CA - Quality Is Aritzia's Trump Card

2023-07-17 14:12:09 ET

Summary

- Aritzia's stock has declined due to increased competition, particularly from fast fashion companies and small businesses replicating their designs on e-commerce platforms.

- The management had plans to defend against competition and return to growth by Q3 2024.

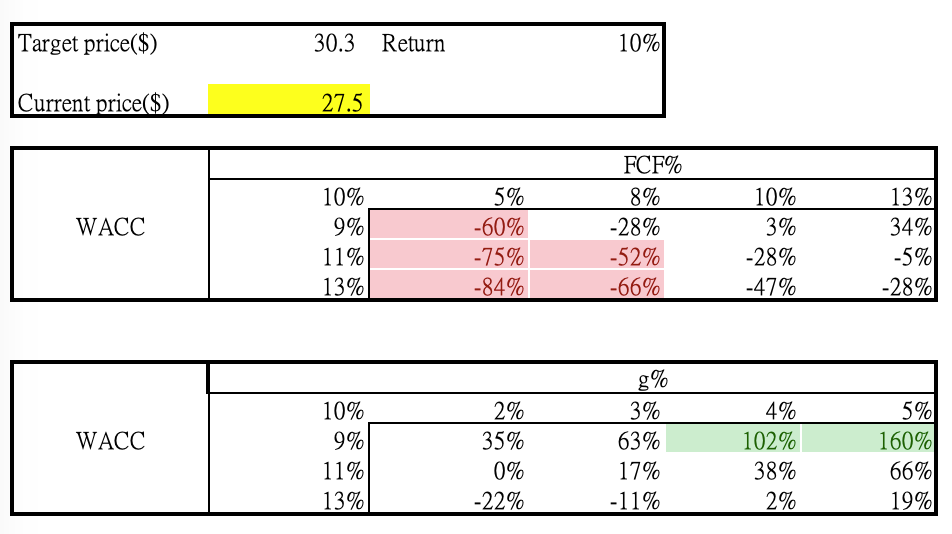

- Our DCF model projects a 38%-66% upside if the plan is implemented and the company resumes its growth trajectory.

Why did the stock go down?

Aritzia (ATZAF) released its Q1 2024 earnings on July 12, resulting in a stock drop of over 20% on that day. The company reported a 13% revenue growth, which is a slowdown compared to the 42% growth in Q4 2023. Additionally, Aritzia expected flat to slightly declining growth in Q2 2024.

We believe the stock drop can be attributed to two factors. Firstly, the deceleration in growth during the quarter, along with a pessimistic outlook due to increased operating costs and a competitive promotional environment. Secondly, there is pressure from competitors impacting the company's performance.

As outlined, the decline was primarily due to the following headwinds; higher product costs, normalized markdowns, temporary warehousing costs and preopening lease amortization for flagship boutiques and our new distribution center. These pressures were partially offset by lower expedited freight costs.

{kind=link}

Seeking Alpha

We believe that the persistent inflation pressures have created a challenging environment for the industry. However, as inflationary pressures gradually ease and the company begins operating its distribution center, the pressure should ease as well. In this article, our focus is on analyzing the competitive pressures.

Competition

Based on our survey of loyal Aritzia customers, articles found online promoting Aritzia replicas , and comments from management, it seems that Aritzia is facing competition, particularly from fast-fashion companies like Shein and small businesses utilizing e-commerce platforms like Amazon. These competitors imitate Aritzia's styles using cheaper fabrics with lower prices, which puts pressure on Aritzia. In essence, Aritzia's products focus more on trendy fashion and lack functionality, resulting in a shallow moat.

Aritzia, established in 1984, is a well-known fashion group in Canada, with over 10 sub-brands and product lines such as WILFRED STUDIO (premium tailoring), BABATON ATELIER (workplace suits), and TNA (athleisure). These brands or lines have distinct focuses and design concepts, but they all fall under the umbrella of minimalist and practical Canadian fashion.

Can fast fashion and online commerce defeat Aritzia?

(1)Quality

According to Aritzia's CEO, the company's answer lies in winning through quality.

As mentioned multiple times before, the quality of our products, including design depth, fabric and material quality, construction quality, and exceptional fit, surpasses that of any competitors out there. We offer all of this at an attainable price point, and I can almost guarantee you that nobody can come close.

Although Aritzia's basic designs are easily imitated, fast-fashion companies often prioritize rapid product turnover and focus solely on imitating style and appearances without fully understanding the design concept. Additionally, due to the need for lower costs and risk mitigation, fast-fashion companies cannot produce as many variations or use high-quality fabrics. By capitalizing on its profound understanding of customers, Aritzia can effectively deliver products that epitomize superior quality without compromising on price.

(2)Product innovation

In a recent earnings conference call, Aritzia's CEO, Jennifer Wong, and CFO, Todd Ingledew, engaged in a captivating discussion that provided valuable insights into the company's competitive strategy. They candidly acknowledged that their excessive focus on existing products over the past two years has hindered their ability to foster new and innovative offerings. Recognizing the need for change, the company has now embarked on a path of developing exciting new products, set to be launched in 2024. By adopting this forward-thinking approach, Aritzia aims to fortify its position in the market, defending itself against competition while simultaneously creating new growth opportunities.

(3)Cost reduction

The company is optimizing the supply chain to achieve cost efficiency across all business areas. They have identified around 150 opportunities that are expected to generate an annual run-rate cost benefit of approximately CAD$60 million starting in the second half of this year.

They also highlighted investments for the future, including expanding infrastructure to match unprecedented growth in 2022 and 2023, as well as laying the foundation for future enhancements such as mobile point of sale and additional omnichannel services.

(4)Expansion of product lines

Aritzia broadened its appeal to men with the recent acquisition of the Reigning Champ brand from CYC Design Corporation.

CYC Design, the parent company of brands like Reigning Champ and the now-closed Wings+Horns, is not only a reputable fabric supplier but also an integral part of the supply chain for ARC'TERYX's wool products. Aritzia's acquisition of CYC Design goes beyond adding a men's sportswear brand to its portfolio; it strategically integrates the fabric supply chain to defend its position.

DCF valuation

We make the following assumptions, coupled with the assumption that the company would grow from CAD$2195 million by 4.5% in 2023 (the midpoint of management's estimate, 2%-7%) and grow 3% thereafter:

- WACC: 11.4%

- Free cash flow margin: The company's free cash flow in FY 2023 declined due to an increase in excess inventory, which grew by 124% during the year. However, the management has taken steps to address this issue by increasing promotions and reducing inventory. As a result, we assume the free cash flow margin to improve and return to the FY2022 level of 14.8% in FY2024. Going forward, we anticipate the company will maintain a similar free cash flow margin.

- Terminal growth rate: 3%

Through the DCF model, we arrived at a CAD $3470 million equity value (CAD$30.3 per share), which is ~10% above the current price.

The company adopted various strategies to defend against competition, and it is expected to return to growth in Q3, 2024. We have confidence in management's strategy, given its competitive advantage in brand awareness and product quality. According to sensitivity testing, the stock has an upside between 38% and 66% if the company reaccelerates and maintains a long-term growth rate of 4% to 5%.

{kind=link}

LEL Investment

Risk

We see the main risks of the stock are inflation and competition. However, we believe that the company's current plans will effectively leverage its brand recognition and quality advantages to regain market share. The company's positioning in the mid-to-high-end market also mitigates the impact of inflation to some extent. Overall, we consider the risks to be limited.

Summary

The management is conscious of the situation it is in and is working on a few efforts to adapt to the effects of the macroeconomic and competitive environment. In general, we support the management team's strategic course.

Our model predicts that the present stock price is 10% undervalued and that once the company accelerates its growth, there may be an upside of 38% to 66%. As a result, we think the current level of the stock price is favorable and advise a buy recommendation.

For further details see:

Quality Is Aritzia's Trump Card