CA - ProPetro: Don't Write Off This Shale Fracker For 2023

2023-05-07 04:50:09 ET

Summary

- Onshore oilfield services saw a major sell-off, spurred by the weakness in U.S. natural gas prices and the regional banking concerns.

- The thought is that dry gas basins will reduce rigs and frac fleets to moderate production; the excess capacity will move to oil basins and erode service margins.

- However, not all fracking companies are in the same boat; PUMP only operates in the oil-focused Permian and its fleets aren't exposed to the spot market.

- PUMP's Q1 EBITDA margin was the best in 3 years; PUMP's customer base is also on the higher end so activity should remain robust.

- The recession concerns are valid, but you can't go bankrupt if you have no debt.

Investment thesis

ProPetro Holding Corp. ( PUMP ) is a provider of hydraulic fracturing, wireline, and other oilfield services; the company operates primarily in the oil-focused Permian Basin. Similarly to Liberty Energy ( LBRT ), which I covered recently, and other peers, like ProFrac ( ACDC ) and CalFrac ( CFW:CA ), PUMP has seen a major sell-off YTD:

A major reason for the sell-off has been the weakness in U.S. natural gas prices ( NG1:COM ):

The mainstream narrative is that the low prices will drive a moderation of gas supply. As the associated gas that comes from oil-focused basins like the Permian isn't price sensitive - the byproduct economics works even with $0 gas prices - the thought is that dry gas basins will have to cut first. Namely, the industry experts have nominated the Haynesville as the new U.S. "swing" gas producer. Appalachia is also gas focused but has better economics due to the higher liquids yield.

If the Haynesville drops rigs or frac fleets, that is a direct hit to the service providers exposed to the basin. However, there could be a secondary effect too. On many Q1 earnings calls, of producers and services providers alike, analysts have been questioning if the rigs and fleets freed up in the Haynesville won't move to other basins, like the Permian. If so, they could tilt the supply-demand balance in favor of the producers and erode the margins of service providers.

Pile onto this the regional banking crisis that portends a further dry up in liquidity, and you have the perfect storm. I am not necessarily disagreeing with the market's narrative although natural gas has the tendency to surprise. Rather, the "macro" ignores the competitive advantages of individual companies, and, in this situation, not everyone is in the same boat.

Here is what I think PUMP has going for it:

- Focus on the Permian where gas prices aren't an activity driver;

- Long-term contracts with more stable pricing than the spot market;

- Soon-to-be 2/3 next generation fleet that will matter more because carbon has become a KPI for operators;

- No debt; this isn't another distressed company, many of which went under back in 2020.

Add to all this the forward EBITDA multiple of 1.5x (!), and I think all together it makes for a decent value stock that is worth taking a look at.

The gas outlook isn't great

The near-term outlook for U.S. natural gas isn't great:

{kind=link}

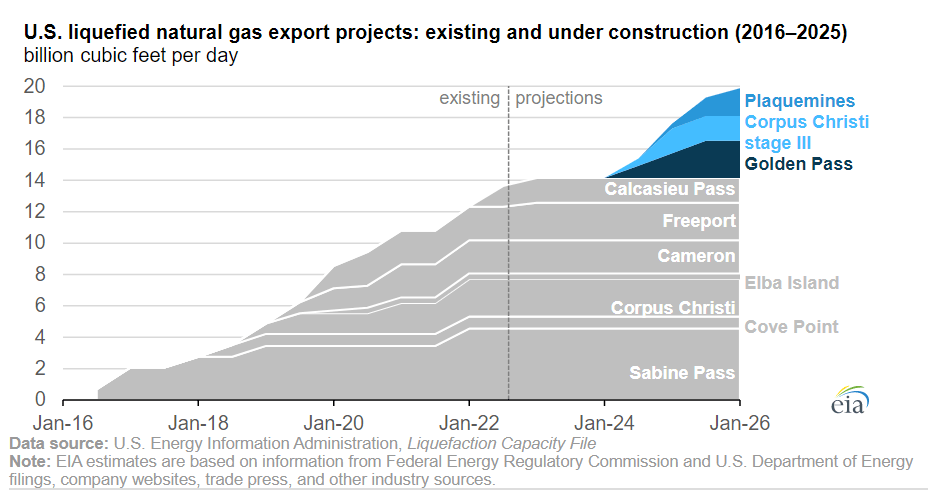

The hope is that LNG exports will absorb a greater share of the U.S. production, but liquefaction capacity won't increase meaningfully until 2024:

{kind=link}

The futures curve is in steep contango, but it doesn't show a return to a $4 handle until December 2024.

But ProPetro isn't a bet on natural gas

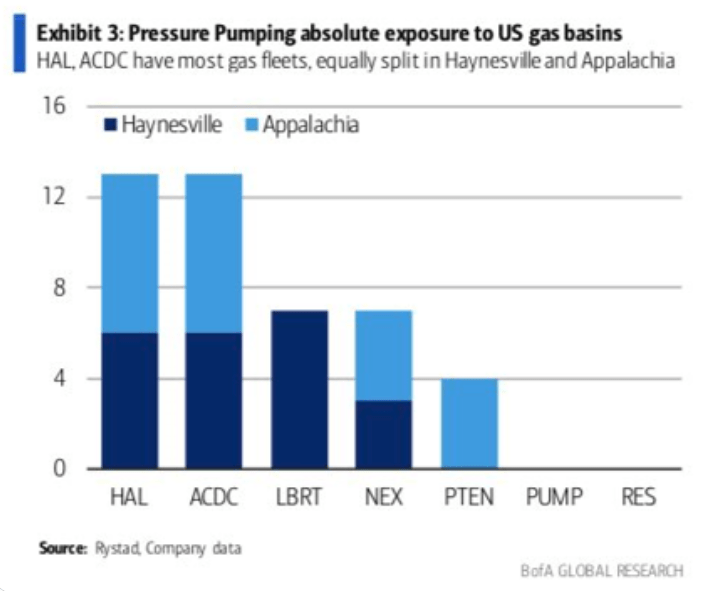

Here is where the bottom-up look disagrees with the macro:

{kind=link}

PUMP has no exposure to gas basins; this was also discussed on the recent Q1 earnings call :

As you know, and as many people know that follow us closely, over 99% of our business - excuse me - is focused right here in the Permian Basin where we're sitting today. That said, on top of that, we're also focused with some of the best blue chip operators that have the most consistent activity outlook.

On the call, management also discussed the long-term contract vs. spot market dynamics:

What we saw in the first quarter in that lull that I mentioned earlier was really very minimal. We have customers that are operating large, complex operations. And our - most of our customers, if not all of our customers, they don't even operate in the spot market. So, the data in which they gather, say, from a pricing or fleet availability standpoint is rather limited because they are so laser-focused on the consistency and continuity of their own operations. Next to that, there has been quite a hit to the spot market. I think you've seen it in some of the results of our peers that are more spot market focused. And that's what happens when the cycle matures like it has here recently that that may be a spot market that ran out in front of the rest of the activity in the Permian and in the U.S. was relatively overpriced and much of the pricing changes that maybe you've seen across the second half of the first quarter going into the second quarter from a lot of our peers or profitability kind of coming in a little bit is absolutely a spot market data point, of which you haven't seen from us nor have you seen in any of our materials or our scripted remarks that we think that, that bleeds into what we're doing here in the near-term.

To sum up: (1) PUMP doesn't have gas basin fleets that it can lose; and (2) it doesn't play in the Permian spot market where the price weakening could be seen.

$70 oil won't shut down the Permian

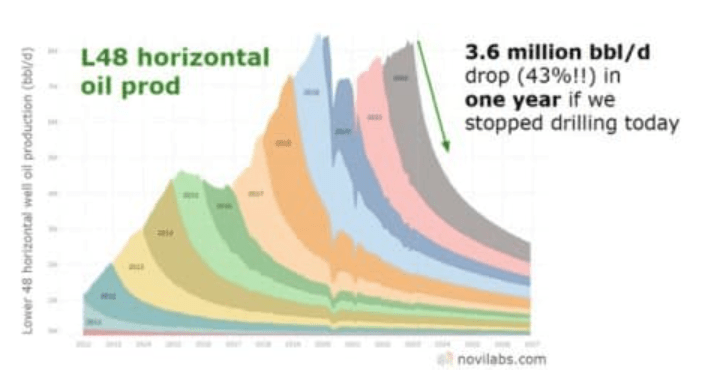

Is the Permian's oil activity in danger though? Probably not at $70 oil ( CL1:COM ). First, "staying flat" requires a lot of work. Here is a chart via NoviLabs and oilprice.com that is worth a thousand words:

{kind=link}

Per this estimate, oil production may drop by 43% (!) in one year without drilling. Unless we have a COVID lockdown repeat from 2020, I can't imagine scenarios in which that much production needs to be lost to balance the markets.

Add to this PUMP's "heavy-hitter" customer base:

{kind=link}

Endeavor is private, but the other 2 in the Top 3 are Pioneer ( PXD ), which boasts the longest-lived Permian inventory, and Exxon ( XOM ) via XTO. When management touted their "blue-chip" customers on the call, I don't think they were exaggerating.

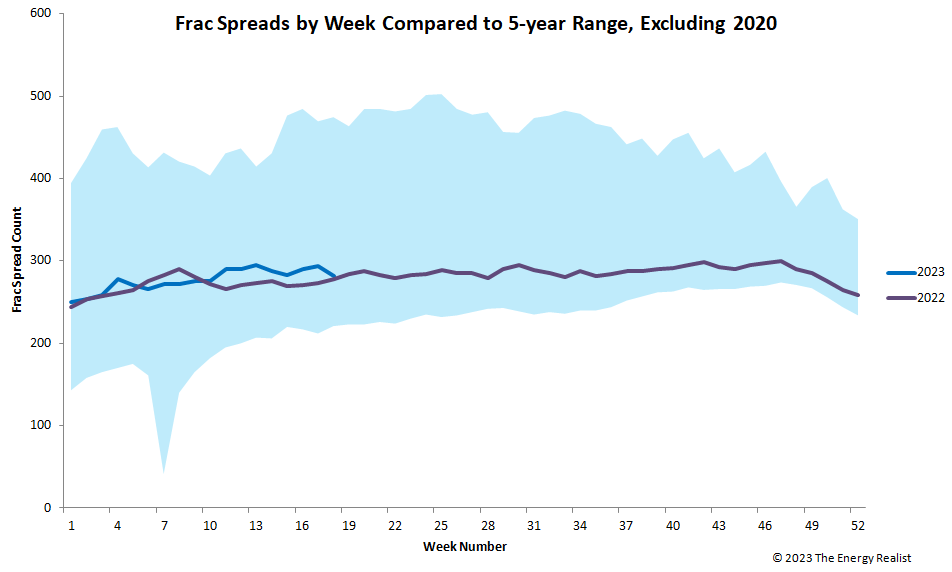

The rig count is down in the last weeks but still higher than a year ago:

Frac spreads also dropped by 12 last week but looks steady compared to 2022:

{kind=link}

Q1 was better sequentially

I am emphasizing "2022" because it was a great year for onshore oilfield services. Flat or even modestly deteriorating fundamentals off a great year is not a terrible thing.

As for PUMP, the 2022 momentum continued into Q1. From the call:

We believe our first quarter financial performance, the best in over 3 years for adjusted EBITDA margin and net income is a catalyst to improved cash flow generation through the remainder of this year and into the future and is evidence of our new strategy at work.

Now, let's move on to our first quarter financial results. During the first quarter of 2023, we generated $424 million of revenue, a 21% increase from the $349 million generated in the fourth quarter of 2022. This increase was largely attributable to increased utilization, improved net pricing across our service lines, the full quarter effect of Silvertip's revenue contribution and the frac fleet repositioning effort we undertook in the fourth quarter of 2022.

Our effective frac fleet utilization of 15.5 fleets for the first quarter of '23 was at the top end of our prior guidance of 14.5 to 15.5 fleets. We expect steady fleet utilization through the second quarter of '23 . And as Sam mentioned, our frac fleet remains effectively sold out and strategically positioned and committed completions programs with efficient customers who value and appreciate our industry leading field performance. Our guidance for second quarter frac fleet utilization is 15 to 16 fleets with steady activity in our wireline and cementing businesses as well .

The capex is for a good reason

One negative from Q1 at first glance is that PUMP didn't generate free cash flow:

However, I think it is for a good reason as the company is upgrading its fleet . Legacy equipment which runs on diesel is converted to natural gas or fully electric fleets:

ProPetro Q1 Presentation

This is expected to be a differentiator as oil companies are increasingly worried about the carbon footprint of their operations:

We will continue to transition our fleet, although at a slower pace to electric and natural gas burning equipment. This allows us to continue to play and compete at the top end of the bifurcated frac market.

My guess is that in the near future, if you want to serve the giants like PUMP's top customers Exxon and Pioneer, having the new generation fleets will be a prerequisite and should command better pricing. The legacy fleets will probably find more work with private operators who are less sensitive about ESG reporting. I think that, like LBRT, PUMP is doing the right thing through these investments.

Valuation and targets

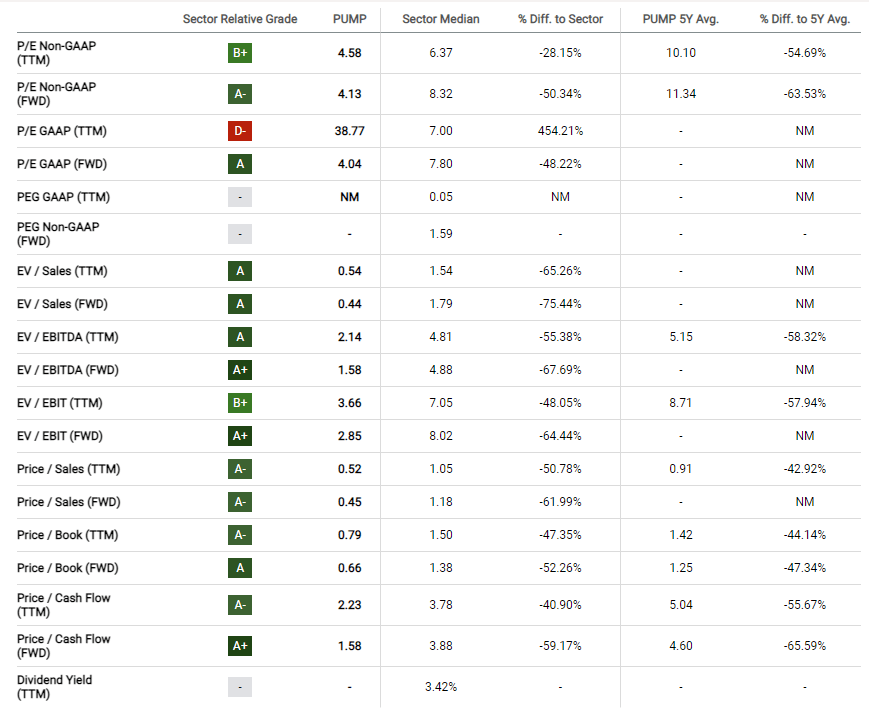

If you are a value-oriented investor, PUMP would be your home turf with a great valuation and terrible momentum. Seeking Alpha's overall valuation score is "A":

{kind=link}

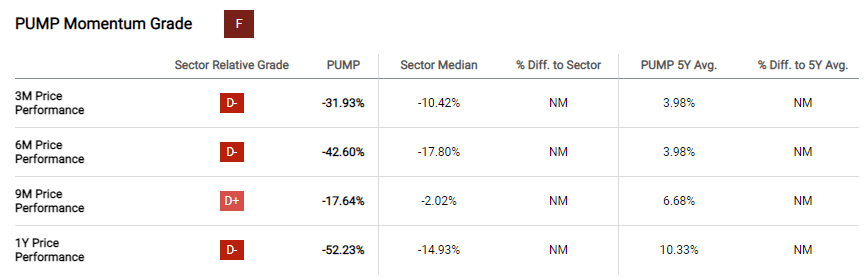

The 1.5x forward EBITDA multiple certainly stands out. Compare of course to the "F" grade on momentum:

{kind=link}

If "not fighting the tape" is your guiding principle, it is probably too early to say if we have already seen the bottom.

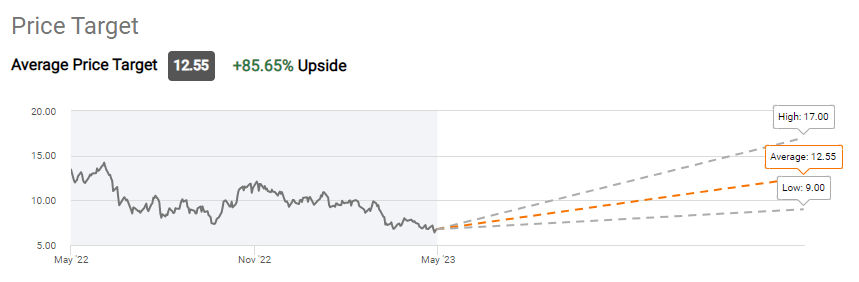

Wall Street thinks the stock may close to double from here:

{kind=link}

At least one professional analyst thinks it could even be a three-bagger with a $17 price target.

Risks and takeaway

Many energy companies, both producers and services providers, filed for bankruptcy in 2020. I would understand investors worried about the coming recession shying away from levered plays. However, ProPetro doesn't have debt, and, without debt, it is hard to go bankrupt.

With bankruptcy off the table, the major risk in my view is further multiple compression. If much of the selling is macro driven, as I think is the case, passive investors may continue reducing their PUMP holdings and that may attract more momentum traders on the short side.

I am managing this risk by limiting the size of my position relative to my overall portfolio, placing some hedges against the broader small-cap universe ( IWM ) and keeping enough cash to buy more if the multiple falls even further. I am also long PUMP's competitor LBRT, based on a similar rationale, and have a smaller position in CFW:CA.

For further details see:

ProPetro: Don't Write Off This Shale Fracker For 2023