ET - Plains All American: Reasonable Well-Financed Play In Crude Oil Midstream

2023-04-25 13:51:06 ET

Summary

- Plains All American Pipeline, L.P. is one of the largest crude oil-focused midstream partnerships in the United States.

- The company enjoys remarkably stable cash flows regardless of energy prices.

- The global demand for crude oil is not likely to surge going forward, which greatly limits the company's forward growth prospects.

- The partnership has one of the strongest balance sheets in the industry and investors should not have to worry about its leverage.

- Plains All American Pipeline, L.P. can easily carry its 8.06% yield and may increase it in order to provide investors with a reward in the absence of growth.

Plains All American Pipeline, L.P. ( PAA ) is one of the largest midstream partnerships in the United States, boasting a network of infrastructure that stretches throughout much of the central part of the nation. As is the case with most master limited partnerships, or MLPs, the company has been fairly popular among income-focused investors, although it does not have as good of a distribution history as some of them. One of the reasons for this popularity is that the company boasts a very high 8.06% yield at the current price along with remarkably stable cash flows. However, its focus on crude oil means that it does not have the same growth potential as some of its natural gas-focused cousins. The yield is still high enough to provide an acceptable total return, though, so this company should not be overlooked when constructing your energy-income portfolio.

About Plains All American Pipeline

As mentioned in the introduction, Plains All American Pipeline is one of the largest midstream partnerships in the United States. The company has a network of liquids pipelines and other infrastructure stretching across much of the central portion of the United States:

Plains All American Pipeline

The company’s infrastructure is primarily centered around crude oil pipelines that are capable of carrying approximately seven million barrels of liquid hydrocarbons per day. The overwhelming majority of this capacity, approximately five million barrels of liquid hydrocarbons per day, services the Permian Basin in West Texas, which has been the focal point of the American energy renaissance over the past ten years. In addition to these pipelines, Plains All American Pipeline has storage facilities that are capable of storing 135 million barrels of liquids along with 185,000 barrels per day of natural gas liquids fractionation capacity. Thus, while the company is certainly not as large as some of its peers like Enterprise Products Partners ( EPD ) or Energy Transfer ( ET ), it is still a force to be reckoned with in the industry.

One thing that we note above is that Plains All American Pipeline’s infrastructure extends to reach just about every major resource basin in which crude oil is produced. This is nice for diversification because each of these basins has different fundamental dynamics. For example, it is much cheaper for an upstream producer to operate in the Permian Basin than in the Bakken Shale. As a result, during times of low energy prices, Bakken production will decline more than Permian Basin production. We saw this during the COVID-related lockdowns and the resulting decline in energy prices. We did see a major production surge in the Bakken Shale around the end of 2020, though, that we did not see in the Permian Basin. This is partly due to the fact that upstream producers can more rapidly spin up production in that tight oil play due to the geology of the region. The fact that Plains All American Pipeline has exposure to all of these different regions provides it with a certain amount of diversification benefits and lessens its dependence on any single region.

As might be expected from the high energy prices that have persisted in the market over the past two years, production in all of the major basins in the United States has been climbing. We can clearly see that here:

U.S. Energy Information Administration

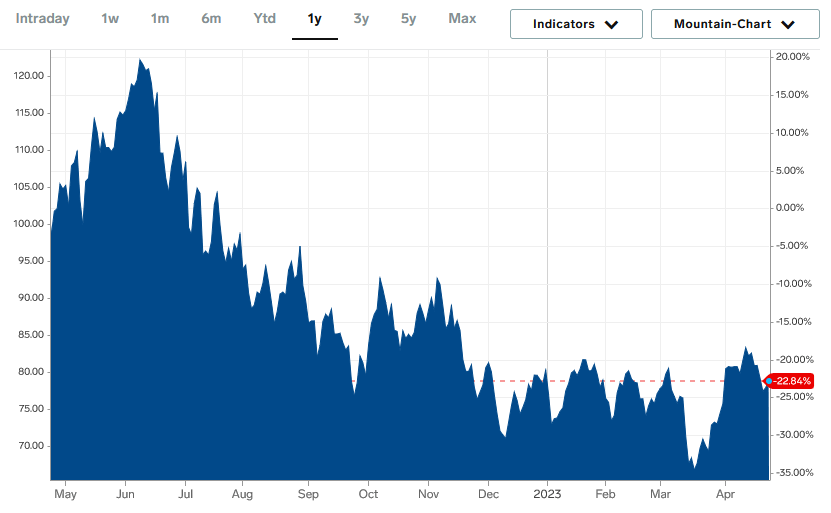

This benefits Plains All American Pipeline even though the company does not actually produce any crude oil itself. This is due to the business model that the company employs. In short, Plains All American Pipeline enters into long-term (typically five to ten years in length) contracts with its customers. Under the terms of these contracts, Plains All American Pipeline provides transportation and storage of the customer’s crude oil and other liquid hydrocarbons using its infrastructure network. In exchange, the customer compensates Plains All American Pipeline based on the volume of resources that are handled, not on their value. This provides the company with a great deal of protection against changes in energy prices, which is nice because crude oil prices have been declining over the past ten months or so:

{kind=link}

As I pointed out in a recent blog post , this trend seems likely to reverse as we enter the summer months due to rising demand for crude oil and global production cuts. However, we do not really have to worry about energy prices too much with Plains All American Pipeline. This is because the company’s contract-based business model results in remarkably stable cash flows over time. Here are the company’s trailing twelve-month operating cash flows for each of the past eleven quarters:

{kind=link}

This is a period of time that included both the lowest price for West Texas Intermediate crude oil of all time (when it went negative in April 2020) as well as the rebound and high prices that followed the outbreak of war in Ukraine. As we can see, none of these events had much impact on Plains All American Pipeline. This is something that we very much like to see as income investors because it provides a great deal of support for the company’s distribution. After all, it is much easier for management to pay out a significant portion of the company’s cash flows if it knows for certain that it will earn a similar amount of cash next year.

As mentioned earlier in this article, Plains All American Pipeline is much more focused on the transportation of crude oil than peers such as ONEOK ( OKE ) or The Williams Companies ( WMB ). It currently expects that approximately 80% of its 2023 adjusted EBITDA will come from the provision of midstream services related to this commodity:

Plains All American Pipeline

This could, unfortunately, be a bit of a handicap for the company. This is because the fundamentals for crude oil going forward are nowhere near as strong as the fundamentals for other energy sources. According to the International Energy Agency, the global demand for crude oil will only grow slightly between now and 2035:

International Energy Agency

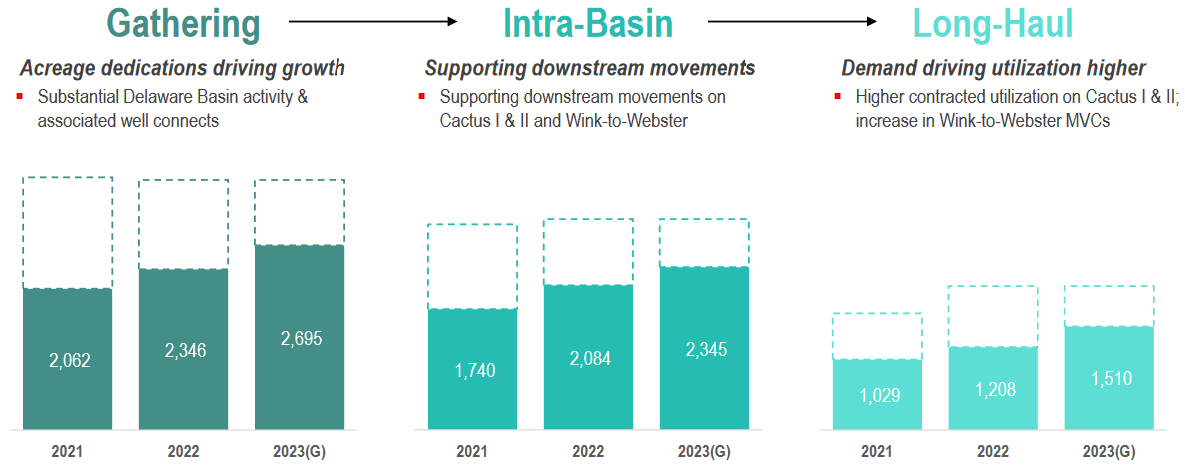

The agency’s most optimistic projections only result in a total daily demand of 107.6 million barrels of crude oil globally by 2050 compared to 96.7 million barrels per day. Thus, demand for crude oil is not likely to increase significantly. This will somewhat limit Plains All American Pipeline’s forward growth, as volumes are not likely to increase much more than demand. However, the United States will likely see some upstream production growth as areas like the Permian Basin will take over from declining production from some of the giant fields that have been supplying the world for decades. The company is certainly not guiding for much growth, though, and, in fact, it does not have many growth projects in the works. The company is only planning to spend $325 million in 2023 on growth projects during 2023, which is much less than it has invested in an average year in the past:

Plains All American Pipeline

Plains All American Pipeline does have the excess capacity to carry considerably more resources than it is currently, however:

{kind=link}

Thus, while it does appear that the company may see some near-term growth, it is not likely to deliver substantial growth over the long term due to the weakness in demand growth for crude oil. It certainly appears that the majority of the partnership’s total investment return will come from its distribution and not from capital gains.

Financial Considerations

It is always important to look at the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a business than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt to repay the existing debt, which can cause a company’s interest expenses to increase during the rollover. This is an especially big concern today as the Federal Reserve has increased interest rates to the highest level that we have seen in ten years, so any company rolling over debt today will almost certainly see expenses go up. In the case of traditional energy companies like Plains All American Pipeline, the market has occasionally experienced periods in which debt issued by these companies is not particularly well received by investors, so they wind up paying higher interest rates than companies in other industries. As such, we want to have a look at Plains All American Pipeline’s finances to ensure that it is not exposing us to an excessive amount of risk due to its debt.

The usual metric that we use to evaluate the debt level of a midstream company is the leverage ratio, which is also known as the net debt-to-adjusted EBITDA ratio. This ratio essentially tells us how many years it would take the company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. As of December 31, 2022, Plains All American Pipeline has a leverage ratio of 3.7x based on its trailing twelve-month adjusted EBITDA. This is a reasonable ratio. As I have pointed out in the past, Wall Street analysts generally consider anything less than 5.0x to be acceptable, but I am more conservative and like to see this ratio under 4.0x in order to add a margin of safety to the position.

As we can clearly see, Plains All American Pipeline satisfies even this more aggressive requirement and as such we probably do not have to worry too much about the company’s debt. This is especially true since Plains All American Pipeline has been working to reduce its leverage over the past few years and is currently projecting that it will get this ratio down below 3.5x by the end of 2023. This would put the company among the most well-financed partnerships in the industry, so it is certainly something that we should keep an eye on.

Distribution Analysis

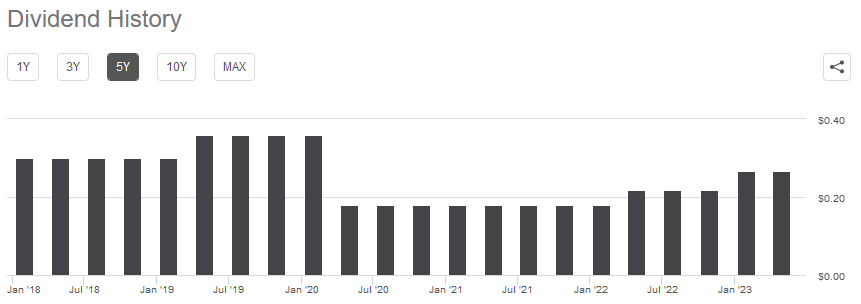

One of the biggest reasons why investors purchase units in master limited partnerships like Plains All American Pipeline is the high distribution yields that these companies tend to pay out. This company is certainly not an exception to this as its 8.06% yield is substantially above pretty much anything else in the market. Unfortunately, the company’s distribution history leaves a lot to be desired as the company reduced its distribution significantly in response to the events of 2020 and has yet to return it to its former level:

{kind=link}

There were numerous midstream companies that cut their distributions back in 2020 despite the fact that their cash flows held up reasonably well. This was mostly because these firms were looking to reduce their debt and their overall dependence on the market. However, the strongest companies in the industry like MPLX LP ( MPLX ) and Enterprise Products Partners never cut their distributions so those investors that are looking for a stable and secure source of income would likely favor one of those companies. However, the market price of the company’s units has adjusted to the current distribution, and it is worth noting that anyone purchasing today will receive the current distribution at the current yield. Thus, the most important thing for anyone buying today is the company’s ability to sustain its current distribution.

The usual way that we evaluate a midstream company’s ability to pay its distribution is by looking at its distributable cash flow. Distributable cash flow is a non-GAAP metric that theoretically tells us the amount of cash that was generated by a company’s ordinary operations and is available for distribution to the company’s limited partners. In the fourth quarter of 2023, Plains All American Pipeline reported a distributable cash flow of $410 million, which works out to $0.58 per common unit. The company’s distribution is $0.2675 per common unit, which gives the company a coverage ratio of 2.17x at the current price. This is a very good ratio that is well above the 1.20x that Wall Street analysts usually consider to be reasonable and sustainable. In fact, the company currently is generating sufficient cash flow to easily raise its distribution quite a bit, which it may do at some point considering its limited forward growth potential. In short, investors should not worry about its ability to cover its distribution and could see some distribution growth even if the company does not grow its cash flows by very much.

Conclusion

In conclusion, Plains All American Pipeline, L.P. does have a lot to offer an income-focused investor. While it does not have the growth potential of some of its peers, it is still generating an enormous amount of cash flow that could easily be used to reward investors in ways other than profit growth. This could result in capital gains despite the lack of cash flow growth as the market frequently prices midstream companies based on their yields, so any distribution increase will likely see the company’s unit price go up. Overall, this one is not as strong a buy as some of its peers, but Plains All American Pipeline, L.P. is still worth considering.

For further details see:

Plains All American: Reasonable, Well-Financed Play In Crude Oil Midstream