CA - Precision Drilling: Marked Down And On The Sale Rack

2023-04-04 08:00:00 ET

Summary

- Precision Drilling has sold off but may be in the process of rebounding as are other drillers. The company appears to have pricing power as rig margins have increased QoQ.

- The company is trading at low multiples now which we expect will rise with crude prices during 2023.

- Investors looking for price performance may find PDS stock attractive at current levels.

- The information in this article was previously discussed in the Daily Drilling Report on 3-31.

- All pricing in CAD unless noted.

Introduction

After a long slide, beginning in late January, drilling contractors are perking up and may be set up for a further rally if recent oil price gains are sustained. In this article we will look at Precision Drilling Corp. (PDS), a Canadian provider of top-tier drilling and related technology services.

{kind=link}

We still hold the view that top tier drillers like PDS are undervalued relative to their earnings potential and are now selling at a discount. The rig count is unlikely to rise significantly from the present 760ish level, meaning there won't be a flood of new rigs driving down day rates. This translates to pricing ability as rigs are recontracted. CEO Kevin Neveu commented about capital discipline keeping the high spec market tight:

We expect to see, let's say, pretty firm discipline. And we've seen really good discipline over the last few months. We've got around limiting the number of potential rigs for upgrades and setting high return thresholds. So it just feels like that discipline is going to stay in place, and we're watching it closely.

PDS is trading down presently, at least from recent highs in the upper $80's, and I think the company presents an attractive entry point for investors seeking growth. With oil prices moving back into the $70's my concerns about operators dropping rigs is largely abated. With a stable to slightly increasing rig market PDS should see growing cash flow through the year.

The thesis for PDS

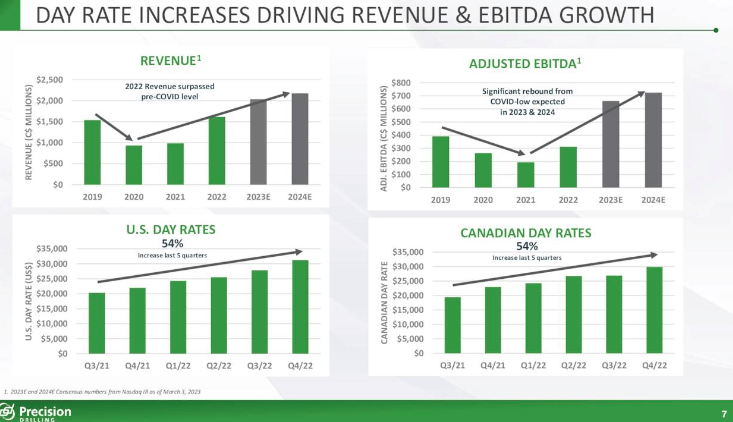

PDS has a sizeable position in the U.S. market with an estimated 8% share, and a fleet of 101 rigs, 66 of which are the Super-Triple that command a top-tier day rate of $35K USD plus. In Canada they hold a dominant share with 33% of the market with 111 rigs available, 26 of which are Super-Triple and 56 of which are the Super-Single. (Note- a Triple can run a 90' stand of pipe, where a single will run a single joint-30'), these can enter the well path at a slant, saving trying to build angle- not always easy in soft formations , into a shallow reservoir. The company also has an 8-rig international footprint with 3 in KSA and 5 in Kuwait. International rigs capture premium pricing at ~$50K per day.

In addition to a well servicing business (basically pulling/running pipe, performing wireline work, and pumping stimulation treatments), PDS also has other retail offerings: Alpha Automation-Drilling Software, and EverGreen emissions monitoring that can run the day rate up substantially. Other drilling contractors we have covered have similar offerings, but we've never had any metrics on what they contribute financially, until now. Kevin Neveu, CEO comments in regard to an DC SCR 1,500 rig upgrade in Canada:

What it will be is a Super Triple ST-1500 rig with remote sport generators and -- we expect to have some additional add-ons above that rate that will include our technology, the technology and expect also there'll be some EverGreen products on top of that rig. So the all-in rate for that rig could easily move into the low $50s (CAD I presume)

This fits into a theme we have discussed with other service providers, ex-fracking companies and sand. The tightness of these premium rigs (High HHP, pad walking, high pressure pumps, increased hookload capacity, AC power) gives PDS leverage when adding ancillary services to the ticket.

Last week PDS has rebounded 10% off 1-year lows, and I believe there are a couple of drivers for this momentum. The first is we have seen a strong turn in oil price since the beginning of March, rising from the mid-$60's to the mid-$70's. Second, the capital discipline that operators have used to keep from over-expanding during the higher prices, held in the other direction as oil and gas prices nose-dived in Q-1. We're only off a few rigs in that time, so the supply/demand equation should remain where it is now, with the drilling contractors holding the high ground.

{kind=link}

In my view, we are not going to see the rate of continued day rate increases that were representative of 2022, but some upside remains. The exception would be the addition of ancillary services to the daily ticket, but there is a limit, that we are not far from, that operators will pay for a land drilling rig.

{kind=link}

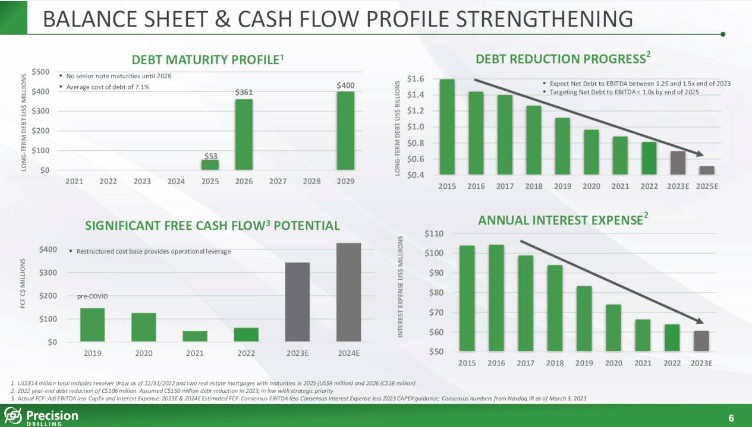

PDS has spent much of the increase in revenue and profitability in cleaning up their balance sheet. LT debt stands at ~$800 mm-USD, and the company projects cutting that in half by 2024. Carey Ford, CFO comments on the balance sheet and liquidity:

We continue to reduce both absolute and net debt levels, primarily through free cash flow generation and succeeded in reducing debt by $106 million in 2022. As of December 31, our long-term debt position, net of cash, was approximately $1.1 billion-CAD, and our total liquidity position was approximately $600 million, excluding letters of credit. With continued debt reduction and activity expectations, we believe we will end 2023 with a net debt-to-EBITDA ratio of between 1.25x and 1.5x, moving Precision closer to our updated goal of below 1x.

A couple of potential catalysts

We have discussed the Clearwater play in Canada's Montney basin in previous articles . PDS has a line of rigs particularly suited for drilling this shallow play. Kevin Neveu, CEO comments on the potential for their Super-Single rigs:

This drilling is ideally Precision's Super Single style rig. With this rig, we typically drill these complex multilateral wells from 12 to 14 days each. Precision enjoys a 45% market share in the Clearwater where we have similar market shares for all heavy oil and sand drilling in Canada. The second quarter, our breakup of shaft activity level looks to be around 40 rigs compared to 19 last year. This higher level was driven largely by sustained pad activity in the Montney and Clearwater.

That's a big bump YoY, going from 19 to 40 and should positively reflect on second quarter earnings, at a time normally the spring thaw slows activity down.

Next is their Haynesville footprint. Drillers have kept the Haynesville humming at multi-year highs for over a year now, with no sign of slowing due to low gas prices. With 12 rigs recently re-contracted at current rates in this basin, this activity appears to be on solid ground for the year.

Q-4, 2022 and Guidance

Q-4, adjusted EBITDA of $91 million increased 43% from the fourth quarter 2021 and was supported by higher North American activity and day rates. It would have been $166 mm but $75 mm cash accrual of performance share price based compensation was realized in the quarter for payment in Q-1.

Let's deal with this "bonus" payment to employees. Top level employees, expect top level compensation. You may have heard there's a shortage of qualified people in some segments of the oilfield. It's a fact. Payment of the performance bonuses help keep these high performers, and it should be noted that the stock rose by half during the year, and debt reduction targets were met. This comes from success in the overall marketing effort, and as a potential investor, you should applaud the company taking care of these folks that put it all together! I freely admit to receiving this kind of compensation in the past, and felt like I'd earned every nickel of it.

Precision averaged 60 rigs in the U.S. in Q4, an increase of 3 rigs from Q3. Daily operating margins in the quarter after impacts of turnkey and IBC were US$11,849, an increase of US$2,187 from Q3 and exceeding previous guidance. In Canada, drilling activity for Precision averaged 66 rigs, an increase of 14 rigs or 27% from Q4 2021. Daily operating margins in the quarter were $12,348, an increase of $2,314 from Q3 2022, and ahead of prior guidance. For Q1, they expect margins to be relatively flat in Canada due to season renewals. Internationally, Precision in the quarter averaged 6 rigs and average day rates were US$49,918, down approximately 4% from the prior year due to active rig mix.

Capital expenditures for the quarter were $57 million and $184 million for the year

Guidance

For Q1, PDS expects normalized margins to increase another US$2,000 per day from Q4 levels. Day rates remain firm with leading edge rates in the $43 ((CAD)) range. They expect to continue repricing currently contracted rigs with existing price environment as the contracts renew over the course of 2023.

Internationally, due to certification timings, they expect 2023 activity to be only slightly higher than 2022 on an annual basis, despite having 8 rigs running by the end of the summer. 2024 activity is projected to increase by 30-plus percent over 2023.

The 2023 capex plan is $235 million and is comprised of $163 million for sustaining and infrastructure and $72 million for upgrade and expansion. Currently PDS has 61 rigs running in the U.S., and expects to be in this range plus or minus for the first quarter. EverGreen solutions are expected to gain wider customer penetration in Lower 48 during 2023. In Canada currently, they have 100% utilization with 28 Super Triples running, and expect to add 2-more during the year. Additionally they have 43 Super Singles running with about 85% utilization, again, the highest since 2014. All told PDS has 78 rigs total in Canada and expects to peak at 79 or 80 later this month.

Risks

The primary risk is gas pricing. At some point if the pricing for natty doesn't improve substantially gas drilling is going to take a hit. There are no real catalysts for gas right now, so this isn't a remote possibility. In that scenario shares of PDS could suffer or languish at current levels.

Your takeaway

The contract drillers are on sale right now. If this segment interests you, you are not likely to get a better entry point this year. This holds particularly true for PDS. With its fairly pristine, and still improving balance sheet, rig utilization, and expanding margins, I view the company as being underpriced.

Currently they are trading at around 2X forward EV/ Adjusted EBITDA. Analysts are calling for a BUY rating on the stock and a median USD price of $66.25 . That only takes them to a 2.5X multiple, which I think is still pretty conservative, but perhaps not for this time of year, when the spring thaw in Canada traditionally kills activity. ( Remember thanks to the Montney pad work they are keeping double the rigs working they did in 2022. )

As of late January their stock was selling at $87 USD, so the analysts may be a little timid here.

For further details see:

Precision Drilling: Marked Down And On The Sale Rack