RRX - Regal Rexnord Corporation: Solid Company But Wait For Better Price Levels

2023-08-23 05:50:51 ET

Summary

- Regal Rexnord posted solid Q2 FY23 results with a significant increase in sales.

- The company's growth trajectory looks solid, with potential for even better results in the future.

- RRX is undervalued compared to its peers and has a lower valuation, but the technical chart indicates a correction might happen.

- Hence I assign a hold rating on RRX stock.

Regal Rexnord Corporation ( RRX ) manufactures power transmission components, air-moving products, and industrial powertrain solutions worldwide. The company operates in four segments: Industrial Systems, Motion Control Solutions, Climate Solutions, and Commercial Systems. RRX posted solid Q2 FY23 results with a significant increase in sales. I think RRX is undervalued with great growth potential. I will review its Q2 FY23 results in this report. I assign a hold rating on RRX because I think we might see a correction in the stock price in the near term.

Financial Analysis

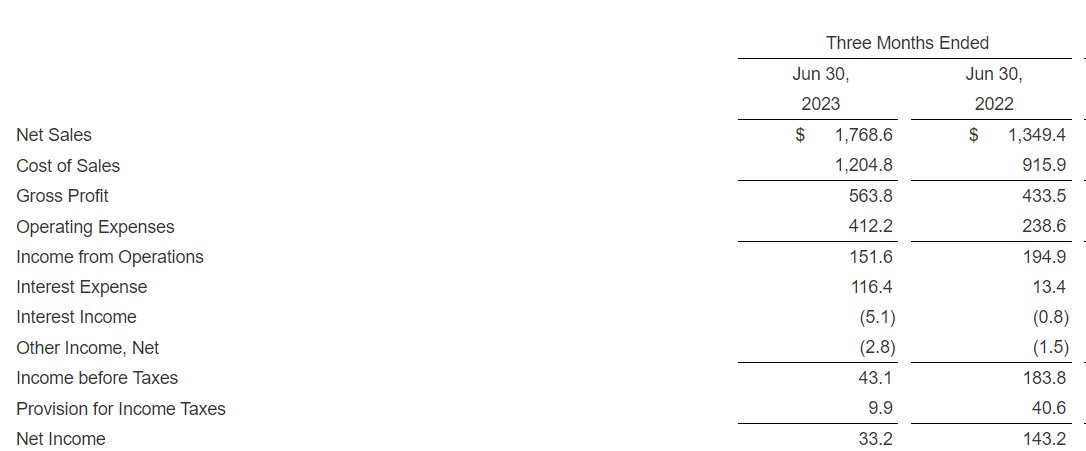

RRX announced its Q2 FY23 results . The sales for Q2 FY23 were $1.7 billion, a significant rise of 31% compared to Q2 FY22. I think increased sales in its automation & motion control and industrial powertrain solutions segments led to a significant rise in the company's net sales. The net sales from the AMC segment grew by 143.7% in Q2 FY23 compared to Q2 FY22. I think strength in the medical and data center market was the reason its AMC segment saw a significant rise in sales. The adjusted EBITDA margin in this segment was 25.3% which was 24.5%. I think volume growth was responsible for the improvement. In addition, this segment's backlog is considerably greater than usual. I think the Altra acquisition proved beneficial for the AMC segment because Altra has a rich portfolio which helped the company expand its sales in high-growth markets like aerospace and medical. I believe the AMC segment might be the primary driver of the company's sales in the coming times. The net sales from the IPS segment increased by 65.5% in Q2 FY23 compared to Q2 FY22. I believe strong demand in the energy and marine markets was the main reason behind the strong performance in the IPS segment. Its EBITDA margin in Q2 FY23 was up by 50 basis points due to the 80/20 approach and volume growth.

{kind=link}

The performance of RRX was extremely impressive this quarter. A 31% increase in sales is quite impressive, but I believe RRX has the potential to perform even better. In Q2 FY23, the company faced destocking headwinds that impacted its power efficiency solutions business and hampered its revenue growth. However, I think the destocking headwind might ease in the fourth quarter of 2023, benefiting its power efficiency solutions business. So I think we might see a rise in the company’s sales in the coming times. In addition, their Altra acquisition which they acquired in the month of March, is proving beneficial for them. The management was able to successfully integrate the acquisition into the business. The acquisition contributed nearly 40% of the sales in Q2 FY23. The Altra acquisition was made by the company in order to boost its business in high-growth markets like medical and aerospace, and the acquisition integrating well into the business is a positive sign because Altra has a portfolio that will complement the company’s AMC and industrial powertrain solutions segment. In addition, the acquisition brings an improved mix and new products, which I think might also improve the margins in the coming times. Hence I believe its growth trajectory looks solid, and in the coming times, we might see even better results which might positively affect its share price.

Technical Analysis

{kind=link}

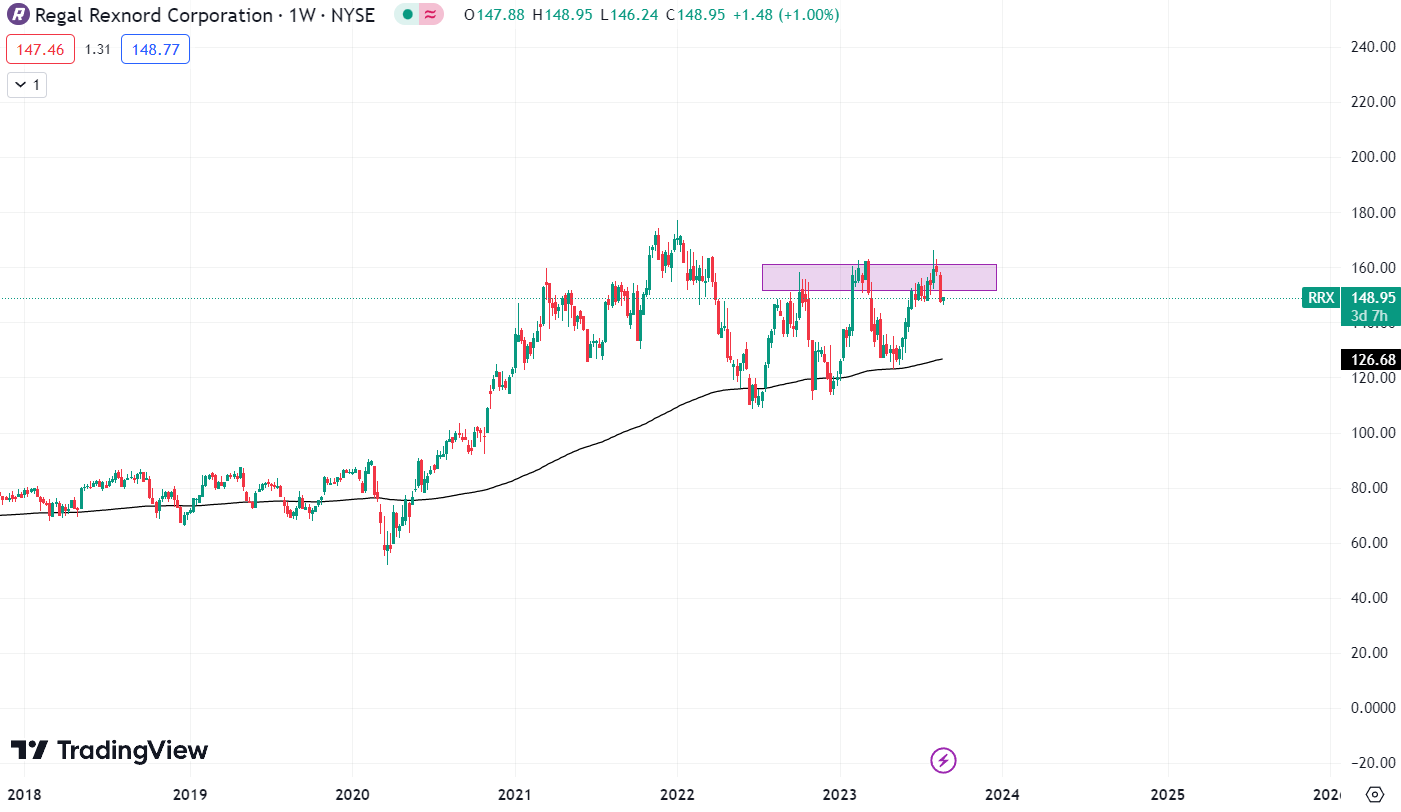

RRX is trading at $149. The stock is trading above the 200 ema, which shows that it is in an uptrend. In my view, the stock is looking bearish, and we might see a correction in the stock price in the near term. There is a strong resistance zone at the $162 level, and after touching the resistance zone, it has formed a big red candle. In the past, the stock twice touched the $162 level and was corrected both times. Hence I believe we might see a correction in the stock. I think the stock might correct 15% from the current level. So I believe one should avoid it for now. Buying opportunity will only arise when it reaches its 200 ema, which is at $127. Historically the 200 ema has been a strong support for the stock. So one can buy it when it touches the 200 ema.

Should One Invest In RRX?

Talking about RRX’s valuation. RRX has a P/E [FWD] ratio of 14.28x compared to its five-year average of 15.49x and the sector ratio of 17.52x. RRX has a PEG [FWD] ratio of 1.43x, lower than the sector ratio of 1.72x. Generally, high-growth companies like RRX trade at a higher valuation. But in this case, even after showing solid growth, the company is trading at a lower valuation, showing that RRX is undervalued. In addition, if we compare RRX to its peers like NVT , GNRC , and VRT , we can see that despite outperforming its peers, RRX is trading at lower multiples compared to its peers. RRX has a three-year revenue [CAGR] of 24.55% with a P/E [FWD] ratio of 14.28x, NVT has a three-year revenue [CAGR] of 13.1% with a P/E ratio of 17.94x, GNRC has a three-year revenue [CAGR] of 22% with a P/E ratio of 21.6x, VRT has a three-year revenue [CAGR] of 15.5% with a P/E ratio of 21.93x. So looking at the performance, I believe RRX is undervalued.

RRX has performed well financially, and its growth trajectory is looking solid. In addition, I like its valuation, but the technical chart indicates a correction in the stock, which I think is a great thing. Because I believe RRX might provide significant returns in the long term, and to get such an undervalued company at a discounted price will be a great deal. So I believe every correction in the stock will be a great buying opportunity. Hence despite solid results and low valuation, I assign a hold rating on RRX as I expect a correction to happen in the stock in the short term.

Risk

They rely on distributors' services in addition to their direct sales force and manufacturer sales reps to sell their products and give clients service and aftermarket support. They maintain a vast distribution network with more than 3,000 distributor sites worldwide. About 27% of their net sales from operations for the fiscal year that concluded on December 31, 2022, came from distributors. Nearly all of the distributors they do business with provide their clients with competitive goods and services. They also frequently have nonexclusive distribution agreements that can be terminated by the distributor with little advance notice. The company's sales and profitability could be significantly impacted by the loss of any significant distributors, a sizable number of lesser distributors, or an increase in the distributors' sales of their competitors' items to customers.

Bottom Line

RRX delivered solid financial results despite the destocking headwind. I expect them to perform better in the coming quarters, and I think they are undervalued. But I believe we might see a correction in the stock price in the near term. Hence I assign a hold rating on RRX, and I believe every correction in the stock will be a great buying opportunity.

For further details see:

Regal Rexnord Corporation: Solid Company But Wait For Better Price Levels