RRX - Regal Rexnord: Improving Growth Prospects And A Discounted Valuation

2024-01-09 17:06:28 ET

Summary

- Regal Rexnord's organic revenue growth is expected to turn positive in FY24 due to healthy backlog levels, improving end-market conditions, and potential interest rate cuts.

- The company's revenue growth was negatively impacted by inventory destocking, but this is expected to improve as inventory levels stabilize.

- The company's margin growth prospects are positive, driven by productivity improvements, cost-saving initiatives, and portfolio transformation.

Investment Thesis

Regal Rexnord Corporation's ( RRX ) organic revenue growth is poised to turn positive in FY24 driven by above-average backlog levels in the Industrial Powertrain Solutions ((IPS)) and Automation & Motion Control ((AMC)) segments, channel inventory destocking coming to an end, improving end-market conditions and a potential reversal in the interest rate cycle this year resulting in good demand recovery. In addition, the company has been strategically shifting its portfolio towards secular growth markets and, in line with this strategy, it acquired Altra Industrial Motion earlier last year and recently announced the divestiture of its industrial motor and generator business. Through these portfolio improvements, the company is targeting secular growth trends like electrification, a global regulatory push to improve energy efficiency, increasing levels of global factory automation, etc., which bodes well for its medium to long-term revenue growth.

On the margin front, the company should benefit from productivity improvement and cost-saving programs like 80/20 and lean initiatives and synergy benefits from Rexnord PMC and Altra integration. Further, as the end-market demand improves and volume recovers as FY24 progresses, the company's margins should also see an improvement from operating leverage. Moreover, the stock is trading at a discount compared to its historical averages. Considering the company's improving growth prospects and discounted valuation, I have a buy rating on RRX stock.

Revenue Analysis and Outlook

Over the last few years, RRX has seen strong growth thanks to good end-market demand and accretive acquisitions. However, a more normalized demand environment and channel partners and customers reducing their inventory levels in response to improving supply chain conditions (decreasing lead times) negatively impacted the company's organic sales growth in recent quarters. In the third quarter of 2023, the company's net sales increased 24.5% Y/Y to $1.649 billion driven by a 34.9% contribution from the Altra acquisition and a 0.4% favorable impact of FX translation, partially offset by a 10.8% Y/Y decline in organic sales.

RRX's Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, I believe we are close to the bottom in terms of organic revenues and the company should return to Y/Y organic growth in the coming quarters.

If we look at the company's results, its organic growth was negatively impacted last year by inventory destocking across the segments, especially in the short-cycle businesses. This was a result of the company's channel partners and customers reducing inventory in response to normalizing lead time and easing supply chain constraints, as well as some weakness in the end markets given the current high-interest rate environment. However, I believe we are close to the end of inventory destocking as inventory across channels is in much better shape after several quarters of destocking. Management also noted that destocking in some of the end markets like residential AC is now complete. Further, with a potential reversal in the interest rate cycle this year, some of the company's short-cycle businesses should also start seeing good demand recovery which should help end destocking.

On its last earnings call , management also noted sequential improvement in orders in October. With the market sentiment improving further in November and December due to commentary around the interest rate cuts in 2024, I expect continued improvement in order trends when the company reports its Q4 earnings.

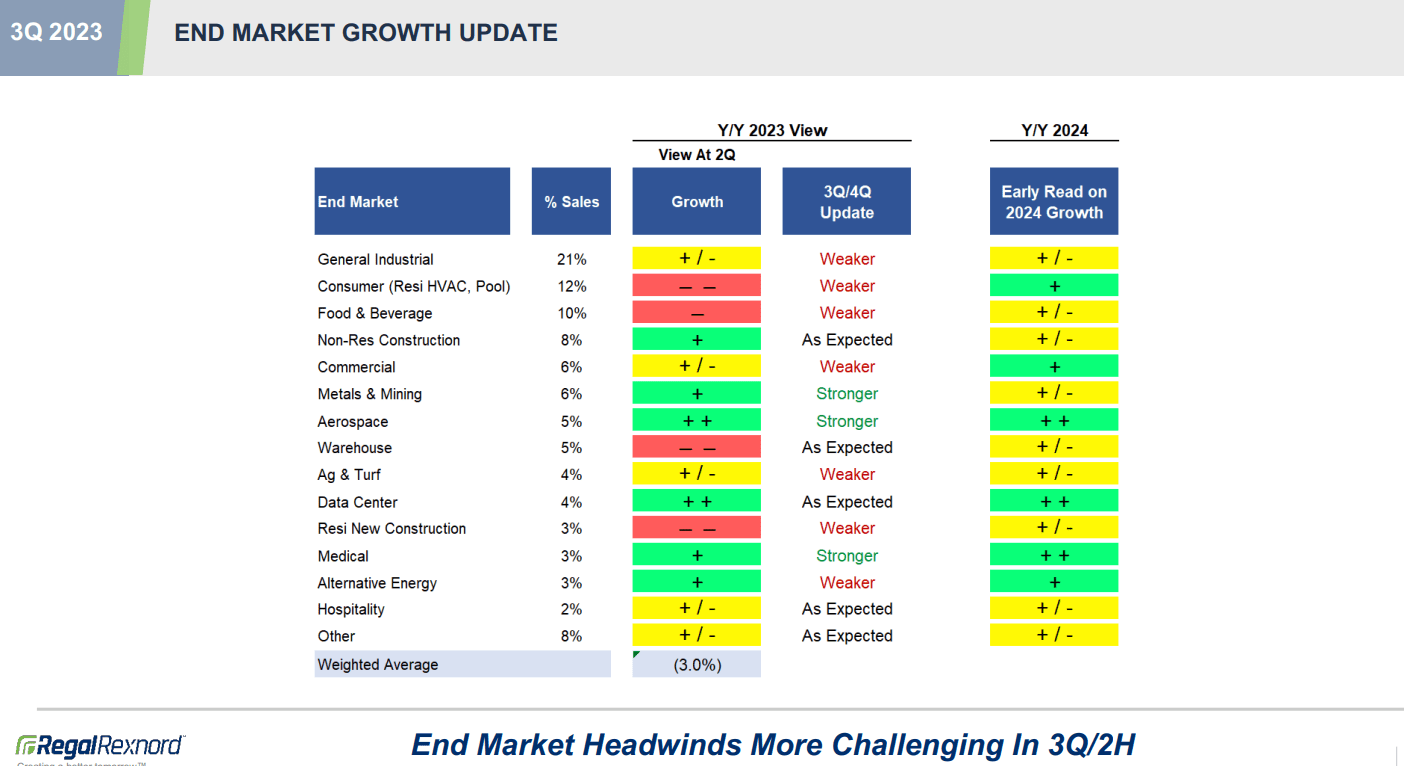

In addition to improving order trends, the company should also benefit from higher than normalized backlogs in IPS and AMC segments. According to management, the backlog in IPS and AMC segments were ~45% and 50% above their normal levels, respectively, at the end of Q3 2023.

The outlook for the company's end markets is also improving. At the time of the last earnings call, management shared an early read on 2024 trends where it was neutral on General Industrial (~21% of sales), non-res construction (~8% of sales), and residential construction (~3% of sales). I believe the outlook of these end markets has meaningfully improved since the time of the last earnings call due to increased expectations of multiple interest rate cuts in 2024. A lower interest rate improves the attractiveness of construction projects as well as stimulates demand in the general industrial sector. So, I am expecting incrementally positive commentary around these markets on the next earnings call.

RRX's Early Read on 2024 End Market Growth (Company's Q3 2023 Earnings Presentation)

{kind=link}

The improved outlook for these end markets coupled with anticipated strength in the consumer market, which should benefit from residential HVAC recovery as inventory destocking ends; improving food and beverage end market, which should benefit from subsiding project-timing related issues and delays which the company saw in the last couple of quarters; and benefit from government stimulus programs like the CHIPS and Science Act and Inflation Reduction Act which are encouraging reshoring. This bodes well for the company's growth in 2024.

The company has also done a good job in terms of portfolio transformation and has steadily increased its exposure to secular markets, including aerospace, warehouse, food & beverage, medical, alternative energy, and data centers. The recent Altra Industrial Motion Corporation acquisition (acquired in March 2023) has increased the company's exposure to the secular growth markets to 37% of the company's sales. When factoring in residential HVAC, driven by consistent regulatory efforts to enhance energy efficiency, the exposure rises to approximately 50%. This portfolio transformation positions the company to capitalize on several secular tailwinds, including a global regulatory push to improve energy efficiency, the reshoring of manufacturing, electrification, an aging population, increasing levels of global factory automation, etc., which should help its sales growth in the medium to long term.

RRX End Market Exposure (Company Presentation)

In summary, I am optimistic about the company's revenue growth prospects fueled by inventory destocking ending, improving order rates, healthy backlog levels, improving end market conditions, the upcoming reversal in the interest rate cycle in FY24, secular growth tailwinds, portfolio transformation, and federal stimulus programs encouraging reshoring trends.

Margin Analysis and Outlook

In Q3 2023, the IPS segment's adjusted EBITDA margin contracted by 690 bps Y/Y mainly due to an unfavorable mix related to short-cycle weakness in the higher-margin aftermarket channel and an impact of $10 million of temporary costs aimed at maintaining high customer service levels during a period of footprint changes related to PMC cost synergies. In the PES segment, the adjusted EBITDA margin expanded by 310 bps Y/Y attributed to positive price/cost, improved operational efficiency, lower freight, and favorable mix which more than offset the impact of lower volumes. The AMC segment's adjusted EBITDA margin declined 10 bps Y/Y on a reported basis. However, on a pro forma basis, the adjusted EBITDA margin increased by 130 bps Y/Y due to favorable price/cost, improved operational efficiencies, benefits from 80/20 initiatives, and cost control. The Industrial Systems' adjusted EBITDA margin decreased by 470 bps Y/Y mainly due to lower volumes.

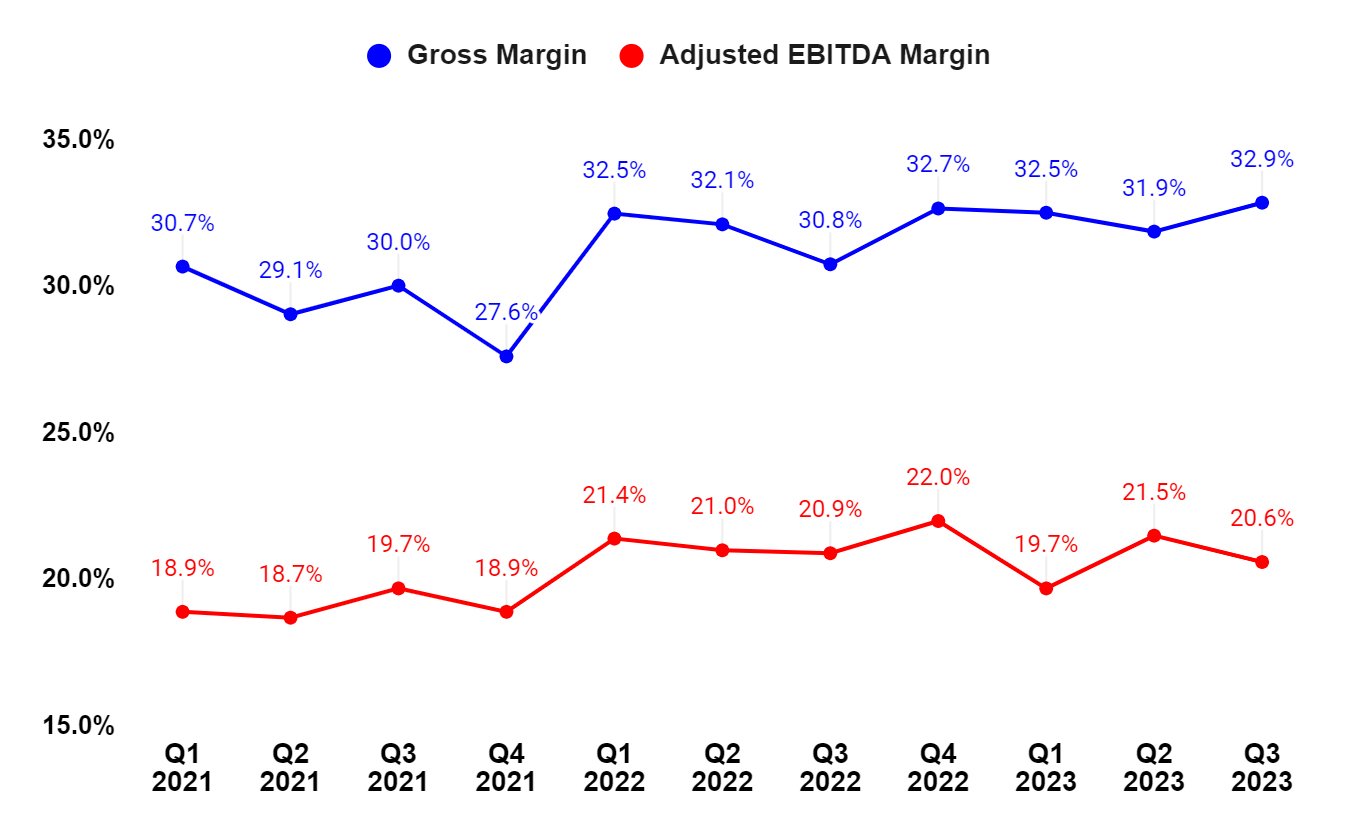

On a consolidated basis, the gross margin improved by 210 bps Y/Y to 32.9% while the adjusted EBITDA margin declined by 30 bps Y/Y, or 10 bps Y/Y on a pro forma basis, to 20.6%.

RRX's Segment-Wise Adjusted EBITDA Margin (Company Data, GS Analytics Research) RRX's Gross Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

{kind=link}

{kind=link}

Looking forward, I am optimistic about the company's margin growth prospects.

The company is doing a good job in terms of productivity improvement and cost-saving initiatives like implementing the 80/20 strategy, lean initiatives, and achieving synergy benefits from the integration of Rexnord PMC and Altra acquisitions. Management expects to realize cost synergies of $13 million from PMC and $10 million from Altra in the fourth quarter, and $45 million from PMC and $45 million from Altra in 2024. In addition, the Altra acquisition brings an improved mix and new products to the company's IPS and AMC portfolio which should also help the margin mix in the coming quarters.

Further, the company's recently announced sale of its industrial motors and generators businesses for cash proceeds of $400 million, which is scheduled to close in the first half of 2024, should help improve the margin mix of the portfolio. Management is expecting the company's gross margin and adjusted EBITDA margin to increase by over 100 basis points as a result of this transaction.

Management has shared the target of achieving a 40% gross margin and a 25% adjusted EBITDA margin by 2025, mainly driven by M&A synergies, 80/20 and lean initiatives, and accretive new product developments. The divestiture of the industrial motor and generator business would help the company achieve this target. Further, as the end market conditions improve and the volume recovers, the resulting operating leverage should also help in margin expansion in the near as well as long term.

Valuation and Conclusion

RRX is currently trading at a 13.22x FY24 consensus EPS estimate of $10.56 which is at a discount compared to its 5-year average forward P/E of 15.55x.

While the company has historically traded at a discount to the broader EE/MI sector, the recent portfolio transformation initiatives and progress towards achieving higher growth/higher margin portfolio mix should help it P/E multiple re-rate versus its historical levels and industry averages.

Recently, Goldman Sachs also mentioned the company among their top industrial picks citing improving fundamental metrics and top quartile EPS growth potential indicating that Wall Street analysts are warming up to the story.

I believe the company's return to organic growth next year should help improve investor sentiment around the stock. The margin prospects are also solid, and the stock trading at a discount to its historical averages provides a good entry point. So, I have a buy rating on the company.

Risks

- I expect an improvement in the general industrial and construction end market this year as the interest rate cycle reverses. If there is any delay in rate cuts or the pace is slower than expected, or it doesn't have the intended impact in terms of improving the growth outlook in the industrial and construction sector, the valuation multiple re-rating I am expecting may not happen.

- Inorganic growth is relatively riskier compared to organic growth as there are risks associated with post-acquisition integration, the company overpaying for an acquisition, and the leverage a company takes to make an acquisition. If the company doesn't realize intended synergies or overpays for an acquisition, the stock price can see some downside.

For further details see:

Regal Rexnord: Improving Growth Prospects And A Discounted Valuation