PLTK - Playtika Holding: No Growth Expected

2023-12-05 03:01:39 ET

Summary

- Playtika's revenue growth has slowed down considerably since going public in 2021, with revenues decreasing in the past four quarters due to a lack of acquisitions.

- The company has recently acquired Youda Games and Innplay Labs, providing slight temporary growth for coming quarters.

- The valuation already expects a poor organic growth, making the risk-to-reward mostly balanced in my opinion.

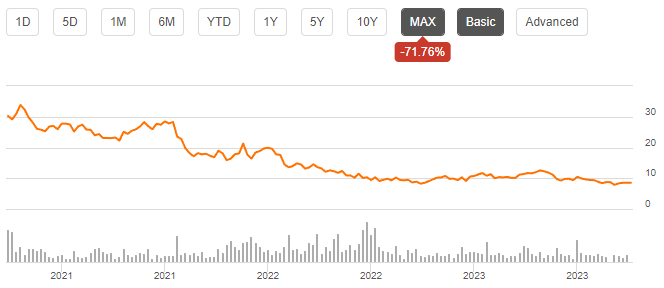

Playtika Holding ( PLTK ) develops and acquires mobile games. The company has a portfolio of casual and casino-style casual games with casual names such as Bingo Blitz, June’s Journey, Solitaire Grand Harvest, and Best Fiends. On the casino side, Playtika owns many known poker-related casual names and other brands, with names such as Governor of Poker, Caesars Slots, Slotomania and the WSOP mobile game. Since Playtika went public in 2021, the company’s stock has deteriorated in value as revenue growth has slowed down into a halt.

{kind=link}

Financials – A Worrying Organic Performance

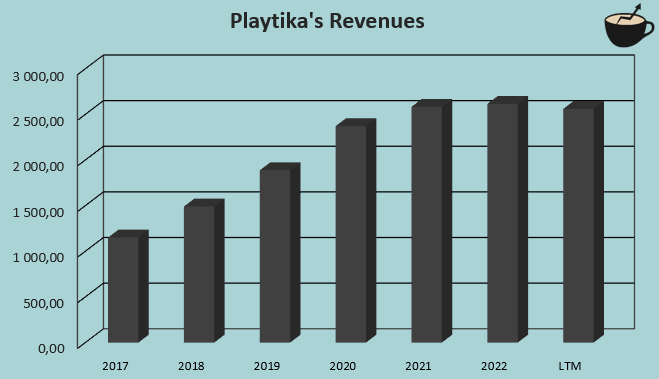

From a quick glance, it seems like Playtika has been able to grow revenues well – from 2017 to 2021, revenues grew at a CAGR of 22.4%. Since the year, Playtika’s growth has slowed down considerably – in 2022, revenues only grew by 1.3%, and the latest four quarters have seen decreasing revenues. After the company had an IPO, Playtika hasn’t been performing up to previous standards in growth.

{kind=link}

The growth has slowed down into a halt as Playtika’s acquisitions have slowed down – the historical growth has been achieved through previous large acquisitions. For example, the company had $1039 million in cash acquisitions from 2017 to 2021 as the company acquired Jelly Button, Wooga, Solitaire Grand Harvest, Seriously, and Reworks in the years. Compared to the current market capitalization of $3.2 billion, the acquisitions are significant in size.

Revenues in recent quarters have started to drop slightly; Playtika has troubles in keeping up active users in the owned companies. Daily active users have decreased by 6.7% year-over-year in Q3. I believe that DAU is a very critical KPI for mobile gaming companies, making the trajectory very worrying.

DAU Trajectory in Recent Quarters (Playtika Q3 Investor Presentation)

According to Playtika’s Q3 presentation , the company’s casino-related games have had a worse performance than other casual games. Year-over-year, casino-related games’ revenue share has fallen by 1.8 percentage points into 43.3% - it would seem that poor casino-related game performance is the main driver of the bad revenue performance.

Playtika has had some smaller acquisitions including JustPlay in 2022 and Youda Games in Q3 of 2023, and the recent acquisition of Innplay Labs , completed in September for an initial consideration of $80 million with a maximum consideration of $300 depending on Innplay’s performance. The recent acquisitions should boost Playtika’s growth temporarily, but I don’t see the acquisitions as groundbreaking for Playtika’s long-term revenue trajectory.

Despite the poor growth performance, Playtika has been able to keep up a good margin level. Currently, Playtika’s trailing EBIT margin stands at 21.2%, somewhat below the 2017-2022 average of 24.1%. The company has been able to cut costs significantly – R&D in 2023 so far is $48 million below the 2022 level from the similar period, and SG&A is down by $74 million. It is yet to be seen, if the cost cuts will have a further negative impact into medium-term and long-term growth, though; I wouldn’t keep my hopes up for revenue growth.

Valuation – The Market is Aware of Low Growth

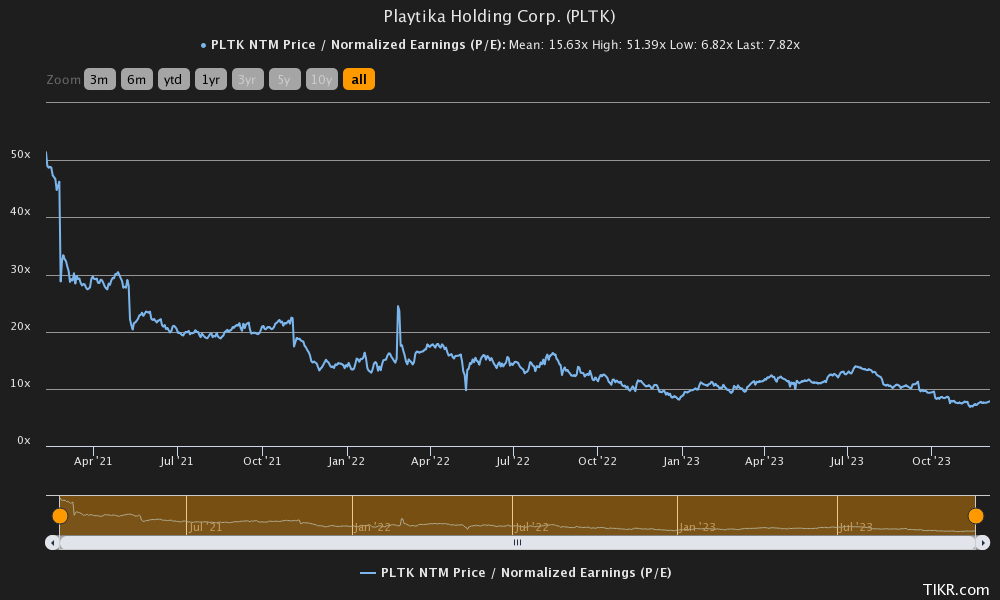

As the acquisition-driven nature of Playtika’s growth has become more apparent with the recent performance, Playtika’s forward P/E has been on a downfall – the figure has come down from a high of 51.4 at the time of the IPO into a current figure of 7.8:

{kind=link}

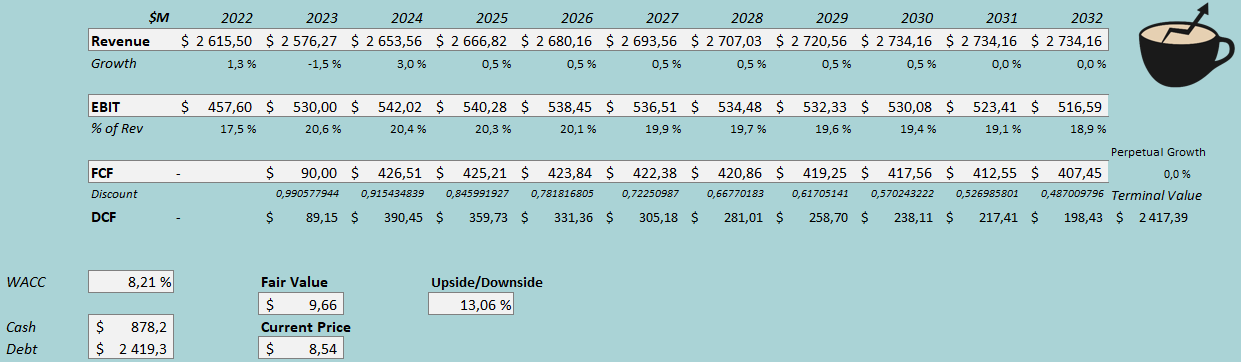

The single-figure P/E seems justified due to the poor organic performance of Playtika. To further demonstrate the valuation and to estimate a rough fair value for the stock, I constructed a discounted cash flow model in my usual manner. In the model, I estimate Playtika to hit its 2023 revenue guidance with total revenue decreases of 1.5%. I estimate a growth of 5% in 2024, as the acquisitions of Youda Games and Innplay Labs start to contribute to revenues. I still estimate a poor organic revenue performance – after 2024, I estimate a growth of 0.5% for a few years that slows down to 0% eventually.

As I estimate the organic revenue performance to be negative in real terms, I don’t believe that Playtika is likely to keep up the current margin level completely – I estimate Playtika’s EBIT margin to fall by 1.7 percentage points from a 2023 estimate of 20.6% to a 2032 estimate of 18.9%. As the margin falls, the total EBIT figure of Playtika deteriorates very slowly. Due to the amortization of past acquisitions being in the EBIT figure, Playtika’s cash flow conversion is mostly quite good.

With the discussed estimates along with a cost of capital of 8.21%, the DCF model estimates Playtika’s fair value at $9.66, around 13% above the stock price at the time of writing. I don’t believe that this amount of upside necessarily makes the risk-to-reward worthy of a buy rating. The company would in my opinion need to prove a better growth to fuel a better rating. Still, the current valuation does prove that the stock market is well aware of Playtika’s likely low future growth.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q3, Playtika had $39.5 million in interest expenses. With the company’s current amount of interest-bearing debt, Playtika’s annualized interest rate comes up to 6.53%. Playtika leverages quite a large amount of interest-bearing debt in the company’s financing – I estimate that Playtika’s long-term debt-to-equity ratio will be 40%.

For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 4.25% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Playtika’s beta at a figure of 0.86 . Finally, I add a small liquidity premium of 0.2%, crafting a cost of equity of 9.53% and a WACC of 8.21%.

Takeaway

Playtika’s low organic growth should worry investors, and has done so as the stock price’s trajectory suggests. The company’s daily active users have fallen quite constantly as Playtika has been without acquisitions in the recent past boosting the KPI. Recent acquisitions of Youda Games and Innplay Labs should provide a temporary boost in coming quarters, but I wouldn’t keep my hopes up for the long run. Still, the deteriorated stock price doesn’t reflect a very poor risk-to-reward in my opinion, as the DCF model estimates slight upside if nominal revenues are mostly stable in the future. For the time being, I have a hold rating for the stock.

For further details see:

Playtika Holding: No Growth Expected