CA - Razor Energy's $100 Million Deal Implies Great Value For Journey Energy's Power Business

2023-07-20 16:04:57 ET

Summary

- Bison sees potential in Journey Energy's rapidly growing power generation business, which could be worth more than the company's current enterprise value.

- The recent FutEra transaction implies a significant upside for Journey Energy’s power business, which could be worth ~60% of its current market cap by early 2024.

- Despite a promising outlook for Journey’s power generation business, market participants seem to be undervaluing it, presenting a potential investment opportunity.

At Bison, we look for heavily discounted oil and gas equities with good assets, survivable balance sheets, proven management teams, and imminent catalysts to help close valuation dislocations in public markets.

This sometimes involves buying equities with core businesses trading at low valuations that also have secondary assets that could be worth a significant portion of their current enterprise values. We believe these offer a degree of downside protection and may offer revaluation trajectories less tied to short-term commodity price movements.

Journey Energy ( JOY:CA ) ( JRNGF ), an Alberta-based publicly traded oil and gas company for which Bison has previously shared its investment thesis , meets these criteria. Despite materially outperforming peers since we disclosed this thesis, Journey's core business has gotten cheaper as underlying fundamentals rapidly improved. Concurrently, Journey has continued to ramp up its power generation business, which is growing so rapidly and cost-effectively that it could be on a path to eventually be worth more than Journey's current enterprise value. More on this below.

Razor Energy: Small Oil Company Selling its Power Assets

In assessing the potential value of Journey's power generation business, it is helpful to look at its neighbor, which recently sold a similar asset: Razor Energy ( RZE:CA ). Razor had exposure to power generation assets through its wholly-owned subsidiary, FutEra Power. Razor effectively sold the majority of its interest in this power generation business through a recapitalization in which its largest lender, the Alberta Investment Management Company ("AIMCo"), agreed to swap all its outstanding debt to Razor in exchange for shares of FutEra. After considering certain price adjustments, this deal implies a healthy value for Journey's power generation assets.

Razor Recapitalization Transaction Overview

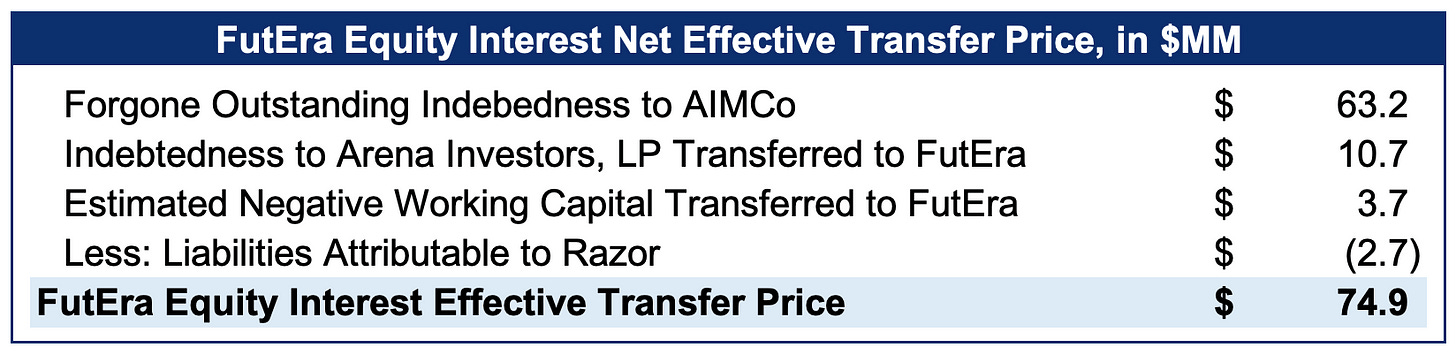

As part of the transaction, AIMCo forgave $63.2 MM of outstanding Razor debt in exchange for 70% of FutEra's outstanding equity, including some convertible preferred shares paying a 12% dividend with a liquidation preference. These preferred shares will effectively give AIMCo another 9% of the outstanding FutEra common shares when converted. FutEra also assumed $10.7MM of outstanding Razor debt to another lender and ~$3.7MM of negative working capital from Razor. Adding the net value of these assumed liabilities to the value of the forgone debt gives us an effective transfer price of $75MM:

{kind=link}

Adjusting for the fully diluted ownership AIMCo received in FutEra, this transaction implies a value of $92MM for FutEra's entire business:

{kind=link}

It is worth noting that Razor Energy itself only had a market capitalization of ~$20MM at the time of the deal - this recent transaction implied a value for a wholly owned subsidiary that was ~5x Razor's market cap. Razor also materially de-levered its balance sheet in this transaction, and its small size does not appear to have been an impediment to the divestiture valuation.

Transaction Value Look-Through for Journey Energy

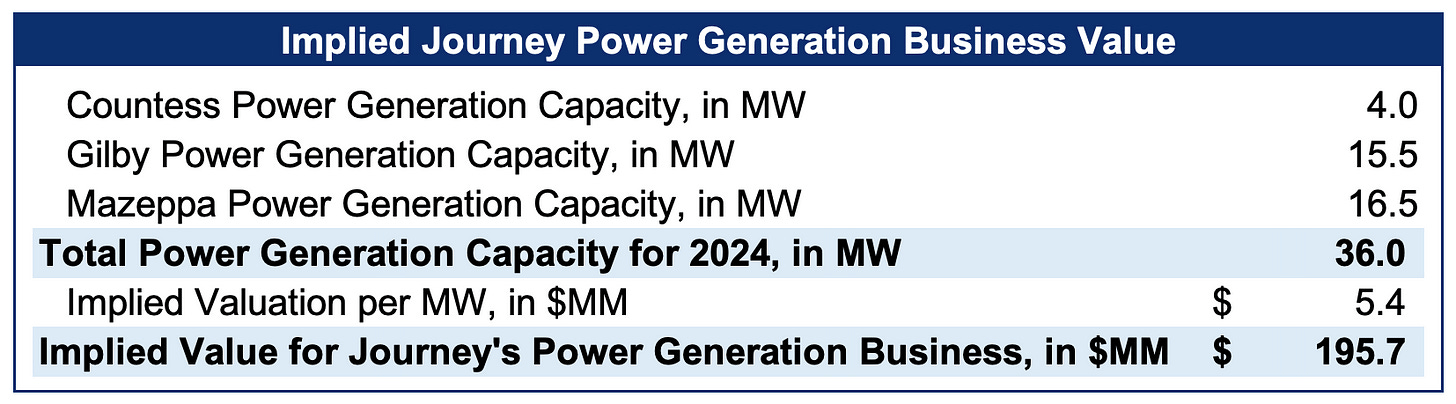

The FutEra transaction implies a significant upside for Journey Energy's nearby, rapidly growing power business. FutEra has 21MW of nameplate installed power generation capacity at its Swan Hills facility, but we estimate the true effective capacity is closer to 17MW, based on disclosures and comments from Razor and FutEra management. This implies a value of $5.4/MW for this transaction:

{kind=link}

Journey currently has 4MW of installed power generation capacity at its Countess facility. Journey had also received preliminary approval to build a 15.5MW generation facility at its Gilby gas plant and recently completed the purchase of a 16.5MW power generation facility in Mazeppa, Alberta. Altogether, Journey is expected to have 36MW of effective power generation by early 2024. The implied value for Journey's power generation, once it is up and running, may be $196MM following this transaction:

{kind=link}

Implications for Journey Energy

The FutEra transaction valuation has positive implications for Journey, whose power generation assets could be worth ~60% of its current market cap of ~$330MM by early 2024. It is worth noting that Journey's power generation business is rapidly growing and has an extremely high return on investment as compared to traditional oil and gas exploration and production. For instance, Journey's Countess power generation facility had a payback period of only 2.5 years!

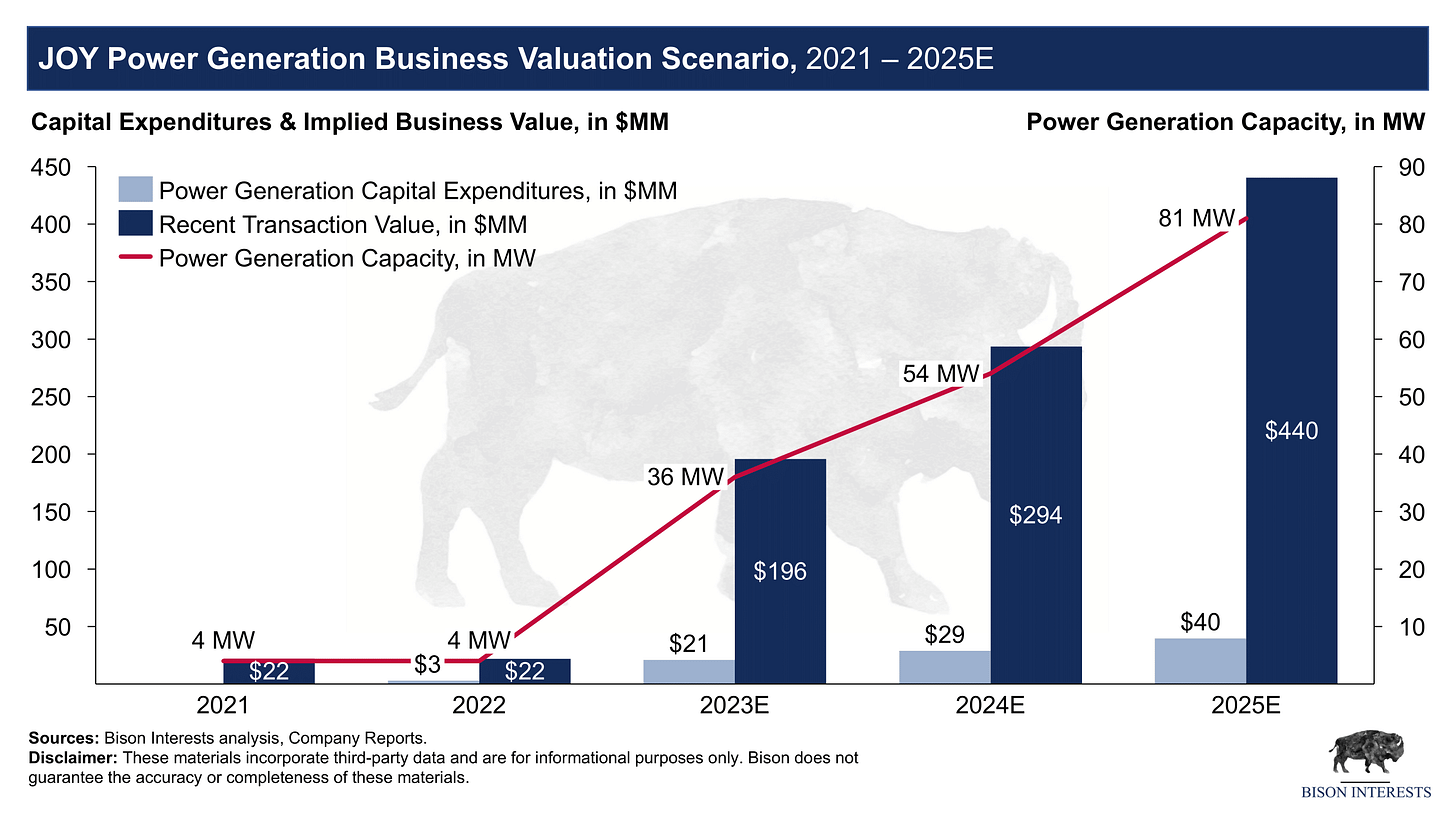

By our estimates, Journey's power generation business could be worth as much as ~$440MM by 2025 if it continued to grow rapidly and cost-effectively:

{kind=link}

As Journey scales up this business over time, power generation may soon make up a significant portion of the overall business and cash flow. AIMCo's willingness to swap its debt for equity in a power generation business reflects its understanding of improving fundamentals in an undervalued sector and was a way for the pension manager to secure a long-term infrastructure cash flow stream at a comparatively low valuation.

Journey's power assets are integrated with its gas production, resulting in lower production costs, higher margins, and an option to sell gas into the spot market should prices recover. For this reason, Journey's gas production may even be worth more than the $5.4MM/MW implied in the FutEra transaction. Consider this excerpt from Journey's Q1 2023 earnings press release:

"The currently operating, 4 MW Countess facility, which was originally commissioned in the fourth quarter of 2020, is already close to paying out the original investment. Based on Journey's realized power prices in 2022, the average, effective, net realized price for natural gas used to generate power for the year was approximately $10.54/mcf. […]

As a comparison, the average AECO benchmark price for 2022 was approximately $5.43/mcf and $3.23/mcf for the first three months of 2023. "

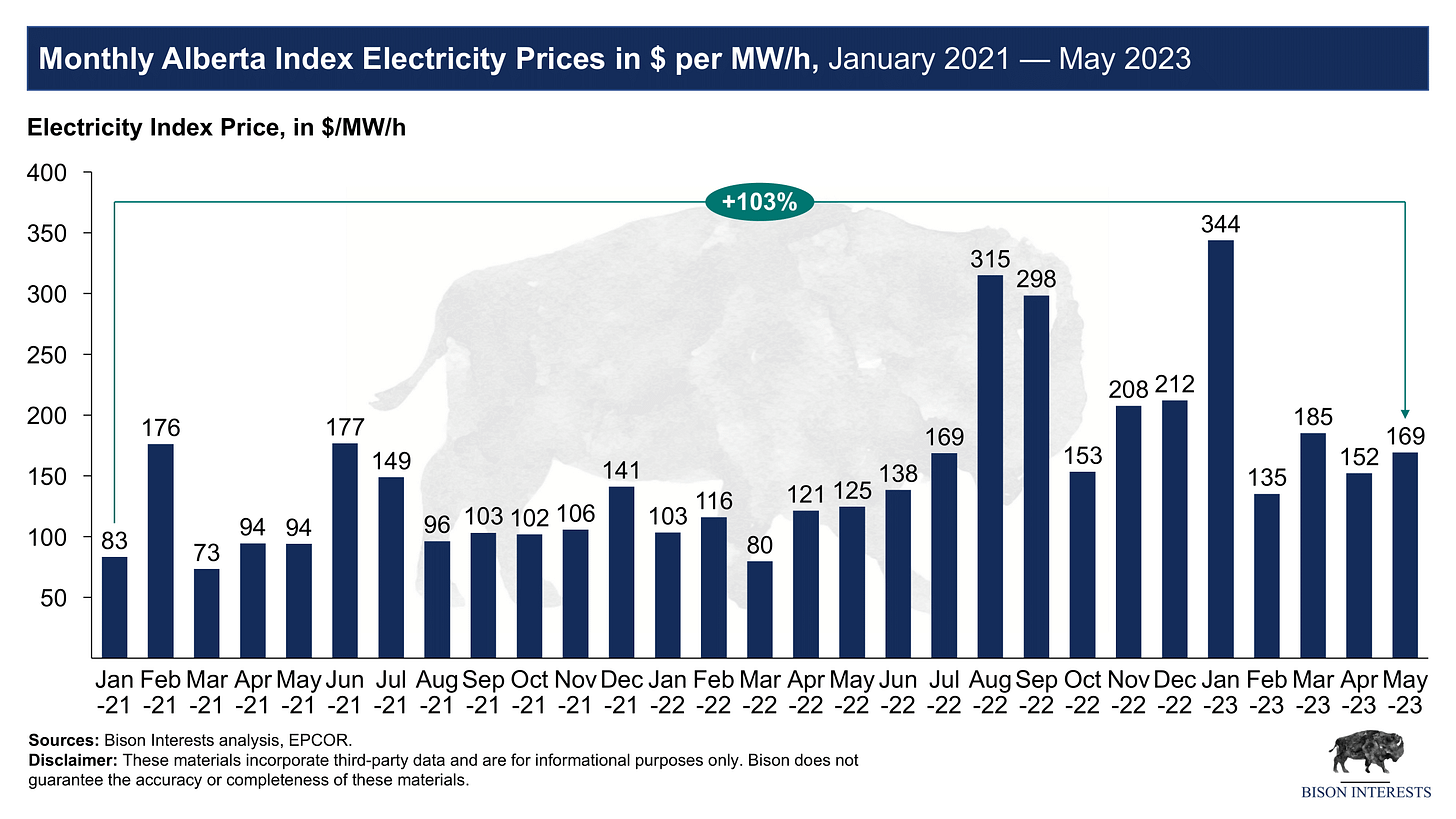

The above implies that Journey can get ~3 times as much value from its gas production when converting it to power. It is also worth noting that Journey will be a direct beneficiary of rising power prices in Alberta once its new facilities are running (after having suffered from being a net high-priced power consumer ahead of the commencement of the new power generation facilities).

{kind=link}

Conclusion/Takeaways

Despite a promising outlook for Journey's power generation business, few analysts and market participants seem to be giving it any credit. This became apparent when Journey shares sold off following Journey's Q1 earnings announcement. Cash flow came in lower than expected in Q1, largely due to lower price realizations following higher WCS differentials, which have subsequently improved, and higher operating expenses due to high power prices. However, Journey's rapidly growing power generation business will soon entirely offset these costs, as they are expected to rapidly shift from a net consumer to a net power producer in less than a year.

Additionally, the market may be incorrectly attributing power generation capital expenditures to oil development activity, showing artificially depressed capital efficiency. The commencement of 32 MW of power generation by early 2024 should illustrate the high return nature of these capital expenditures, as well as the low capital requirements on Journey's low decline oil & gas production business.

The recent pullback in Journey's share price presents an opportunity to invest in a discounted low-decline oil and gas producer with proven management. And as a bonus, investors are getting exposure to a rapidly growing, high-margin power generation business in an environment where power prices are rising. As the cash flow from Journey's power generation becomes more material and Journey's overall margin profile improves, we see the potential for a material re-rate in their valuation.

For further details see:

Razor Energy's $100 Million Deal Implies Great Value For Journey Energy's Power Business