XOM - Plains All American Pipeline: Solid Q4 Earnings Good Core Holding For Income Portfolios

Summary

- Plains All American Pipeline's results disappointed analysts as the company announced both revenue and earnings misses.

- The company's volumes and cash flows were up, although its reported volumes look a bit strange and bear further investigation.

- The company had an impairment charge during the quarter that made its earnings look worse than they really were.

- The company's balance sheet appears quite strong and its leverage is reasonable.

- The 8.55% yield is not only sustainable, but PAA could conceivably increase it with no real trouble.

On Wednesday, February 8, 2023, crude oil-focused pipeline giant Plains All American Pipeline ( PAA ) announced its fourth quarter 2022 earnings results. At first glance, these results were rather disappointing as the company missed the expectations of analysts both in terms of revenue and earnings. The company, therefore, bucked the trend that we have been seeing across the midstream sector recently as many of the company’s peers reported remarkably strong results. However, as I have pointed out in numerous past articles, net income is not the best metric to use to measure the financial performance of these companies due to various large non-cash charges that asset-heavy master limited partnerships experience. This is certainly the case here as a closer look at Plains All American Pipeline’s earnings report reveals that the company performed fairly well. In fact, there is very little to be disappointed about here and while this company may not have as much forward growth potential as some of its peers, it still looks like a pretty good way to get an 8.55% yield today.

Plains All American Q4 Earnings Results Analysis

As my long-time readers are no doubt well aware, it is my usual practice to share the highlights from a company’s earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from Plains All American Pipeline’s fourth quarter 2022 earnings report:

- Plains All American Pipeline brought in total revenue of $12.952 billion during the fourth quarter of 2022. This represents a 0.28% decline over the $12.989 billion that the company brought in during the prior-year quarter.

- The company reported an operating loss of $37.0 million during the reporting period. This compares very unfavorably to the $600 million operating profit that the company reported in the year-ago quarter.

- Plains All American Pipeline transported an average of 8.094 million barrels of crude oil per day during the most recent quarter. This represents a steep 12.39% increase over the 7.202 million barrels of crude oil per day that the company transported in the equivalent quarter of last year.

- The company reported a distributable cash flow of $410 million in the current quarter. This represents a 6.22% increase over the $386 million that the company reported last year.

- Plains All American Pipeline reported a net income of $263 million in the fourth quarter of 2022. This compares rather unfavorably to the $450 million that the company earned in the fourth quarter of 2021.

It seems essentially certain that the first thing most readers will notice here is that Plains All American Pipeline generally saw its financial performance decline relative to the year-ago quarter. This makes the company an exception to the trend that we have been seeing across the sector. After all, most midstream companies have been reporting stronger earnings than a year ago. Curiously, the lower revenues come in spite of the fact that the company’s volumes were up across the board:

| Q4 2022 |

| Q4 2021 |

| Crude Oil Tariff Volumes (mbpd) |

| 8,094 |

| 7,202 |

| Natural Gas Liquids Fractionation Volumes (mbpd) |

| 155 |

| 127 |

| Natural Gas Liquids Pipeline Volumes (mbpd) |

| 222 |

| 189 |

| Propane and Butane Sales |

| 128 |

| 125 |

As I have mentioned in the past, Plains All American Pipeline’s revenue and cash flow depend on resource volumes, not on values. With that said, crude oil prices were still higher in the fourth quarter of this year than in the equivalent period of 2021. I pointed this out in a previous article . The company’s management provided no information about why the company’s revenue came in weaker than last year when tariff volumes are up. It could possibly be due to declining margins in the company’s fractionation volumes and propane sales, but those operations are such a small part of the company’s business that it is difficult to believe that they would have much of an impact.

The company’s reported crude oil tariff volumes also seem a bit strange. According to the U.S. Energy Information Administration, the United States produced an average of 12.337 million barrels of crude oil per day in November 2022:

{kind=link}

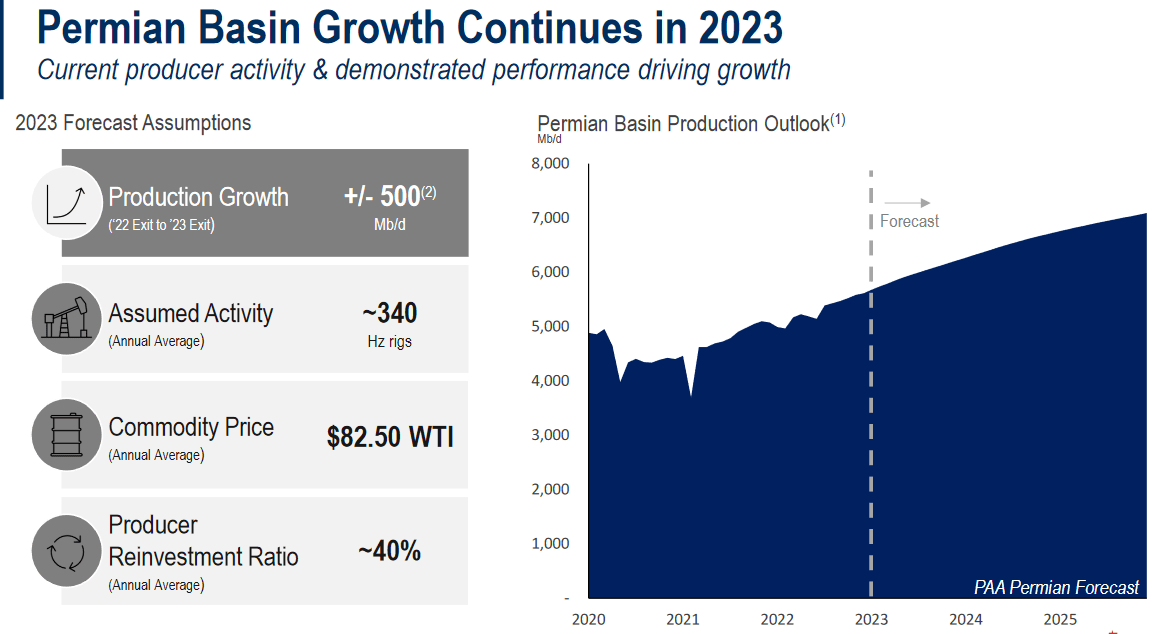

Thus, Plains All American Pipeline’s reported volumes would have it transporting 65.6% of the entire crude oil production of the United States. That cannot possibly be correct as no single midstream company has such a dominating presence in the market. With that said, we can draw some conclusions by looking at the per-basin numbers. Plains All American Pipeline reports that it transported an average of 6.195 million barrels of crude oil per day in the Permian Basin region during the quarter. However, during the conference call, Willie Chiang, Plains All American Pipeline’s Chairman and CEO, made the following statement,

“As shown on slide 5, we anticipate 2023 Permian crude oil production to grow plus or minus 500 thousand barrels per day exit-to-exit, based on an assumed 2022 exit production level of approximately 5.65 million barrels per day.”

Here is the slide referenced by Mr. Chiang:

{kind=link}

In other words, it appears the company’s earnings report actually states that its volumes in the Permian Basin were higher than the entire production of the Permian Basin during the period! That allows us to draw the logical conclusion that the company likely had situations in which crude oil left its pipeline network, re-entered it, and got counted for a second time. Thus, the company does not actually transport two-thirds of the crude oil production in the United States. Ultimately, it does not matter though since the most important thing here is that Plains All American Pipeline saw its transported volumes increase, which should have had a positive impact on its financial performance. It clearly did not in terms of revenue or earnings.

We can find the solution to this problem by looking at the company’s California infrastructure. The company reported a $330 million impairment charge related to its California assets during the quarter. There was no impairment charge in the prior-year quarter. The company did not state what assets these were during the conference call, nor is there any news release regarding Plains All American Pipeline selling anything in California during 2022. The company did sell three interconnected terminals in California to Zenith Energy back in 2020, though. It is likely that this is the cause of that impairment charge but it seems strange that a sale back in 2020 would have an impact on the company’s results in the most recent quarter. It would have been nice to have some insight from management regarding the actual source of this charge.

Fortunately, impairment charges are non-cash expenses as they do not actually represent money leaving the company. They only exist because of an accounting rule that requires a company to reduce its income when the value of the assets on its balance sheet declines. Thus, they are basically a way for the company to save money on taxes. The most important thing for our purposes as income investors is the company’s cash flow. After all, it is ultimately cash that the company uses to pay our distributions, buy back stock, or repay its debt. Plains All American Partners did quite well at this during the fourth quarter:

| Q4 2022 |

| Q4 2021 |

| Adjusted EBITDA |

| $659 |

| $564 |

| DCF |

| $410 |

| $386 |

(all figures in millions of U.S. dollars)

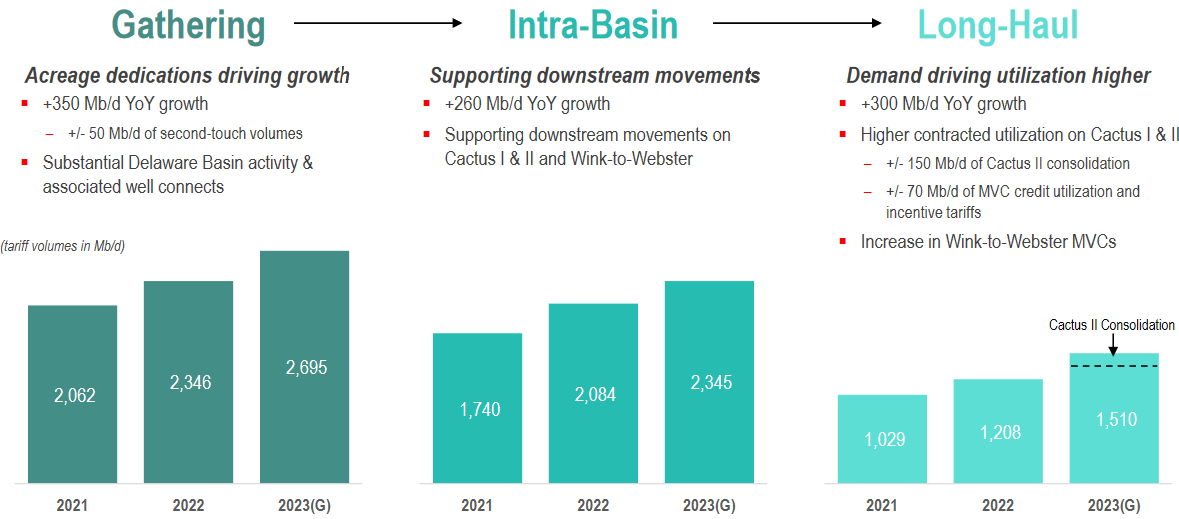

This was mostly driven by the higher volumes that we saw moving through the company’s pipeline and other infrastructure during the quarter. Fortunately, it does seem likely that this will increase going forward. As Mr. Chiang noted above, it is likely that production will grow in the Permian Basin during 2023. I have pointed this out in the past as we are seeing companies like ConocoPhillips ( COP ) planning for higher production going forward. With that said, they are doing it quite cautiously so it seems very unlikely that we will see a production growth rate that is anywhere close to what it was over the 2016 to 2020 period. However, production growth should still translate into higher volumes for Plains All American Pipeline as the company is one of the largest operators of crude oil pipelines in the United States so it is only logical that the company will get at least some of this business. The company itself is projecting this and has guided for higher volumes through its Permian Basin infrastructure:

{kind=link}

This should result in a growing cash flow for the company. That is something that would be nice to see, particularly for those hoping for distribution growth. The company actually did just increase it, although it remains lower than it did prior to the pandemic. Obviously, more money would be useful for us as we try to maintain our standard of living in the face of inflation. The nice thing here is that we do have some confidence that the company’s volumes will come in at least somewhat close to its guidance. This is because upstream producers tend to share their production plans with midstream operators because the midstream company needs to make sure that it has the infrastructure in place to meet the demand of its customer. Thus, we can be fairly confident that Plains All American Pipeline will indeed be able to deliver us some cash flow growth in 2023.

Financial Considerations

It is always important that we look at the way that a company funds its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. That, unfortunately, can cause a company’s interest expenses to increase following the rollover in certain market conditions. In addition, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company’s cash flow to decline can push it into insolvency if it has too much debt. Although midstream partnerships like Plains All American Pipeline usually have remarkably stable cash flows due to their contractual volume-based business model, this is still a risk that we should not ignore.

The usual way that we judge a midstream company’s ability to carry its debt is by looking at its leverage ratio. This ratio, which is also known as the debt-to-adjusted EBITDA ratio, essentially tells us how many years it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. As of December 31, 2022, Plains All American Pipeline has a leverage ratio of 3.7x based on its trailing twelve-month adjusted EBITDA. That is a reasonable ratio that is generally in line with the most well-financed firms in the industry. As I have pointed out in previous articles, Wall Street analysts generally consider anything below 5.0x to be acceptable for a midstream partnership. I am much more conservative and like to see this ratio under 4.0x, which is where most midstream partnerships have been trying to get their leverage ratios in the two years since the pandemic. It is nice to see that Plains All American Pipeline easily meets this ratio and in fact, the company wants to try and get it down under 3.5x for the long term. That would be nice to see, but it is not really necessary. Overall, the company’s leverage is fine here.

PAA Stock Distribution Analysis

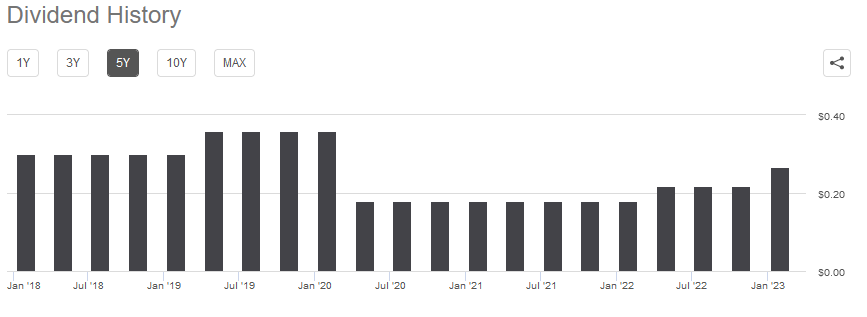

One of the biggest reasons that we invest in midstream partnerships is because of the high yields that they typically possess. Plains All American Pipeline is certainly no exception to this as the company currently boasts an 8.55% yield. The company, unfortunately, did cut its distribution back in 2020 in order to focus some attention on fixing its finances, but it has been working to restore it since that time:

{kind=link}

The company’s current distribution of $0.27 per unit is well below its pre-pandemic level. However, the recent increase was 18.52%, which is above the rate of inflation that we saw in 2022. This is something that is very nice to see right now, particularly as upstream producers like Chevron ( CVX ) and Exxon Mobil ( XOM ) have been giving us token increases. The reason that such a large distribution increase is nice to see right now is that the forty-year high inflation rate has been greatly reducing the number of goods and services that we receive from the investments in our portfolios. This has had the effect of making us feel poorer and poorer with every passing month. The fact that Plains All American Pipeline provided such a large increase offsets this increase and ensures that we can still buy as much with the distribution as we could previously.

As is always the case though, it is critical that we ensure that the company can actually afford the distribution that it pays out. After all, we do not want it to be forced to reverse course and cut the distribution once again. That would both reduce our income and almost certainly cause the company’s unit price to decline.

The usual way that we judge a midstream partnership’s ability to maintain its distribution is by looking at its distributable cash flow. The distributable cash flow is a non-GAAP metric that theoretically tells us the amount of cash generated by the company’s ordinary income that is available for distribution to the limited partners. As stated in the highlights, Plains All American Partners reported a distributable cash flow of $410 million during the fourth quarter of 2022. This works out to $0.58 per common unit but the company only pays out $0.27 per common unit. That gives Plains All American Pipeline a distribution coverage ratio of 2.15x. That is, to put it mildly, an almost unreasonably high level. Wall Street analysts normally consider anything over 1.20x to be reasonable and sustainable. I usually like to see this ratio above 1.30x in order to add a margin of safety to the investment. At 2.15x, Plains All American Pipeline should not only have no trouble at all maintaining this distribution but could safely increase it by quite a bit and still be able to maintain it. In fact, if the company were to drop this ratio down to 1.60x, it could have a distribution of $0.36 per unit. That would give the company an 11.39% yield at the current price and it would still be easily sustainable. Thus, investors should have no concerns at all about the distribution at the current price. If anything, they should be complaining that it is not higher.

Conclusion

In conclusion, Plains All American Pipeline had some interesting results in the latest quarter. The market was certainly a bit disappointed by them but overall, they were not that bad. My biggest concern here is that I wish management was a bit more forthcoming during the conference call. The company posted year-over-year cash flow growth, which is always nice to see, and it is likely to be able to produce further growth next year. The company ended the year with a fairly strong balance sheet and a very high distribution coverage ratio. Overall, the company looks like a very reasonable core holding in any income investor’s portfolio.

For further details see:

Plains All American Pipeline: Solid Q4 Earnings, Good Core Holding For Income Portfolios