CA - Platinum Group Metals: I Remain On The Sidelines

2023-08-03 16:47:29 ET

Summary

- PLG's Waterberg is a promising low-cost mining project, however, depressed PGM prices have hurt the share price badly.

- Trading at its 52-week lows, the stock appears attractive, however, the apparently-low valuation is explained by a downward revision in NPV estimates.

- The absence of a concentrate offtake agreement with a third party, and the impending finalization of CAPEX financing arrangements impact the construction decision on Waterberg.

- In the prevailing circumstances, I see the stock as a hold.

Thesis

Platinum Group Metals Ltd. ( PLG ) is a junior-stage development company in the PGM (read: Platinum Group Metals) industry. The company is invested in two strategic assets namely the WBDP (read: Waterberg Development Project), and the research project operated by Lion Battery Technologies Inc. The latter is jointly funded by PLG and Anglo American Platinum ( AGPPF ), with FIU (read: Florida International University) acting as the key research partner. The objective of this project is to research new lithium battery technology using platinum and palladium. Since this research initiative is in its initial stages, I believe it's too early to analyze the growth prospects associated with this venture. Hence, our analysis will focus on PLG's investment in its flagship mining asset, the WBDP.

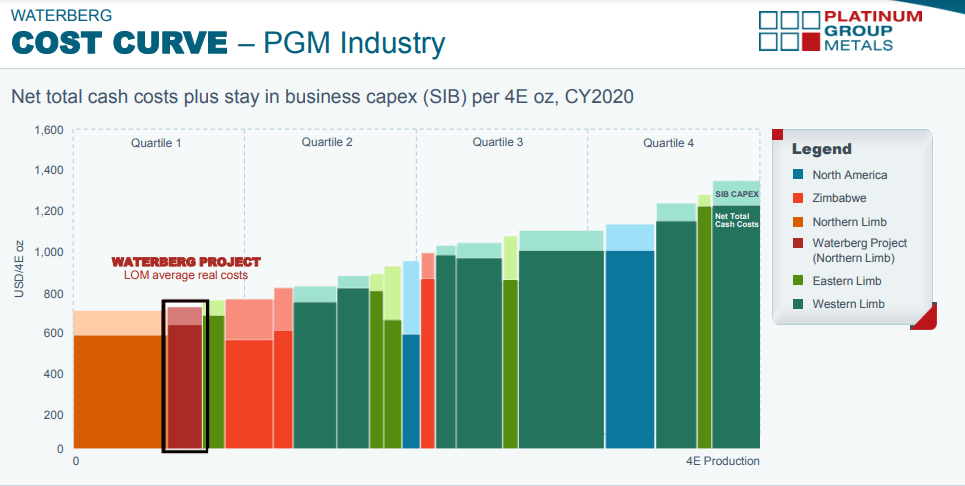

The WBDP is anticipated to be one of the low-cost underground PGM mines (check the figure below) comprising P&P (read: Proven and Probable) reserves of ~19.50 million ounces of 4E PGM (read: platinum, palladium, rhodium, and gold), and is expected to produce ~420,000 ounces of 4E PGM annually at an average cash cost of ~$640/oz. The project is expected to sustain these average production numbers for ~45 full years of production with the capacity to add to the underlying resource and mine life based on the results of ongoing exploration activities.

{kind=link}

PLG's 2019 technical report (NI 43-101) on the WBDP estimated the project's after-tax NPV based on two scenarios (discounted at 8%). First, an after-tax NPV of $333 MM using an average basket price of ~$1,045 per 4E PGM ounce, and second; an after-tax NPV of ~$982 MM using a slightly higher 4E PGM average basket price of ~$1,425 per 4E PGM ounce (based on September 2019 spot prices).

This NPV estimate further improved to ~$1,325 MM based on the average basket prices of ~$1,772 per 4E PGM ounce witnessed in November 2022. Based on PLG's fully diluted ~105.3 million shares and because PLG effectively owns ~50% of the JV interest in the WBDP project, we can assume that the project's NPV/share attributable to the PLG shareholder is approximately $1.58 ($333 MM X 50% / 105.3 MM), $4.66 ($982 MM X 50% / 105.3 MM), and $6.29 ($1,325 MM X 50% / 105.3 MM) respectively for the three scenarios mentioned above. This compares favorably with PLG's current share price of ~$1.30.

Although the above numbers look interesting, I believe three important challenges hamper PLG's growth potential. In this article, we discuss those challenges to highlight why PLG is not a good investment candidate at present, despite carrying an attractive price tag. Let's get into the details .

Palladium Prices Are In A Tight Spot

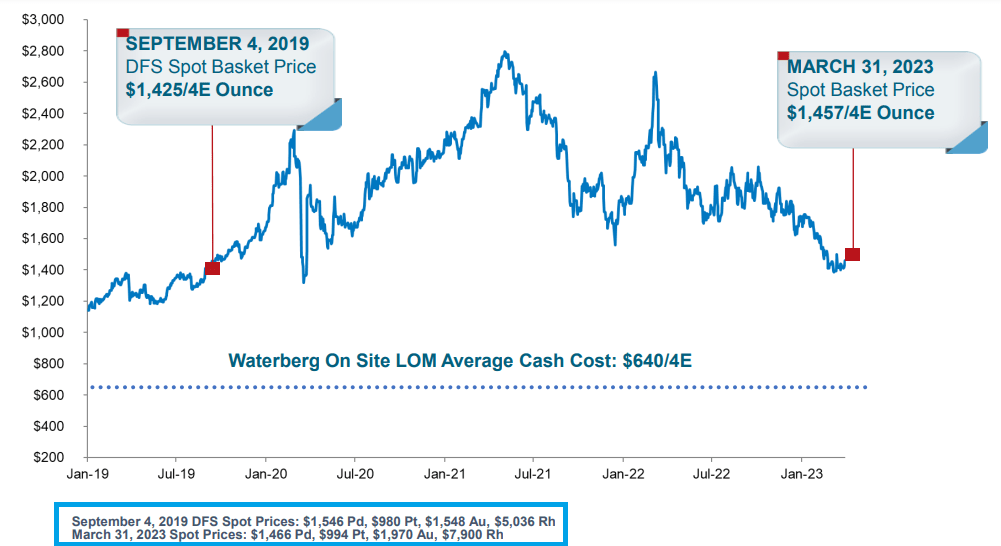

It's estimated that approximately 63% of the reserves and resources of the WBDP comprise palladium which is a precious/industrial metal. PLG's April 2023 presentation shows that the spot basket 4E PGM prices of $1,457/oz (based on March 31, 2023 spot prices) are close to the DFS (read: Definitive Feasibility Study) basket prices of $1,425/oz.

{kind=link}

Now look at the table below which highlights the significance of palladium prices in determining the after-tax NPV of the WBDP project.

| September 2019 Spot -DFS |

| March 2023 Spot |

| August 2023 Spot |

| Palladium ($/oz) |

| $1,546/oz Pd |

| $1,466/oz Pd |

| $1,225/oz Pd |

| Platinum ($/oz) |

| $980/oz Pt |

| $994/oz Pt |

| $922/oz Pt |

| Gold ($/oz) |

| $1,548/oz Au |

| $1,970/oz Au |

| $1,972/oz Au |

| Rhodium ($/oz) |

| $5,036/oz Rh |

| $7,900/oz Rh |

| $4,100/oz Rh |

Metal price changes - from September 2019 to March 2023:

Note that when palladium prices went down by only ~$80/oz (from $1,546/oz to $1,466/oz) it leveled the impact of an increase in other metal prices (platinum up from $980 to $994, gold significantly up from $1,548 to $1,970, and rhodium massively up from $5,036 to $7,900), barely increasing the basket price from $1,425/4E PGM ounce to $1,457/4E PGM ounce.

Metal price changes - from March 2023 to August 2023:

Meanwhile, a comparison between the metal prices witnessed in March 2023 and August 2023 reveals that not only has palladium dropped by another ~$240/oz (from $1,466 to $1,225), there is also a notable decline in the per ounce prices of other metals (platinum down from $994 to $922, gold flat at ~$1,970, while rhodium significantly down from $7,900 to $4,100). In my view, this would lower the bar for 4E PGM basket ounces to the range of ~$1,250-1,300/ounce at spot metal prices.

Impact on estimated after-tax NPV

Recall that PLG's base-case NPV estimate of $333 MM used an average basket price of $1,045/4E PGM ounce. In contrast, a more optimistic case estimates an NPV of $982 MM using an average basket price of $1,425/4E PGM ounce (we'd call it the benchmark case).

As noted above, the estimated basket price of 4E PGM based on prevailing metal prices lies somewhere between the range of ~$1,250-1,300/oz. Hence, we can say that WBDP's after-tax NPV could fall somewhere between the range of $683 MM and $768 MM. This implies that at present, the NPV/ share of PLG attributable to the Waterberg project could be somewhere between $3.25 and $3.65/share.

My calculations are based on the following data:

| Basket Price (or BP) level |

| $1,300/oz |

| $1,250/oz |

| BP decline from benchmark ($1,425/oz) |

| $125 |

| $175 |

| NPV decline from benchmark ($982 MM) |

| $213 MM |

| $299 MM |

| Remaining NPV (estimated) |

| $768 MM |

| $683 MM |

| PLG's proportionate NPV@50% |

| $384 MM |

| $341 MM |

| NPV/share of PLG |

| $3.65 |

| $3.25 |

Section Conclusion: Based on the prevailing share price of ~$1.30, the stock cannot be termed as a value stock especially when the mine development and ramp-up to full-scale production will take approximately 6-8 years and the prevailing adverse trend in PGM prices could take a toll on WBDP's mining dynamics (including NPV estimates). Besides, two other challenges shroud PLG's near-term growth outlook. We will discuss these challenges in detail in the following sections.

Concentrate Offtake Agreement Is Missing

PLG is currently assessing commercial alternatives for concentrate offtake for the WBDP. It's an important part of PLG's beneficiation strategy for the project, and one which is vital in making a construction/development decision regarding the Waterberg project.

Notably, PLG prefers to have a South Africa-based smelter/refiner to process Waterberg concentrate, and this seems like a cost-effective preference. PLG could also explore the possibility of constructing a refinery for processing Waterberg concentrate. However, keeping in view the fact that PLG already needs ~$600M+ in peak funding requirements for WBDP construction, I believe the company could have trouble arranging the additional capital for the construction of a refinery, despite its unlimited authorized share capital.

It's pertinent to note that to date, PLG has been unable to conclude an offtake agreement with any third party. In case there is any offer from a third party, PLG's 15% shareholder Impala Platinum ( IMPUY ) has the right of first refusal to match the terms so offered.

Section Conclusion: In my view, PLG's ability to negotiate an agreement for Waterberg's concentrate offtake will also be impacted by the prevailing uncertainty in PGM prices as lower metal prices generally make a project less attractive for a potential partner. In turn, the delay in securing such an agreement may also impact PLG's ability to have a financing arrangement in place for funding Waterberg's development and construction.

Project Financing - Another Concern

PLG's 2019 technical report estimates the project development CAPEX at ~$1.1 BB, with a peak funding requirement of approximately $617 MM. PLG's balance sheet for the quarter ended May 31, 2023 (Q3 2023) showed cash and equivalents of ~$8.2 MM. The existing cash position is sufficient only to meet the running expenses over the next 12 months because, during the past six months, PLG's cash position declined by ~$4 MM (from $12.3 MM to ~$8.2 MM).

Regarding the peak CAPEX funding requirement of ~$617 MM, it is anticipated that ~$200 MM will be raised through the issuance of equity to Waterberg's existing shareholders (PLG's 50% proportionate share amounts to ~$100 MM), ~$300 MM will be raised through a metal streaming arrangement, while the remaining ~$100-150 MM will be funded through debt.

Section Conclusion: In my view, given the depressed metal price environment, it will be difficult to find a streaming partner unless there is a notable improvement in PGM prices (especially palladium). Likewise, the increase in shareholder equity required to fund PLG's proportionate share of development CAPEX would result in significant value dilution given the prevailing share price of ~$1.30/share.

It's worth noting that the finalization of project financing arrangements would be a positive signal for the market, nonetheless, the aspect of dilution of shareholder's value emanating from the issuance of additional shares to Waterberg's existing shareholders would have consequences for the PLG shares.

Technical Analysis and Investor Takeaway

At the time of writing, PLG last traded at $1.28 which is at the lower end of its 52-week range (between $1.22-1.99). The company's technical price chart reveals that the share price trajectory has witnessed a falling wedge pattern. With support from PGM prices, this trend could potentially reverse to the range of ~$1.50 in the near term (say, 6 to 12 months).

{kind=link}

From a technical analysis perspective, such a low share price could appear to be a good entry point. However, the depressed metal prices, the absence of a concentrate offtake agreement with a third party (or IMPUY for that purpose) for Waterberg's future production, and the fact that arrangements for CAPEX financing are not finalized so far indicate otherwise. I believe one should be wary about investing in the company at this time, at least until there is a sustainable increase in PGM prices. That said, the stock is a 'hold' in my view.

For further details see:

Platinum Group Metals: I Remain On The Sidelines