QS - QuantumScape: Not Out Of The Woods But Cautiously Optimistic

2023-11-30 11:35:44 ET

Summary

- QuantumScape Corporation has lost half its value over the last 4 months.

- QS is now well-stocked with cash to manage operations for the next two years.

- The addition of a new production specialist should put QS in a better place and we are already seeing some tenuous benefits.

- The consensus revenue estimates have been trimmed for the next two years, and the valuations still look inordinately pricey despite the correction in the share price.

- The stock appears to have formed a bottom.

Introduction

Early in Q3-23, we had written about QuantumScape Corporation ( QS ), a pre-revenue company that has been attempting to leverage solid-state technology, to mitigate some of the flaws associated with legacy battery tech.

Back then, whilst we were appreciative of some of the outcomes coming out of the Q2 event, we were not too enthused about kickstarting a long position. Four months on, we've seen a few more developments on the operational and financing side (both positive and negative), but most crucially, the stock has also ended up losing over half its value.

Has the pronounced drawdown tilted our stance on QS? Well, it's hard to come out with a definitive answer, and there are certain nuances worth considering that make this a tricky candidate to rate. Broadly, it's safe to say that we're still feeling rather conflicted about the stock, but with a slightly bullish tilt. Here's our read on some of the dominant themes associated with the QS stock.

Follow-On Offering Is Not Ideal, But QS Looks Well-Stocked For The Next Two Years

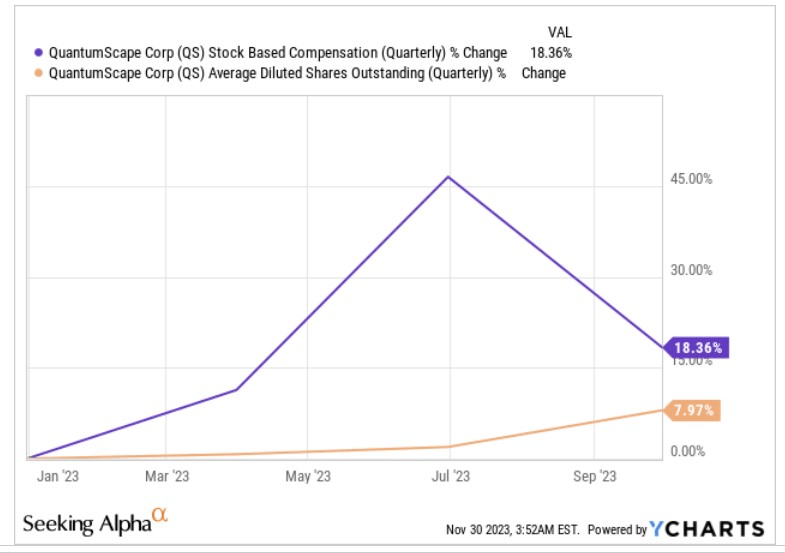

One of the reasons why a lot of investors are wary about QS is on account of its heavy cash burn, and the threat of dilution by follow-on equity raises and increasing chunks of stock-based compensation (SBC). Note that on a YTD basis, the shares outstanding are up by 9%, and there's the looming risk of even further dilution in the future, given a double-digit step-up in the SBC this year.

{kind=link}

Whilst the equity mode of funding is not ideal, investors can take heart from the fact that the worst is probably over, at least over the next two years. In August, QS had ended up raising around $300m via a follow-on offering, and as a result, the liquidity balance which had been sliding for eight straight quarters and had dropped below the $1bn mark in H1, has now reversed and currently stands at over $1.1bn.

What's crucial to note is that management now believes that this will be sufficient enough to supplement their operational requirements all through FY26 . Investors should not play down the importance of QS garnering these funds, as quite a few fledgling EV plays could struggle to raise adequate financing and struggle to kick-on with production, given an adverse shift in funding sentiment towards this space.

Manufacturing Function Could Be In A Better Place

When it comes to the manufacturing side, investors can perhaps also be cautiously optimistic of better dynamics here as the company attempts to step up its volume run rate; in Q3, QS made an important c-suite addition, by hiring the President of Tech at Western Digital - Siva Sivaram, someone who is well-versed in multi-layer advanced semiconductor tech, and someone who has a good track record in scaling advanced tech at high volumes. Sivaram is a production specialist, and it's fair to say we're already seeing some of the benefits from his appointment.

On the Q3 call, he spoke of the need for a higher threshold of automation , amongst other things. Besides implementing the fast-separator heat treat equipment we touched upon previously, QS has also installed some equipment that will scale up process automation linked to unit-cell assembling. As a result, QS could now see the benefits of higher production and better reliability. These automation developments have also likely driven some additional savings on the CAPEX front.

During the Q3 event, CAPEX forecasts for the year were trimmed from previously expected levels of $125m (mid-point of guidance) to $87.5m. Granted most of this is just timing-related shifts, but around one-third of the cut, or around -$13m, was linked to cost-saving efforts, which we'd like to think came from the automation tilt.

All in all, we do think that QS is in better hands with Sivaram coming on board; we expect him to make a difference in ironing out some of the potential roadblocks that could crop up with the volume uplift of the high cathode-loading QSE-5 format cells which are believed to be a lot more complex than the A0 prototype cells which already appear to have demonstrated impressive discharge energy retention compared to other alternatives in the market.

Severe Downward Revisions To Forward Estimates

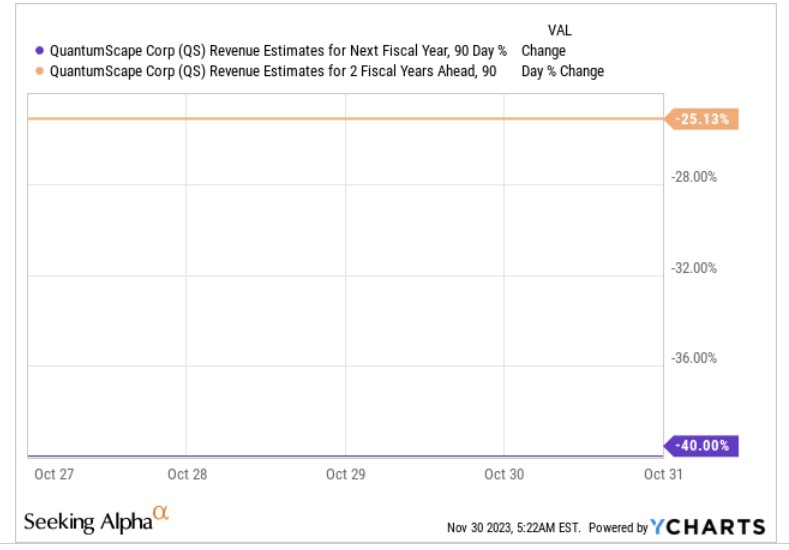

As QS management has been unable to put out any concrete guidance on the expected topline for the next few years, one will have to derive insight from how consensus estimates shift through the quarter. Unfortunately, over the last few periods, the progression of the forward topline expectations hasn't been great.

When we first covered QS back in May 2022 , the expectation was that QuantumScape could potentially be generating annual revenue of $12.5m by the end of FY24. In the periods since there's been a drastic downward adjustment to the numbers; over the last three months in particular, we've seen analysts trim their topline estimates for FY24 by -40% (based on low volume b0 samples from the Raptor system), and the estimates for the following year by -25% (based on high-volume b0 samples from the Cobra system)

{kind=link}

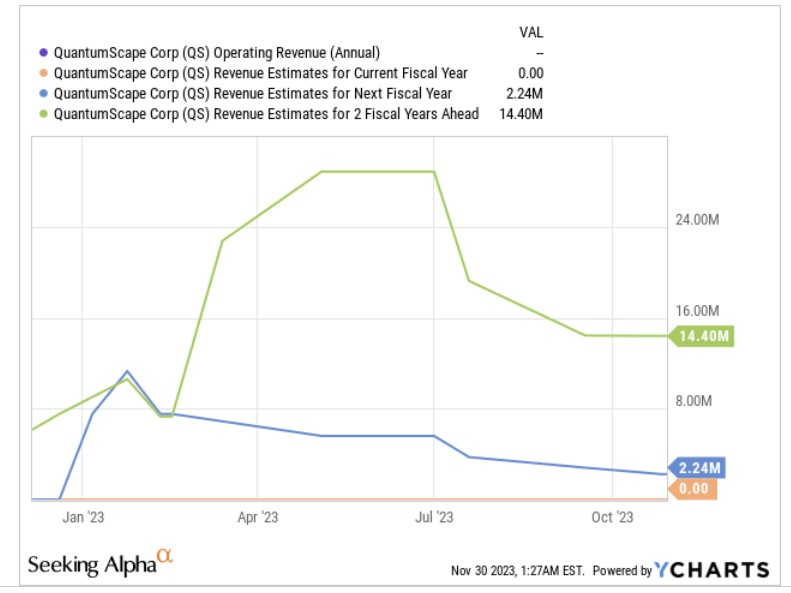

Essentially, now you're only looking at a little over $2m in sales for FY24, followed by a little less than $14.5m in FY25.

Forward Valuations Don't Make A Great Deal Of Sense At This Stage

{kind=link}

Given these lowly numbers, QS's valuation quotient does look quite astounding. Based on a current market-cap of roughly $3000m, you're looking at a business that is priced at a forward P/S of over 200x (based on the FY25 figure)!

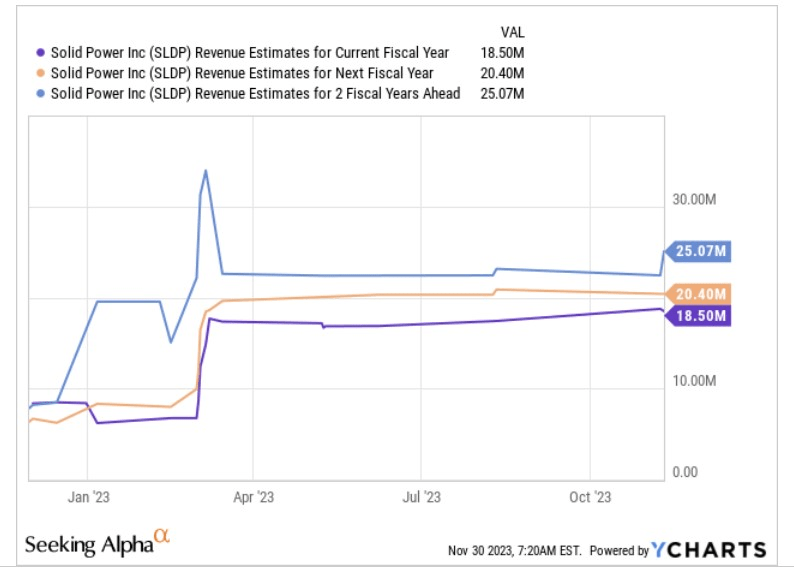

In contrast, consider the competing entity- Solid Power ( SLDP ). This company has its fair share of challenges, but by FY25 it could be generating $25m of topline, yet it is priced a lot more reasonably than QS at 11x price to sales (based on the FY25 numbers).

{kind=link}

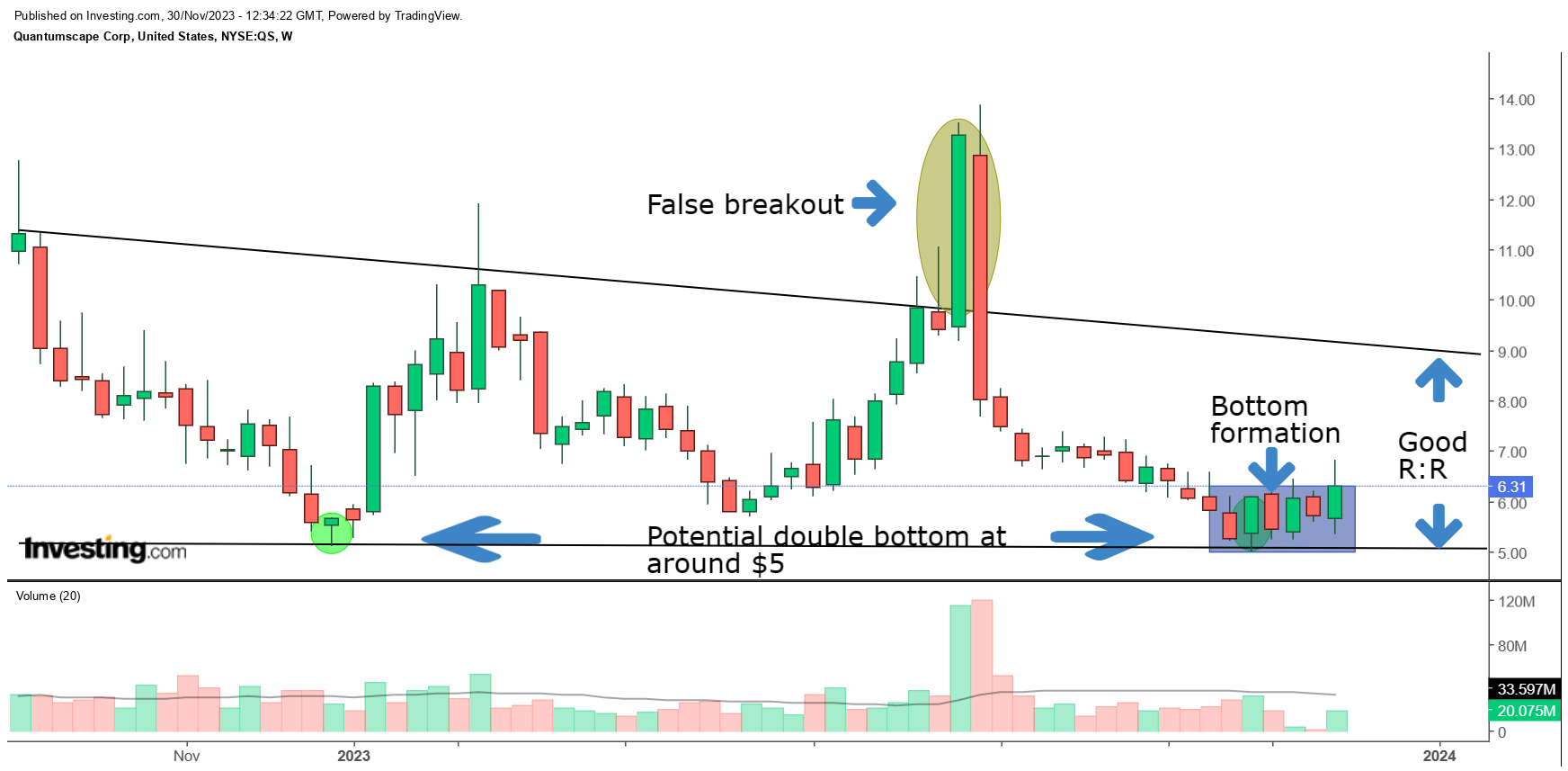

Closing Thoughts - Technical Considerations

When it comes to the charts, we feel a lot better about the risk-reward now than we did back in July. Back then we had advised investors against going long as we had pointed out the risk of additional supply coming into the market capping further upside. Eventually we saw the breakout fail, and since then we've seen a drastic pullback to the lower boundary of the trading range.

{kind=link}

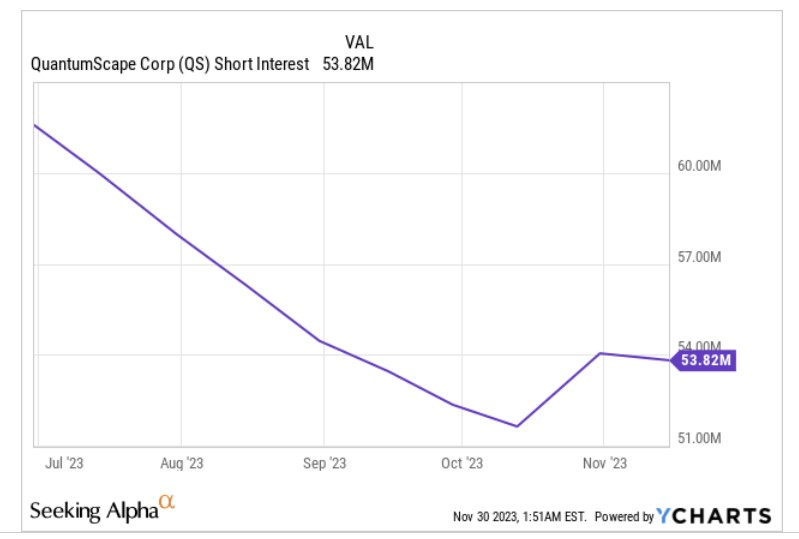

There are a few things that enthuse us at these levels; last month we saw a double bottom at around the $5 level, and since then the price has also shown signs of flattening out, opening up the likelihood of bottom formation. Meanwhile, it also appears that the short-sellers are losing interest, with the short-interest declining by around 13% over the last few months.

{kind=link}

For further details see:

QuantumScape: Not Out Of The Woods, But Cautiously Optimistic