PLTK - Playtika Stock: Play The Free Cash Flow Game Rating Upgrade

2023-07-02 23:13:05 ET

Summary

- I upgrade Playtika, a leading mobile game publisher in the US, to a buy due to its improved technical setup, solid valuation, and impressive free cash flow.

- The company's earnings are expected to rise steadily this year and next, with acceleration expected in 2025.

- Despite competition in the Social Casino space, Playtika's strong operating cash flow and resilient consumer spending trends make it less susceptible to higher interest rates.

- The company's earnings multiples and EV/EBITDA ratio are also attractive, trading at a discount to their long-term price-to-cash flow multiple.

- Though stock has not yet broken out, there are growing signs that it may due to its high free cash flow.

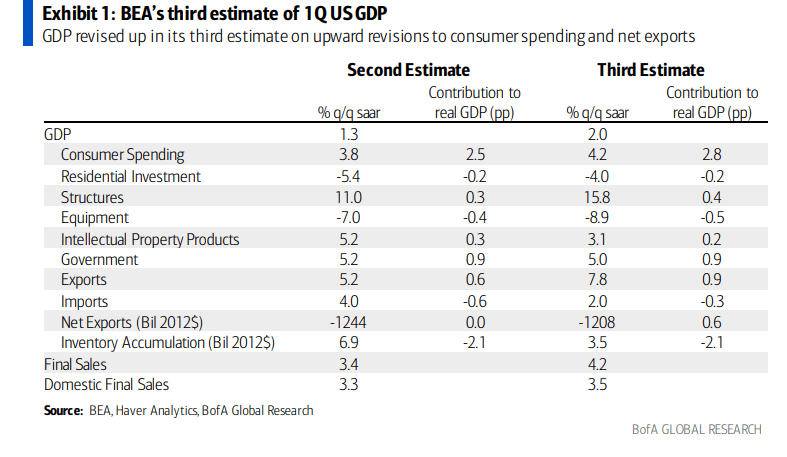

The US consumer is doing what they do best. Upward revisions to first-quarter GDP were based largely on an uptick in consumer spending. At a 4.2% seasonally adjusted annual rate, the threat of a technical or NBER recession remains muted compared to what was expected late last year.

One retail-related company features an improved technical setup, solid valuation, and downright impressive free cash flow. I am upgrading Playtika (PLTK) stock to a buy.

GDP revised up in its third estimate on upward revisions. Consumer spending and net exports stronger.

{kind=link}

According to Bank of America Global Research, PLTK is a leading mobile game publisher in the US and has established itself as a dominant player in the Social Casino segment. The company has several games ranking in the Top-100 charts, including many highly ranked games in their respective categories. Playtika generates revenue primarily from sales of virtual items, with the remaining 3% of its revenue from in-game advertising. The company is headquartered in Israel with offices around the world.

The Israel-based $4.2 billion market cap Interactive Home Entertainment industry company within the Consumer Discretionary Sector trades at a low 16.1 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal. The stock has a somewhat high 47% implied volatility reading.

Back in May, Playtika reported a solid earnings beat while it also exceeded top-line expectations. Videogame sales fell in April despite console gains , but PLTK continues to produce strong operating cash flow net of capital expenditures. A key risk, however, is that the Social Casino space is getting crowded, and competition is growing among Playtika’s well-capitalized rivals.

What has benefitted this small player is that recession risks have ebbed, and a resilient consumer spending trend has been a boon. In its upcoming Q2 report, the bulls obviously want to see another EPS beat, but a full-year guidance increase would be particularly positive; the company left FY 2023 profit forecasts unchanged in May, perhaps disappointing investors along with the year-on-year revenue drop. Just recently, analysts at Wells Fargo came out cautious on PLTK, highlighting its aggressive acquisition history that could be challenged amid a higher cost of capital environment and its lackluster top-line growth. I assert, however, that its ample free cash flow makes PLTK less susceptible to higher interest rates today.

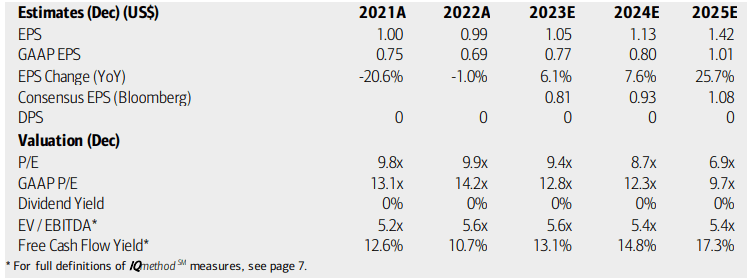

On valuation , analysts at BofA see earnings rising at a steady pace this year and next before per-share profits are expected to accelerate in 2025. The Bloomberg consensus outlook is not as sanguine compared with BofA’s outlook. While the small-cap company does not pay dividends, notice how strong its free cash flow yield is.

Selling for a mere 7 times FCF, PLTK’s earnings multiples are likewise attractive. Moreover, the company’s EV/EBITDA ratio is less than half that of the broad market. I continue to like the earnings trajectory, profitability , and overall valuation of Playtika. Just recently, its momentum factor has ticked up (I will detail that in the Technical Take later).

Playtika: Earnings, Valuation, Free Cash Flow Forecasts

{kind=link}

While I mentioned how I liked the firm’s valuation in a report last year, let’s dig deeper to find out what an appropriate fair value might be.

The mobile gaming company has a low price-to-sales ratio of just 1.63 on a forward basis – its historical TTM P/S is 2.8. Also, shares trade at a 30% discount to their long-term price-to-cash flow multiple. Surely higher interest rates today should mean a lower valuation, but this high free-cash-flow name should not get slapped with a major valuation re-rating lower since its profits are not confined to later years.

So, if we apply a sector P/E of 17 (warranted given the significant growth potential), then the stock should trade near $14.50 if we assume a conservative $0.85 of next-12-month EPS.

PLTK: Compelling Valuation Reading Given EPS Growth Expectations

Seeking Alpha

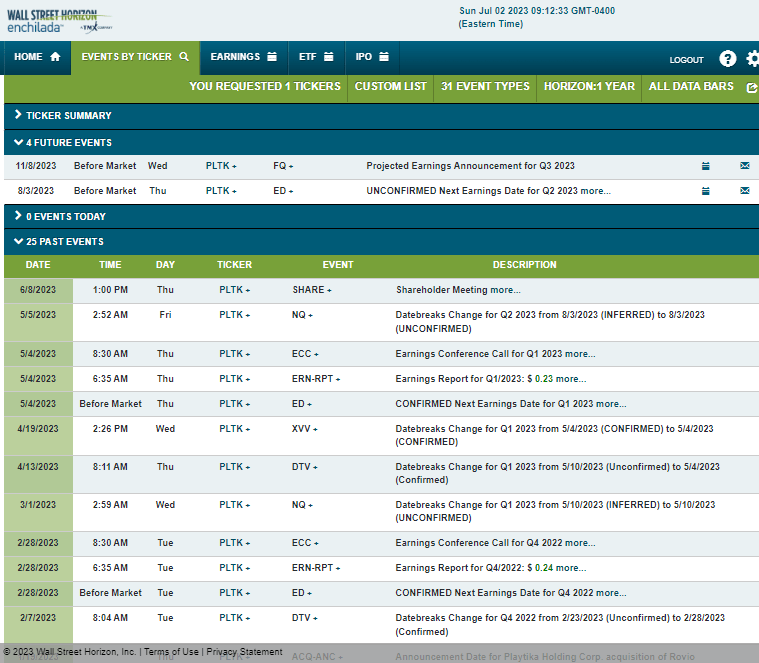

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q2 2023 earnings date of Thursday, August 3 BMO. The calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

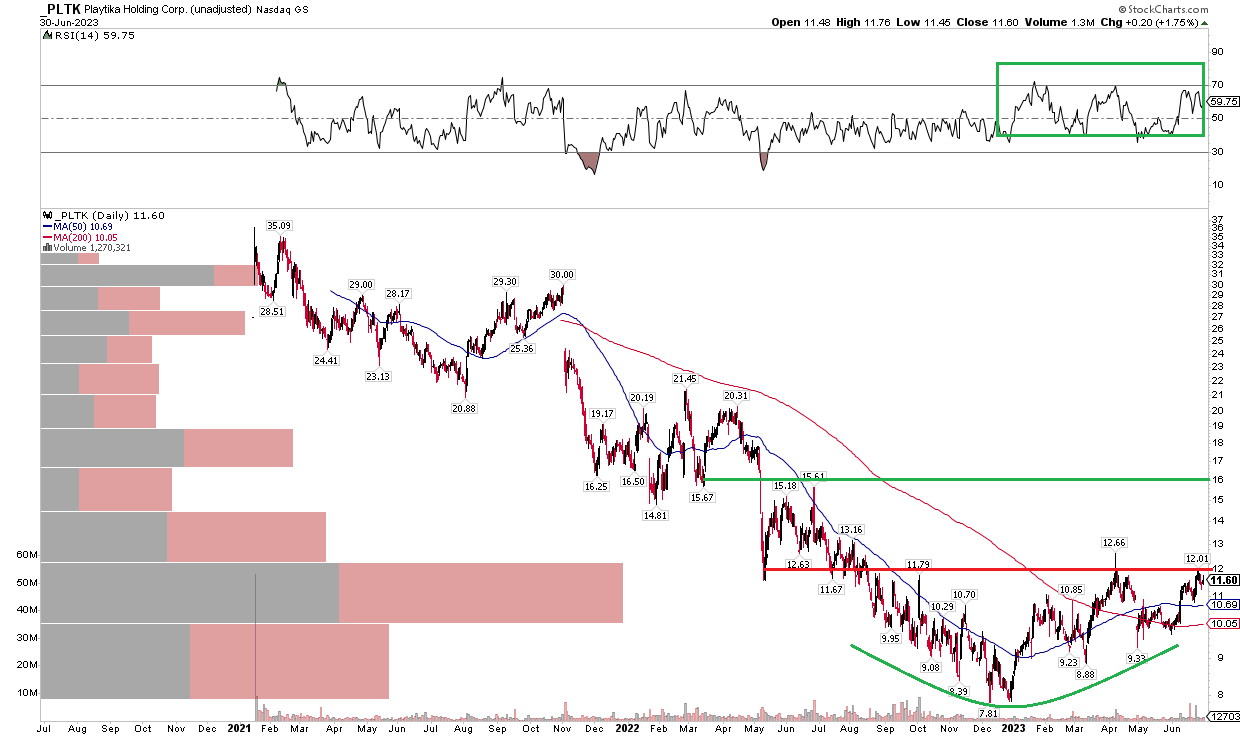

I was admittedly cautious on Playtika late last year . The chart was mired in a steep downtrend that showed few signs of reversing higher. Today, though, the situation has improved. Unfortunately, waiting to buy it has been costly. The stock is up more than 40% in 2023. Investors should always pose this tough question to themselves: Is the stock a buy today ? We must relook at each company with fresh eyes in an impartial manner.

In this instance, while it is lousy to think about missing out on gains of the past, I see bullish signs. Notice in the chart below that PLTK is working on a bearish to bullish reversal pattern. A close above $12 would portend a measured move upside price objective to near $16 – about the peak from June last year. This rounded bottom formation also comes with a flattening long-term 200-day moving average, indicative of an emerging trend inflection.

What's more, the RSI momentum reading at the top of the chart has ventured into bullish territory, ranging from near 40 to above 70. That is a positive contrast to the pessimistic range I highlighted last year. Lastly, there is a significant amount of volume by price in the current trading zone, so a rally through $12 would be accompanied by a significant cushion on subsequent pullbacks.

Overall, the technical situation is better. Sure, it would have been great to nail the bottom last December, but that’s life as an active investor.

PLTK: Bearish to Bullish Rounded Bottom Reversal Pattern, Eyeing $12 Resistance

{kind=link}

The Bottom Line

I continue to like PLTK’s valuation and better technical signals warrant a buy rating. While the stock has not busted out yet, there are growing signs that may happen to this company with high free cash flow.

For further details see:

Playtika Stock: Play The Free Cash Flow Game, Rating Upgrade