CA - Polaris Renewable Energy: Get Paid To Wait With A 6% Dividend Yield

2024-01-14 23:21:39 ET

Summary

- Polaris Renewable Energy owns renewable energy projects in Latin America.

- With significant capex now behind them, the company has several projects due to come onto the market in the next few years that should meaningfully increase EBITDA.

- With more growth plans ahead to get to its $100 million EBITDA target by 2028 ($60 million today), shares are not priced for any growth at 6.1x EBITDA.

- The stock looks undervalued as the company trades at half the valuation of its peers.

- Investors today are getting a 6% dividend covered by cash flows while they wait for EBITDA to grow and the multiple to expand over time.

Please note all $ figures in (the reporting currency), not , unless otherwise stated.

Introduction

Polaris Renewable Energy Inc. (RAMPF) ( PIF:CA ) owns renewable energy projects in Latin America. These projects include a geothermal plant, four hydroelectric power plants, and three photovoltaic solar projects.

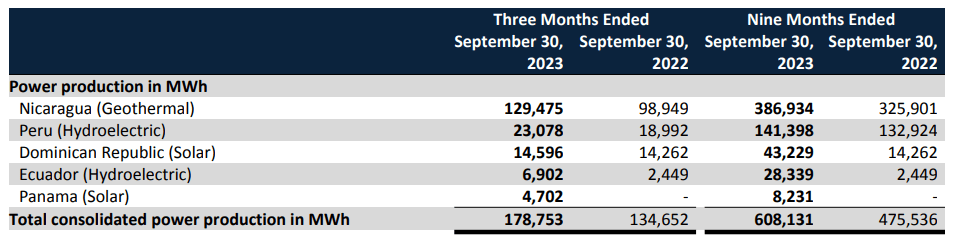

In the company's recent MD&A , Polaris Renewable experienced 30% growth in total power production year over year for the quarter, with year-to-date power production up 28%. Much of this was driven by growth in the company's largest operation, a geothermal plant that generates the majority of its revenues.

{kind=link}

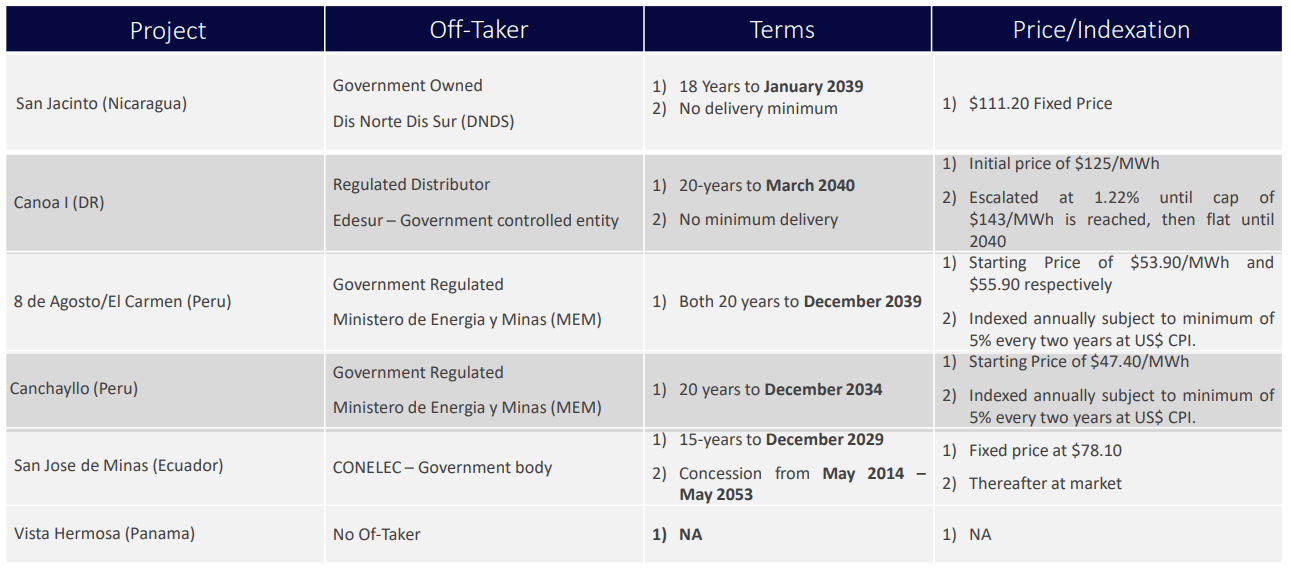

Located in northwestern Nicaragua, the San Jacinto Tizate Geothermal plant is responsible for 72% of the company's total power production. This plant has the capacity to generate 72MW of electricity with another 10MW capacity that was just added through its binary plant completed in December 2022. Like 98% of the power Polaris generates, it has contracts with the government to supply power. The Nicaragua deal is with the Nicaraguan Ministry of Energy and Mines whereby Polaris is allowed to sell at a price of $111.20 per megawatt-hour as per their agreement.

In my view, part of the attractiveness of investing in Polaris Renewable is the long-term contracts it has with governments. As shown from the chart below, Polaris has several long-term contracts (around 15-20 years) with both fixed-priced terms as well as inflation escalators indexed to US CPI. I believe this gives the company long-term visibility in the revenue it can generate from its existing power generation activities, providing a stable and predictable income stream. These cash flows help to fund part of its 6.0% dividend as well as fund future renewable energy projects and acquisitions.

{kind=link}

Additional Projects on the Horizon

When looking at the company's recent financials , we can see that with the revenue growth, Polaris has also been improving its profitability. After a tough few years, particularly in 2020 having to accept a 16% reduction from the $130.72 that the company was initially getting from its Nicaragua operation, the company has been on the road to recovery in its profitability.

{kind=link}

In addition to this increase in profitability, we have also seen Polaris expand beyond Nicaragua in recent years to other countries in Latin America. For 2023, we started to see revenues generated from the company's solar project in Panama. After acquiring it in March 2022, the company took about a year to complete the project, beefing up the capacity and connecting it to the grid and national transmission network. While it doesn't have contracts with the government just yet, it is able to sell at spot rates ($132.51 per MWh) and may decide to enter into a long-term contract with the government if it looks favorable for the company. I think a long-term contract is likely, given that this project (only 2% of revenues) is the only part of Polaris' operations that isn't in contract. In my view, given that a lot of the capex is behind them on this front, I think we'll start to see strong free cash flow generation here.

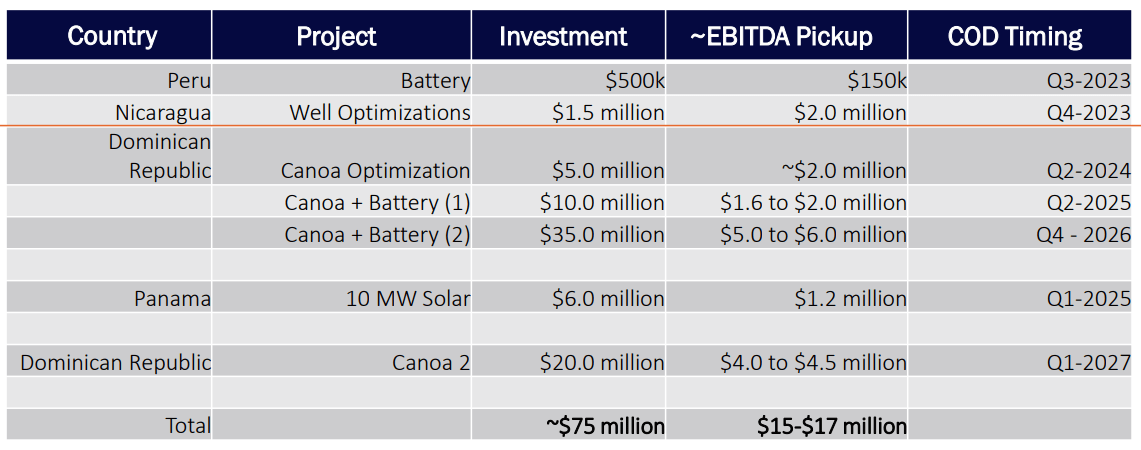

Just as Polaris did in Panama, I think we're due to see strong growth in revenues from the company's Dominican Republic projects through is Canoa project. As you can see from the graph below, the Canoa operation is a project that Polaris has invested significantly in (around $50 million) and we should see an additional pickup of about $8.6 million to $10.0 million in EBITDA over the next 2-3 years.

{kind=link}

With Polaris Renewable's run rate EBITDA at around $60 million for 2023, the additional EBITDA growth year could be highly significant, not to mention the growth we should also expect to see from Panama. With a $6 million investment in a 10MW solar project, the company expects to generate about $1.2 million annually from the project. Longer-term, the Canoa 2 project in the Dominican Republic which the company has been investing heavily in is also expected to generate EBITDA of over $4 million a year.

Potential for Acquisitive Growth

All in all, the company should be able to generate about $15-17 million in EBITDA from new organic growth projects plus another $3-5 million from existing project growth when looking out to 2027. With a target to get to $100 million in EBITDA by 2027-28, management's goals look a bit higher than what its current project growth might suggest ($60 million run-rate plus $15-17 million of project growth from investments). But where the company does see an opportunity to fill that gap is through acquisition.

Historically, Polaris has done several deals to grow by acquisition, acquiring projects, and then adding additional investments to grow capacity and expansion. Right now, the company has a fairly modest balance sheet with a Net Debt coming in at $130 million implying a Net Debt to EBITDA ratio of 2.4x, so I think the debt load is pretty manageable. While the company does have pretty high interest rates on its debt (between 7.0% to 12.4%), the maturities are fairly long-dated and spread out and as the company becomes more mature and interest rates start to come down again, it can likely refinance at better rates going forward. Moreover, its loans are all non-recourse as they are financed at the project level (not to the company itself) so in a worse-case situation the company has some protection.

Undercovered and Undervalued

Finally, Polaris is relatively undercovered by sell-side analysts, with only one analyst from Raymond James covering the stock. He has a buy rating on the stock with a target price of $21.50. From the current price, this implies a potential upside of about 60.6% over the next year. I think this under coverage by the Street could potentially act as a catalyst as institutional interest grows in the stock and more eyes catch onto Polaris Renewable.

On the valuation front, the company seems undervalued at around 6.1x EV/EBITDA. With decent growth in EBITDA expected just from current projects, that multiple will look even better as EBITDA picks up in the years ahead as its current projects in the pipeline begin to materialize. Not to mention you're getting paid a 6.0% dividend ($0.15 paid quarterly) which is supported by the company's free cash flow.

When comparing the company to its peers like Boralex (BRLXF) ( BLX:CA ), Northland Power (NPIFF) ( NPI:CA ), and Innergex Renewable Energy (INGXF) ( INE:CA ), who have multiples of 12.4x, 9.8x, and 13.8x, respectively, there seems to be a large delta in multiple compared to Polaris at 6.1x. If we use those three companies' average multiple of 12.0x, Polaris is essentially trading at half the valuation despite having a similar leverage ratio. While I think Polaris should trade at somewhat of a discount based on the geographical risk of operating in Latin America (compared to much more North American exposure for the peer group), trading at half the multiple seems like too much of a discount.

In terms of the risks to the investment thesis here, the debt could be a concern if rates were to rise. On the plus side, only the San Jacinto project ($100 million loan) is floating rate, the rest are fixed rate. Right now, as rates have risen the cost of growth has become more expensive so the company will have to be a lot more selective in the types of opportunities it looks for and only select the ones that have sufficiently high IRRs.

The second risk is jurisdictional risk. While Latin America has higher growth than the U.S. and also uses significantly less renewable energy in their total energy usage compared to the U.S., the political climate is much less stable, which has implications for multinational companies that operate there. The 16% reduction in price per megawatt at its geothermal plant in Nicaragua is just one example of the types of risks of investing in Latin America. Balancing this out, however, are long-term contracts with the government that should hopefully insulate the company somewhat.

Conclusion

In summary, Polaris Renewable provides investors with a great way to invest in renewable energy projects in growth markets. With significant capex now behind them, the company has several projects due to come onto the market in the next few years which should meaningfully increase the company's run rate EBITDA. While there is jurisdictional risk to investing in Latin America, the market has unfairly punished Polaris Renewable's stock as the company trades at half the valuation of its peers. In addition, with only one analyst covering the stock, Polaris is relatively undercovered by the sell side, which could provide an opportunity as the company grows. With more growth plans ahead to get to its $100 million target by 2028 (from the $60 million today), shares of Polaris are simply not priced for any growth at 6.1x EV/EBITDA. With investors getting a combination of dividend income, earnings growth potential, and the possibility of multiple expansion, I believe shares of Polaris look attractive at the current price.

For further details see:

Polaris Renewable Energy: Get Paid To Wait With A 6% Dividend Yield