RXT - Rackspace Technology: Wait Until It Proves It Can Execute

Summary

- Execution has been an issue for Rackspace for some time; it needs to show investors it can improve in that area.

- The challenge for the company is, with macroeconomic headwinds it could lead to longer sales cycles which means confirmation of improved execution will take some time.

- A key area to watch will be in regard to its decision to shift its pipeline mix to high-value services.

- A disastrous shut down of its hosted exchange systems in early December could be a major headwind in a company that is struggling to regain trust.

Since Rackspace Technology, Inc. ( RXT ), an operator of multicloud technology services, has been working on rebuilding trust in the company concerning execution, it had the nightmare experience of undergoing a ransomware attack that shut down its hosted exchange service offering.

In its last communication on the company website, it said the incident had been contained with an impact of approximately 1 percent on its total annual revenue. While that may be true based solely upon its current users, what isn't possible to project is the long-term impact from the loss in confidence in the company. Only time can tell what that will be.

As for the company in general, the major thesis of my article is in regard to the execution issues the company has had in the past and the steps management is taking to improve its performance in that area.

One potentially interesting outcome of the ransomware attack is it could accelerate the company's decision to focus on shifting its product mix to higher value services, which many of the customers affected by the attack have been doing.

Concerning the macro-economic headwinds the company faces, it could lead to longer sales cycles according to management, which would push out some of its revenue and earnings.

Combined with the loss in revenue from the ransomware attack and unknown impact on its overall business, along with uncertainty from the expected challenging year ahead, RXT could be in for a tough year ahead.

In this article we'll look at how the company has been performing recently, the steps it's taking to improve execution, and how it is likely to do in 2023.

{kind=link}

Recent numbers

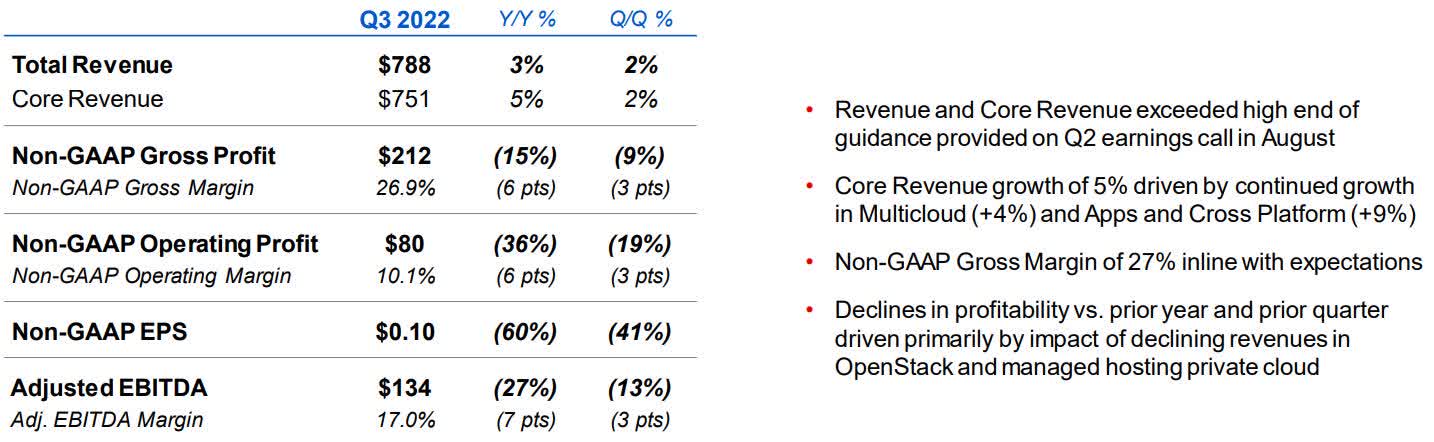

One of the strong areas of the company is its ability to generate revenue, which in the third quarter of 2022 came in at $788 million, up 3 percent year-over-year. The company guided for revenue in Q4 to be around $772 million to $782 million.

Gross profit in the reporting period was $212 million, down 15 percent from the third quarter of 2021. Gross margin in the third quarter was 26.9 percent.

Operating profit in the quarter was $80 million, down 36 percent from the third quarter of 2021. Operating margin was 10.1 percent. Operating profit in the fourth quarter of 2022 is projected to be from $65 million to $69 million.

{kind=link}

Adjusted EBITDA was $134 million, down 27 percent, with earnings per share of $0.10, down 60 percent year-over-year. Earnings per share for Q4 is estimated to be from $0.4 to $0.06. With profit metrics guided to be down, when including the fallout from the ransomware attack, it's likely to be worse than originally thought.

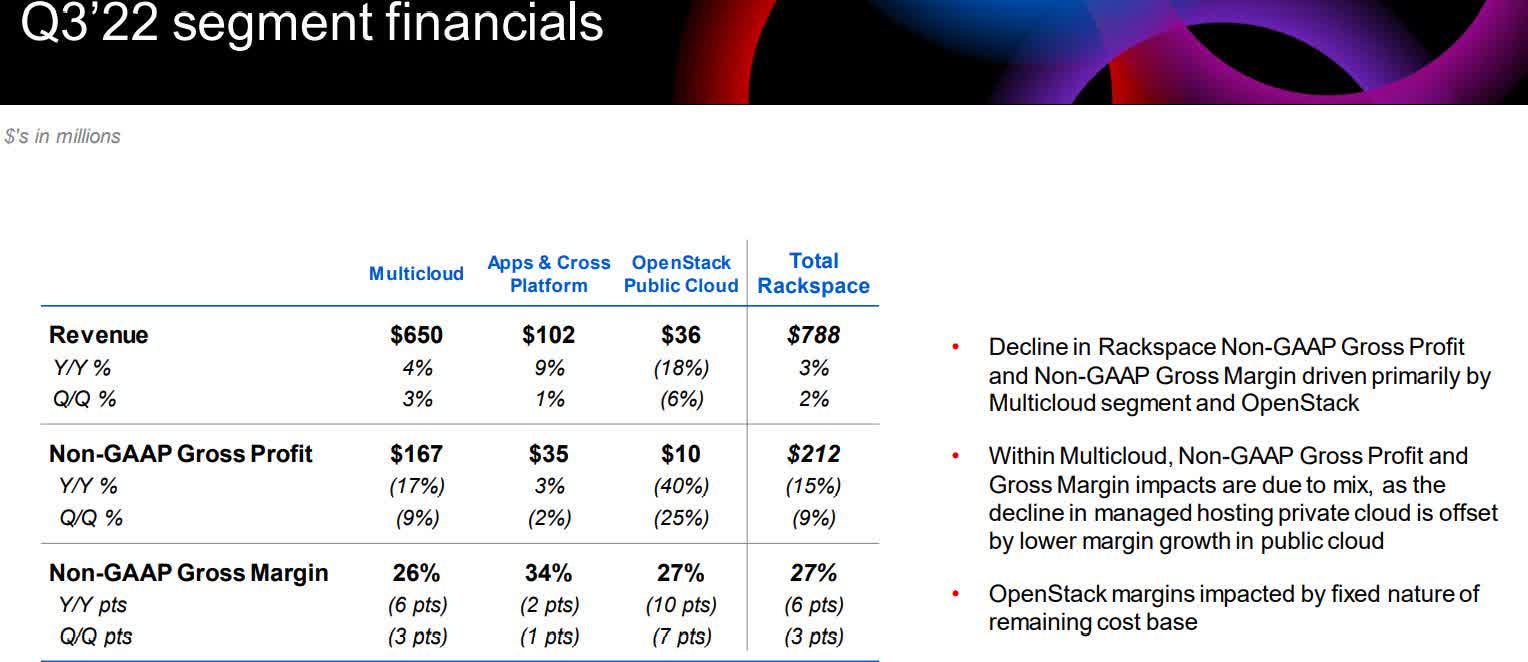

The plunge in profitability measured against the third quarter of 2021 was from falling revenues in OpenStack and managed hosting private cloud, but all its segments were negative in the third quarter of 2022 in gross margin and gross profit.

Free cash flow has also been a strength for RXT, and that continued on the third quarter with it reaching $52 million in the reporting period.

Cash and cash equivalents at the end of the quarter were $249 million, with $375 million undrawn from its revolving credit facility. The company holds total debt of $3.4 billion.

While the company has refinanced its debt to 2028, it still has to pay over $50 million in interest on a quarterly basis, and that's going to get worse as the Federal Reserve continues to raise interest rates. Also, $2.3 billion of its debt is at floating rates. On its term loan it pays approximately $5.75 million per quarter.

{kind=link}

Strategy for profitability

As the company has rightly stated, demand across its multi-cloud offerings continue to be strong but executing on that opportunity remains a challenge. The problem isn't getting business or generating revenue, the problem is doing it at a profit.

So, while it's competing in a high-growth sector, it has to take steps to improve margin and earnings in order to take the company to the next level. The reason it's able to produce a lot of cash flow is because of recurring revenue, but to leverage that it must improve its product mix in order to sustainably improve its bottom line. If and when it's able to do so the company's share price should take off.

{kind=link}

Taking that into consideration, the strategy of the company is to launch services that are "value-added and operationally scalable."

The company wants to move beyond infrastructure resale to providing high-value solutions in the public cloud that generates deeper engagement from its customers.

With management stating it wants to emerge from 2023 with a public cloud organization that targets opportunities with high value, it suggests it's going to take at least a year to transition to that operating model.

It also sees its hosted private cloud business as being underestimated at this time, with a lot of opportunity for growth lying ahead of it. Management estimates that more than 60 percent of workloads are currently in customer data centers. Over the next several years it sees a lot of them moving to the public cloud or hosted private cloud based upon better pricing options, among other advantages. Some of the workloads it sees as benefitting from the hosted private cloud are data-intensive workloads, legacy applications that are cost-prohibitive to restructure on the public cloud, and regulated sectors such as government and health. RXT believes it is strongly positioned to win in the hosted private cloud sector because of it being a "well-known brand with deep experience in private cloud, a global data center footprint, cutting-edge technology and IP and strong partnerships with key ecosystem players such as Dell and VMware." The company acknowledges it's in the early stage of reversing the declines in its managed hosting and private cloud business and knows it's a multi-year project that will take time to bear sustainable fruit. Another area the company is exploring is in customized private cloud offerings in different verticals. It's already making progress in that initiative in healthcare.

Lastly, the company noted it has started working with its existing customers to help them accelerate their transition to the private cloud of RXT.

All of these things combined to have the potential to improve margin and the bottom line of the company, but as mentioned in the article, it must prove it can execute on its strategy while improving earnings.

Conclusion

As of now, RXT is a mixed bag. Its recurring revenue base is approximately 90 percent, with over half of the customer base consisting of Fortune 100 companies. It also appears to have strong relationships with these and other companies otherwise the level of recurring revenue wouldn't be so high. The challenge for the company is to move away from growth at any costs and improve the services it offers by adding value to its customers and potential customers. It will have to do so while starting to lower its debt level, which is very high. With the recent ransomware attack on the company and the immediate loss of revenue, along with the negative news coverage that gave it a black eye, it's not going to help generate trust in the near term.

On the other hand, it did accelerate the process of transitioning to its hosted cloud business, which over time should be a benefit to the company. The question as to how much business it lost beyond the initial disruption has yet to be clarified. We should see that in the next earnings report.

As the company stands today, its share price at close to 52-week lows, I think there's still a lot of risk in the company, and until it proves via its performance it can execute successfully on its plan to grow revenue while improving earnings, I think it's a risky gamble.

For further details see:

Rackspace Technology: Wait Until It Proves It Can Execute