PSNY - Polestar Q2 Earnings: A Buy-The-Dip Opportunity (Rating Upgrade)

2023-09-03 03:24:33 ET

Summary

- Polestar missed revenue expectations, but nonetheless saw double-digit top line growth in Q2.

- Polestar's shares declined 13% after earnings submission, presenting a buying opportunity for long-term investors.

- Polestar's growing EV portfolio and upcoming product launches could lead to incremental revenue growth as well as improving investor sentiment.

- Shares have an attractive valuation relative to other EV companies with significant delivery volumes.

Volvo-owned electric vehicle start-up Polestar ( PSNY ) reported results for the second fiscal quarter on Thursday that missed revenue expectations. Despite Polestar seeing continued momentum in deliveries and revenues in Q2'23, the EV company's shares declined 13% after earnings submission. Considering that Polestar continues to expect to deliver 60,000 to 70,000 electric vehicles to customers this year and is set for new EV product launches in the near future, I believe the drop constitutes a buying opportunity!

Previous rating

Polestar confirmed its guidance for FY 2023 deliveries and is now just about to kick off production for its latest EV product, the Polestar 4, in China in the fourth-quarter. An expanding product portfolio could translate to incremental revenue growth for the EV firm and, given the most recent drop in the share price following Q2 results, Polestar continues to make an even stronger value proposition on the drop, in my opinion. For those reasons, I am upgrading my rating from hold -- Strong Delivery Growth, But Risks Remain -- to buy. In January, I rated Polestar a buy -- A Turnaround Stock For FY 2023 -- but I lowered by rating following multiple disappointments in the EV industry and investors unwillingness to reward companies for their delivery achievements.

Polestar missed revenue expectations, investors are unimpressed by continual EV ramp

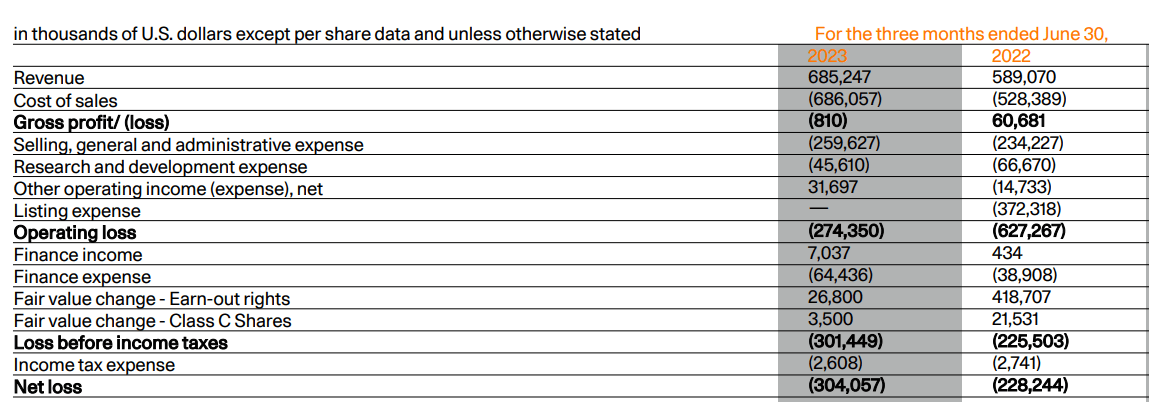

Polestar reported revenues of $685.25M for the second fiscal quarter which missed the consensus estimate by approximately $71M. Following the earnings release, shares of Polestar fell 13% and I believe results were better than investors' reaction suggests.

Polestar achieved more than $685M of revenues in Q2'23, showing 16% year over year growth as the company ramped up production and deliveries, chiefly of its flagship model, the Polestar 2. Polestar's net losses, however, expanded year over year as the company continued to grow its footprint and churned out a much higher level of deliveries compared to the year-earlier period. Polestar reported a net loss of $305M in Q2'23 compared to $228.2M in the second-quarter of last year. As the EV company starts and then ramps production of its newest Polestar 4 and 5 models in the near future, investors must expect continual operating and net losses in the medium term.

According to SA-provided consensus estimates for PSNY, the electric vehicle maker is expected to achieve positive EPS only in FY 2027 which puts the company about on the same profit timeline as U.S.-based EV manufacturers such as Lucid Group ( LCID ) and Rivian Automotive ( RIVN ).

{kind=link}

Growing EV portfolio and new product launches could translate to incremental revenue growth

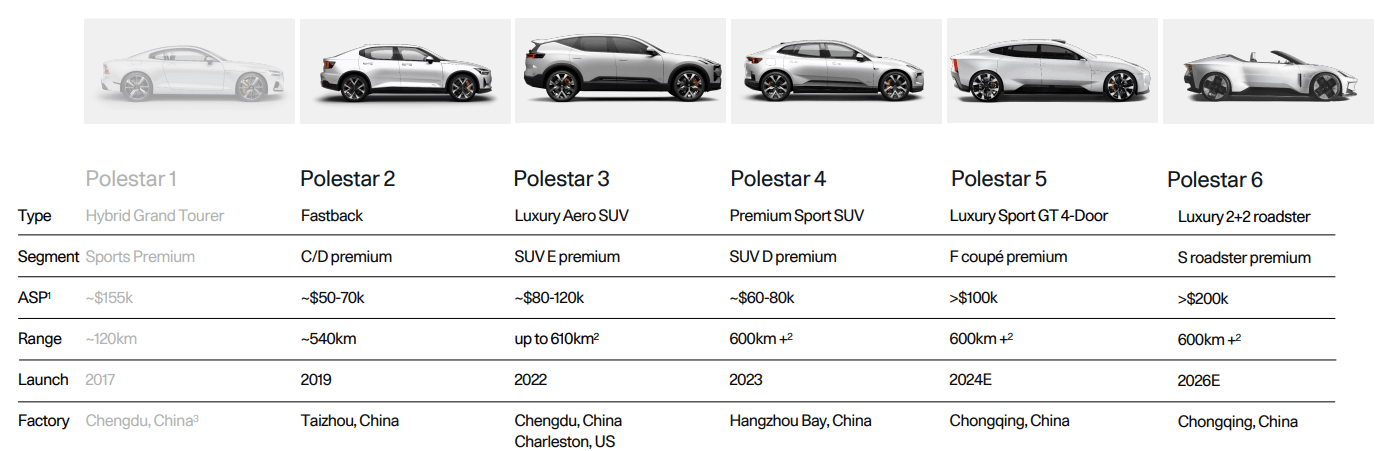

Polestar is set to release new EV products in the near future which is set to result in a denser electric vehicle portfolio and which can reasonably be expected to lead to incremental delivery growth going forward. The company is expected to launch the Polestar 4, a coupe SUV, in China with production set to begin in November 2023 in Hangzhou Bay. Next year, the Polestar 5 is set to launch, a fastback sedan, which is set to compete against the Lucid Air and the Porsche Taycan. With a tight schedule in place to launch EVs in the short term, I believe investors could see some surprises in terms of delivery projections for Polestar and ultimately the return of investor confidence in Polestar's execution.

{kind=link}

Confirmed delivery outlook

Polestar confirmed that it continues to expect 60,000 to 70,000 electric vehicle deliveries in FY 2023 and a gross profit margin of 4%. In FY 2022, the electric vehicle company delivered 51,500 EVs, meaning the confirmed outlook implies up to 36% year over year delivery growth. In the first six months of FY 2023, Polestar delivered 27,841 electric vehicles, showing 31% year over year growth, chiefly due to strong sales momentum for the Polestar 2 electric vehicle in the United Kingdom, Australia and Canada.

Polestar’s valuation

After the valuation decline on Thursday, Polestar now has a more attractive valuation and risk profile, especially in comparison to U.S.-based EV manufacturers such as Lucid Group or Rivian Automotive. Both U.S.-based EV companies achieve significantly higher market valuations which, given the accomplishments presented by Polestar for the second-quarter, is not deserved in my opinion.

Polestar is currently expected to generate top line growth of 76% next year which is lower than Lucid’s projected revenue growth rate of 169%. Rivian is anticipated to grow its revenues by 63% in the next year, so Polestar is expected to grow faster than Rivian, yet has a significantly lower multiplier factor. Therefore, based off of revenues, I believe Polestar remains an attractive investment in the EV space: shares are currently valued at a P/S ratio of 1.3X compared to 6.7X for Lucid and 3.1X for Rivian.

I believe Polestar could be valued at 2.0X forward revenues if the company manages to move towards profitability and continues to ramp up deliveries as expected. This implies a potential market cap of $10.8B, or approximately 54% valuation upside. A fair value for the shares may therefore be seen around $5.10. The two most important factors for the realization of my price target will be the successful roll-out of new EV models as well as Polestar's delivery achievements. If Polestar manages to fulfill its delivery targets, expands internationally and lowers its losses, I believe the achievement of my price target is realistic.

Risks with Polestar

The EV company still has considerable timeline and production risks (regarding the Polestar 4 and 5) which affect all electric vehicle companies that are moving into the mass-production stage. Another risk that I see with Polestar is that despite a rapidly growing delivery volume, the electric vehicle manufacturer is not yet profitable and any snags in terms of production could delay Polestar’s projected profitability date.

Final thoughts

Polestar submitted a decent earnings sheet for the second-quarter and given the confirmed guidance for FY 2023 as well as demonstrated revenue momentum, I believe the 13% price drop on Thursday was not justified. I like that Polestar is seeing solid delivery momentum and that the firm has a tight schedule in place that points to the launch of two new electric vehicle models until the end of the next year. Considering that shares of Polestar are also much more attractively valued since my last work, I believe the risk profile is more favorable and I am buying the drop!

For further details see:

Polestar Q2 Earnings: A Buy-The-Dip Opportunity (Rating Upgrade)