XOM - Pioneer Natural Resources Would Be A Crown Jewel For Exxon Mobil

2023-10-06 07:56:05 ET

Summary

- Exxon Mobil is considering a major acquisition of Pioneer Natural Resources, which would make it a leading Permian producer.

- PXD has a strong portfolio of assets in the Permian Basin and a focus on generating free cash flow.

- The acquisition price is estimated to be around $60 billion, and Exxon Mobil may need to issue substantial equity to fund the deal.

Exxon Mobil ( XOM ) is a $435 billion multinational oil and gas company, the largest publicly traded in the world besides Saudi Aramco. Rumor has it the company is considering a massive $60 billion acquisition of Pioneer Natural Resources ( PXD ), which would make a massive Permian producer at a 20% premium and represent one of Exxon Mobil's largest acquisitions.

As we'll see in that article, that acquisition would represent a strong incentive to invest in Exxon Mobil.

Pioneer Natural Resources Portfolio

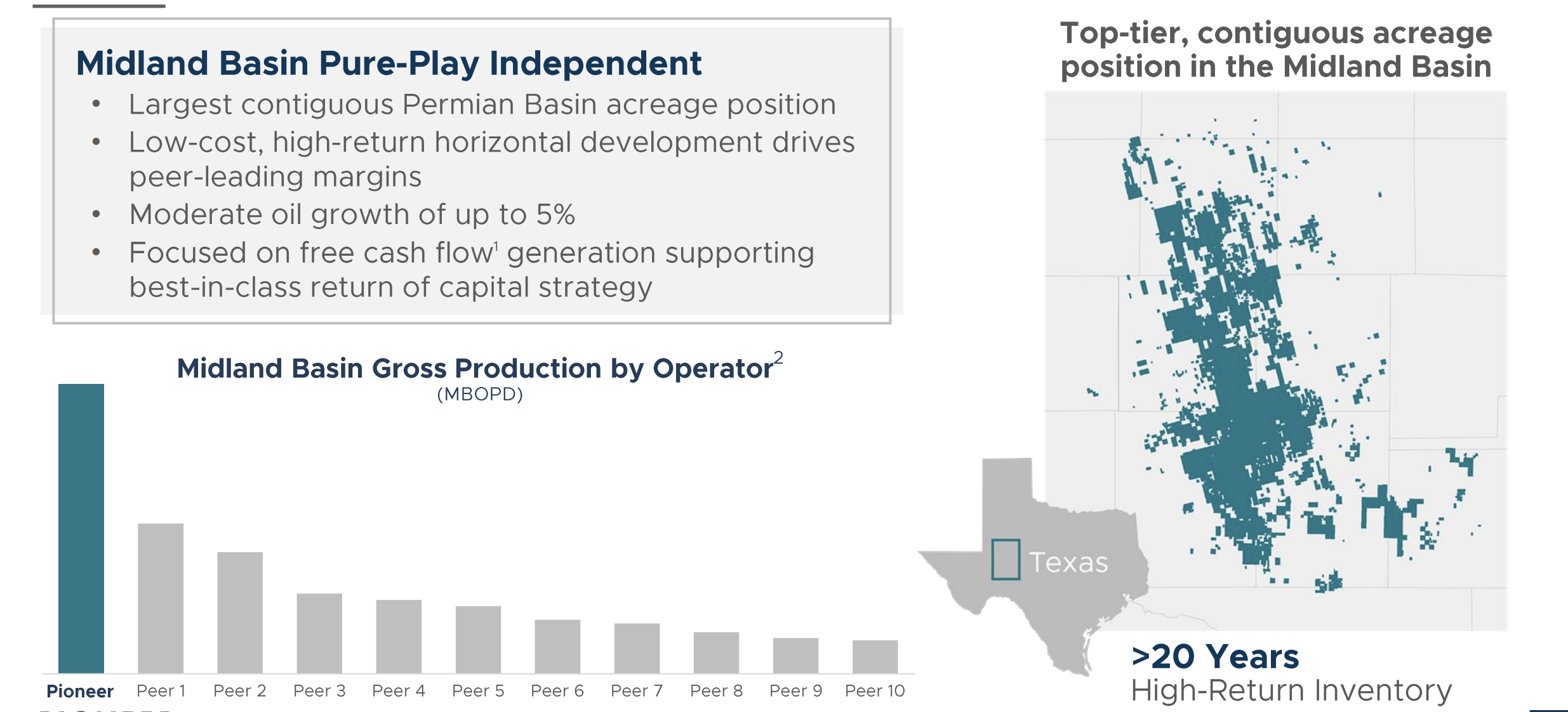

Pioneer Natural Resources has a strong portfolio of assets.

{kind=link}

The company has one of the strongest portfolios in the Permian Basin with more than 20 years of high-return inventory. More importantly, the company has one of the largest contiguous portfolio of assets with oil growth of up to 5%. The company is focused on FCF generation and continuing to take advantage of its strong portfolio.

The company's annualized FCF in the most recent quarter of $3 billion would be a ~5% FCF yield on the acquisition price, a relatively high price, but not bad given the company's continued production growth. The company's production has hit more than 700 thousand barrels/day and the company has increased guidance.

Acquisition Price and Cost

The acquisition price is currently estimated to be roughly $60 billion. That represents a ~20% premium to the company's current share prices, and Pioneer Natural Resources strong operations mean that the company was already trading at a relatively high share price. Unfortunately, Exxon Mobil's Denbury acquisition earlier this year was primarily in stock.

That means as much as we'd like to see Exxon Mobil utilize cash and debt to make the acquisition, we think it's likely that a substantial amount of equity will be issued to make the acquisition. That could substantially hurt Exxon Mobil's ability to drive long-term returns for existing shareholder returns with the acquisition.

Unfortunately, as the all-stock XTO Energy acquisition showed, an all-stock acquisition can position the company in a tough position.

{kind=link}

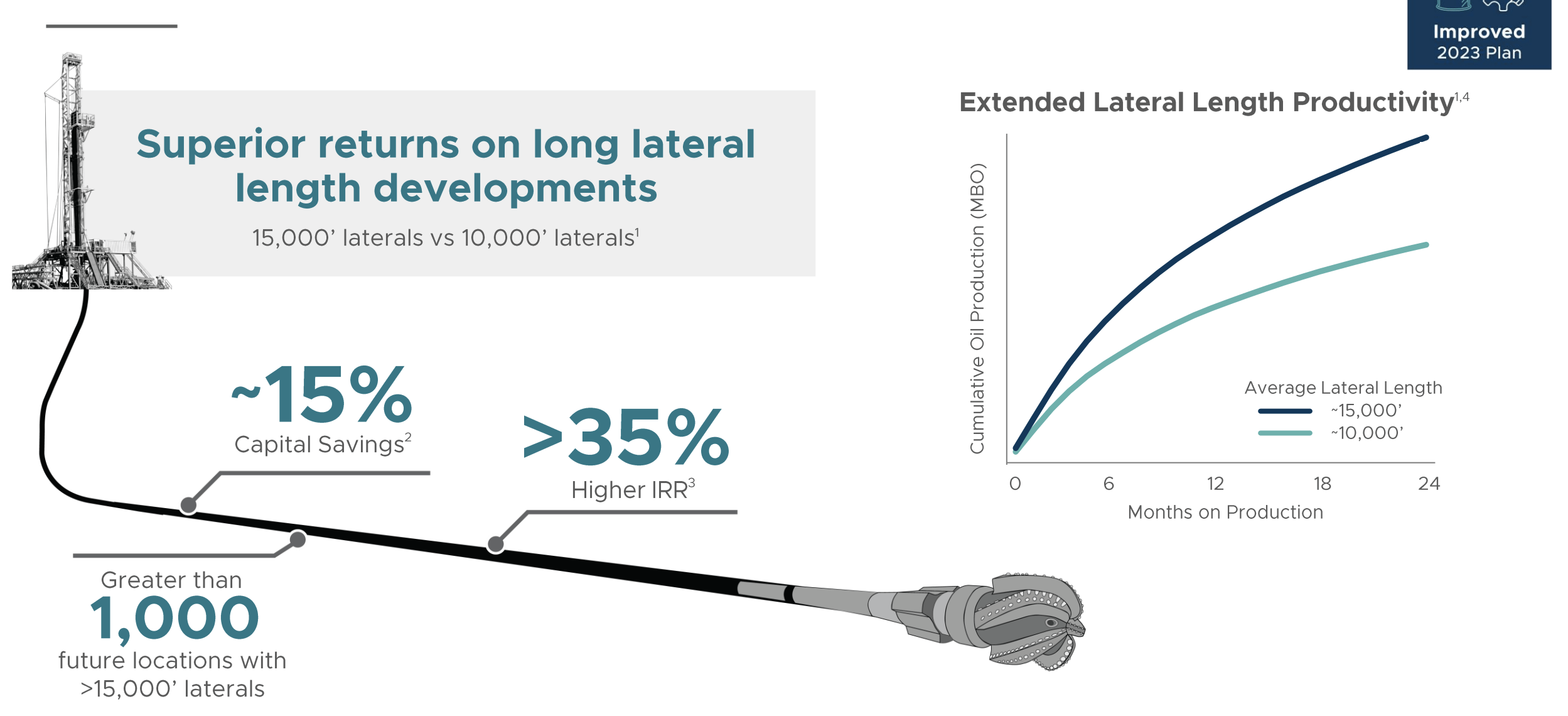

The question will become what are the synergies. Pioneer Natural Resources already runs a strong operation focused on cutting costs and capital spending. As with all other shale producers, they've already discovered that longer lateral developments lead to higher margins and much stronger returns for the portfolio.

To drill long laterals you need technical expertise and contiguous acreage. Pioneer Natural Resources already has substantial contiguous acreage, and Exxon Mobil's strong shale acreage will line up for that. Exxon Mobil is a leader in long laterals with almost 20 wells >17.5k feet, double any of the company's competitors. That expertise could lead to strong synergies.

Exxon Mobil Permian Basin Strategy

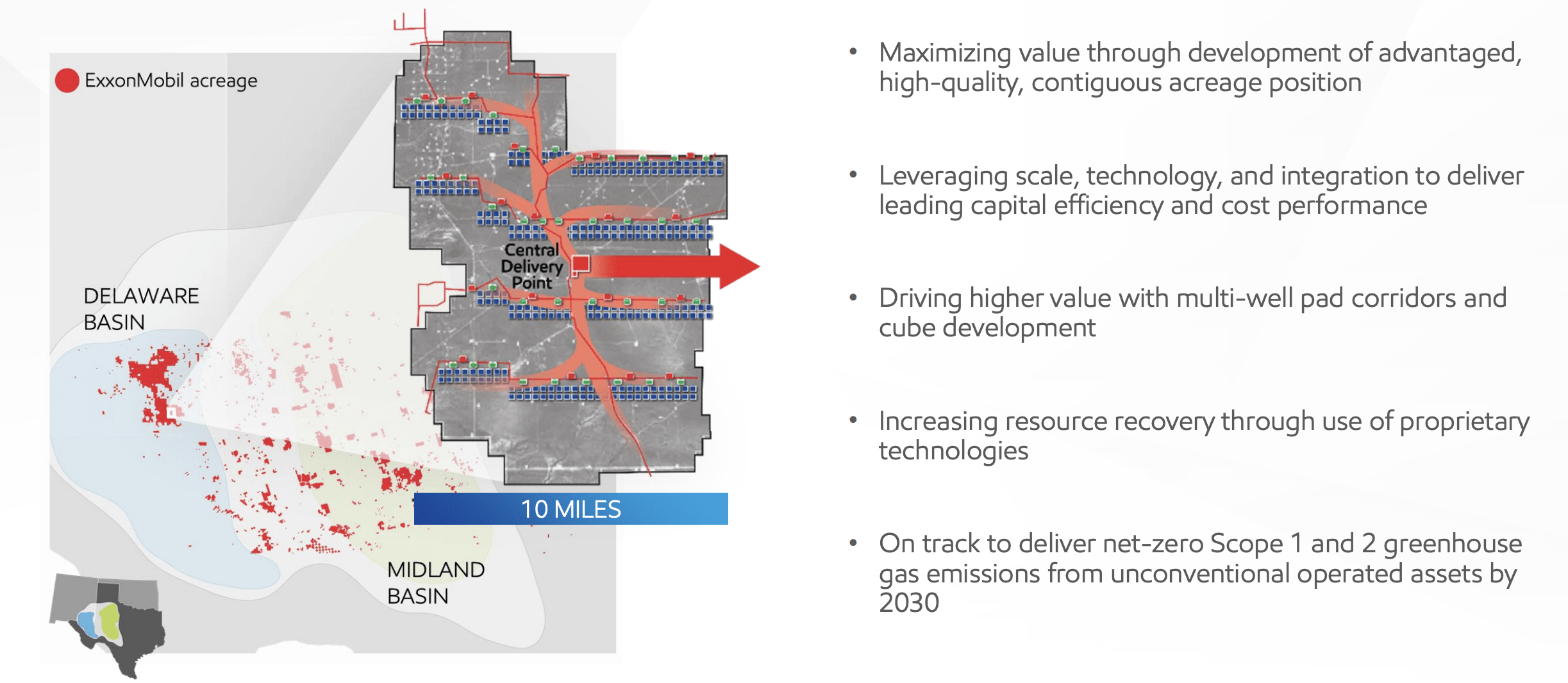

Exxon Mobil is continuing to scale up its Permian Basin assets to target a $15 / barrel breakeven.

{kind=link}

The company has the same strong acreage position we discussed elsewhere, and it's focused on continuing to develop shared central corridors. The company's cube development across its acreage leads to sustainable development and lower margins, while the company also works to increase resource recovery as well.

Additionally, the company expects to hit net-zero Scope 1/2 greenhouse gas emissions by the end of the decade a strong target. Another one of Pioneer Natural Resources risks is its Waha Exposure and Exxon Mobil's strong Permian Basin takeaway capacity tied into its existing acreage should have strong synergies as well.

Exxon Mobil Earnings Potential

The company is focused on growing its earnings and the production growth from Permian Basin will help the company.

{kind=link}

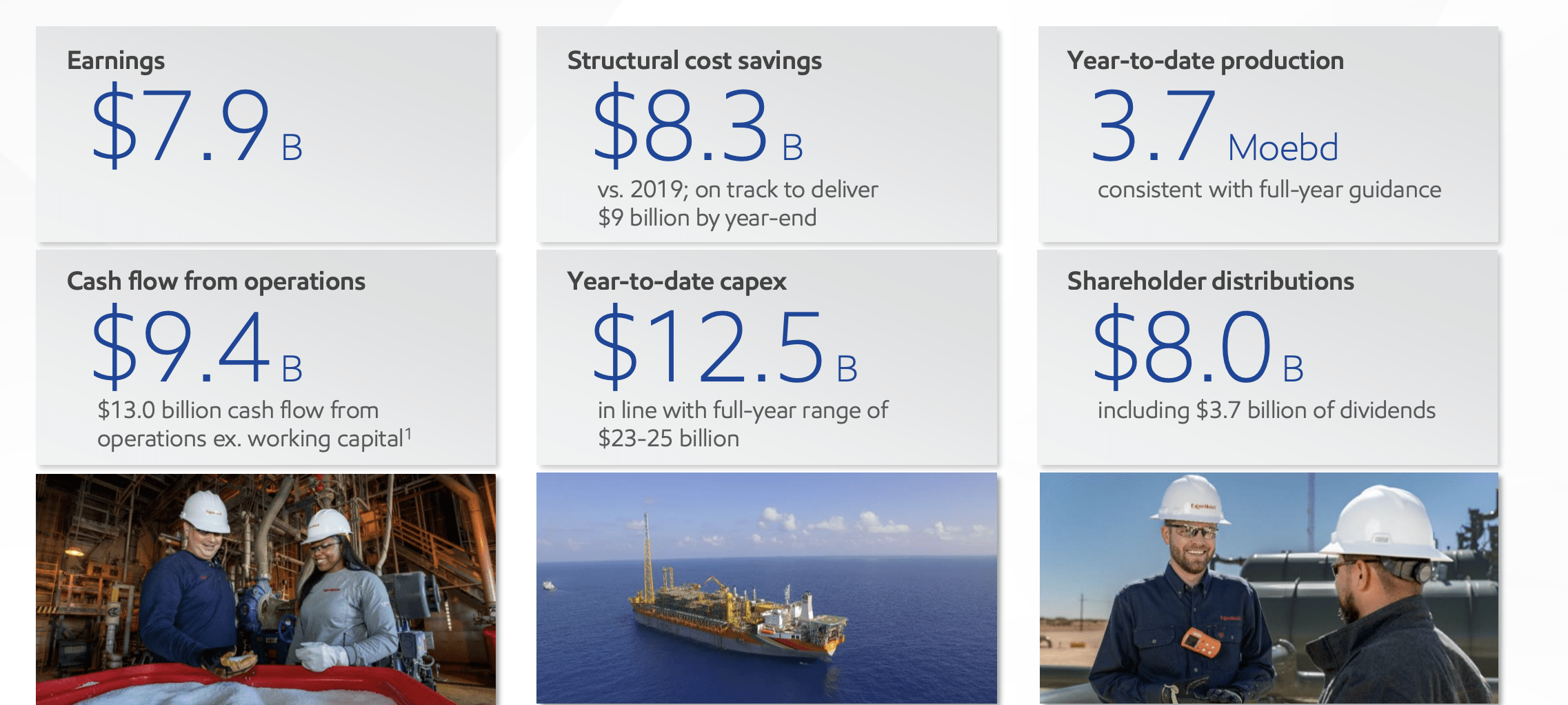

The company earned $7.9 billion in earnings in the most recent quarter and $8 billion in shareholder distribution. It has $9.4 billion in CFFO counting working capital but true FCF was more in the range of $7 billion with $6 billion in capex quarterly off of its $13 billion in CFFO. That's $28 billion in FCF giving the company a pre-acquisition FCF yield of 7%.

The company is continuing to target strong FCF growth. We expect it to lower its breakeven price and continue its production growth. That FCF strength should enable the company to both continue its 3.3% dividend yield and share repurchases. The necessity of share repurchases will depend on how it pays for the acquisition.

Thesis Risk

As Exxon Mobil works to diversify its portfolio for a changing climate, its largest risks continue to be climate change and crude oil prices. Crude oil prices have remained strong recently as demand has remained high but prices are always volatile. Any weakness in prices could hurt Exxon Mobil's share price substantially.

Conclusion

Exxon Mobil is a relatively expensive company right now with a strong portfolio of assets. However, a major acquisition of Pioneer Natural Resources would move the needle for the company, enabling it to grow its Permian Basin production while capturing substantial synergies. The company is a world leader in the Permian and can carry that skill to the acquisition.

More so with the recent strength in oil prices, the company is incredibly profitable. However, should prices drop, the company's ability to continue justifying its valuation and driving shareholder returns should drop substantially. That makes it a potentially risky investment. Let us know your thoughts in the comments below.

For further details see:

Pioneer Natural Resources Would Be A Crown Jewel For Exxon Mobil