RMAX - RE/MAX Holdings Stock: Expect Continued Volatility In 2024

2024-01-19 04:42:07 ET

Summary

- RE/MAX Holdings, Inc. is facing a challenging real estate market for its residential brokerage network.

- The company's financial performance has declined, with shares losing more than half their value in the past year.

- A large balance sheet debt position and a history of poor strategic execution highlight our expectation for shares to remain under pressure.

RE/MAX Holdings, Inc. ( RMAX ) has struggled to adapt to a changing real estate landscape over the last several years. Recognized as one of the world's largest traditional brokerage franchisors, the challenge here is dealing with an increasingly competitive market including disruptive digital platforms.

Multi-decade high mortgage rates in the U.S. and overall weakness in residential home sales are simply the latest headwinds. Indeed, shares have lost more than half their value over the past year, adding to a steady decline going back to an all-time high back in 2017.

While the current outlook suggests a path for at least recurring profitability, we don't see much in terms of a catalyst to support a big rebound in the stock price. Even with room for interest rates to pull back through 2024, soft conditions in the housing market should linger with downside risk for fee-related income. We expect shares to remain volatile.

RMAX Financial Recap

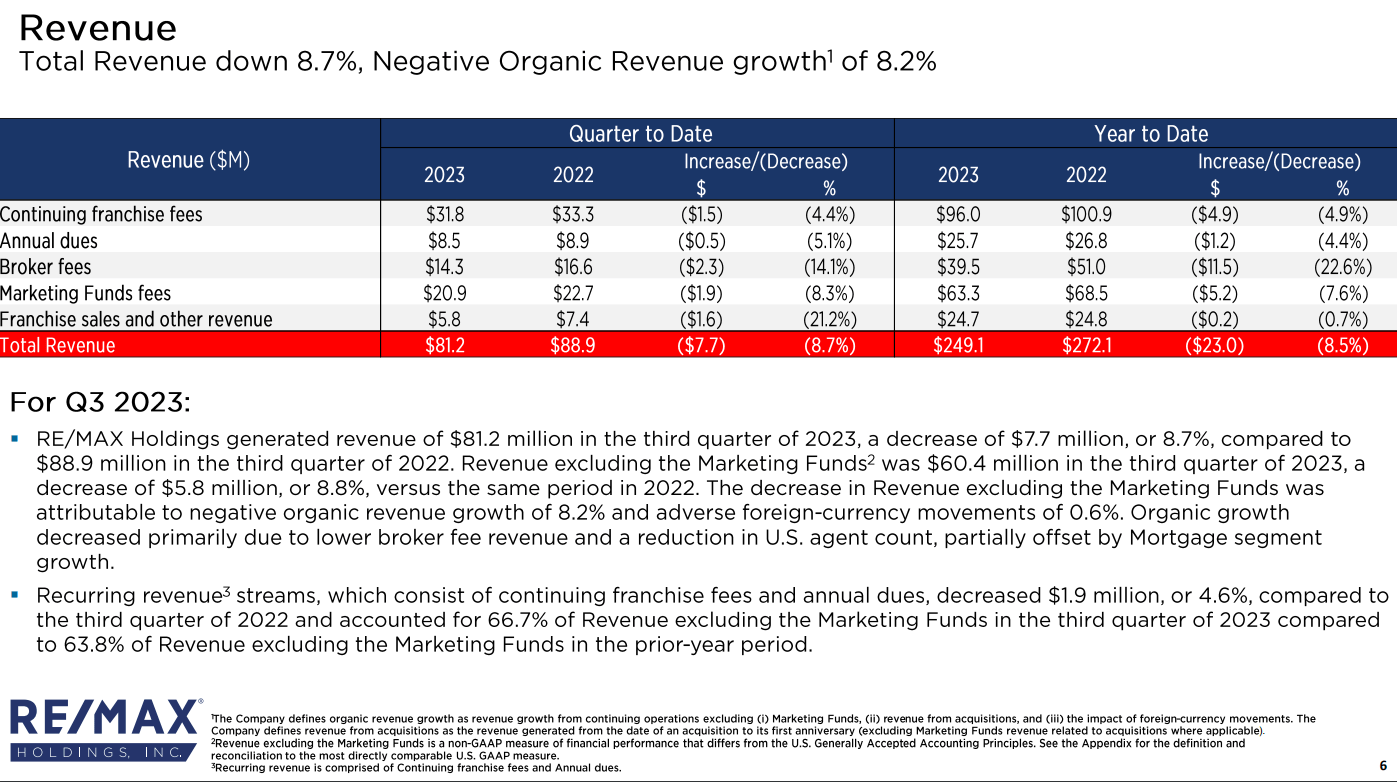

RMAX last reported its Q3 earnings back in November with an adjusted EPS of $0.40, coming in ahead of estimates, but also down from $0.56 in the year prior. Revenue of $81.2 million fell by -8.7% year over year.

Within this amount, the weakness was widespread across core business drivers. Franchise fees, annual dues, broker fees, and marketing fees were all lower reflecting the decline in transaction volumes .

Keep in mind that there is also the "Motto Mortgage" franchise that now includes 242 offices. This segment has been a growth driver but remains a relatively small part of the overall business.

{kind=link}

source: company IR

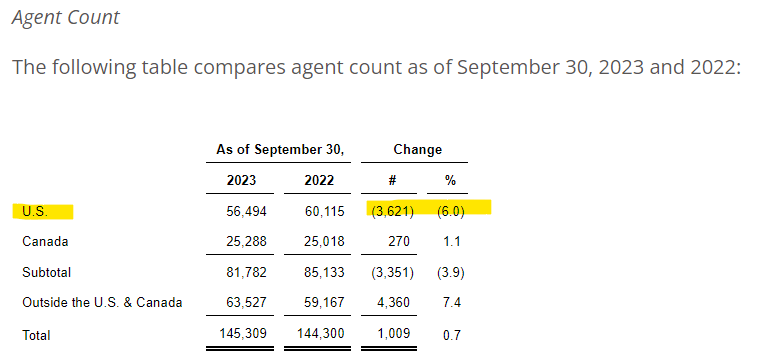

Even as the global total of affiliated agents climbed by 0.7% y/y to 145.3k, there was a bigger decline in the transaction per agent as a key operating metric. What's more concerning here is the company's core U.S. market posted a bigger drop with total U.S. agents down by -6% y/y.

We bring this up because even as the company is generating stronger growth internationally, the U.S. market represents a higher value of business with stronger margins. That impact is reflected in adjusted EBITDA declining -15% y/y to $26.7 million. The 32.9% margin is also lower from 35.4% in Q3 2022.

{kind=link}

source: company IR

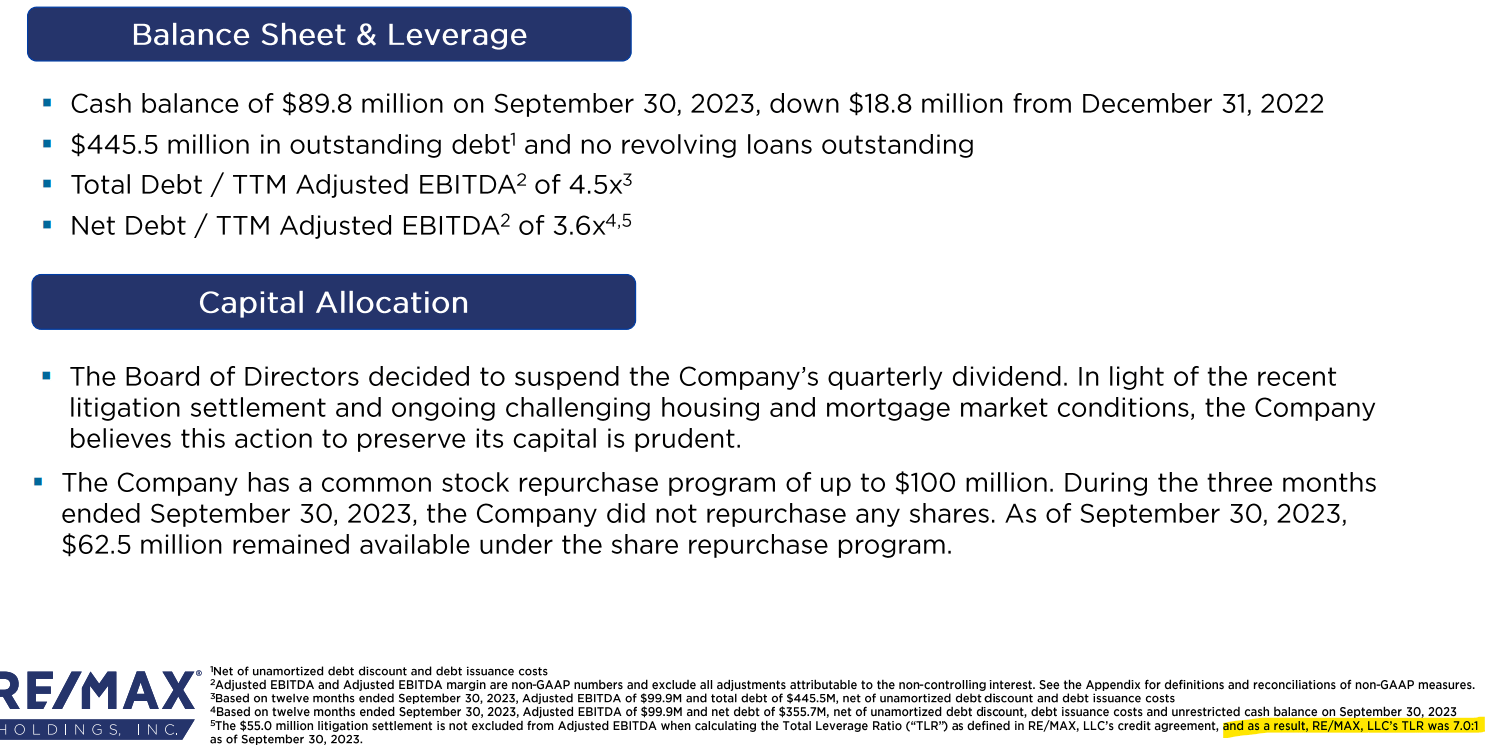

The other key development was the recognition of a $55 million class action lawsuit settlement charge. At issue is RE/MAX's apparent role in systematically inflating buyer-broker commissions. The immediate implication was a suspension of the company's quarterly dividend. We do not expect the dividend to be reinstated this year.

As of September 30th, the net debt to adjusted EBITDA leverage ratio was noted as 3.6x. At the same time, the unadjusted measure including the $55 million cash charge is noted as reaching 7.0x, expected to remain elevated for the foreseeable future. This otherwise distressed financial position explains some of the equity price volatility and represents a weakness in the company's investment profile.

In terms of guidance, the expectation is for a continuation of Q3 trends over the next few quarters. Management is targeting Q4 revenue in a range between $74 and $79 million, down about 5% at the midpoint from 2022. The adjusted EBITDA forecast is between $21.5 and $23.5 million, if confirmed, represents a decline from $26.5 million in the period last

{kind=link}

source: company IR

What's Next For RMAX?

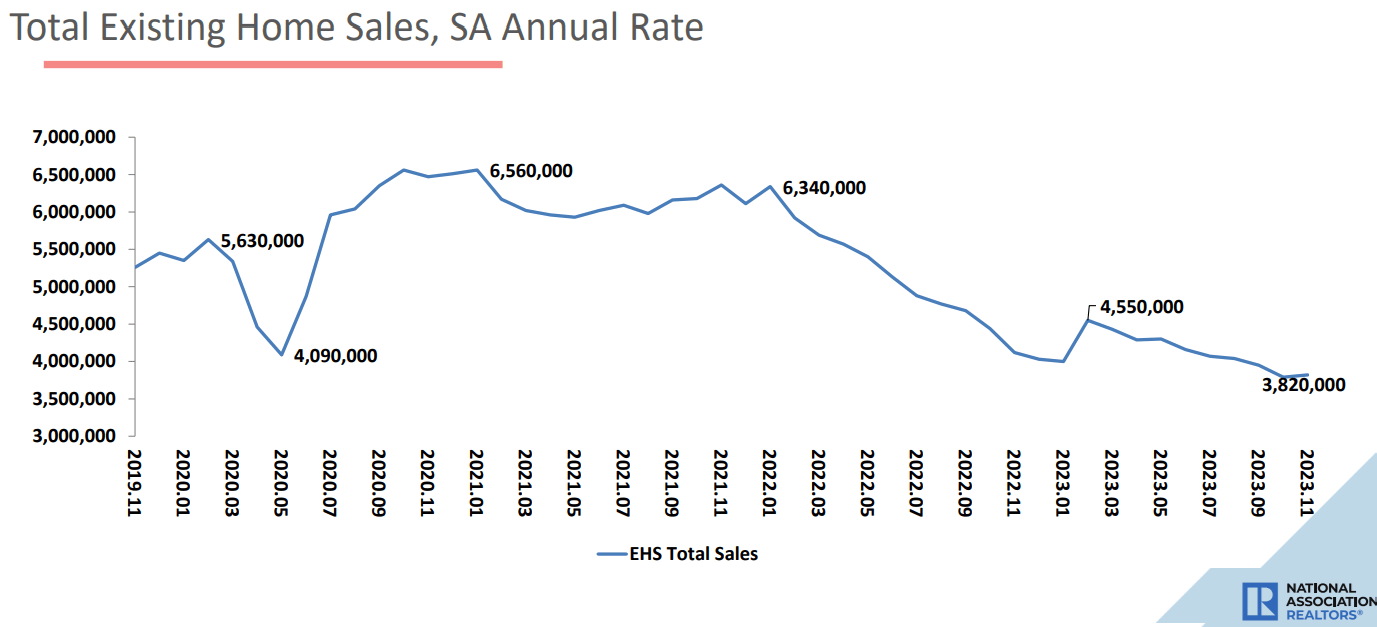

It's clear to us that sentiment towards the stock is terrible based on not only poor operating trends and financial results but also the sector outlook. In the U.S., data from the National Association of Realtors industry group shows that existing home sales continue to decline with a 7.3% drop in November.

While this trend has moderated compared to the sharper pullback in the first half of last year, there is significant uncertainty on when a sustained rebound will take place and how strong the market will evolve over the next few years.

On one hand, expectations for Fed Rate cuts could provide some relief for buyers on the financing side. Still, the issue remains affordability with the same report suggesting existing home prices have begun climbing again.

Whether or not a deeper correction in real estate develops, our take is that the process for normalization will take several years. Outside the U.S., high-interest rates are a global theme. We can say with some measure of confidence that it's not a great time to be starting a residential real estate brokerage business.

{kind=link}

source: company IR

The setup here should continue to weigh on RE/MAX revenue and fee income. There is also thought that the litigation headlines and poor stock price performance itself limit the attraction of the RE/MAX brand to potential agents seeking to join the network.

This is important considering the abundance of options and competitors on the market. We mentioned disruptive digital competitors. eXp World Holdings, Inc. ( EXPI ) through its eXp Realty brand stands out as a player essentially capturing market share at the expense of RE/MAX. In Q3, EXPI reported positive revenue growth while onboarding more agents.

Nevertheless, the sense is that this is a difficult time for the entire industry, but RE/MAX is simply an underperformer. The bigger risk is that conditions deteriorate with a catalyst being interest rates remaining higher for longer or even upside from the current level.

{kind=link}

Seeking Alpha

Final Thoughts

We rate RMAX as a sell with a view that risks are tilted to the downside. The company faces some real operating and financial challenges over the next few quarters and it's fair to maintain a level of skepticism that management will be able to successfully engineer a turnaround.

The first step would be to see signs of stronger growth reflecting some brand momentum. Monitoring points include the ability to attract agents to the core U.S. and Canada franchisees. We also want to see a recovery in franchise sales as a funnel for sustained long-term momentum. The company will also need the macro picture to cooperate with materially improving housing market statistics.

Putting it all together, there are several headwinds at play and we recommend investors avoid RMAX.

For further details see:

RE/MAX Holdings Stock: Expect Continued Volatility In 2024