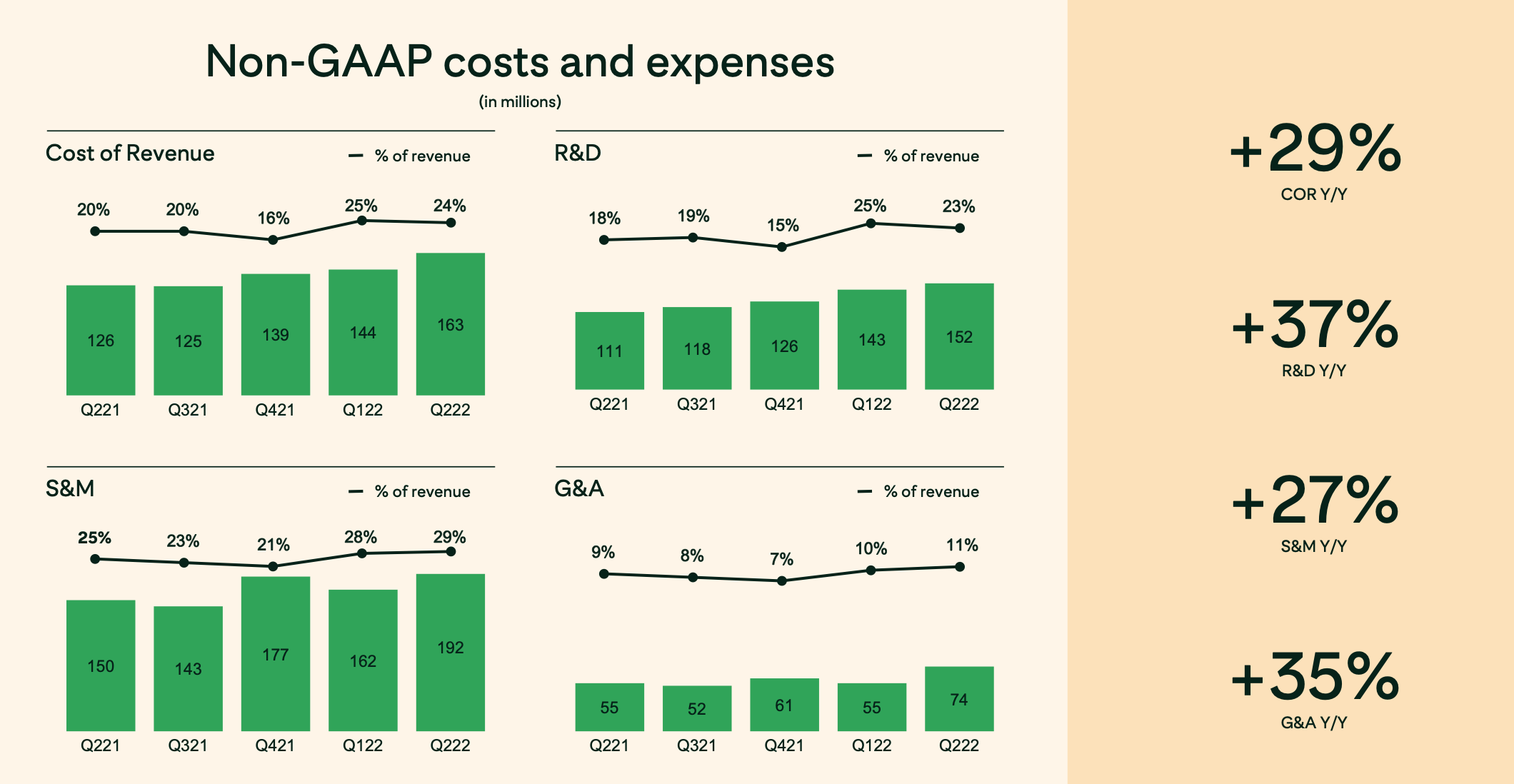

Adding insult to injury, however, each component of Pinterest's operating expenses ballooned y/y: most notably R&D spending, which jumped 27% y/y and consumed a staggering 23% of revenue:

{kind=link}

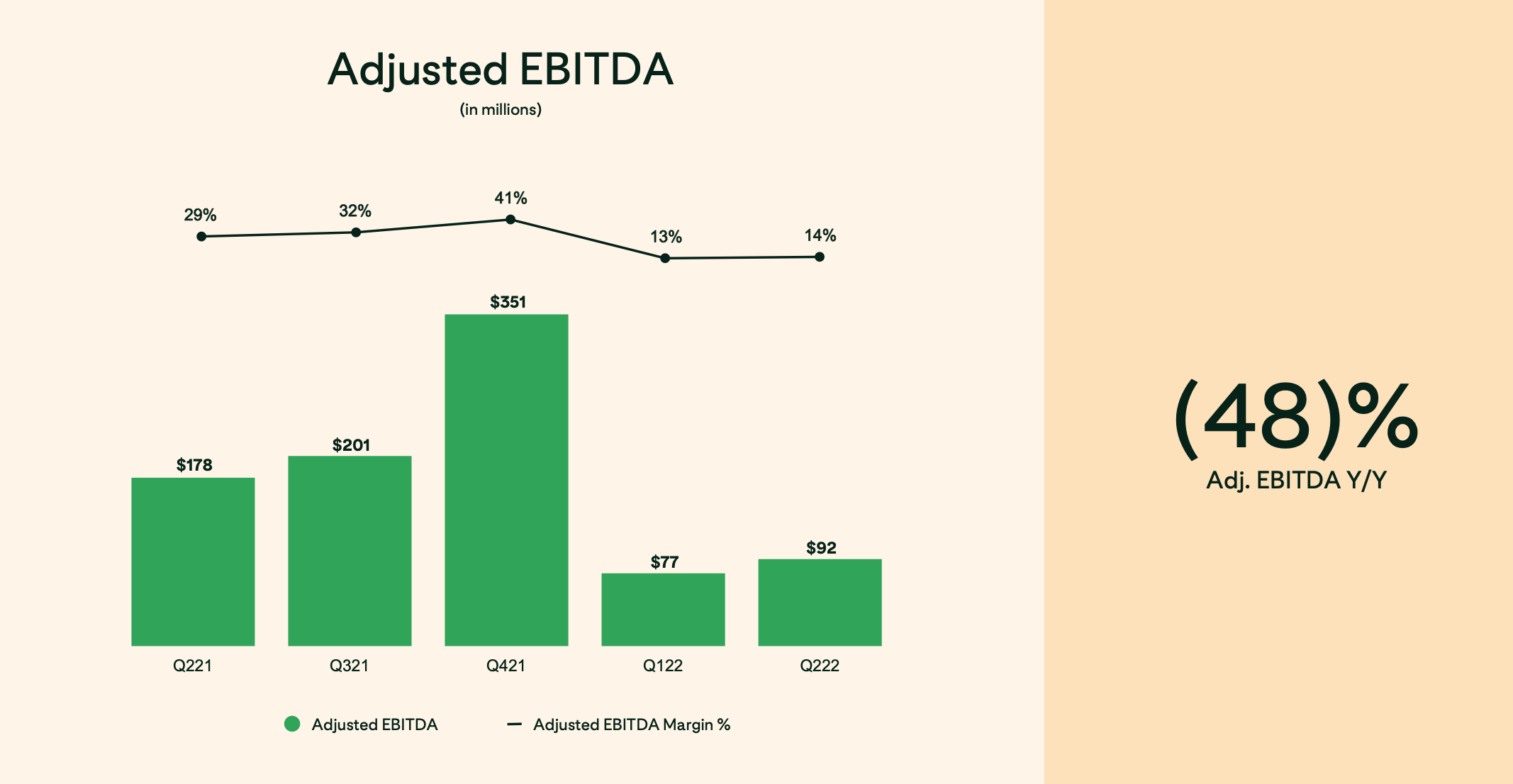

The net result here is that adjusted EBITDA fell -48% y/y to just $92 million, hitting a 14% adjusted EBITDA margin - fifteen points worse than 29% in the year-ago quarter.

{kind=link}

Key takeaways

Especially in the current risk-off market, Pinterest's sharp declines in profitability, plus the fact that there's no clear line of sight to recovering users particularly in the U.S., should increase selling pressure on this stock. I find very few catalysts that can lift this stock forward. Proceed with caution here.

For further details see:

Pinterest: This Sell Decision Is Easy