CA - RB Global - Vulnerable To Customer Activity But Still At A High Premium

2023-08-05 11:10:22 ET

Summary

- RB Global Inc has seen significant revenue growth and currently has a valuation of $11 billion.

- The company recently acquired IAA, resulting in an additional $560 million in revenues and showcasing its potential for future growth.

- The company operates as a leading auctioneer of industrial equipment on an international basis, generating revenue from various sources.

Investment Rundown

Since its of funding year in 1958 RB Global Inc ( RBA ) has grown its revenue streams. The company operates in diversified support services where it has grown its valuation to $11 billion. The share price has risen quite quickly in the last couple of months and the p/e sits quite high right now at 25x.

The company not long ago made a solid acquisition of IAA which in the most recent earnings report from the company resulted in an additional $560 million in revenues. This totaled the revenues at $1.1 billion. I think this is showcasing the potential going forward with RBA but the valuation has me question the immediate potential of an investment right now. The valuation seems expensive to pay and the company doesn't necessarily have the growth to justify it. As a result, I am rating the company a hold right now.

Company Segments

Back in early May Ritchie Bros Auctioneers Incorporated made the name change to RB Global Inc instead. This has of course not changed the operations and priorities of the business. The company still operates as a leading auctioneer of industrial equipment on an international basis.

The company aims to provide a transparent marketplace where sellers and customers can interact efficiently and capital can circulate quickly. There are many different groups on both sides of the sales agreements, all from major companies to small businesses and governmental agencies too.

{kind=link}

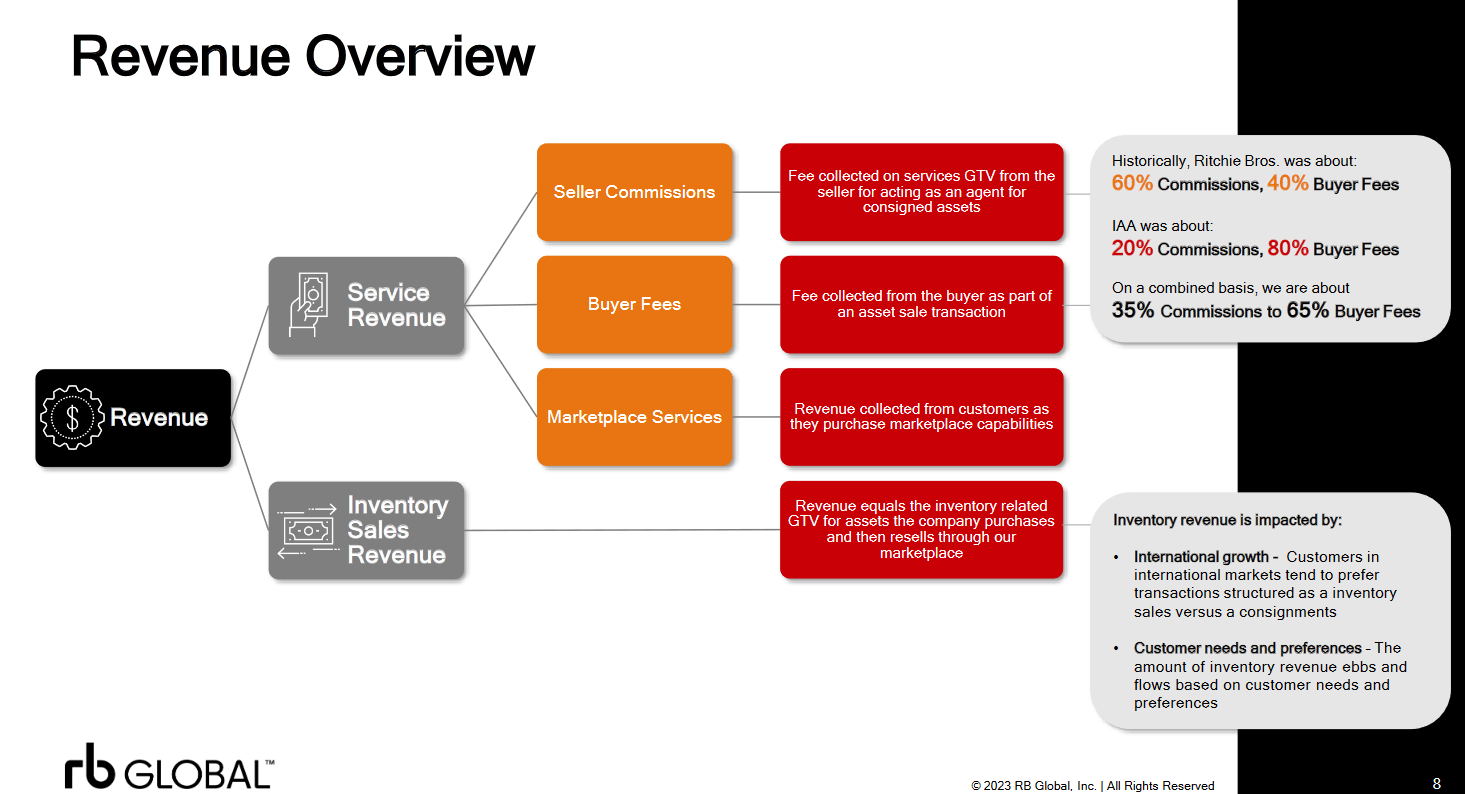

Revenue Overview (Investor Presentation)

The revenue overview of RBA showcases that the revenue is being generated from a variety of sources and this lends RBA to a somewhat stable top-line growth over time. Over the last 10 years, the CAGR of revenues has been 15.49% which is incredibly impressive. The service revenues that RBA gets comes from three different sources, those being sales commissions, buyer fees, and marketplace services. The inventory sales revenues are impacted by international growth as RBA holds a broad presence. The revenues here are however very driven by the demand and supply from customers. The higher the activity is the more revenues RBA can generate. That means RBA is quite vulnerable to economic slowdowns and this likely results in slowing revenues and earnings.

Expenses (Investor Presentation)

The cost or expense categories for RBA include the cost of services, selling, general and administrative expenses but also acquisition-related and integration costs. This year RBA completed the acquisition of IAA which was valued at $7 billion making this one of the largest moves by the company in its path to establish itself as a leader in the global auctioneer space.

IAA is an auto retailer that focuses on auctioning and selling heavy industrial equipment to customers all over the world. The additions add a strong market opportunity for RBA to be a part of and I am excited to see the development of it in the coming quarters.

{kind=link}

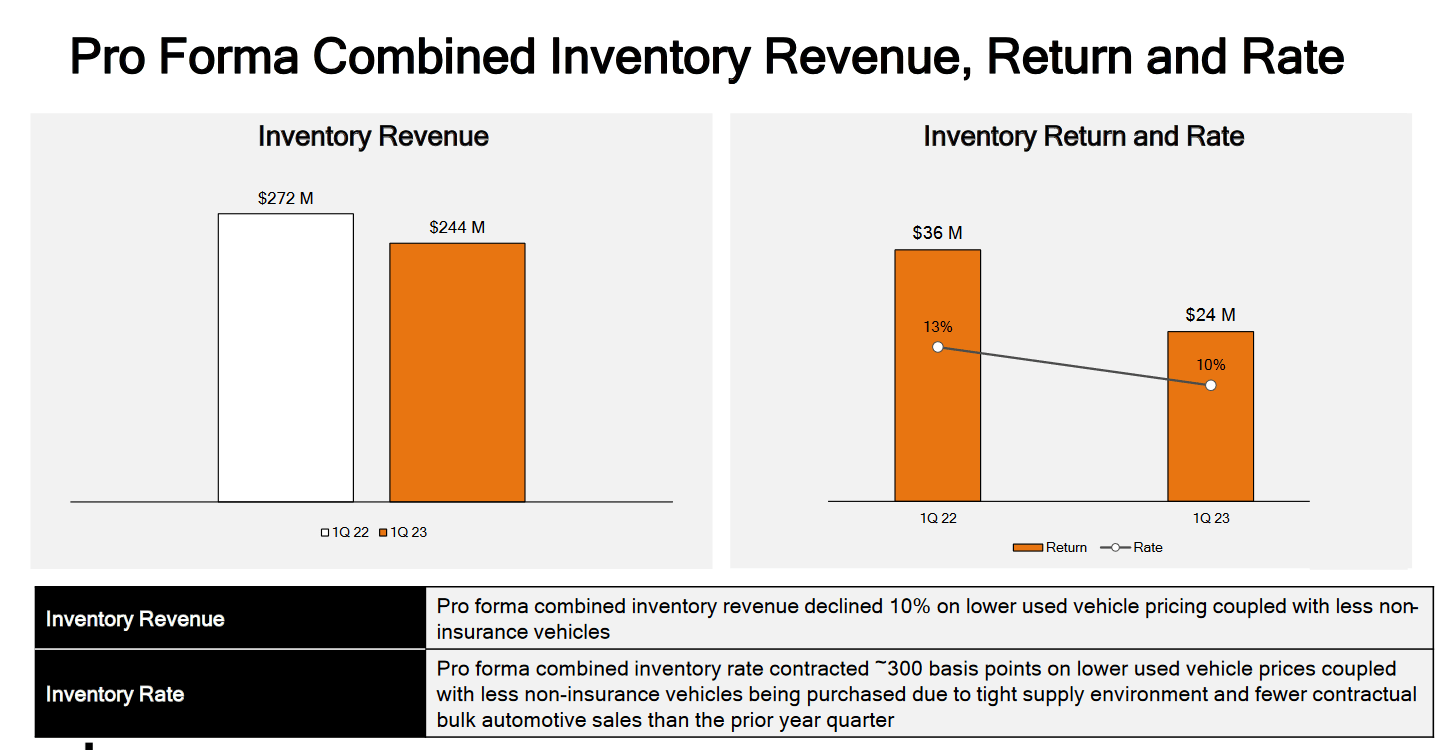

Inventory (Investor Presentation)

A significant portion of the revenues of RBA comes from inventory revenues. The inventories currently sit at the highest level ever at over $200 million. The YoY inventory revenues are however slightly down, most likely caused by higher interest rates which create a less incentivized customer base. When we see lower interest rates I do expect there to be more activity in this part of the company and that will be a driving force for the top and bottom line going forward.

Risks

In the current challenging market environment, characterized by cautious spending and economic uncertainties, companies like RBA, operating as auctioneers, could face increased vulnerability to the impact of a slowing economy and reduced customer spending.

As economic conditions fluctuate, customers may exercise more prudence in their spending decisions, especially when it comes to non-essential items or assets. Auctions, which involve discretionary purchases and investments, may experience reduced demand as customers prioritize essential needs and cost-saving measures.

Furthermore, in a sluggish economy, companies and individuals may be more inclined to hold onto their assets rather than parting with them through auctions, potentially leading to a decrease in the supply of items available for sale. As supply and demand dynamics shift, auctioneers like RBA might face challenges in attracting sufficient inventory and achieving optimal auction outcomes.

Financials

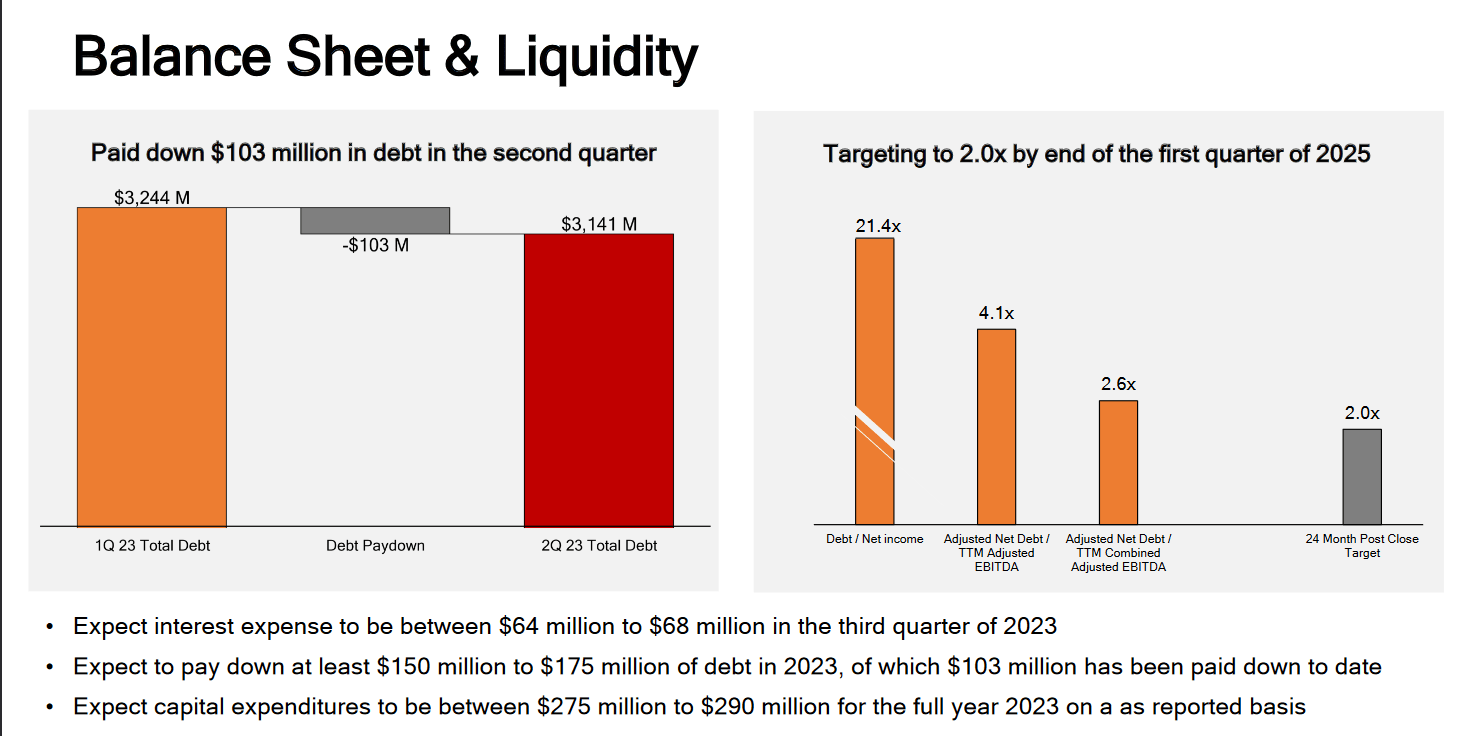

One of the highlights of RBA I think is the financials of the company. The company has the highest cash position in its history at $432 million and when comparing this to the long-term debt it might look worrying. The long-term debts sit at over $3.2 billion.

{kind=link}

Balance Sheet (Earnings Presentation)

However, I think we are wrong to assume that RBA has overleveraged it because of this. The debt grew to this number from $577 million in 2022. The raised debts come from the $7 billion acquisition that RBA performed earlier in 2023. This acquisition is however adding a lot of net income to the business and I think that will in time help essentially pay itself off. Just for 2023, RBA is expecting to pay down at least $150 - $175 million in debts, that's a reduction of 4.2% on the higher end of the estimation.

Final Words

RBA is a very unique investment opportunity where it operates auctions on an international basis and the revenues and earnings are largely driven by demand and activity but also the operational performance of the company. In slowing market conditions the revenues take a hit but in times of high spending, the growth is almost euphoric.

But that price to pay for RBA right now I think is a little too expensive at a P/E of 25. This isn't indicating to me that I am getting in at an undervalued price point. I want some solid margin of safety for my investment and I don’t feel I am getting that. But, the acquisition of IAA is looking very promising and this could be a driving force for RBA and results in me latest having a hold rating for the company.

As I have mentioned earlier I think that CLNE is trading at a premium, at a too high when to pay for. Seeing as the bottom line is negative there is no point in comparing the P/E. But looking at the EV/EBITDA on a FWD basis it sits at a 22x multiple. That is 284% above the sector, indicating investors are having to take on a significant premium to get into the company. Further highlighting the risks and rich valuation is the P/FCF which is at 27 on a FWD basis. That is far above the sector's 4.7 average. I think we are far out from seeing these multiples decline significantly and make CLNE look appealing.

For further details see:

RB Global - Vulnerable To Customer Activity But Still At A High Premium