TLT - Q1 2024 Stock Market Outlook: Navigating A Minefield Of Risks

2024-01-02 09:59:24 ET

Summary

- Stocks ended 2023 with strong gains, although conditions appear technically overbought with risks tilted to the downside into Q1.

- Several areas of macro uncertainty can drive renewed volatility.

- We share a near-term price target for the S&P 500.

The S&P 500 Index ( SP500 ) closed out 2023 with a spectacular 24% gain in 2023, storming back to a near-record high. The tech-heavy Nasdaq-100 (NDX) fared even better with a 53% return. Compared to the air of pessimism at the start of the year, the backdrop now can be described as a night and day difference.

Despite interest rates climbing to a two-decade high, the U.S. economy managed to remain resilient while inflation cooled sharply lower. Entering 2024, the consensus is that the Fed is on track to cut rates. Indeed, that was our bullish thesis at the end of 2022 where we predicted many of the trends that have played out. Unfortunately, there's not much time for a victory lap.

The problem, as we see it, is that while these factors appear strong, this "soft landing" narrative is already old news. Simply put, anyone turning bullish now is late to the party.

{kind=link}

We'll keep things simple to highlight the two main risks from here that can result in the next big market move being a step lower in Q1 2024.

- Our base case is that economic data will begin to disappoint over the next several months, suggesting a deeper underlying weakness in the economy. Here the risk is that the operating environment and earnings outlook for companies suffer as a headwind for stocks.

- There is also the risk that inflation surprises to the upside, undermining any timetable for the Fed to start cutting rates. In this scenario, renewed volatility in the bond market would likely translate to pressure on equities.

1) Watch For Signs of a Recession

We're a bit concerned about the strength of the economy. The data in recent months has been mixed, with some areas like consumer spending coming in a bit stronger than expected, along with solid labor market trends. On the other hand, there is a sense that the toll of rate hikes since early 2022 is finally catching up with other segments already showing signs of cracking.

Industrial activity indicators and forward-looking surveys including the latest PMI and ISM are objectively weak , pointing to what we believe is a fragile economy. The latest housing market data with pending home sales in December is stuck at a near 22-year low.

The general thinking here is that while these data prints are poor, they also play into an outlook for the CPI to continue trending lower. The market is running with the idea that as the Fed begins to cut rates, possibly as soon as March, this should work as a swooping boost to the economy, curing all ills. We're more skeptical on that point.

In many ways, it's possible bulls and economy optimists are making the same mistake bears and doomers fell for in late 2022. While each rate hike in the cycle didn't "crash" the economy and lead to surging unemployment, as some had predicted, we can flip that around and claim that the rate cuts in 2024 could fail to produce the necessary immediate economic support.

The Fed cutting rates by 5.5% to 4.5%, or lower, and mortgage rates falling by +100 basis points doesn't begin to address what is an already overleveraged consumer that is dealing with affordability challenges in several spending categories.

It's a stretch to suggest a "hard landing" is around the corner, but we'll plant a flag on the hill that the soft landing faces some unexpected turbulence. So when we talk about the possibility of a recession, it's gonna be in terms of a couple quarters of a technical contraction where GDP comes up against what is a high watermark of comparables from 2022.

The way that could begin to transpire would likely start with the labor market rolling over. While non-farm payrolls averaged around 250k jobs added per month in 2023, a few months with a print under 100k or even negative would confirm the shifting environment. Initial and continuing jobless claims are key monitoring points that will identify this key foundation of the economy follower over.

2) Inflation Can Surprise To The Upside

Continuing our theme of what may be a challenging 2024 for investors, let's assume we're flat wrong about a recession and the economy once again emerges stronger than expected.

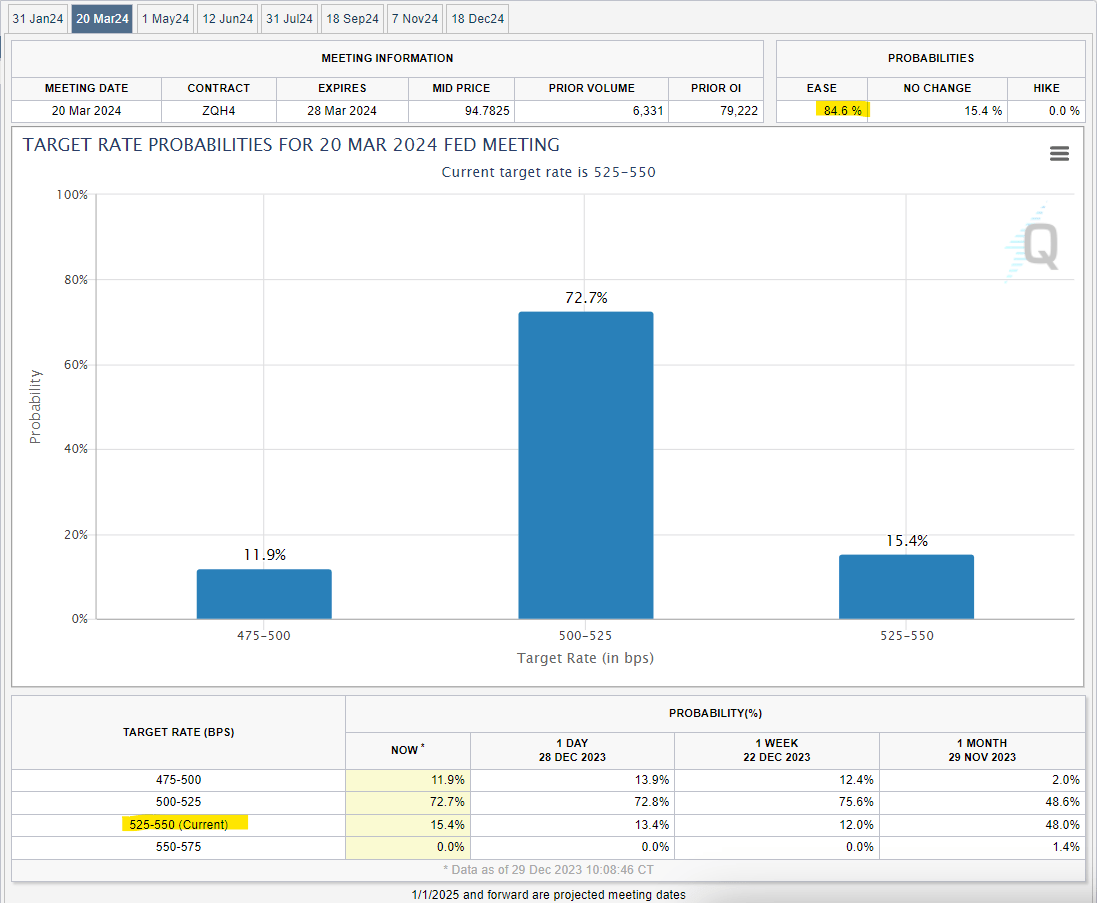

This scenario could also prove to be a different type of headache with the implications it has for how the CPI and inflation expectations will progress. The market appears to be pricing in an 85% chance the Fed will make its first rate cut by the March 20th FOMC. The market is also pricing in around six rate cuts for the year, taking the Fed funds rate down to 4.0% or lower.

We believe this forecast for an initial rate cut within 2 months is very aggressive. without sharply weaker economic hard data over the next two months, which would foreshadow that same recession we alluded to.

If the economy does indeed remain on a firm footing, a new round of inflationary pressures could emerge and jeopardize that final leg lower need to push the CPI towards 2%.

For us, the head-scratcher in 2023 was the trajectory of housing "shelter" prices that remain elevated even as other core goods and services stabilized lower. Fed rate cuts could inadvertently kickstart another leg higher of housing prices that would limit the downside to the headline CPI any further.

{kind=link}

Through the same line of thinking- there is also a case to be made that further strength of economic conditions and even a rebound of global growth should also be supportive of energy and commodity prices.

We've previously covered how the oil selloff in recent months was a "gift" for investors by helping to push lower the CPI since September. A sustained rally higher in energy prices at a time when the Fed is expected to start cutting could introduce volatility to inflation readings over the next few months.

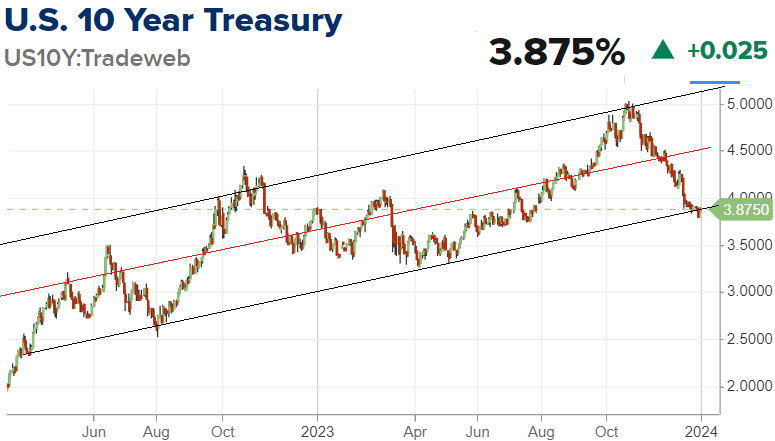

Renewed uncertainties on the pace and sizing of the 2024 Fed rate cuts should be reflected in a spike higher of bond yields. The potential that the 10-year Treasury rate rebounds above 4.0% and towards 4.5% would likely be a bearish headwind toward risk assets.

{kind=link}

3) Lofty Earnings Expectations

Whether the economy rolls over or stubbornly high inflation forces the Fed to push back on rate cut expectations, we believe the 2024 earnings growth estimates are exposed to downside risks.

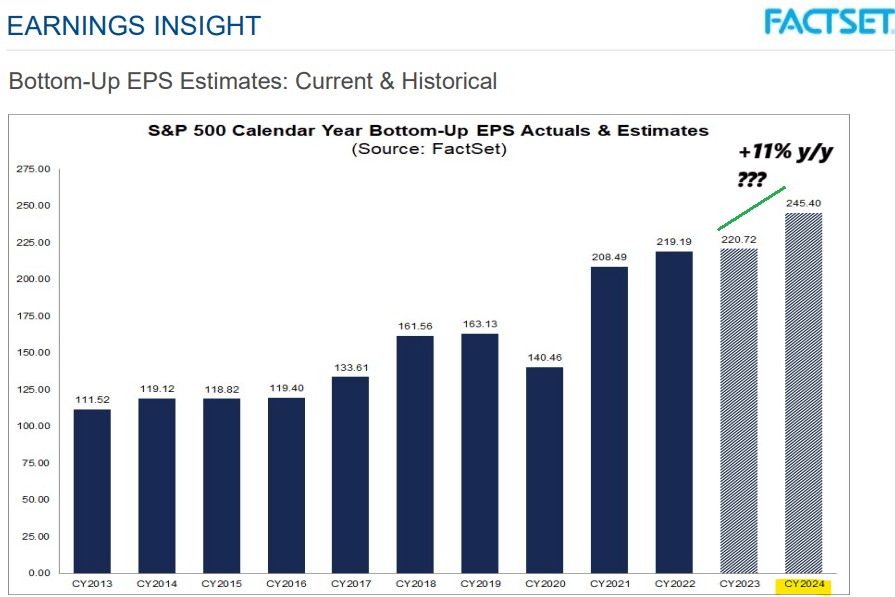

According to consensus bottom-up EPS tracked by FactSet, S&P 500 EPS is expected to reach $245.40 in 2024 , up 11% over 2023 pending the final Q4 results. Either way, our take is that these figures are aggressive benchmarks companies will struggle to achieve.

Keep in mind that one of the stories in 2023 was the ability of companies in general to support margins through "efficiency efforts" and cost-cutting measures as an earnings growth driver. With many of those initiatives already implemented, further margin gains will need to come from top-line momentum.

{kind=link}

From there, the open question is how sensitive earnings will be to potential deviations from the consensus path in the economy and interest rates.

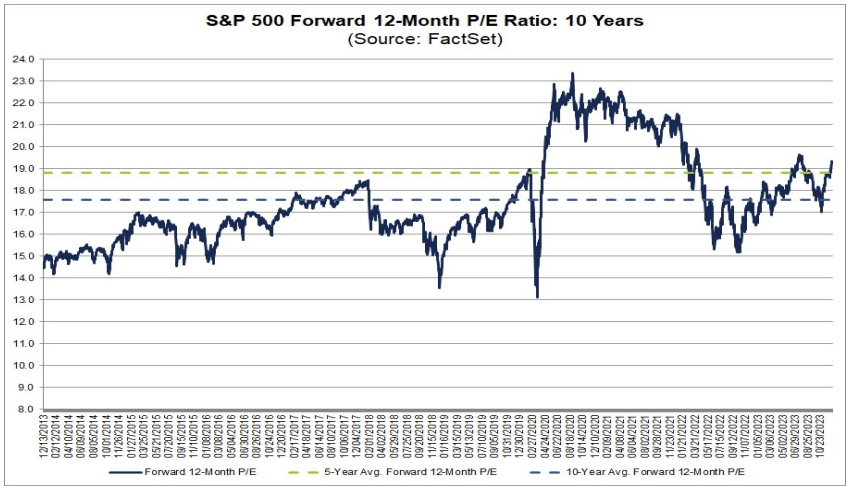

In terms of valuation, the index P/E multiple around 19x is not necessarily at extremely expensive levels but also poses the question of how much more room there is for these earnings multiples to expand, particularly when thinking about the mega-cap tech leaders that have already rallied to incorporate the improved macro backdrop.

{kind=link}

Upcoming Q1 Events To Watch

Overall, there's a lot that can go wrong with various scenarios potentially limiting further upside in stocks. Upcoming macro updates and economic indicators will be critical to setting the stage for the year ahead, either confirming the recent bullish market momentum or forcing another reset of expectations. Lots of lingering questions will need to be addressed.

- Non-Farm Payrolls: Jan 5th/ Feb. 2nd (How strong is the labor market?)

- CPI Updates: Jan 11th/ Feb 13th (Is disinflation ongoing?)

- Retail Sales: Jan 17th (Consumer spending momentum)

- FOMC: Feb 1st (Does Powell signal a March pivot?)

- Q4 Earnings: Big banks start reporting including JPMorgan & Chase Co. ( JPM ) and Wells Fargo & Co ( WFC ) on Jan. 12th (Will earnings and forward guidance match the recent market enthusiasm?)

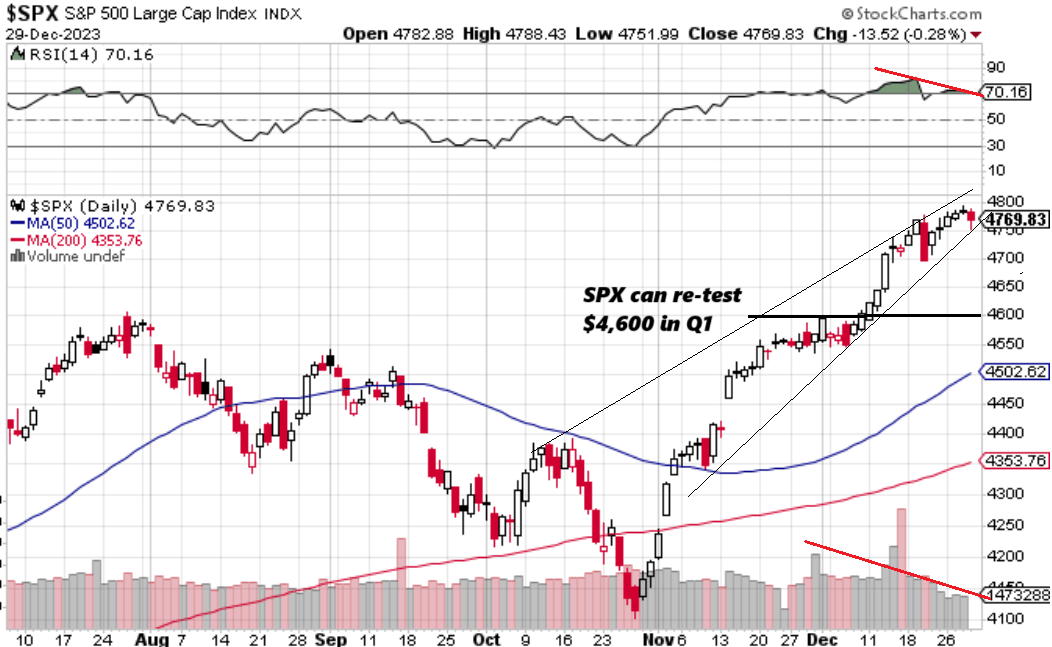

We Expect SPX To Retest $4,600 In Q1

As 2023 becomes a distinct memory, our message is that returns in 2024 will be a lot harder. We still see room for small-caps to perform well compared to mega-caps and also see opportunities in emerging markets, including China in the near term. Gold and precious metals miners are one market segment we believe can shine in 2024.

Our recommendation as the first step in 2024 is to take a defensive approach. The big prediction we have today is that the next move in the S&P 500 may see it retest down to $4,600 as more likely than a ~200 point higher to $5,000.

Into January with the market returning from the quiet holiday period- a closer look at data with some time to reset expectations should translate into rising volatility for equity prices.

{kind=link}

For further details see:

Q1 2024 Stock Market Outlook: Navigating A Minefield Of Risks