IIPR - Power REIT: Attractive Fundamentals Mask Real Issues

Summary

- The management team at Power REIT has done well to grow the firm's top line and cash flows in recent years.

- Based on pricing alone, the company offers attractive prospects, with robust upside on the table.

- But there are real issues for investors to contend with that even the risk-to-reward ratio for PW stock.

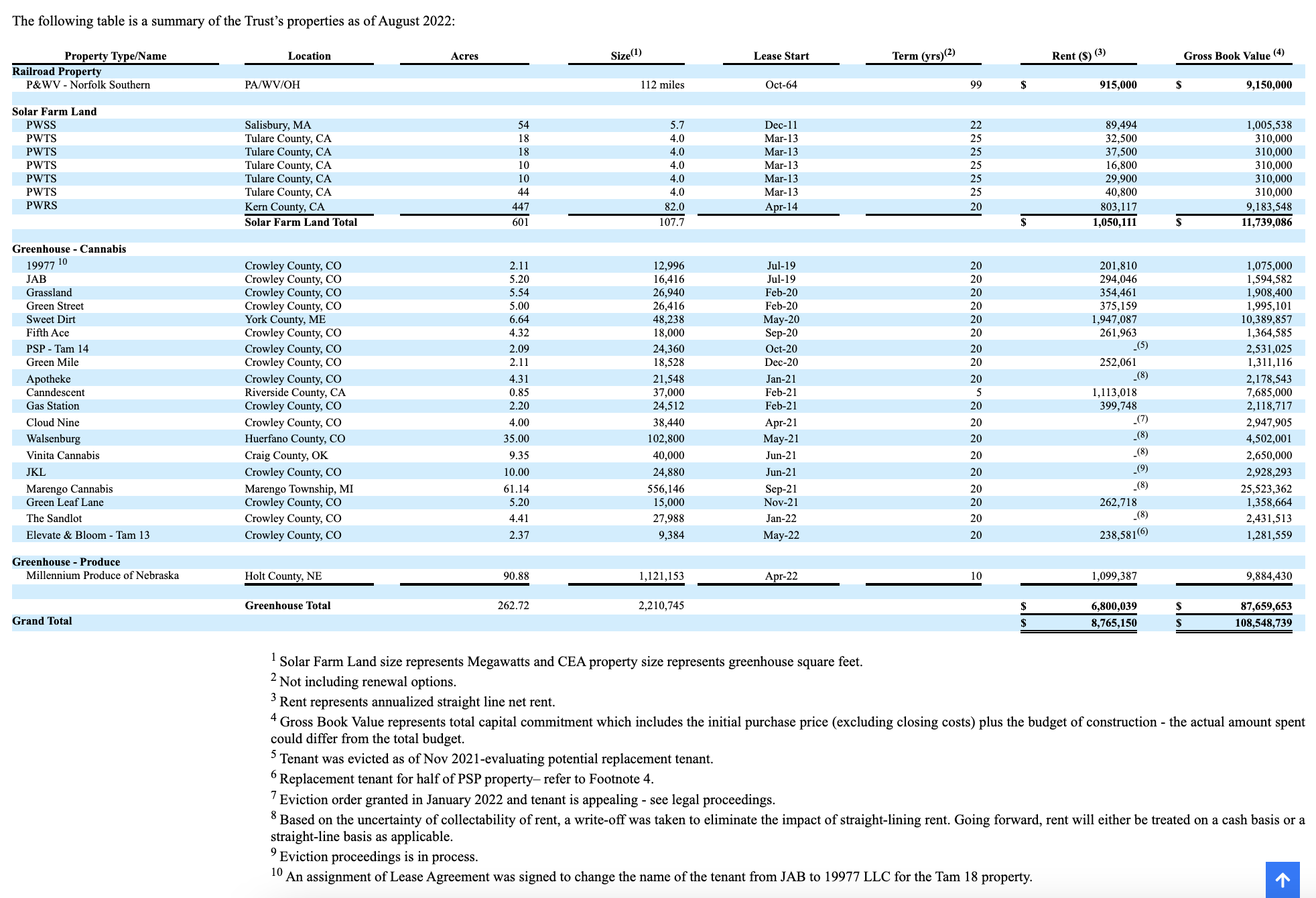

While it would be nice for investing to be nothing more than simple math, the fact of the matter is that sometimes the outcome of an investment is determined by factors that cannot be calculated. A great example of a firm with relatively robust and improving fundamentals that is trading on the cheap but that is riskier than it initially appears is Power REIT ( PW ). This company, which owns a variety of real estate, such as 112 miles of railroad assets, solar farm land totaling 601 acres, and greenhouses dedicated to both cannabis and produce, happens to have robust fundamentals but is the subject of tremendous scrutiny related to some of the disclosures in its financial reports. In truth, if the company can withstand the scrutiny, shares should offer significant upside potential. Investors who don't mind that risk might want to consider a stake in the firm. But for most investors, myself included, it would be best to approach this cautiously because of the risk involved.

Power REIT - A risky proposition

Since early January of this year when I last wrote about Power REIT, shares of the company have fallen by roughly 85%. This decline has been driven by a variety of factors. First and foremost, when I did write my bullish article on the firm, the company had been exhibiting rapid revenue growth that was driven by significant property acquisitions. Much of these acquisitions had been dedicated to the cultivation of cannabis, making the company one of only two publicly traded cannabis REITs in the US. In recent months, however, the company has significantly reduced these activities. With $33.07 million in net debt on its books and another $8.42 million in preferred stock, the firm does not appear significantly over-leveraged, with a net leverage ratio of 4.17 based on data from the 2021 fiscal year . But even so, the company has definitely decreased its acquisition activities.

The most recent purchase made by the company was completed at the end of March of this year. This was unlike any other purchases the company had engaged in though. While prior greenhouses the company acquired were focused on cannabis production, this particular one will instead focus on the production of tomatoes under a 10-year triple net lease that should bring the enterprise nearly $1.10 million in rent per year. But of course, this is just the introductory rate. After the first year, the firm will benefit from a 10% increase upon the renewal of the lease after the 10-year window, with subsequent renewal options coming in at 5% each year. Set on nearly 91 acres of land and totaling 1.12 million square feet in all, this particular property accounts for 34.6% of the company's greenhouse acreage and for 50.7% of its greenhouse square footage . But the asset in question will be far less valuable than prior cannabis acquisitions, accounting for an estimated 12.5% of all annual rent the company is expected to receive.

{kind=link}

Ardent fans of the cannabis space may view this acquisition as perplexing. After all, the purchase is slated to be less valuable from a revenue perspective than other investments the company had made. Having said that, I see this as a sign that management is trying to further diversify away from the cannabis market. This has a lot to do with the state of that market today. Due to an over-investment in the cannabis space, there seems to be a glut that formed. From January of 2021 to January of 2022, for instance, the price for marijuana flower, edible, and vaping products each fell by more than 11%. The picture in recent months has been even more severe. According to one source , from January of 2021 through the end of June of this year, the average wholesale price per pound of marijuana flower dropped nearly 59%, with growers and dispensary owners saying that the decline had actually been sharper than the data suggests. On a wholesale basis, the cost per pound between October of last year and August of this year was down by 40% in Colorado where the company has most of its exposure.

At first glance, some investors may not view this as terribly significant. After all, Power REIT engages in the leasing out of assets for cannabis production, not in the actual production of it itself. While this is true, it's also true that its tenants might be showing signs of financial stress. As pointed out by another Seeking Alpha author earlier this year, there are multiple greenhouses being leased out that are facing significant issues. At one location, called Cloud Nine, the company was granted an eviction order in January of this year but, as of the end of the second quarter of this year, the tenant was appealing. At another location, called PSP - Tam 14, the tenant was evicted in November of last year and that property has not been leased out to another tenant since. At another location, called Elevate & Bloom - Tam 13, a replacement tenant for only half of the property was identified. The list of other problems goes on, but you should get the idea from this.

{kind=link}

Also pointed out by the same aforementioned author, there seems to be an issue with an entity that is partially owned by CEO David Lesser. That entity, known as Millennium Sustainable Ventures Corp ( OTCPK:MILC ), is 20% owned by Power REIT's head chief. Multiple greenhouses with combined lease payments due of over $7 million annually, are considered by management to be risky in the sense that the uncertainty of collectability of rent is elevated. Interestingly, this is the same business that owns the tomato production firm that is leasing out the aforementioned produce greenhouse owned by Power REIT. However, that particular property is not listed as being subjected to elevated risk. One good thing for shareholders is that Millennium is also a publicly traded company, so we can know how it is faring fundamentally. Unfortunately, the answer to that is that it's not faring all that well. In the first half of the 2022 fiscal year, for instance, the enterprise generated revenue of less than half a million dollars and generated a net loss of $7.71 million. Even its cash flow is negative to the tune of $4.48 million. Add on top these allegations of poor company governance, and risks regarding the firm are many and significant.

{kind=link}

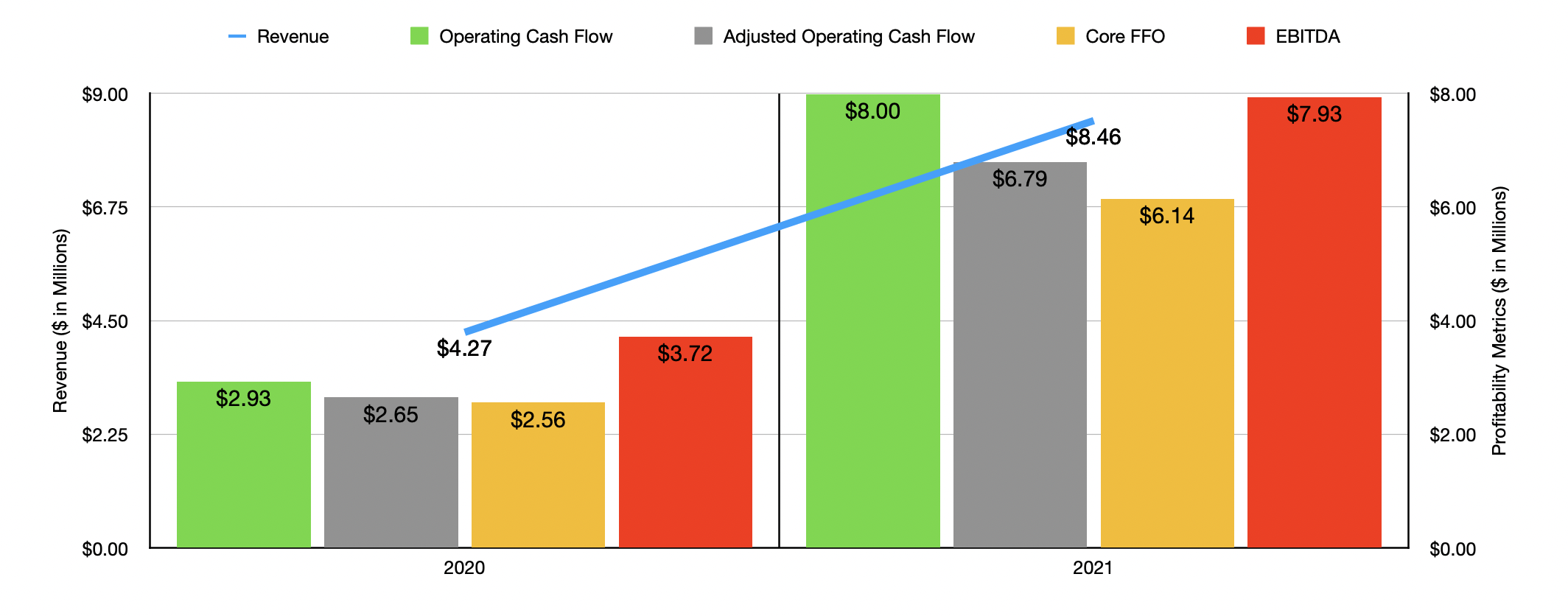

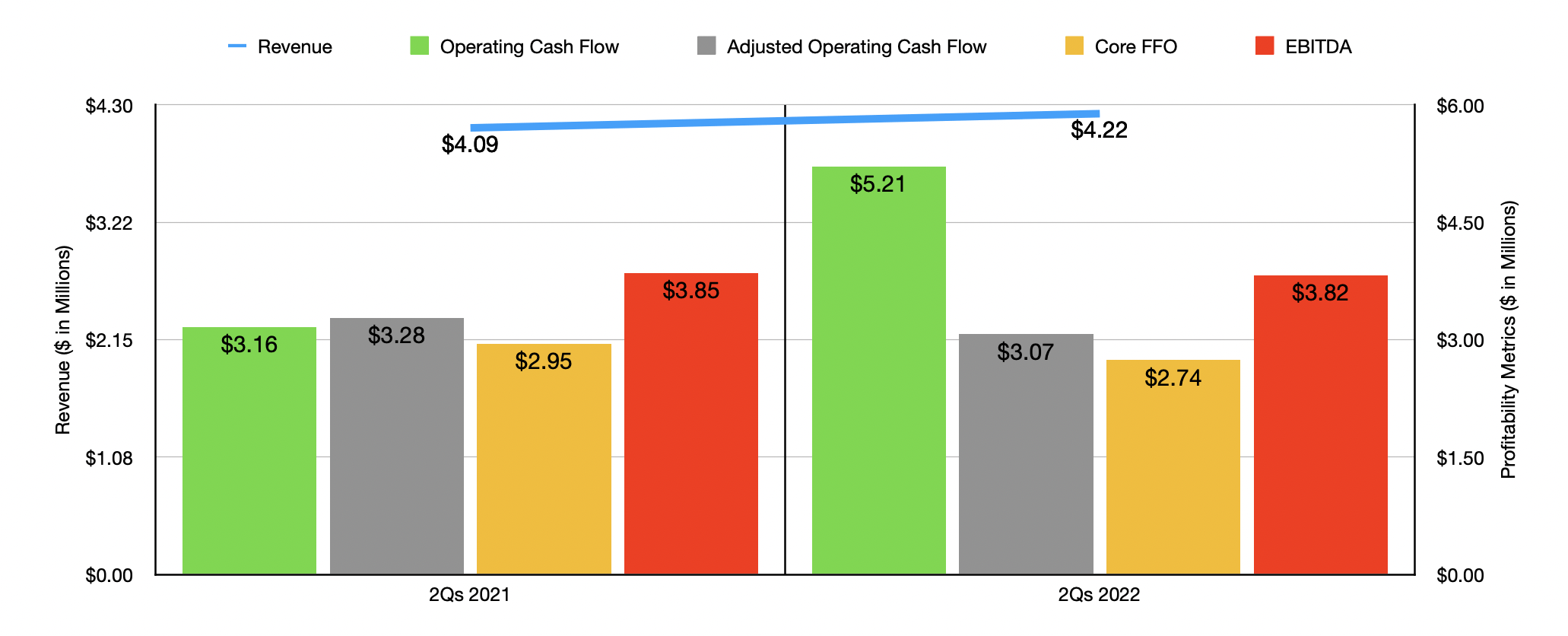

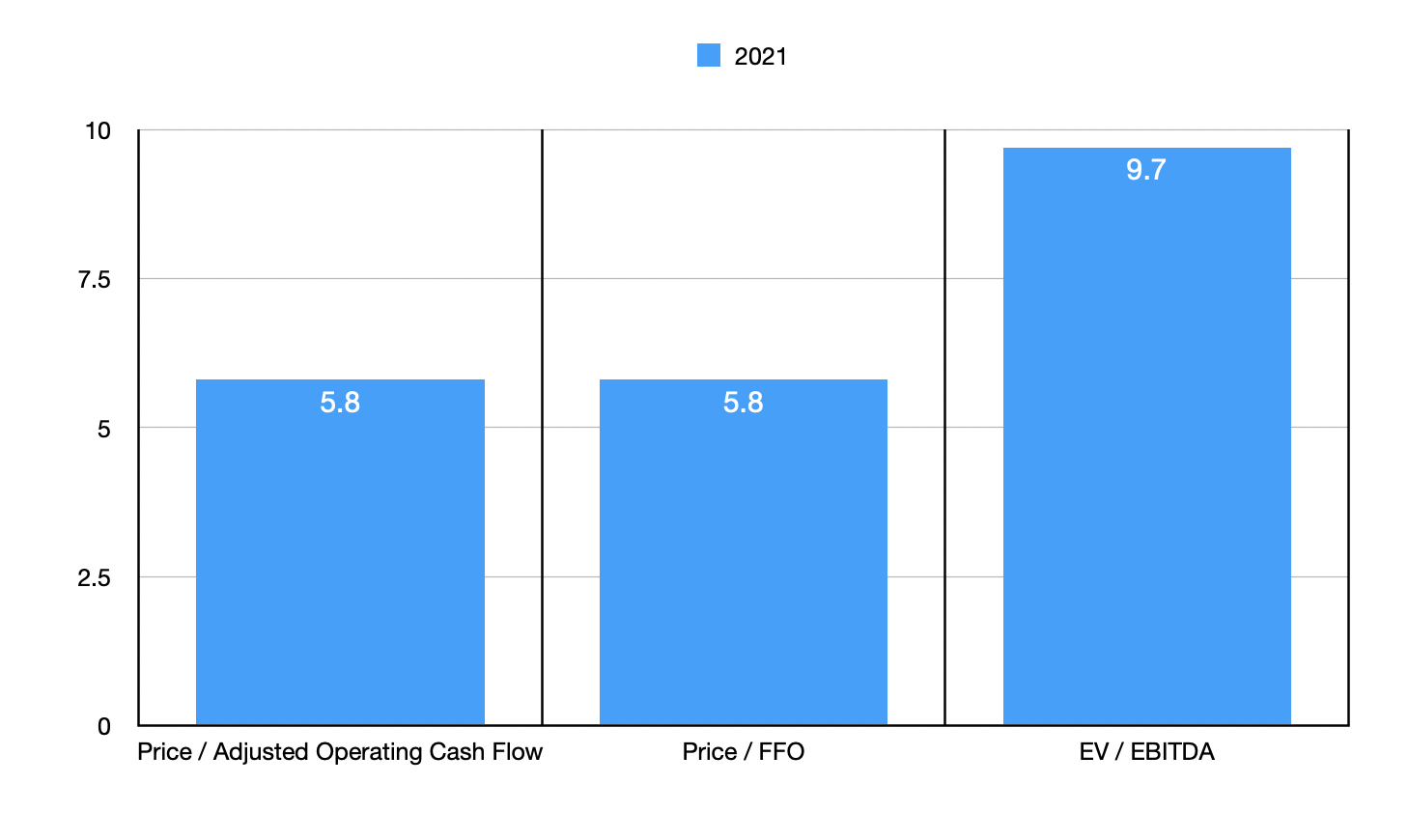

In the event that management can pull out of these issues, upside for investors could be meaningful. As you can see in the charts above and below, recent financial performance for the company has been encouraging. As shown below, the firm does look to be trading on the cheap from an absolute perspective. For instance, using data from the 2021 fiscal year, the enterprise is trading at a price to adjusted operating cash flow multiple of 5.8 and at a price to FFO (funds from operations) multiple of 5.8 as well. The EV to EBITDA multiple of the company, meanwhile, is 9.7. To put this in perspective, I also compared the company to Innovative Industrial Properties ( IIPR ), another REIT dedicated to the cannabis market. By comparison, it's trading at a price to operating cash flow multiple of 36.5 and at an EV to EBITDA multiple of 40.6.

{kind=link}

Takeaway

All things considered, I do believe that Power REIT is an interesting business. But interesting does not always make for an attractive investment. Given how shares are priced and if management can pull out of this cannabis downturn, upside for investors could be very significant indeed. But at the same time, there are a great number of red flags to worry about. I would go so far as to say that the risk here may only be appropriate for investors who understand a significant loss of capital could be on the table. For most investors, however, I would take a more neutral stance in the sense that while upside could be significant, the amount of risk assumed for that upside is likely significant as well.

For further details see:

Power REIT: Attractive Fundamentals Mask Real Issues