ET - Plains All American: 8% Yield And Growth In The Permian Can Take Shares Higher

2024-01-12 09:00:00 ET

Summary

- Plains All American is undervalued and has an attractive net debt to Adjusted EBITDA metric, trading at an inexpensive valuation and paying an 8% yield.

- PAA is well-positioned in the energy infrastructure industry, with strong crude infrastructure connecting basins in middle America to the Gulf Coast.

- Increased oil production, particularly in the Permian Basin, is good news for PAA as it increases the demand for transportation and storage in the energy infrastructure industry.

It's no secret that I feel midstream operators are still undervalued. As a sector that I track through the Alerian MLP ETF (AMLP) the sector has finally gotten back to its pre-pandemic levels. While long-term MLP investors are still feeling the pain from the downward decline that started at the end of 2014 until the pandemic lows, many newer investors have substantially lower entry points into this asset class. Unlike SaaS or beverage companies, energy infrastructure is one of the hardest sectors for new competitors to compete in. Anyone can raise capital, hire engineers, build a product, and compete in the SaaS space. Individuals could also raise capital, reverse engineer a beverage, make some adjustments, hire a celebrity to be the face of the company, and try to compete. I am not saying that these two ideas would be profitable, but the companies could be created, the products could be made, and the companies could go to market and compete. Energy infrastructure is a much different arena, as you can't just raise capital, hire top-tier talent, and start building out pipelines or storage facilities. There are government and local regulations, zoning, environmental studies, land requirements, and other aspects that need to be accomplished prior to building any energy infrastructure assets.

Plains All American (PAA) is trading at an inexpensive valuation while having an attractive net debt to Adjusted EBITDA metric and paying an 8% yield. PAA has one of the strongest crude infrastructures connecting the basins throughout middle America to the Gulf Coast. I think PAA can still move higher while paying an enticing distribution that continues to grow.

{kind=link}

Following up on my previous article about Plains All American

Back in August, I wrote an article on PAA ( can be read here ) where I discussed why I felt PAA was positioned well for future appreciation while generating a generous distribution. Since then, units of PAA have appreciated by 1.87%, which has trailed the S&P 500's appreciation of 5.98%. When PAA's distribution is factored in, the total return is 3.7%. I am following up on my investment thesis, as we have significantly more U.S. energy production information than when I wrote my last article. While I am not an investor in PAA, I do think it is one of the best-positioned energy infrastructure companies to rally in 2024 and could be an acquisition target as more consolidation could occur across the industry.

PAA has some of the best energy infrastructure assets and is in the right basins at the right time

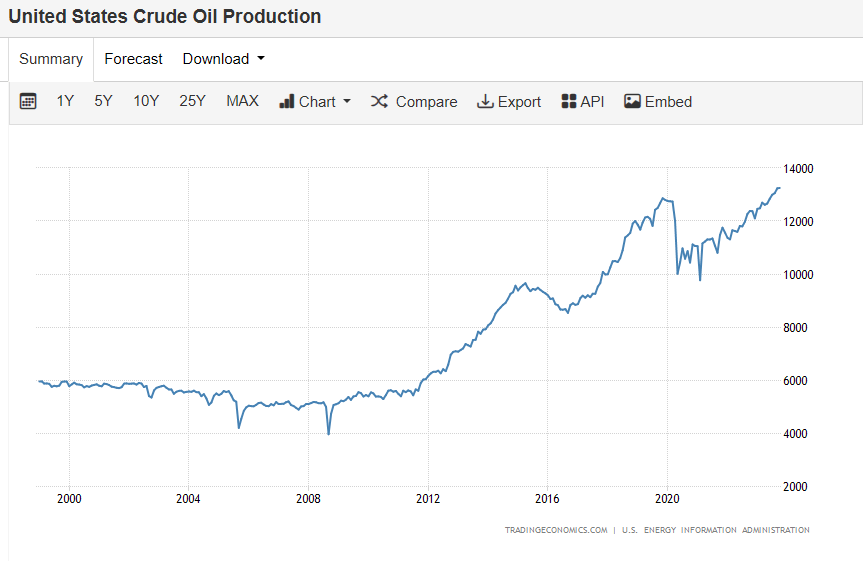

The United States has surpassed its pre-pandemic levels of oil production and has produced over 13 million barrels per day in August, September, and October. While there has been a certain narrative in the mainstream media around energy, the underlying fundamentals are showing a much different reality where more upstream production is occurring. While this is good news for upstream companies that have low break-even prices on each barrel, it's arguably better news for energy infrastructure companies. When oil and gas are produced, they need to be transported or stored, and higher levels of production increase the demand for transportation and storage throughout the energy infrastructure industry.

{kind=link}

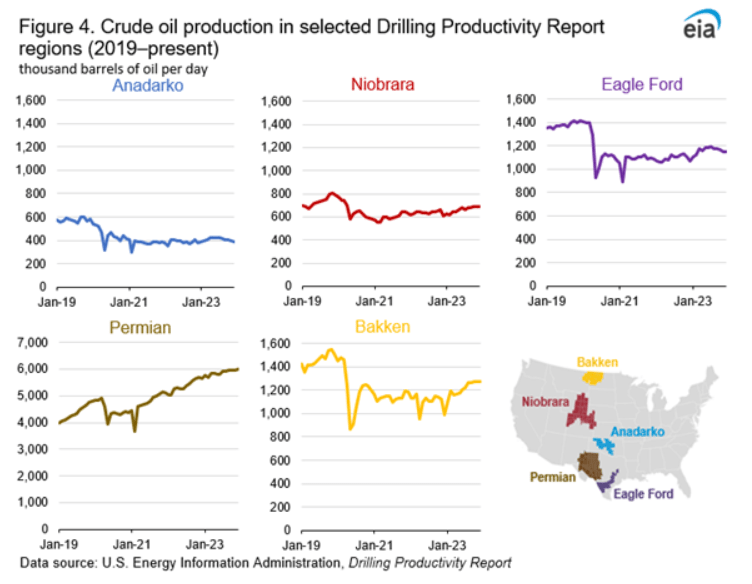

Below is the most recent drilling report I could find on the U.S. Energy Information Administration website. It clearly indicates that the Permian Basin is the only basin within the DPR region that is operating at peak production and continuously expanding the amount of production output. This is why so many companies are looking to increase their takeaway capacity in the region, as around 6 million barrels per day are being produced in the Permian, which is more than the combined production in the Anadarko, Niobrara, Eagle Ford, and Bakken basins.

Increased oil production is good for energy infrastructure companies, but the combination of increased oil production and increasing production in the Permian is great news for PAA. Most pipeline contracts are structured as either take or pay and fee-based contracts. When an upstream producer enters into a take-or-pay contract, the transporter, which in this case is PAA, is entitled to payment regardless of whether the contract capacity is met. Under the fee-based structure, a fixed fee is established and collected regardless of the volatility or fluctuation in commodity pricing.

{kind=link}

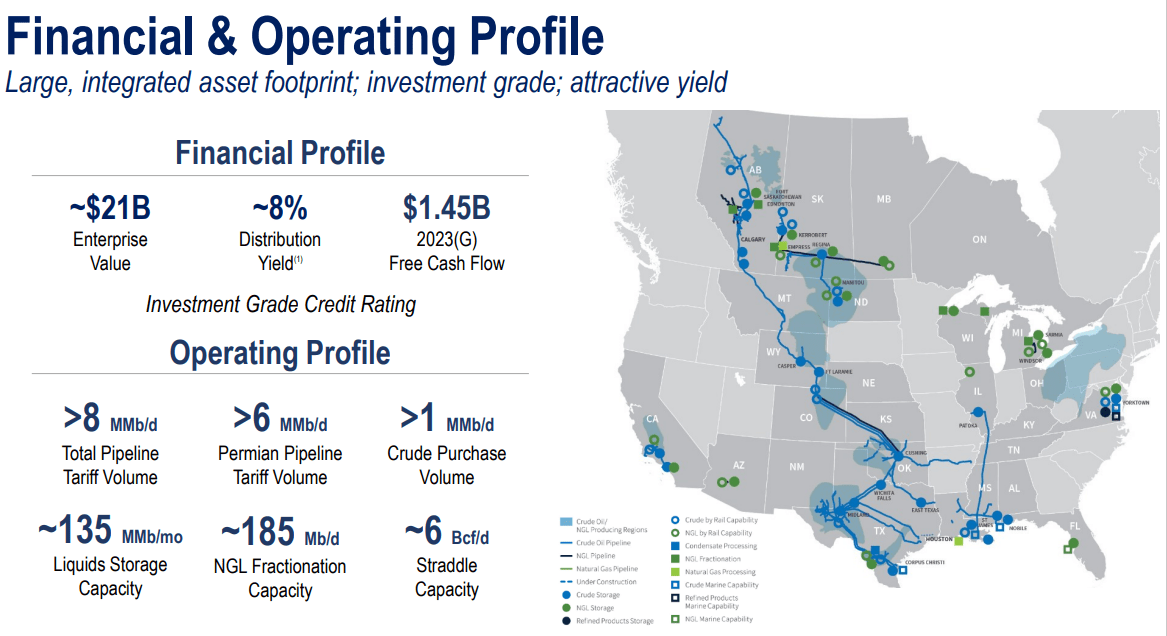

This sets PAA up for future growth as they recently closed on two gathering bolt-on acquisitions to boost their Permian capacity. These bolt-on acquisitions are expected to generate unlevered returns and enhance PAA's position in the Delaware Basin. The assets will allow PAA to expand its service and offerings while extending commercial relationships to its existing customers and any potential new customers in the future. PAA has one of the most robust crude systems in middle America, with over 8 MMB/d of capacity, of which more than 6 MMB/d is dedicated to the Permian. PAA is expecting to generate YoY growth in its crude segment driven by tariff volume increases. After accounting for the cash outlay for its recent acquisitions, PAA expects to generate $2.45 billion in cash flow from operations and $1.45 billion of free cash flow in 2023.

{kind=link}

There is an opportunity in the energy infrastructure sector in general, but the opportunity in PAA looks bigger

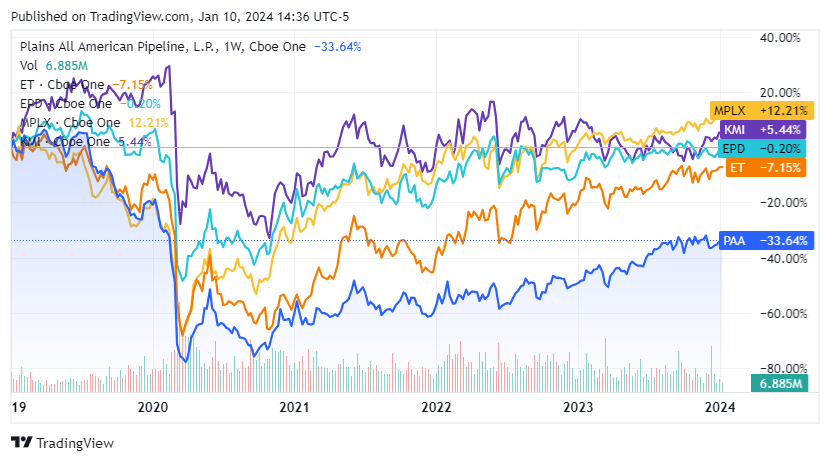

When I compare PAA to Energy Transfer (ET), Enterprise Products Partners (EPD), Kinder Morgan (KMI), and MPLX LP (MPLX) it still looks as if there is an opportunity. PAA has significantly underperformed its peers over the previous five years as it's still down -33.64%, while MPLX and KMI have gotten back to pre-pandemic levels, and EPD and ET are closing in on them. Just because the chart looks like PAA can close the gap, I always need to look at the underlying metrics to see if there is truly an opportunity. To establish this, I look at the enterprise value to Adjusted EBITDA, market cap to Adjusted EBITDA, market cap to distributable cash flow ((DCF)), net debt to Adjusted EBITDA, and the distribution yield.

{kind=link}

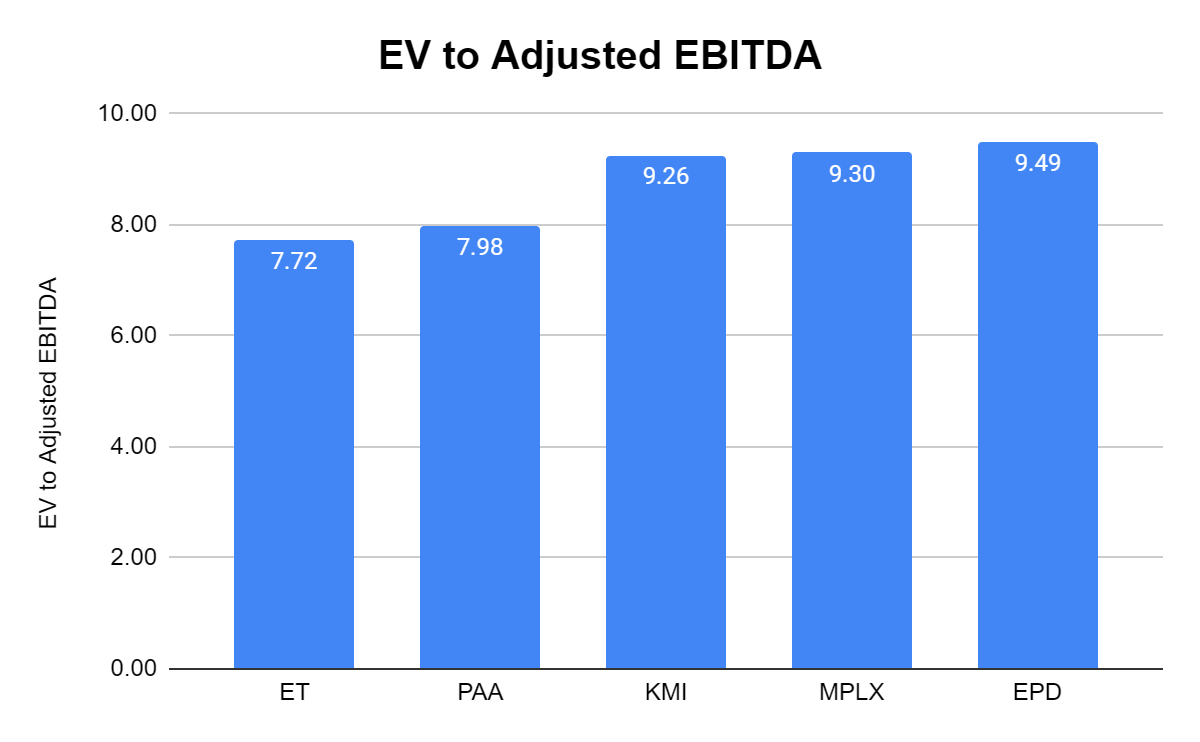

PAA trades at the second lowest enterprise value to Adjusted EBITDA valuation. Some prefer this metric because it incorporates the debt. PAA and ET look to trade at a much more enticing valuation than their peers.

{kind=link}

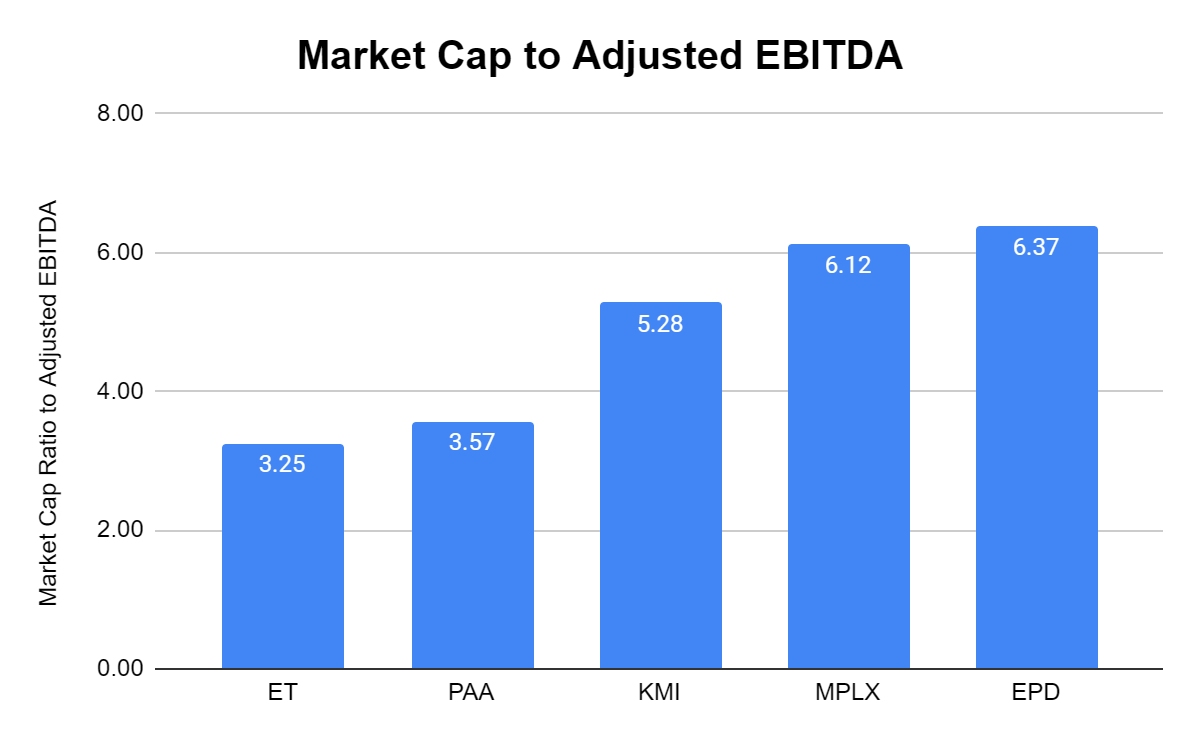

When I look at the market cap to Adjusted EBITDA ratio ET and PAA are neck and neck while their peers trade at significantly larger valuations. The peer group trades at 4.92x average multiple while PAA trades at 3.57x its Adjusted EBITDA.

{kind=link}

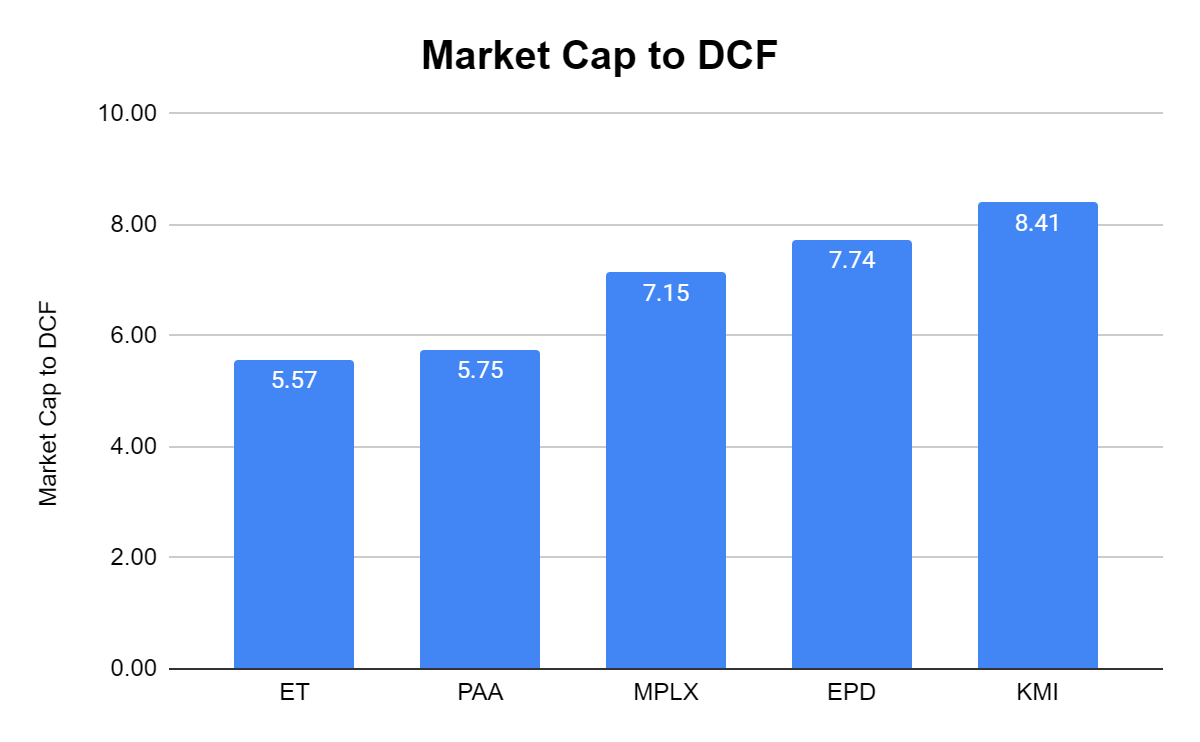

The reason I look at the market cap to DCF is because I want to see how cheaply I can purchase a company's distributable cash flow. Today, I can purchase PAA at 5.75x its distributable cash flow while the peer group trades at an average of 6.93x.

{kind=link}

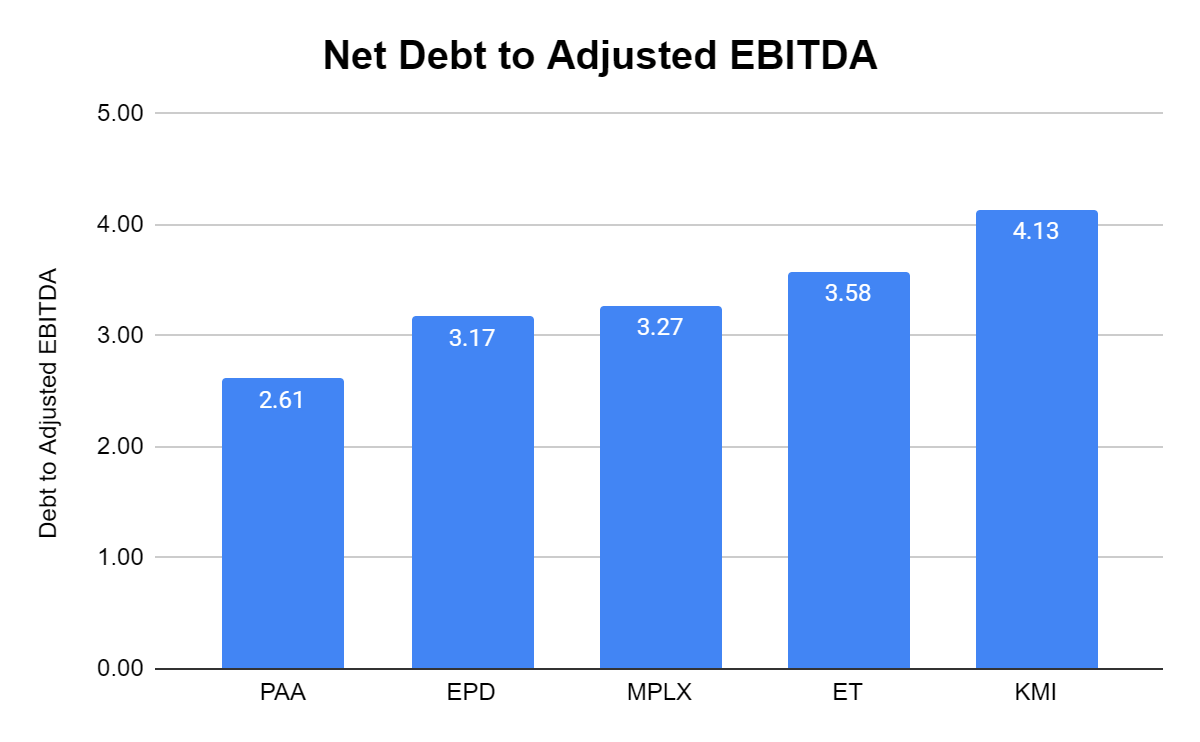

Pipeline companies have always been correlated to large debt loads, so I look at the net debt to Adjusted EBITDA metric. This allows me to see how leveraged these companies are. PAA is trading at the lowest net debt to Adjusted EBITDA valuation and well under the 3.35x peer group average.

{kind=link}

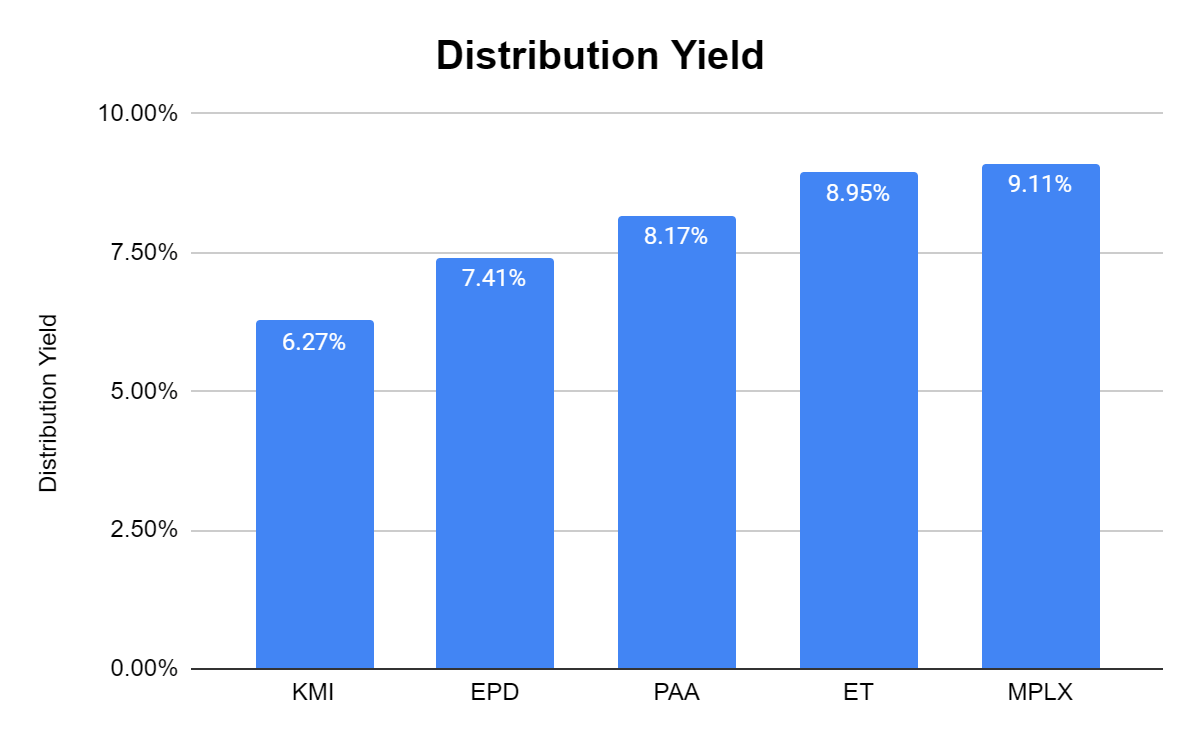

The last thing I am looking for is yield. Pipelines have always been looked at as income plays, so it's no surprise that the peer group average has an average yield of 7.98%. PAA has an 8.17% distribution yield, and I am paying 5.75x its distributable cash flow and 3.57x its Adjusted EBITDA, which looks very enticing.

{kind=link}

Risks to my investment thesis

Investing in the oil patch is always risky, and just because the valuation and yield looks good, doesn't mean it's a sure thing. The oil patch, in general, is fighting a battle against an energy transition with strong supporters in power positions. PAA, in general, could face tougher scrutiny with future permits and fines and damages if the pipeline leaks or explodes. If breakthroughs in energy occur that reduce the need for oil and gas, that would also impact PAA. Nobody can predict the future, but there are some very smart people working tirelessly to develop breakthroughs in energy, and when that occurs, we could see lower utilization numbers from traditional fossil fuels.

Conclusion

Despite the risks, I am still bullish on the energy sector. I think that more investors will gravitate toward pipelines as a source of generating income as the risk-free rate of return declines. I think that PAA has further to run in 2024 as it's still trailing its peers when looking at how the group has recovered since the pandemic. PAA has an asset base that is next to impossible to replicate as its pipelines connect all of the major basins in middle America with a strong focus on the Permian, which is the most sought-after land for drilling oil. As oil production continues to increase, the demand for takeaway capacity will grow, and this is a catalyst for PAA, especially since most of the growth occurs where most of their takeaway capacity is. I think PAA is trading at an enticing valuation, and investors are getting an 8% yield to wait for the story to unfold. While I am not invested in PAA, I think it's one of the stronger opportunities in the sector.

For further details see:

Plains All American: 8% Yield And Growth In The Permian Can Take Shares Higher