RTX - Raytheon: 3 Compelling Reasons To Be A Buyer

Summary

- Raytheon is benefiting from rapid demand growth in all of its segments. Commercial aerospace is recovering, while defense demand is picking up due to higher spending.

- 2022 will continue to struggle with supply chains. However, going into 2023, these issues are fading, providing RTX with the chance to boost output.

- Free cash flow is expected to remain high, supporting improving dividends and buybacks after 2022.

Introduction

We need to talk about Raytheon Technologies ( RTX ), a company I added to my long-term dividend growth portfolio in 2020 after the merger between Raytheon and United Technologies. I have frequently covered RTX, focusing on the benefits that come with holding the company as a vehicle for dividend growth. In this article, we're also going to do that. However, as Raytheon just released its earnings, there's more to discuss. Raytheon is now seeing strong demand in all segments, which is set to boost profitability and related financial indicators after 2022. Commercial demand is rebounding, led by very strong traffic in the US. Meanwhile, the war in Ukraine and general defense needs are boosting the company's already high order book value. Moreover, the company is still suffering from supply chain issues, hurting its 2022 revenue expectations, which I expect to fade quite significantly going into next year.

While the RTX ticker is somewhat struggling due to bad market sentiment, I believe that buying on weakness is the way to go. 2022 is tough, but I see no way around significant long-term outperformance.

FINVIZ

Let's dive into the details!

Demand Is Back

Throughout this article, we're going to discuss the company's latest earnings, which I believe were extremely bullish - even though the headline numbers did not suggest that.

Raytheon generated $17 billion in sales in its third quarter. The defense giant missed analyst estimates by $250 million, which is quite significant. However, it reported adjusted earnings per share of $1.21, beating estimates by $0.07.

As the graph below shows, the company has beaten estimates quite consistently in the past few quarters - despite ongoing headwinds consisting of commercial weakness and supply chain issues.

Seeking Alpha

With that said, commercial weakness is becoming a thing of the past.

In 2021, commercial sales accounted for roughly 48% of Raytheon's total sales. Commercial exposure comes from the company's Collins Aerospace and Pratt & Whitney segments. Collins builds almost everything one can think of, ranging from wheels and airplane toilets to high-tech applications, connectivity solutions, cargo systems, aerostructures, flight deck applications, training hardware, and power control. Pratt & Whitney builds engines for a wide range of airplanes - mainly single-aisle jets used for short-haul transportation.

Needless to say, the pandemic took its toll, pressuring commercial sales as manufacturers stopped ordering new inventory.

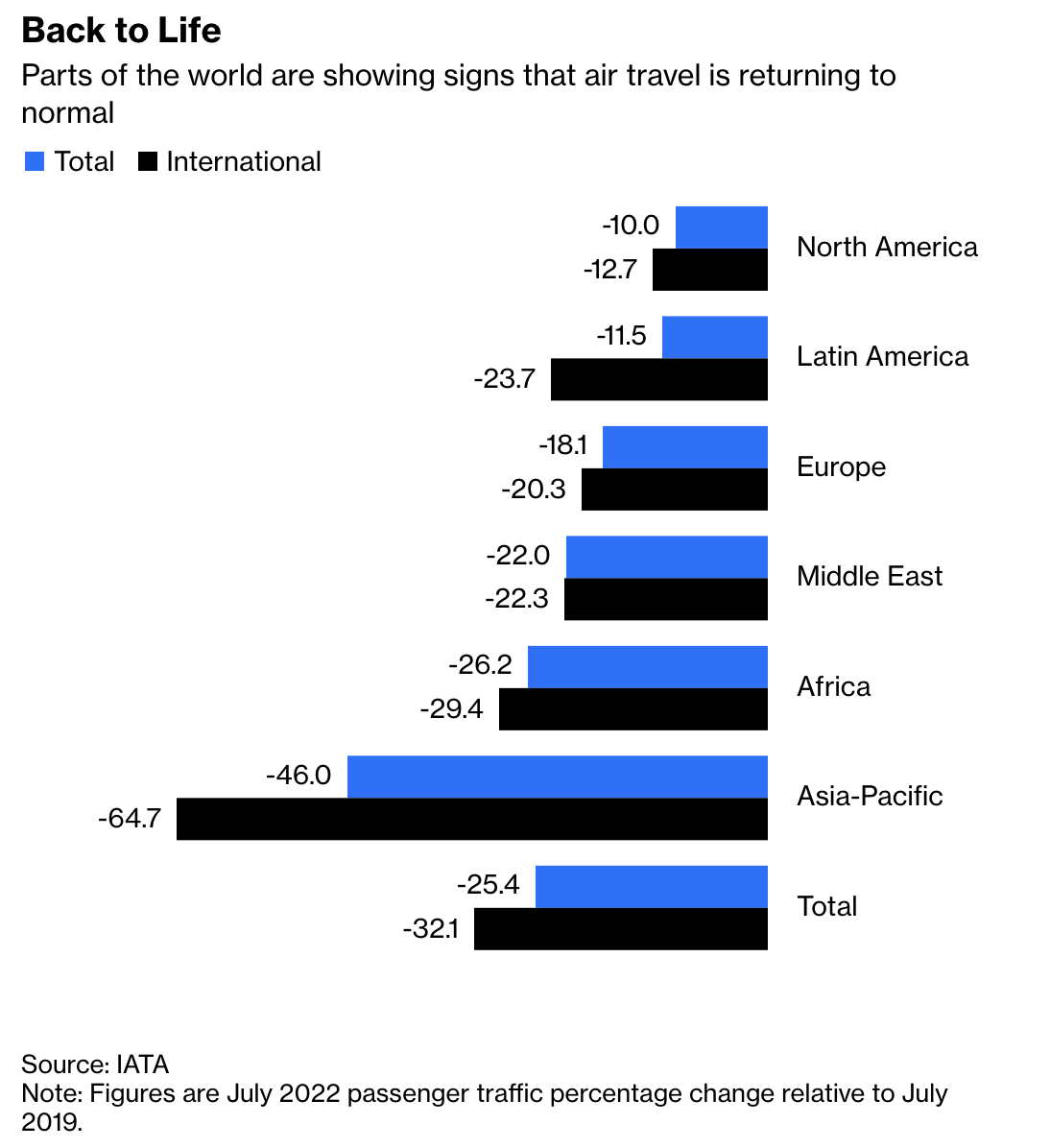

This ye ar's summer traffic numbers were still horrible compared to pre-pandemic levels (the summer of 2019). While North America was the leader with a 10% domestic decline, Europe was down 18%, with traffic in China falling 46%. China is underperforming due to its zero-COVID policy, which will keep a lid on demand until further notice from the CCP. Also, note that international demand is weaker than domestic demand. This, too, is a result of the pandemic. It mainly hurts wide-body demand. This benefits Pratt & Whitney, which mainly focuses on narrow-body airplanes.

{kind=link}

With that said, good times are arriving as producers are ordering products again.

Collins Aerospace reported 11% revenue growth in 3Q22, to $5.1 billion. Organic sales (meaning adjusted for M&A) were up 13%. Commercial aftermarket sales were up 25% Commercial OE (original equipment) was up 16%.

Pratt & Whitney did $5.4 billion in sales, growing sales by 14%. Organic growth in this segment came in at 15%. Commercial OE sales were up 26% with aftermarket sales coming in at 23%.

Note that these numbers don't add up as the average growth rate is way lower than OE and aftermarket sales growth. That difference is caused by defense sales. We'll get to that later.

These results were supported by further growth in commercial aerospace. According to Raytheon, global revenue passenger miles reached 75% of 2019 levels in 3Q22. I was pleasantly surprised as this includes both long- and short-haul and countries depending on Chinese travel.

TSA checkpoints in the US reached 91% of 2019 levels with Labor Day traffic exceeding 2019. In other words, the US is once again leading the uptrend.

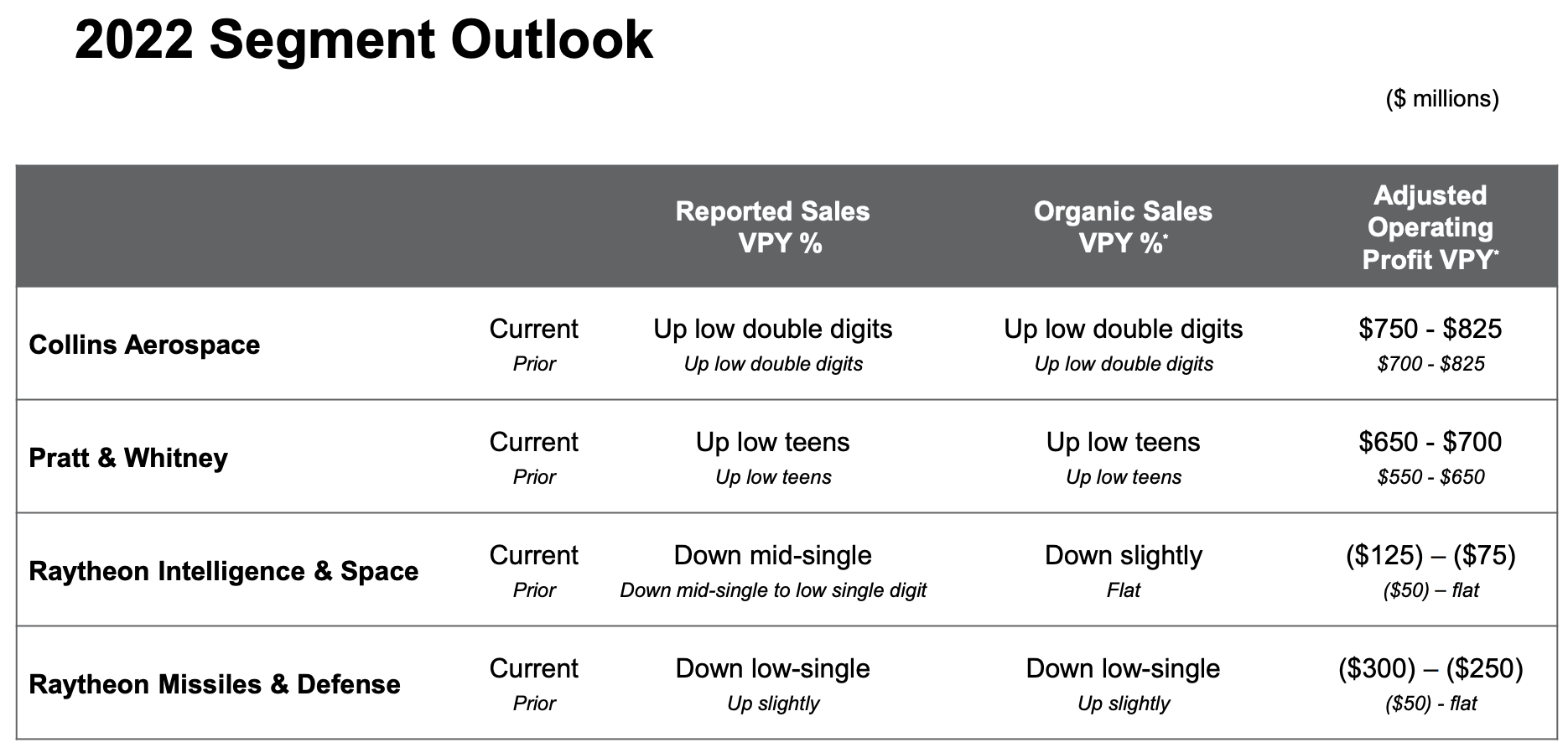

These numbers caused the company to hike the Collins outlook. It now sees an adjusted operating profit rate of $750-$825 million, up from the prior $700 million to $825 million range. It's not that big of an improvement, but what matters is that global aerospace is recovering nicely.

Raytheon also hiked Pratt & Whitney's outlook. It now sees an operating profit of at least $650 million, up from $550 million.

{kind=link}

Now, with that said, the performance in defense segments was different. As the table above shows, the company's defense-focused segments RIS and RMD got revenue and adjusted operating profit revisions - to the downside.

Intelligence & Space saw 2% organic sales growth. Missiles & Defense saw a 5% organic sales contraction. Pratt & Whitney's defense sales were down 2%. Defense (or, "Military" as RTX calls it) sales in the Collins segment were down 6%.

This is the result of one thing: supply chain headwinds.

The demand side was actually quite good. In the case of defense giants like Raytheon, that doesn't translate to higher sales immediately because it takes time to turn backlog into finished products.

Raytheon is now sitting on a $168 billion backlog, which is rapidly rising due to global geopolitical developments - like the war in Ukraine. These developments are a reason for defense partners (i.e., NATO) to rethink their strategies. Especially when it comes to equipment procuration.

For example, as I wrote in a recent article covering Raytheon's peer Lockheed Martin ( LMT ), Ukraine is getting defense support worth $9 billion with another $14 billion earmarked for the replenishment of US equipment. Moreover, US allies have increased their funding plans by $60 billion.

Raytheon, which produces the engines of Lockheed's F-35 fighter is seeing higher demand as a result of strong F-35 sales. Switzerland, for example, ordered 36 new jets. A fun fact is that Raytheon recently delivered the 1,000th F-135 engine - that's the name of the F-35's engine.

Moreover, the company is selling two surface-to-air missile systems (NASAMS) to Ukraine, with orders for two more.

{kind=link}

The company also got a $1 billion award to develop the Hypersonic Attack Cruise Missile for the US Air Force. It also got $1 billion for advanced AMRAAMs, which are air-to-air missiles.

Compared to the second quarter, the company's defense backlog grew by $2 billion, putting the book-to-bill ratio at 1.22. What this means is that orders are rising faster than RTX can turn backlog into sales - that's indicative of future sales growth.

So, to sum this up, Raytheon was awarded more than $22 billion in 3Q22, putting its total book-to-bill ratio at 1.32, which I believe is absolutely terrific, and a confirmation of the commercial rebound on top of accelerating defense demand.

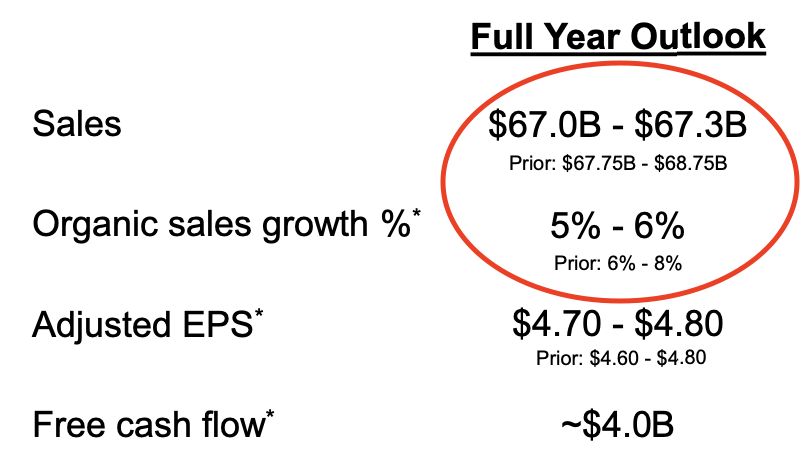

Unfortunately, the company had to adjust its sales guidance for the aforementioned reasons: it has supply chain issues. Luckily, the company maintained its EPS and free cash flow outlook.

{kind=link}

This brings me to the second benefit: supply chains.

Supply Issues: It's Getting Better

Since 2020, aerospace & defense earnings were dominated by supply chain comments - almost all of them were negative. That's basically why I was able to make Lockheed Martin my largest position as I aggressively bought after disappointing earning calls.

While all companies suffer from supply chain issues in some way, aerospace companies are among the biggest "sufferers". Not only does labor play a major role in the development and production of major programs, but companies in this industry also rely on high-tech materials and supplies like semiconductors and related electronics.

Hence, when CEO Greg Hayes discussed the company's great demand environment, he had to highlight that everything was still impacted by supply issues:

[...] notwithstanding the strength in demand that we're seeing across our businesses, the industry-wide challenges we're facing remain the same. You've heard me talk about them before: supply chain, labor, and inflation.

The good news is that these issues are slowly fading, turning into a tailwind.

More than two years after the start of the pandemic, companies have adjusted. Production of key materials and components has been increased. Moreover, economic growth expectations are down as we're headed for a recession in the US and Europe - to name two key markets for aerospace components.

What this does is that it lowers competition for electronic components. While Raytheon and its peers will be in a good spot to boost production (despite a recession), non-defense and non-aerospace peers will likely reduce their orders, causing demand to fall.

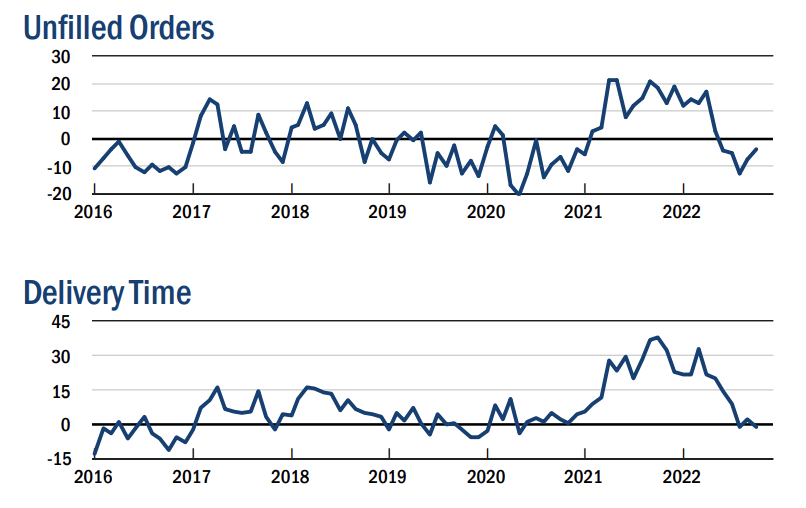

For example, using New York Fed data, delivery times have come down from all-time highs in 2021 to contraction territory. The same goes for unfilled orders, which have been contracting for a while now.

{kind=link}

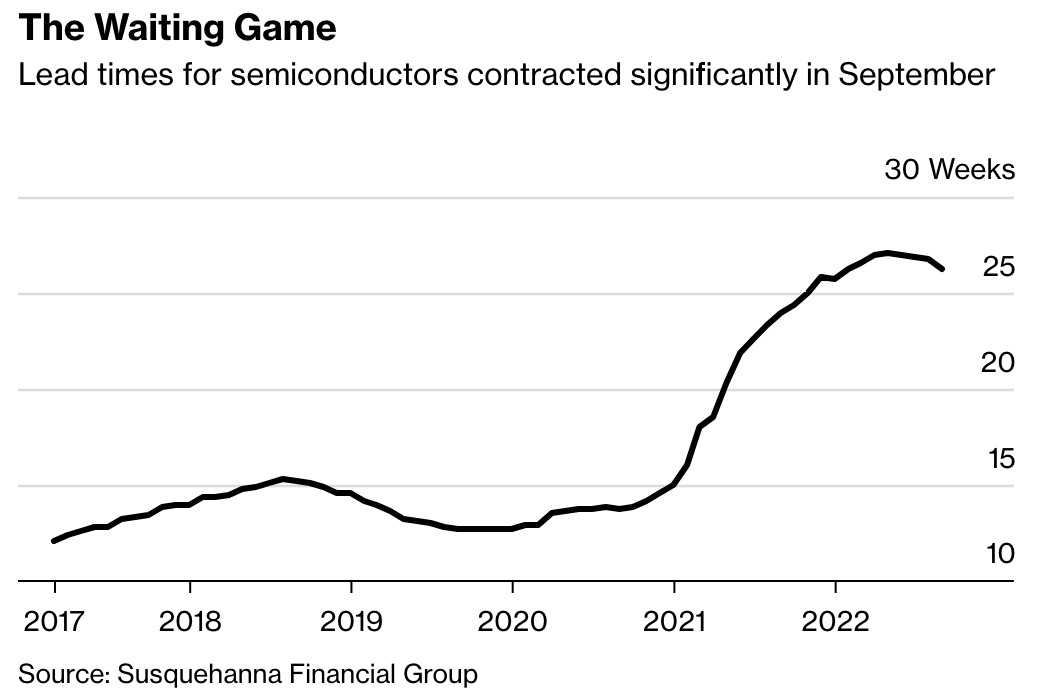

The same goes for one of the most important indicators since 2020: semiconductor lead times. The gap between when a chip is ordered and when it's delivered has come down to 26.3 weeks. That's down from 27 weeks earlier this month.

{kind=link}

The reason why lead times are coming down is based on lower demand .

A sales slowdown in certain markets, such as personal computers, has left Intel Corp. and Advanced Micro Devices Inc. with less demand than expected. AMD’s third-quarter sales missed projections by more than $1 billion earlier this month, and Intel is poised to cut jobs to cope with the slump.

Raytheon has 13,000 suppliers. First of all, a number this big is why government investments in defense in times of economic turmoil support hundreds of thousands of jobs. Second of all, dealing with this many suppliers is tough. As of 3Q22, roughly 400 suppliers are a problem for Raytheon. The company has deployed additional teams to deal with these suppliers on a daily basis, to support them in getting the raw materials they need.

That's the pinnacle of buyer/supplier relations as it makes Raytheon a preferred customer of the most critical suppliers, supporting them in times when suppliers need to choose between buyers.

Moreover, so far, the company has hired 27,000 people in 2022. However, it needs 10,000 more employees. While challenges persist, labor availability is getting better. Note, in this situation, the company also benefits when the economy "tanks" as labor becomes more available.

While these issues are still sticky, the trend is in favor of Raytheon. According to Greg Hayes:

And while supply chain disruptions are frustrating, we are seeing some stabilization, and we're encouraged by the demand signals across the business.

So Much Cash

Yes, reason three is connected to the reason you're holding RTX shares in your portfolio - I'm assuming.

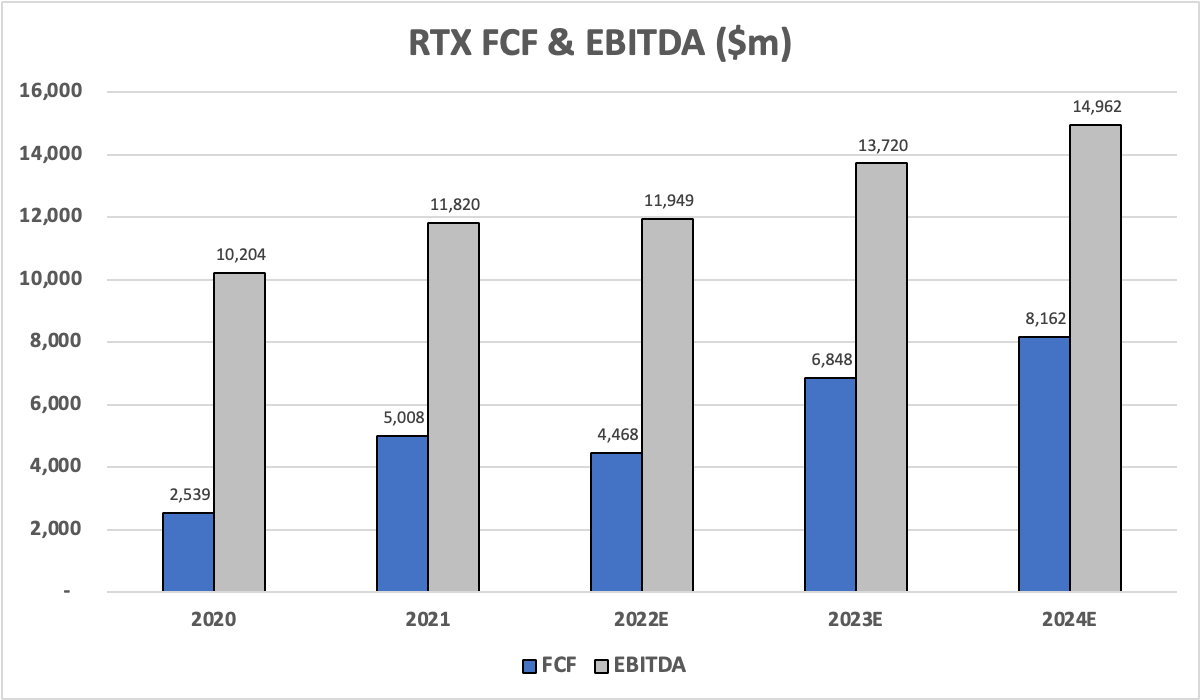

As we discussed in the first part of this article, Raytheon did not lower its free cash flow outlook. The company is still looking at $4 billion in 2022 free cash flow, which is based on lower tax payments in several large international receipts in the fourth quarter.

With that said, next year, free cash flow is expected to increase meaningfully to $6.8 billion. This includes organic growth from major programs as the backlog is turned into sales and small headwinds from investments in new production capacity - like the Texas facilities and RIS programs.

{kind=link}

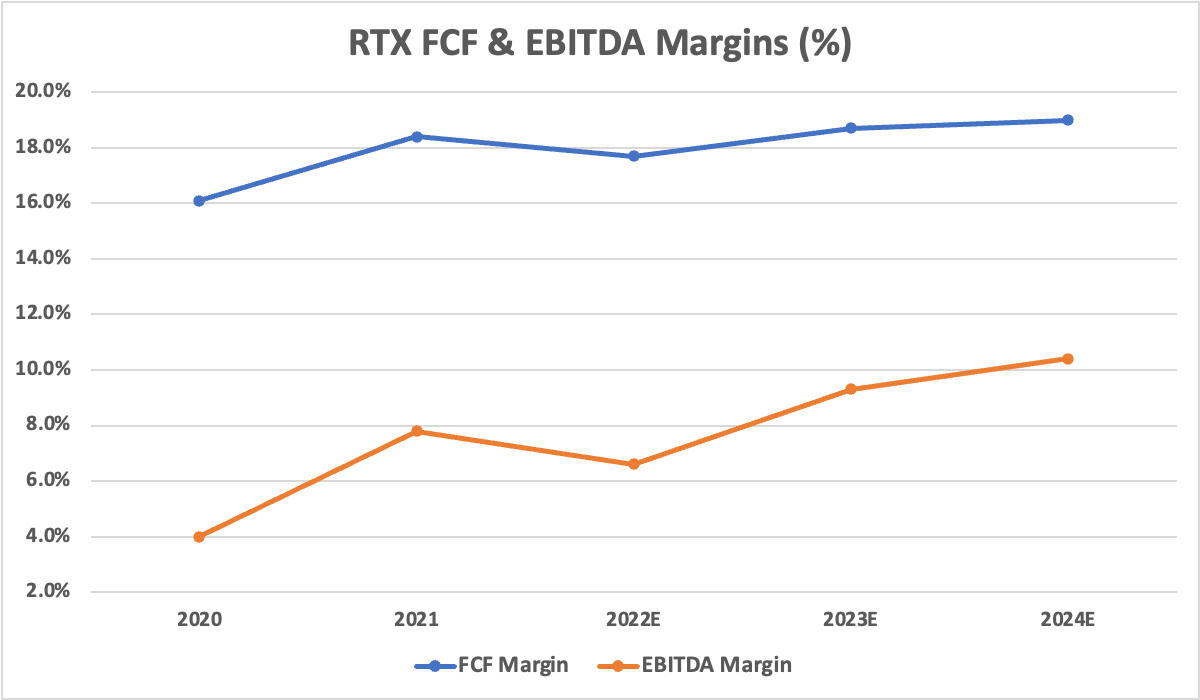

The free cash flow margin is expected to rise by 100 basis points in 2023 to 18.7%.

{kind=link}

The chart above implies that free cash flow could hit $8.2 billion in 2024. That would imply a free cash flow yield (do not confuse this with margin) of 6.3% based on the company's $130 billion market cap.

That's a big deal as it not only protects the company's dividend yield of 2.40% currently, but also opens up new opportunities for aggressive buybacks and dividend hikes.

The average dividend growth rate since the 2020 merger is 7.6%. I expect that number to accelerate toward 10% in the years ahead.

This is what I wrote with regard to buybacks in September:

As buybacks are more attractive when it comes to taxes and a way more flexible tool to distribute cash to shareholders, Raytheon has used buybacks to reward investors on top of its regular dividend. In 2Q22, the company repurchased shares worth $1.0 billion, pushing buybacks to $1.8 billion on a year-to-date basis. The goal is to repurchase $2.5 billion worth of shares this year, which is 1.9% of the current market cap, bringing total shareholder returns to 4.4% including the current dividend. That's not too bad.

2022 buybacks of $2.5 billion were confirmed. Next year, buybacks are likely to end up at $3 billion.

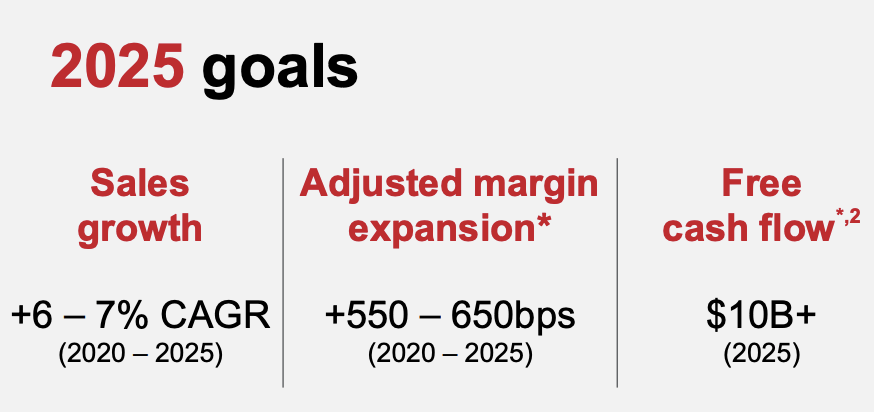

Even more important is that the company is sticking to its 2025 targets.

The future remains absolutely bright for RTX. The 2025 commitments that we laid out a year ago may remain in sight. And we're not going to back off from any of those, be it top line, bottom line, or cash.

These goals see more than $10 billion in 2025 free cash flow, implying a 7.7% FCF yield.

{kind=link}

With that said, the valuation has become quite attractive - in addition to high implied free cash flow yields.

Raytheon Valuation

Raytheon is trading at 12.0x 2023 EBITDA of $13.7 billion. That is based on its $130 billion market cap, $25.6 billion in expected 2023 net debt, $1.6 billion in minority interest, and $7.4 billion in pension-related liabilities.

Hence, I stick to what I wrote in September:

This valuation is more than fair and it opens up new opportunities to either add exposure to existing positions or initiate a position.

{kind=link}

With that said, I don't know if the market bottoms at these levels. More downside is not unlikely as the Fed is aggressively hiking into economic weakness.

However, when it comes to long-term investing, I buy quality stocks when I see an opportunity. Right now, I really like the valuation and the business environment of RTX. Hence, I expanded my position by roughly 8% in September as I added at an average price of $87.94.

Takeaway

In this article, we discussed the reasons that make Raytheon Technologies an attractive investment.

The company is finally benefiting from strong demand growth in both its defense and commercial segments. Despite the recession and China's zero-COVID policies, global commercial aerospace demand is improving. We now see higher demand for both domestic and international flights, benefiting new orders in the aerospace industry.

This is boosting organic growth for both OE and aftermarket sales.

Moreover, defense is booming. RTX benefits from accelerating defense spending as it is a key supplier of all of its peers and the backbone of NATO defense forces.

The company saw close to $20 billion in new orders, boosting its backlog and the book-to-bill ratio to 1.30.

While 2022 will remain challenging due to supply chain issues, 2023 and beyond are looking good. The company will be able to turn backlog into finished sales, boosting free cash flow and related financial numbers.

It also helps that the 2025 outlook was once again confirmed, providing investors with an outlook of further accelerating dividends, high buybacks, and an attractive valuation.

While I significantly increased my RTX stake in September. I will continue to be a buyer at these levels.

(Dis)agree? Let me know in the comments!

For further details see:

Raytheon: 3 Compelling Reasons To Be A Buyer