RRX - Regal Rexnord: An Interesting Play Despite Recent Weakness

2023-05-18 10:56:59 ET

Summary

- Regal Rexnord Corporation has experienced a decline in sales, profits, and cash flows due to fundamental weakness.

- Despite these issues, the company's recent acquisition and transitory problems make it an attractive investment with a soft 'buy' rating.

- Regal Rexnord's acquisition of Altra Industrial Motion could lead to significant upside in the future, with annualized cost synergies and increased revenue.

One of the more diverse companies that I've come across in recent years is Regal Rexnord Corporation ( RRX ). Although the company describes itself as an engineering and manufacturing firm that focuses on powertrain solutions, its operations truly do touch on many different market segments. For instance, it produces and sells AC and DC motors, electronic variable speed controls, fans and blowers, fractional horsepower motors, industrial bearings, high quality conveyor products, and more. Over the past several months, shares of the company have outperformed the broader market. But recently, fundamental weakness has been a problem. Sales, profits, and cash flows are all showing signs of pain. But when you consider how transitory these problems are, and the fact that its recent acquisition makes it cheap on a forward basis, I do believe the company still warrants a soft 'buy' rating.

Staying the course despite recent weakness

As of this writing, it has been almost exactly one year since I last wrote about Regal Rexnord. In that article, published May 23, 2022, I decided that the company made for a solid opportunity for investors to consider. A major merger that created the business set the stage, for what I believe will be attractive returns moving forward. And on top of that, shares of the company looked attractively priced. This ultimately led me to rate the business a ‘buy’, a rating that reflected my view at the time that shares should outperform the broader market for the foreseeable future. Since then, that is what happened, but not to the extent I would have been hopeful of. While the S&P 500 is up 4.7%, shares of Regal Rexnord have seen upside of 5.6%.

{kind=link}

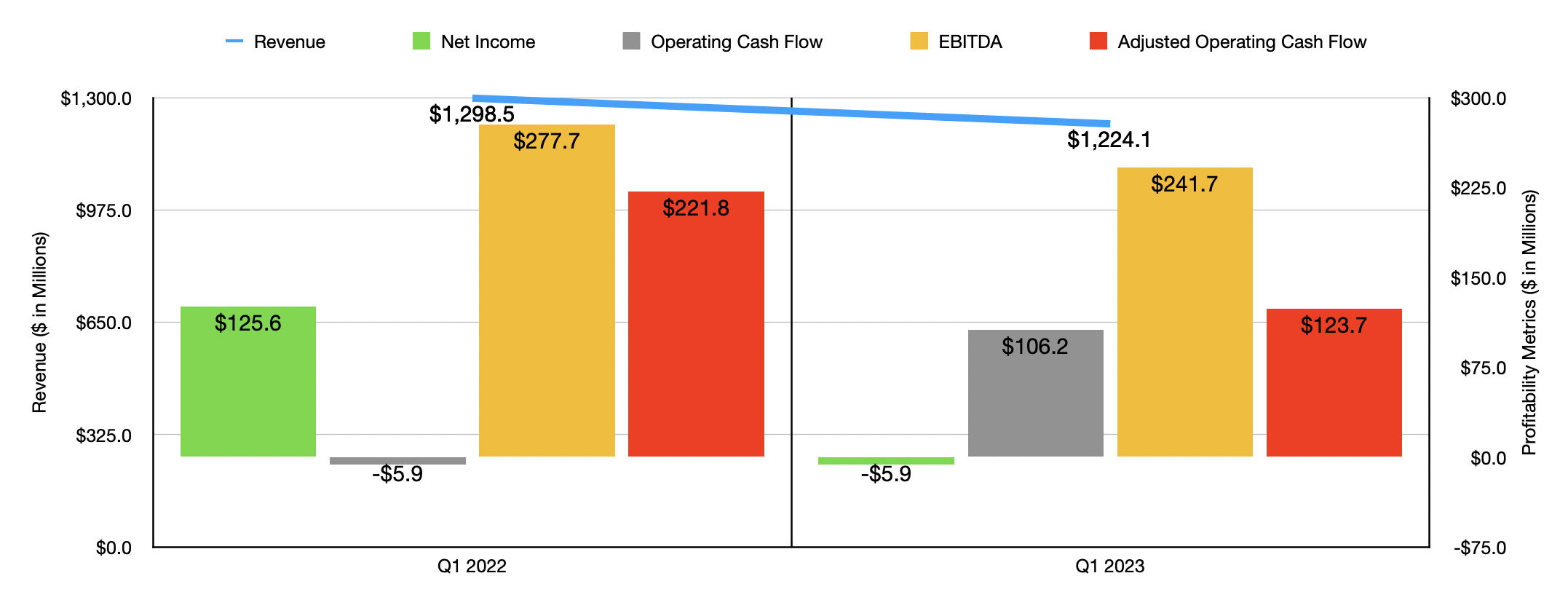

Given how volatile and picky this market is, I am a bit surprised that shares have outperformed the market. What I mean, we need only look at the most recent financial data available. This is data covering the first quarter of the company's 2023 fiscal year. According to management, revenue came in at $1.22 billion. That's 5.7% lower than the nearly $1.30 billion the company reported one year earlier. When we dig a bit deeper, we find that this financial performance was rather lopsided. Two of the companies four operating segments actually saw revenue increase year over year. For instance, the Industrial Systems portion of the enterprise saw revenue jump 4.8% from $130.7 million to $137 million. Even more impressive was the 10.3% increase in revenue associated with the Automation & Motion Control segment, with revenue climbing from $184.3 million to $203.2 million.

The problem areas for the company where it's two largest segments. The Industrial Powertrain Solutions segment of the company, for instance, saw revenue dip by 0.5% from $416.3 million to $414.4 million. Even though organic sales grew by 1.3% during this time, foreign currency fluctuations more than offset this. The most painful segment, however, was the Power Efficiency Solutions segment. Revenue there plunged 17.2%, dropping from $567.2 million to $469.5 million. This decline, management said, was driven in large part by a 15.9% drop associated with organic revenue. Worsening volumes caused by slowing market demand in the North America pool pump and residential market, as well as weak demand in the light commercial HVAC market, negatively impacted sales.

With the decline in revenue also came a drop in profitability. Net income went from a positive $125.6 million in the first quarter of 2022 to a negative $5.9 million in the first quarter of this year. Although gross profit figures varied from segment to segment, overall gross profit for the company remained flat relative to revenue. The pain for the business, then, came from other operating expenses. For instance, the Industrial Powertrain Solutions segment saw operating expenses jump from 25.9% of sales to 36.6%. This was instrumental in pushing segment operating profits down from 11.1% to 6.3%.

This decline, according to management, may very well be temporary, since the vast majority of the increase in costs was associated with a rise in acquisition costs from its Altra transaction. However, higher employee compensation costs were also a factor, though management did not describe the size of the impact there. Even more disastrous was the Automation & Motion Control segment, with operating expenses climbing from 27.5% of sales to 39.7%. This pushed the segment from generating and operating margin of 6.7% to generating an operating loss of 2.6%. Even though the company increased pricing for the segment, higher acquisition costs and a rise in employee compensation costs negatively impacted the business.

Unfortunately, other profitability metrics largely followed the same kind of trajectory. Operating cash flow was an exception, going from negative $5.9 million to positive $106.2 million. But if we adjust for changes in working capital, we would see the metric fall from $221.8 million to $123.7 million. Even EBITDA took a hit, falling from $277.7 million to $241.7 million.

When it comes to the 2023 fiscal year, management has some rather interesting guidance . They think that earnings per share will only be between $2.74 and $3.64. But on an adjusted basis, earnings should come in at between $10.20 and $11.10. Significant add-backs associated with transactions costs and amortization expenses, account for the lion's share of this disparity. If we take the adjusted figure for the company, this would imply net income of $662.7 million. That would represent a meaningful improvement compared to the $488.9 million reported for the 2022 fiscal year. When it comes to the other profitability metrics, the picture does get more complicated. Management has not provided any guidance for these. If we annualize the results experienced so far, we would expect adjusted operating cash flow of $446 million and EBITDA of $905.6 million.

{kind=link}

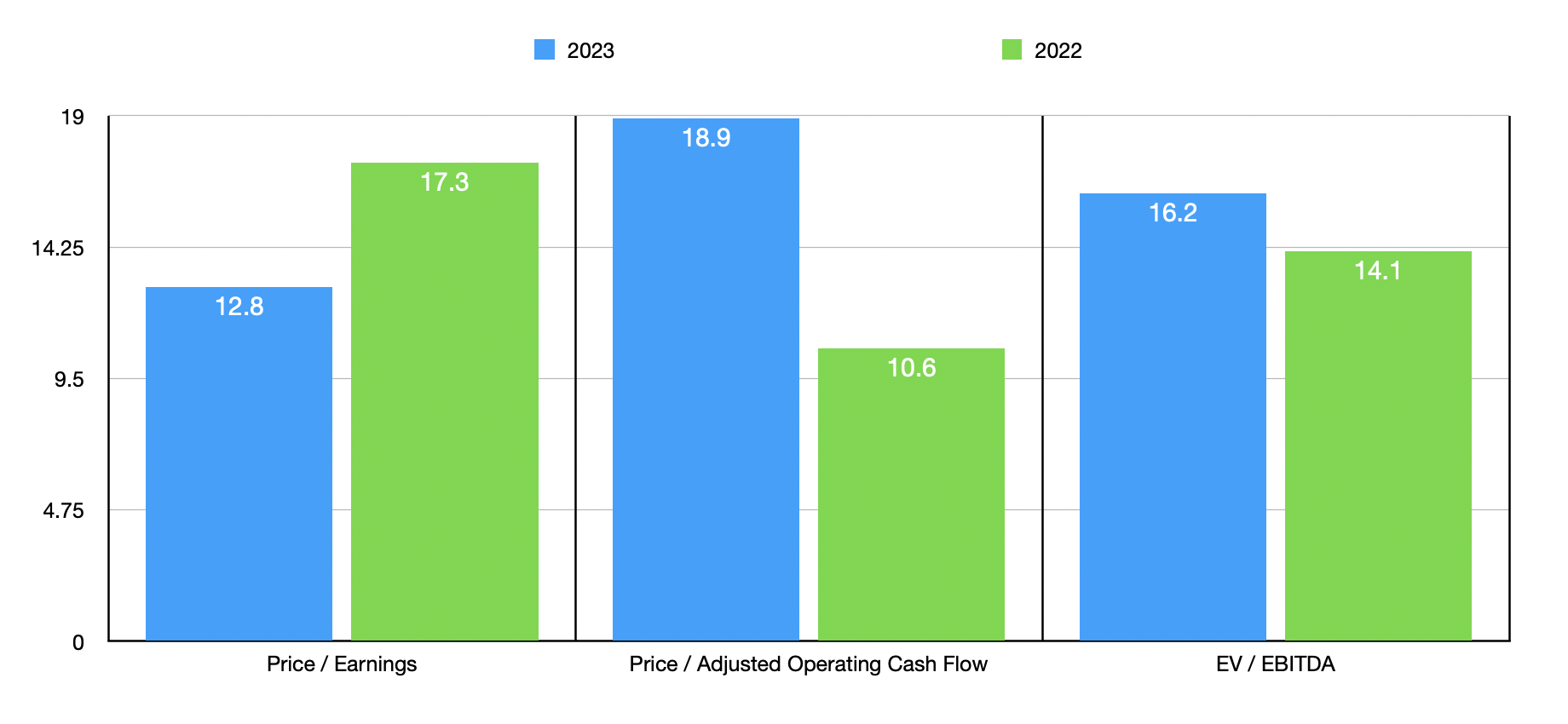

Using these figures, I was able to value the company on a forward basis. The end result can be seen in the chart above. Also in that chart is pricing for the company using data from 2022. In all, I wouldn't say that shares look expensive. In fact, they look quite affordable on a forward basis. As part of my analysis, I did also compare the company’s financials to those of five similar enterprises. The data here can be seen in the chart below. If we rely on the forward guidance then, on a price to earnings basis, Regal Rexnord ends up being the cheapest of the group. The same applies to the price to operating cash flow approach. And finally, when it comes to the EV to EBITDA approach, two of the five ended up being cheaper.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Regal Rexnord Corporation |

| 12.8 |

| 7.8 |

| 10.4 |

| Sensata Technologies ( ST ) |

| 16.7 |

| 12.3 |

| 9.9 |

| Hubbell Incorporated ( HUBB ) |

| 26.0 |

| 20.0 |

| 16.4 |

| Acuity Brands ( AYI ) |

| 13.8 |

| 10.5 |

| 8.5 |

| nVent Electric ( NVT ) |

| 16.1 |

| 15.0 |

| 11.7 |

| Generac Holdings ( GNRC ) |

| 29.0 |

| 145.3 |

| 14.3 |

Focusing more on the long term, it is worth keeping in mind that the company did recently acquire Altra Industrial Motion in a deal valued at $4.95 billion. Current guidance for 2023 already takes into consideration this transaction. The same holds true for my cash flow metrics for the company that I highlighted already. In the years that follow this year, management believes that some attractive upside exist. For starters, they're forecasting annualized cost synergies associated with the deal totaling $160 million by the fourth year following the completion of the purchase. By 2025, it's expected that the combined company will generate annual revenue of about $8.3 billion, with an EBITDA margin exceeding 25%. Even at 25%, this would translate to a reading of $2.08 billion. That's more than what I'm forecasting for the current fiscal year. If this does come to fruition, it could be very bullish for shareholders. But as with anything, it would be wise to wait and see how that picture unfolds before getting too excited.

Takeaway

Operationally speaking, the picture for Regal Rexnord has gotten a bit complicated. Its recent bottom line problems can be traced back to acquisition activity. This is good since that means its problems are transitory in nature. That realization, combined with expectations about the future that investors have thanks to the aforementioned acquisition, are the likely reasons for the firm's continued outperformance. Assuming that projected earnings for this year are indicative of how the firm's cash flow figures will look, the stock is trading on the cheap and likely has some decent upside from here. As such, I have no problem upgrading the business from a 'hold' to a 'buy.

For further details see:

Regal Rexnord: An Interesting Play Despite Recent Weakness