PLTK - Playtika: Cheap And Making Efforts Despite EPS Miss

2023-12-07 11:16:31 ET

Summary

- The guidance given for the future is beneficial, and the company is making significant changes in the organization including not only restructuring efforts, but also closure of certain studios.

- Despite this, there is room for optimism due to the company's guidance for 2023, which includes restructuring efforts and the exploration of strategic alternatives.

- With the company's know-how in data analysis and the profile of its founder, further development of successful games is expected, making Playtika undervalued.

Playtika Holding Corp. ( PLTK ) recently delivered lower than expected quarterly EPS and revenue growth, and many analysts lowered their expectations for the coming quarter. With that, I do believe that there is room for optimism given the guidance for 2023. The company is making a lot of efforts including restructuring and closure of studios. In addition, it appears to be looking for strategic alternatives. In my view, considering the know-how accumulated with regards to data analysis and the profile of the founder, we could expect further development of successful games. Even taking into account risks from interest rate increases or dependence on large gaming platforms, I think that PLTK is undervalued.

Playtika’s Earnings Reports, Net Sales Growth, And Guidance

With principal offices located at Hertsliya, Israel, Playtika Holding develops mobile games, and distributes them through various web and mobile platforms, such as Apple ( AAPL ), Facebook ( META ), and Google ( GOOG ). I believe that the most appealing thing about the business model is its capacity to bring new users. Playtika offers free-to-play games in order to connect with new players, and sells virtual items to enhance the game experience. It is relevant to note that payments for virtual items are not refundable. Given the recent history of FCF generation, I believe that monetization appears to be working.

Payments from players for virtual items are non-refundable and relate to non-cancellable contracts that specify our obligations and cannot be redeemed for cash nor exchanged for anything other than virtual items within our games. Source: 10-Q

Source: YCharts

With that about the previous net sales generation and business model potential, in my view, the most recent earnings were not that exciting. In the three months ended September 30, 2023, the company reported net income of about $37 million, which was lower than expectations. EPS GAAP was also lower than expectations at close to $0.10 per share.

Source: SA

Earnings lower than expectations and recent decreases in the earnings expectations seem to be pushing the stock price down. In the last 90 days, nine different analysts lowered their expectations for the next quarter. Right now, they are expecting EPS GAAP close to $0.17 per share.

Source: SA

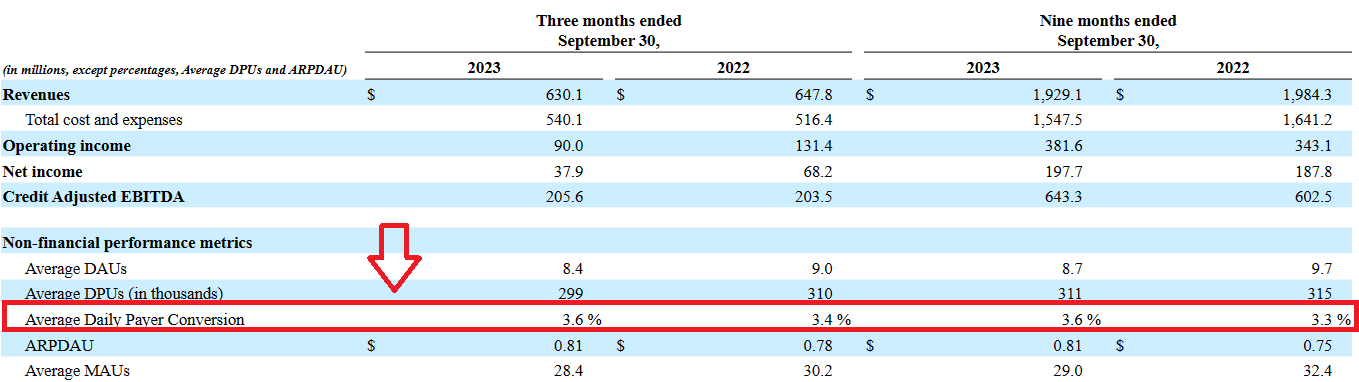

With that about the bottom line and the expectations, I believe that there is room for optimism given the increases in quarterly payer conversion, which increased as compared to the same quarter in September 30, 2022. Further increases in the payer conversion could lead to better FCF margin improvements in the coming years.

{kind=link}

Source: 10-Q

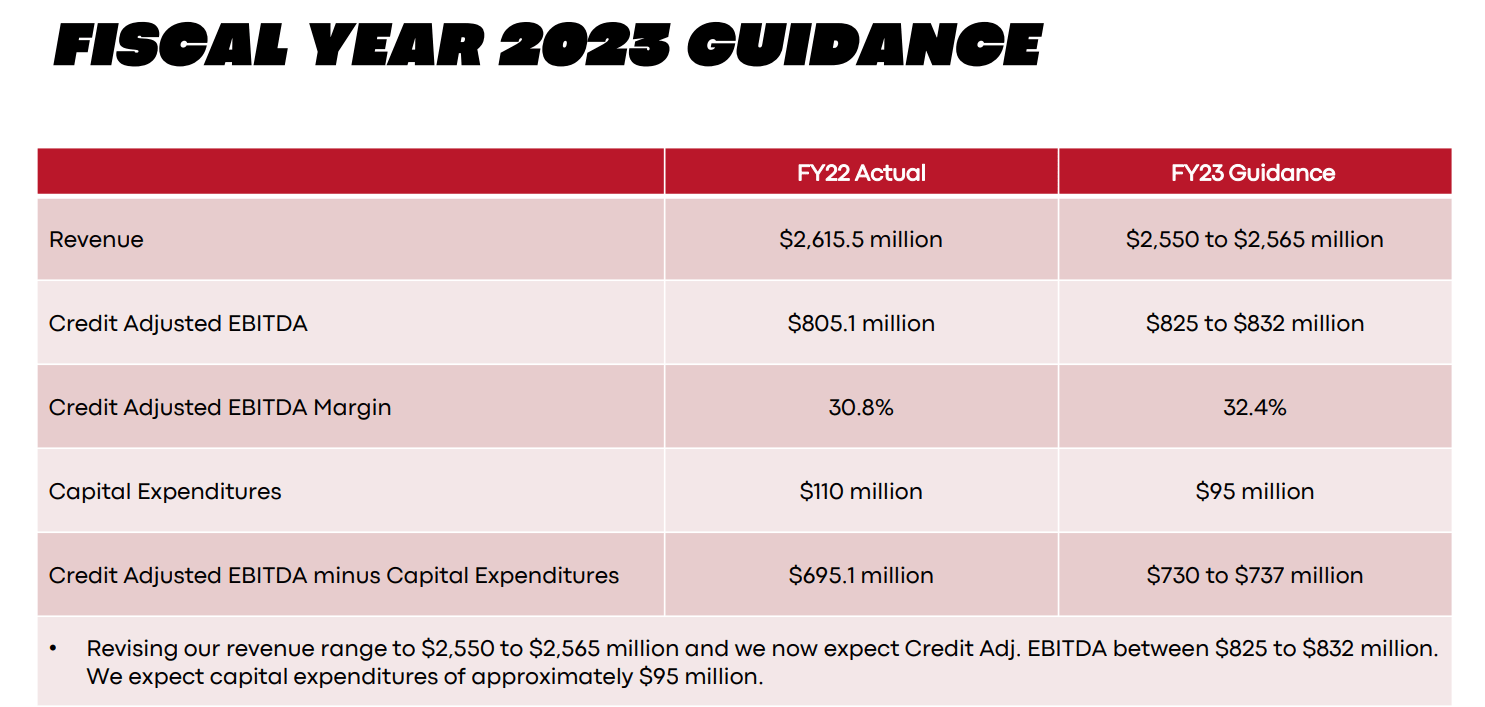

I also think that management did deliver a beneficial 2023 guidance that investors may have forgotten. Playtika Holding expected the credit Adjusted EBITDA margin to increase from about 30% in 2022 to close to 32.4% in 2023. The credit adjusted EBITDA margin minus capex is also expected to grow from about $695 million to close to $730-$737 million. Considering these beneficial expectations, I believed that a quick look at the valuation would be beneficial.

{kind=link}

Source: Earnings Presentation

Balance Sheet

I dislike the fact that Playtika’s balance sheet does not show an asset/liability ratio larger than 1x. With that being said, the company reports a significant amount of cash in hand, which could be used for acquisition of new games.

As of September 30, 2023, Playtika Holding reported cash and cash equivalents worth $878 million, restricted cash of about $1 million, and accounts receivable close to $168 million. Total assets were equal to $2.977 billion, a bit more than the figure reported on December 31, 2022.

Goodwill increased to close to $1.005 billion. With this in mind, I think that management is overall optimistic about the future of the industry. Managers usually do not buy new targets when they believe that their business model may not perform well in the future.

Source: 10-Q

Playtika Holding does report a considerable amount of debt, so I understand the concern of some investors. The debt to equity ratio increased from around 0.2x in 2021 to close to 0.6x in 2023. I believe that lower leverage would most likely have a positive effect on the current EV/FCF valuation. However, it appears clear, given previous financial figures, that Playtika does not seem concerned about the total amount of debt. In sum, I believe that this is a company for investors who may not worry about debt levels.

Source: YCharts

In the last quarterly report, current maturities of long-term debt stood at close to $16 million, with total current liabilities of about $400 million, long-term debt of about $2.402 billion, and contingent consideration worth $77 million. Total liabilities stood at $3.259 billion, a bit lower than that in 2022.

Source: 10-Q

Debt, And Cost Of Capital Assumptions

Playtika Holding reported a term loan with maturity of around 2028, an interest rate close to 8%, and 2026 senior notes including an interest rate close to 4.2%. Under my own calculations, the weighted average cost of debt does not seem far from 7.2%. With these figures, I assumed that a WACC ranging from 4.2% to 7% would make sense.

{kind=link}

Source: 10-Q

Source: CW Capital

For the assessment of the exit multiple, I checked the valuation in the sector, which appears significantly more expensive than that of PLTK. The sector median EV/EBITDA is close to 8.4x, and the P/Cash Flow stands at about 9.5x. Given these figures, I assumed an exit multiple of close to 6.7x-10.7x FCF. Competitors like Kabam ( KABAM ), Activision Blizzard ( ATVI ), DoubleDown Interactive ( DDI ), and Machine Zone ( MZ ) do not trade far from these trading multiples.

Source: SA

Source: SA

With Know-How Accumulated For Many Years And Team Of Coders, Artists, And Data-scientists, I Would Expect New Engaging Games

Given previous successful games developed like Slotomania, I believe that the team of developers, coders, and data-scientists will most likely come out with new successful games. The profile of the CEO and Chairman is worth noting, who did not only found the company, but appears to be responsible for a significant part of Playtika’s successful business story.

Robert Antokol, the CEO, was responsible for the sale of Playtika to Caesar’s Interactive Entertainment. Besides, he also negotiated the deal with Giant. Mr. Antokol graduated in Engineering from Ort Braude College. With this business executive in the Board of Directors, I believe that investors will most likely be interested in Playtika.

We are led by our visionary co-founder, Robert Antokol, who has managed Playtika since inception, transforming the company from a small games business, through numerous acquisitions and steady organic growth, to become one of the largest mobile games platforms in the world. Source: 10-k

Further Successful Optimization In The Acquisition Of Users Will Most Likely Bring Increases In The Payer Conversion And FCF Margin Growth

I believe that management accumulated a significant amount of know-how with regards to data assessment and marketing capabilities to acquire users. In my view, the payback period methodology used will most likely bring further reduction in user acquisition costs. As a result, I believe that we could expect FCF margin growth.

We leverage our centralized marketing team to achieve efficiencies across our portfolio of games. Our performance marketing capabilities focus on cost-effectively acquiring users. Our user acquisition strategy is centered on a payback period methodology and we optimize spend between the acquisition of new users and the reactivation of inactive players. Source: 10-k

Given The Total Amount Of Cash In Hand And Previous Acquisitions, I Would Expect Further Inorganic Growth

I believe that management knows well how to acquire, negotiate, and integrate new companies. Playtika Holding reports a significant number of acquisitions and growing goodwill larger than $799 million.

Over the past 10 years, we have successfully acquired a number of mobile games and studios, including JustPlay (2022), Reworks (2021), Seriously (2019), Supertreat (2019), Wooga (2018), Jelly Button (2017), House of Fun (2014), World Series of Poker (2013) and Bingo Blitz (2012). Source: 10-k

Besides, the CFO reports substantial expertise in M&A. With this in mind and current cash in hand, I would be expecting further inorganic growth in the coming years.

Craig Abrahams is Playtika’s President and Chief Financial Officer, Mr. Abrahams has overseen several of the company’s acquisitions, including Buffalo Studios, EA Mobile Montreal (makers of World Series of Poker) and Pacific Interactive (makers of House of Fun). Previously, Mr. Abrahams served as Chief Financial Officer of Caesars Acquisition Company from 2013 to 2017. Source: Craig Abrahams

I Assumed That Headcount Reductions May Not Affect Future Productivity And Development Of New Games

In the last quarter, Playtika noted that employee compensation costs declined as a result of headcount reductions. Even if reductions may lead to higher FCF margin growth, under my DCF model, I assumed that Playtika Holding will maintain the best artists and coders so that new games will continue to be successful.

Recent headcount reductions have reduced employee compensation costs, including decreased stock-based compensation expense, for both the three and nine months ended September 30, 2023. Source: 10-Q

The Company May Be Evaluating Strategic Alternatives

In the last quarter, Playtika noted strategic alternatives, certain restructuring activities, and the closure of certain Montreal, Los Angeles, Helsinki, and London studios. Given this news, I believe that we could see lower revenue growth. With that, I believe that we may also see increases in the FCF margin as Playtika may be choosing to continue activities that are more profitable.

The Company announced the closure of its Montreal, Los Angeles, Helsinki and London studios, along with limited other cost reduction activities. Source: 10-k

The company also announced the evaluation of strategic alternatives. I did not see the sale of divisions or sale of games in the past, but I know that certain investors could expect these actions. As a result, the sale of games could bring cash in hand that may enhance the balance sheet.

Also included in general and administrative expenses in 2022 are expenses incurred in connection with the Company’s evaluation of strategic alternatives. Source: 10-Q

Amounts for the three and nine months ended September 30, 2022 also include $2.7 million and $6.1 million, respectively, incurred related to the restructuring activities. Source: 10-Q

My Valuation Figures Based On Previous Assumptions And Cash Flow Statements

My expectations, which are in line with those of other analysts, include net sales growth close to 2% and 11%, growing operating margin, and growing FCF/Net sales. 2029 Net sales are expected to be close to $3.478 billion, with 2029 EBITDA of $1.117 billion, 2029 EBIT of $735 million, and 2029 net income close to $489 million. Finally, I also expect exit free cash flow close to $701 million, which is not far from the figures delivered from 2020 to 2022.

Source: CW

My DCF model includes a WACC between 4.2% and 7.7% and exit multiples close to 6.7x-10.7x. FCF would range between $420 million and $701 million. The results included a valuation without net debt between $4.6 billion and $7.9 billion.

Source: CW

If we divide by the share count, the forecast price would range between $12 and $20 per share with a median close to $13 and $17 per share. The internal rate of return would not be far from 4%-18% with a median around 11%.

Source: CW

Source: CW

Risks

The company may suffer from significant changes in the interest rates because the Revolving Credit Facility signed by Playtika represents floating rate facilities. Higher interest rates may lower FCF margins, and may also have a detrimental impact on the fair valuation of Playtika Holding.

Our exposures to market risk for changes in interest rates relate primarily to our Term Loan and our Revolving Credit Facility. The Term Loan and our Revolving Credit Facility are floating rate facilities. Therefore, fluctuations in interest rates will impact the amount of interest expense we incur and have to pay. Source: 10-k

I also think that acquisitions, restructuring efforts, and closure of some offices may have a detrimental impact on future net sales growth. If key individuals decide to leave the company, I believe that future games may not be as successful as in the past. Besides, the company may lose employees, who may be good at buying new games from other companies.

Playtika receives a significant amount of dollars from players using large platforms. More than 70% of the total amount of sales seems to be generated from iOS App Store, Facebook, and Google Play Store. This appears to be risky. If these companies make changes in their platforms, reduce the fees given to Playtika, or lower the visibility of the games, Playtika’s net sales could lower.

A significant number of the virtual items that we sell to paying players are purchased using the payment processing systems of these platforms and, for the year ended December 31, 2022, 71.5% of our revenues were generated through the iOS App Store, Facebook, and Google Play Store. Source: 10-k

Conclusion

Playtika Holding recently delivered lower than expected earnings including net sales growth declines, which the market did not really appreciate. With that being said, the guidance given for the future is beneficial, and the company is making significant changes in the organization including not only restructuring efforts, but also closure of certain studios. The company is also looking for strategic alternatives. I have beneficial long term expectations because of previous successful acquisitions, the profile of the founder, and the team of artists, coders, and data experts working inside the organization. Yes, there are risks from changes in the interest rates or changes in the large gaming platforms, however I believe that Playtika Holding appears quite cheap.

For further details see:

Playtika: Cheap And Making Efforts Despite EPS Miss