RLYB - Rallybio: Gearing Up To Be An Opportunity

2023-09-15 17:15:40 ET

Summary

- Rallybio has proof of concept data from two more assets, RLYB211 and RLYB116, in addition to their lead asset RLYB212.

- RLYB212 demonstrated rapid and complete elimination of transfused platelets in patients, while RLYB116 showed a reduction in Free C5 greater than 99%.

- The company has a cash balance of $138mn and a cash runway of approximately 6 quarters.

When I first covered Rallybio ( RLYB ) six months back, they just announced phase 1b proof of concept data from lead asset RLYB212 targeting ultra rare disease FNAIT or Fetal and neonatal alloimmune thrombocytopenia. 6 months later, they now have proof of concept data from two more assets. One of these is RLYB211, which is a precursor molecule of RLYB212. Their difference is that 212 is a subcutaneous injection, while 211 is intravenous - other than that, they are both HPA-1a targeting antibodies (211 is polyclonal, 212 is monoclonal). The other one is from RLYB116, their second asset. However, the stock, after nearly doubling at one point, has now settled down to where it was last time - prompting the question, is this partially derisked stock an opportunity?

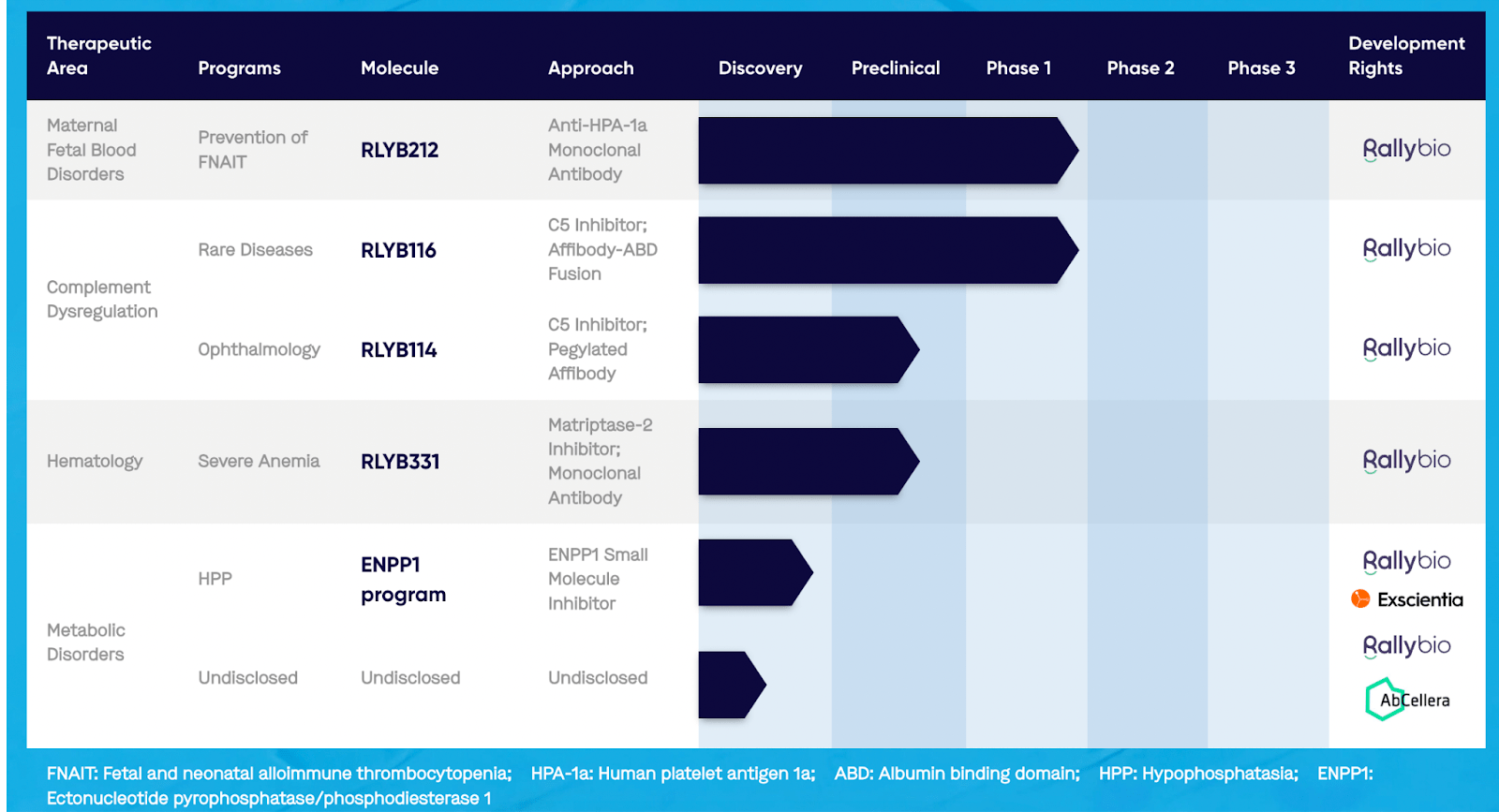

In that earlier article, we checked out RLYB’s diverse pipeline targeting rare diseases. The pipeline looks like this:

{kind=link}

Lead asset is RLYB212, an anti-HPA-1a mAb targeting FNAIT in phase 1 trials. In that last article, I discussed the disease etiology, mechanism of action, and market potential. I also noted that there are “...no approved treatments and the only option is platelet transfusion.”

Preclinical testing was done in a precursor molecule called RLYB211, as well as in RLYB212, both of which reported positive data. Clinical trials were shifted to RLYB212, whose proof of concept data I discussed. A single subcutaneous dose of RLYB212 eliminated transfused, HPA-1a positive platelets in HPA-1a negative subjects within one week after dosing. This was where we stood vis-a-vis the company.

In March, after this positive data, the company decided to permanently shelve 211 for 212. Despite that, though, they published data from 211 in April, from a trial that had been obviously begun before this decision to shelve it was taken. The trial focused on elimination of infused HPA-1a, whose validity as a surrogate endpoint was argued in this way:

As has been shown with anti-D prophylactic agents, the ability of RLYB211 to drive the rapid and complete elimination of antigen positive cells is a surrogate indicator of its potential to prevent maternal alloimmunization, and therefore FNAIT.

Data was published in the Journal of Thrombosis and Haemostasis, the official journal of the International Society on Thrombosis and Haemostasis, which stated:

-

RLYB211 accelerated the elimination of HPA-1a positive platelets versus placebo, with all subjects meeting proof-of-concept criteria for greater than 90% reduction in platelet elimination half-life compared to placebo.

-

Rapid elimination of transfused platelets was evident 7 days after RLYB211 administration, simulating prophylactic administration of an anti-HPA-1a antibody prior to a fetal-maternal bleed.

-

RLYB211 was well tolerated and no serious adverse events were reported.

While 211 is shelved, the company indicates that since its mechanism of action is similar to 212’s, that certain parallels could be drawn from this data on to 212. However that may be, since 212 is now independently producing data and will soon be in a registrational study, these parallels are redundant.

In June, again, updated proof of concept data from RLYB212 was presented at the 31st Congress of the International Society on Thrombosis and Haemostasis (ISTH). Data was from 11 adult male patients of all age groups. Data showed:

-

RLYB212 demonstrated a dose-dependent, rapid and complete elimination of transfused HPA-1a positive platelets in HPA-1a negative subjects.

-

Mean platelet elimination half-life was 5.8 hours (0.09mg) and 1.5 hours (0.29mg) for RLYB212 compared to 71.7 hours for placebo, meeting the study’s prespecified criteria for proof-of-concept in both dose groups (? 90% reduction in mean platelet elimination half-life).

The rapidity and near complete elimination of HPA-1a positive platelets is very impressive. There were no surprises with the tox profile as well. All in all, a very successful PoC trial. They will do a confirmatory phase 2 trial and then a registrational trial.

RLYB116 is their second asset, a long acting C5 complement inhibitor. It is a novel antibody mimetic fusion protein with an albumin-binding domain. It can be self-delivered by an autoinjector. Earlier this month, the company reported data from a phase 1b proof of concept trial of 116 in healthy volunteers. Data showed the following:

-- First-In-Human Single Ascending Dose Clinical Data for RLYB116 Demonstrated a Reduction in Free C5 Greater than 99% at 24 Hours for the 100 mg dose and at 12, 24, and 72 Hours for the 300 mg dose in Healthy Participants --

-- Mean Estimated Elimination Half-Life for RLYB116 was > 300 Hours --

-- No Severe or Serious Adverse Events with Single-Dose Administration of RLYB116 --

C5 inhibition has potential benefit in complement-driven inflammatory diseases. Rallybio’s team is especially suited for this line of approach because of their past work at Alexion, which developed soliris, perhaps the most well-known C5 inhibitor. Besides soliris, the other approved C5 inhibitor is Ultomiris. These are, of course, blockbuster drugs; seeing their success, a number of next generation C5 inhibitors are being run through clinical trials. These include crovalimab and nomacopan.

Financials

RLYB has a market cap of $210mn and a cash balance of $138mn. R&D expenses were $13.1 million for the second quarter of 2023, while G&A expenses were $7.0 million. At that rate, they have a cash runway of some 6 quarters.

RLYB stock is mostly held by PE/VC firms and institutions, with the retail public holding a few percentage points of shares. Key holders are Viking Global, 5AM and New Leaf. Insider transactions are a mix of buys and sells.

The company has an in-license deal with Sanofi for $3mn which they signed last year to acquire an early stage molecule. They have a 50-50 joint partnership with R&D focused AbCellera for discovery stage programs. Late stage assets are self owned.

Risks

RLYB is sort of early stage so their cash runway is probably not going to be enough to see them through an approval. The company does not have major outgoing big pharma deals. Their registrational data is also a year or more away, so the stock is not going to be a quick gainer.

Bottom Line

I like RLYB. I liked them last time as well. They have proven to be reliable and steady, and there have been no nasty surprises till date. I think this is gearing up in such a way as to induce me to take a pilot position soon. Stay tuned.

For further details see:

Rallybio: Gearing Up To Be An Opportunity