PCOR - Procore: Long-Term Outlook Remains Fine

2023-11-19 23:47:57 ET

Summary

- Procore's recent earnings exceeded expectations with revenue of $248 million and a non-GAAP EBIT margin of 3%.

- The stock saw a dip post-earnings due to weak RPO growth and low net customer additions, signaling a softening of demand.

- Despite short-term concerns, Procore's long-term growth outlook remains positive, with strong revenue growth, product innovation, and a volume-based pricing model driving adoption.

Overview

My recommendation for Procore ( PCOR ) is a buy rating, as I remain confident in the long-term outlook of the business. Note that I previously rated PCOR a buy as the company exceeded my expectations, which led me to believe that they would be able to deliver breakeven profitability much earlier.

Recent results & updates

PCOR reported 3Q23 revenue of $248 million and a non-GAAP EBIT margin of 3%, a very strong set of results that came in above the upper end of management guidance. Most importantly, PCOR appears to be on track to achieve positive FCF this year, which is in line with prior management guidance. The stock, however, saw a ~20% dip post-earnings, which I believe was driven by the weak RPO metric. PCOR current RPO grew 27% in the quarter, a 500-bps deceleration vs. 2Q23. Doing the math, this meant that implied current bookings growth decelerated to 20%, a major step down of 1300bps vs. 2Q23, and the absolute figure was down 1% sequentially. Net customer additions of 363 were also low compared to the 600 net additions seen in the previous few quarters. The low rate of net customer growth suggests that smaller-sized customers are less eager to invest in transformative projects. The near-term outlook is already weak, and management's highlighting of a few large deals that have been delayed since 3Q23 and have not yet been closed adds fuel to the fire by signaling an incremental softening of demand.

There is some truth to the bear case, and I agree that the immediate outlook is not promising in light of these concerns and weaknesses. But as a long-term investor, I believe this might be an interesting opportunity to buy the stock. Objectively, in 3Q23, revenue did grow 33%, beating consensus by 600 bps. This strong growth was driven by 14% customer growth and 15% ARPU growth. The latter showed an acceleration of 200bps vs 2Q23, indicating that users are willing to pay more once they start using it. Importantly, there has been a marked improvement in the renewals, where a higher percentage of customers renewed their flat volume commitments. This translates to better visibility, which makes management revenue guidance seem much more reliable. Moreover, management is also now guiding for a 2-3% positive non-GAAP EBIT margin range, which was one of the driving factors for my rating upgrade (reaching profitability). PCOR cash flow is also coming in nicely, reaching positive ground as FCF came in at $22 million.

The long-term growth outlook appears very positive, the way I see it, as PCOR continues to roll out product modules that should further enhance its offerings. To give a few examples, PCOR has just released Copilot, a Gen-AI platform that can summarize and compare data against various regulatory requirements and provide users with "what-to-do next." Given that users already store their data on Procore, this module should accelerate workflow processes. PCOR also released Procore Pay to increase wallet share. I see each of these product launches as another weapon in PCOR's arsenal that it can use to further deepen its claws into the customer's workflow process. The more embedded PCOR is (from planning to workflow processes to even payments), the harder it is for users to replace PCOR. This ends up with PCOR having more pricing power over time.

{kind=link}

{kind=link}

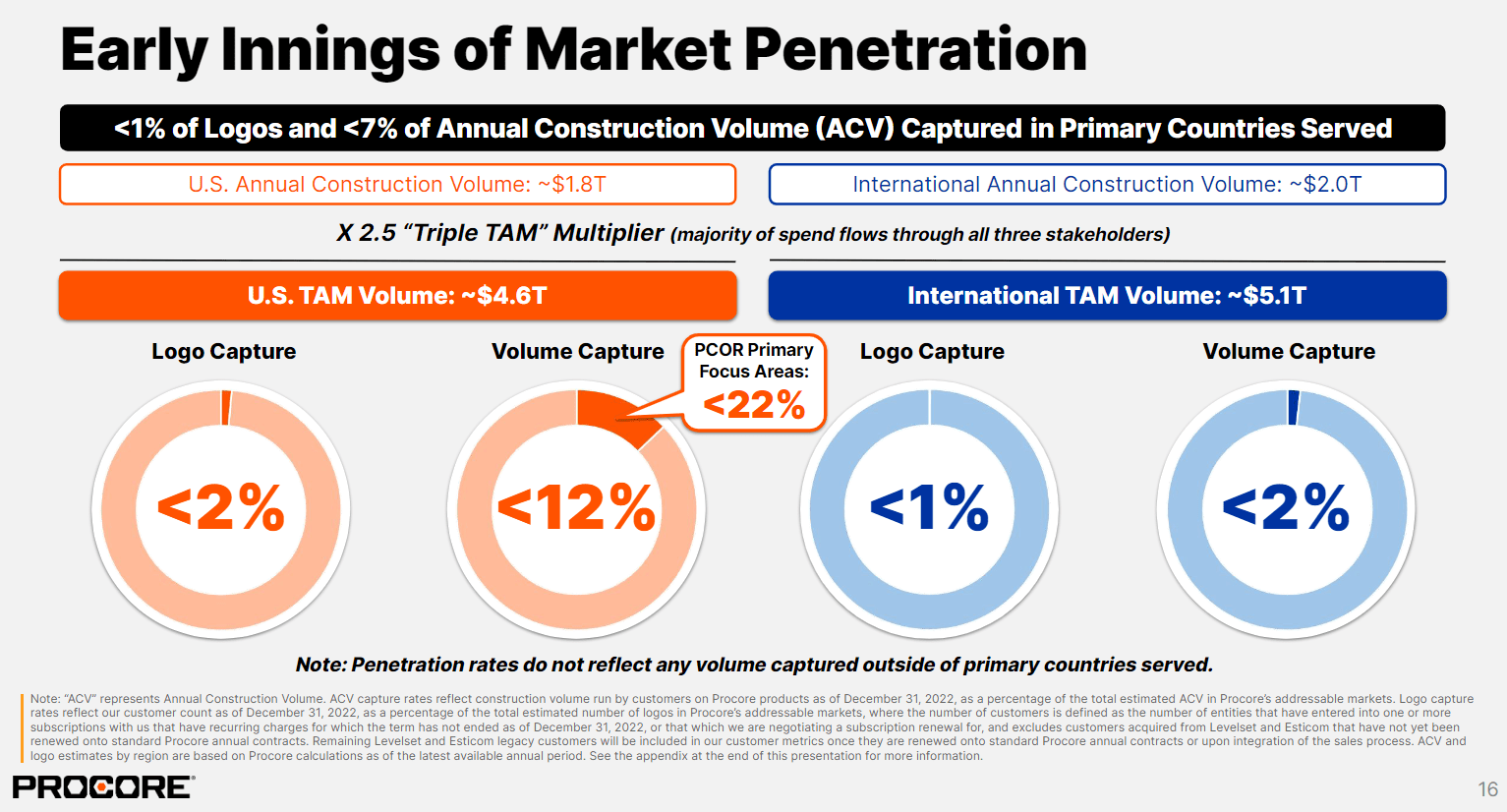

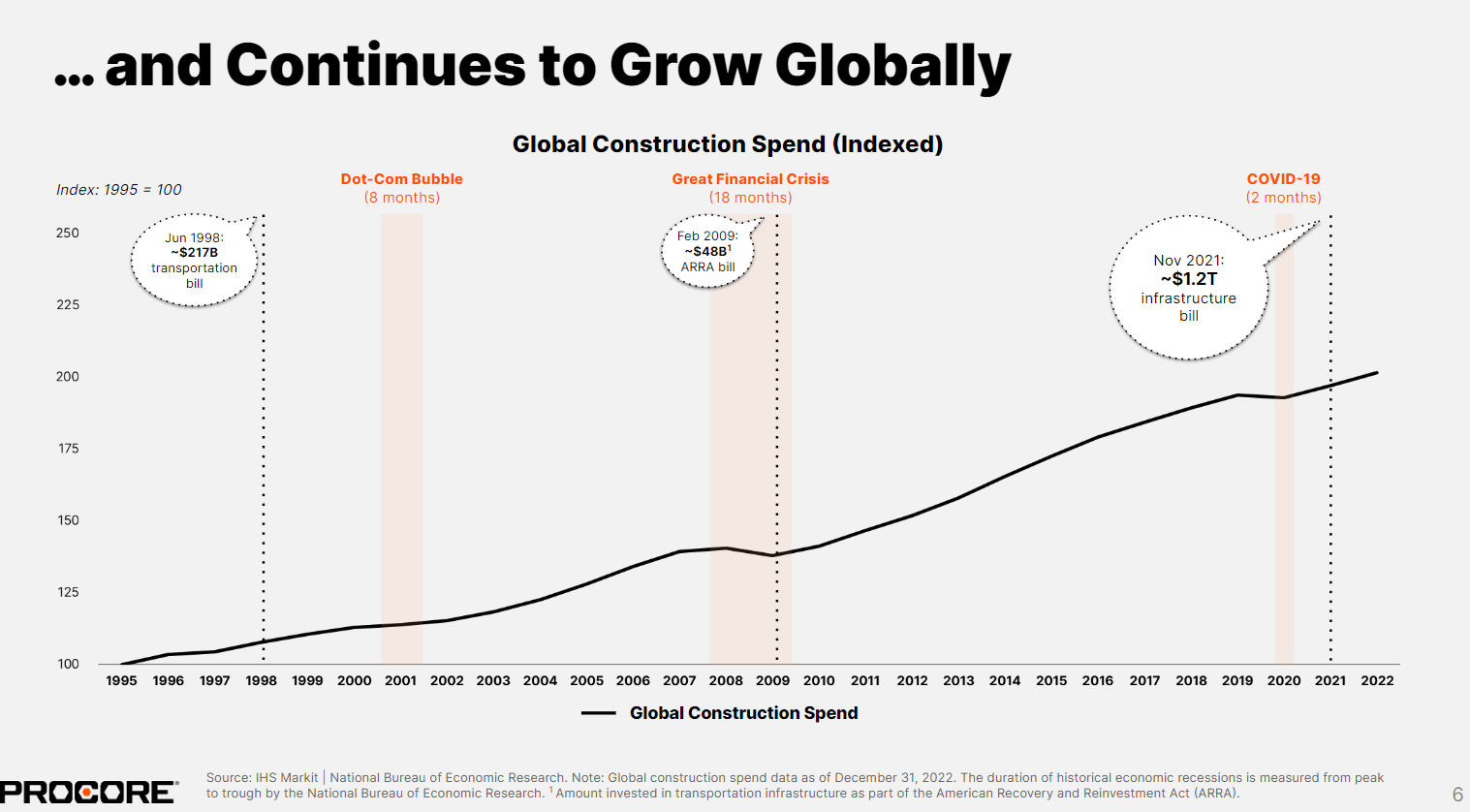

I would like to remind long-term investors that PCOR has not even begun to scratch the surface of the market and that the industry is still in its infancy in terms of digitization. The volume-based pricing model that distinguishes PCOR is a key factor in driving widespread adoption and collaboration on the platform, which in turn attracts even more users, projects, and data, resulting in a strong network effect. Additionally, I anticipate that PCOR will keep releasing new products to further unlock incremental TAM via cross-selling.

Valuation and risk

Author's valuation model

According to my model, PCOR is valued at $91 in FY24, representing a 62% increase. My growth assumption remains the same for PCOR, as revenue continues to grow very strongly and management has even raised their guidance. While RPO might be weak, the metric can be easily disrupted by the timing of the closing of the deal; as such, I am not raising the alarm bells yet.

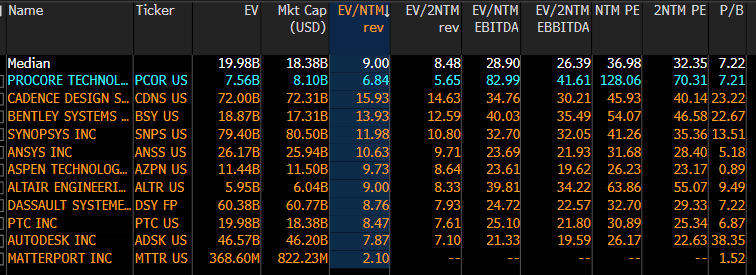

Because of the near-term outlook concern, PCOR is now trading at 6.8x forward revenue, which I believe will increase as the market recognizes that PCOR's long-term outlook remains unchanged. Historically, PCOR has traded in line with peers (who are now trading at ~9x forward revenue), and I expect the gap to close over time. PCOR is a business that is growing much faster than peers on average, and it is still in the early innings of its growth. I don’t think it deserves to trade at a discount.

{kind=link}

The investment risk here is that AGCO is likely to continue facing macro pressures. Management has called out the challenging demand environment, citing increased scrutiny, deal slippage, and weakness in the last two weeks of 3Q. Given the weak stock sentiment, if 4Q results show another massive deceleration in RPO growth, the stock might be hit further in the short term.

Summary

Despite recent stock dips following PCOR earnings, my long-term buy recommendation remains. While concerns over weak near-term outlook and declining RPO growth have affected market sentiment, I remain optimistic based on PCOR's 3Q23 performance. Strong revenue growth of 33%, bolstered by customer and ARPU growth, signals robust fundamentals. Continuous product innovation should continue to enhance PCOR’s product offerings and its stickiness over time.

For further details see:

Procore: Long-Term Outlook Remains Fine