RRX - Regal Rexnord: Risky But Guidance And Secular Growth Imply Undervaluation

2023-05-25 11:48:22 ET

Summary

- Regal Rexnord Corporation is a global engineer and manufacturer of industrial power and mobility solutions.

- I believe that Regal Rexnord will be able to get more exposure to markets with secular growth as it is one of the number one initiatives of management.

- It is also worth noting that Regal Rexnord recently reported a re-segmentation process, which significantly reduced the number of business units.

Regal Rexnord Corporation ( RRX ) recently reported an increase in the guidance for the year 2023 as a result of the acquisition of Altra. I am optimistic about the outcome of the merger integration. I also believe that further investments in markets with secular growth could bring further FCF generation. Even taking into account potential M&A integration failure, risks from the total amount of debt, and failed restructuring of business units, I believe that the stock could trade higher.

Business Model And Recent Guidance Increase

Regal Rexnord Corporation is a global engineer and manufacturer of industrial power and mobility solutions, including power transmission components, electric motors and electrical controls, airborne motion products, and general electronic solutions.

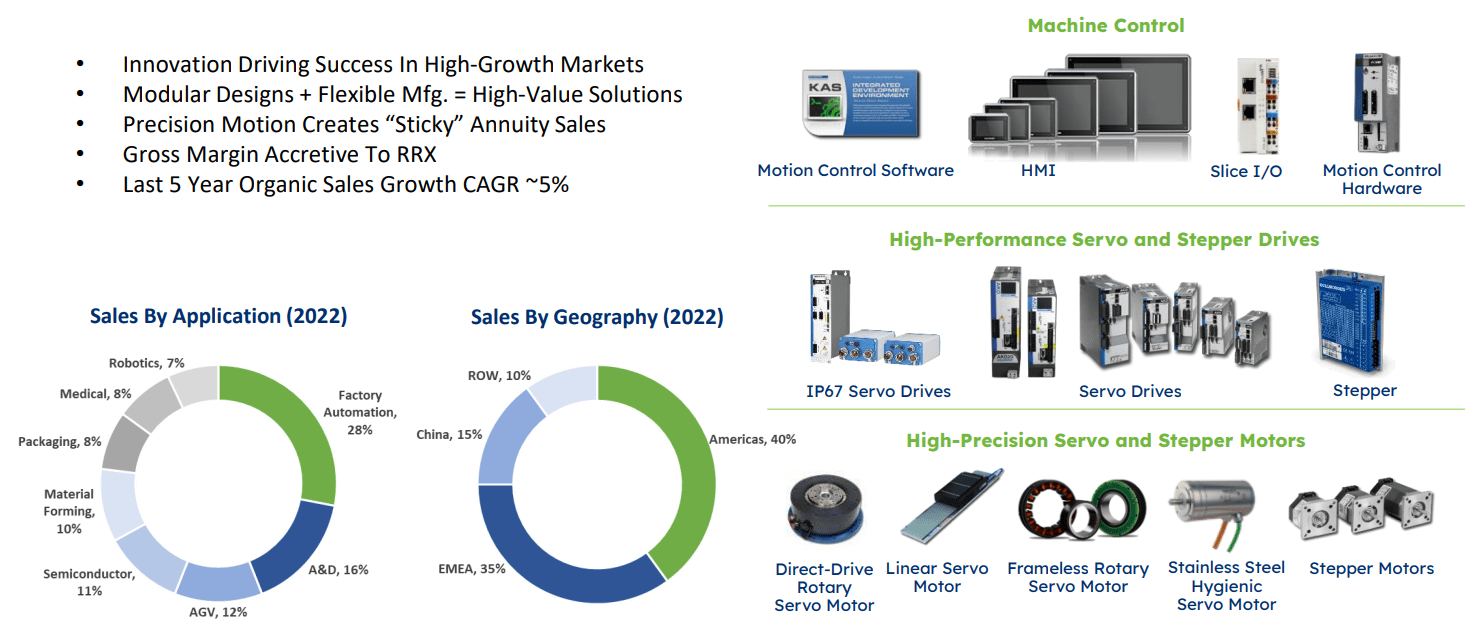

The company is based in Wisconsin, and has manufacturing, distribution, and customer service facilities internationally. 40% of total sales comes from America, but the company also sells in China and the EMEA region. I believe that the international exposure will likely bring some stability to the revenue line in case of a global recession.

Source: 2023 1st Quarter Earnings Presentation

{kind=link}

Company's operations are divided into four segments: commercial systems, industrial systems, motor control and solutions, and climate solutions. Each of these segments develops products of high technological complexity that serve end consumers and original manufacturers from various industries. These products include high voltage conditioning systems, power line transmission solutions, electric motors for factory operation, mechanical transmission, or security installations, specific electronic components, components for the aeronautical industry, and internal transportation systems.

The largest amount of revenue comes from original manufacturers and companies dedicated to industrial refrigeration or conditioning systems. They are a fundamental and structural part of the development and operation chains of their clients.

{kind=link}

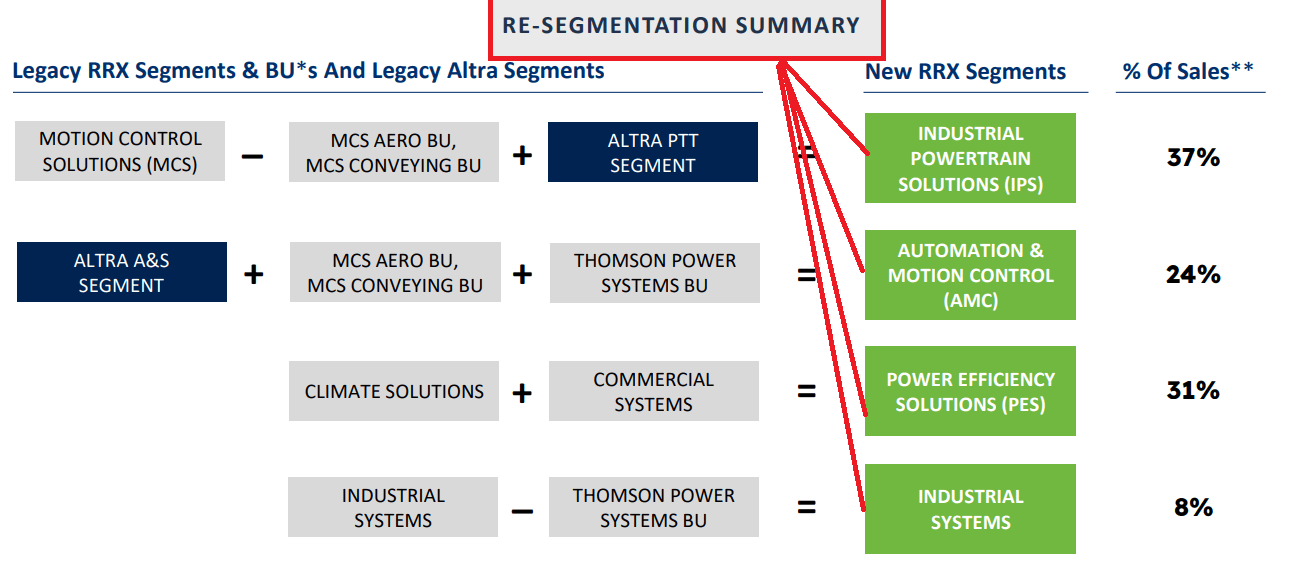

It is also worth noting that Regal Rexnord recently reported a re-segmentation process, which significantly reduced the number of business units. I believe that we can expect a reduction in reporting and auditing costs as well as more business flexibility. I believe that further restructuring may be expected, and may be celebrated by market participants.

Source: 2023 1st Quarter Earnings Presentation

{kind=link}

I believe that the optimistic tone reported in the last quarterly report is remarkable. Management noted incoming benefits from M&A strategies, enhancement of the product mix, and several productivity initiatives. Among the commentaries given in the last quarterly report, the following words are, in my view, very important.

We expect benefits from merger and acquisition synergies, improving new product mix, ongoing 80/20 initiatives and various productivity initiatives to be more than offset by headwinds from lower volumes, material and non-material inflation, strategic growth investments, a higher tax rate and higher net interest expense. Source: 10-Q

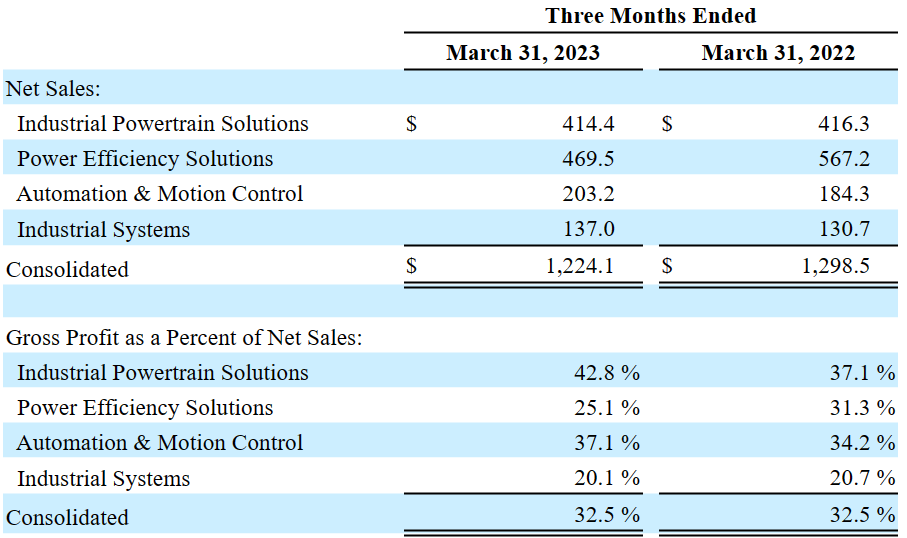

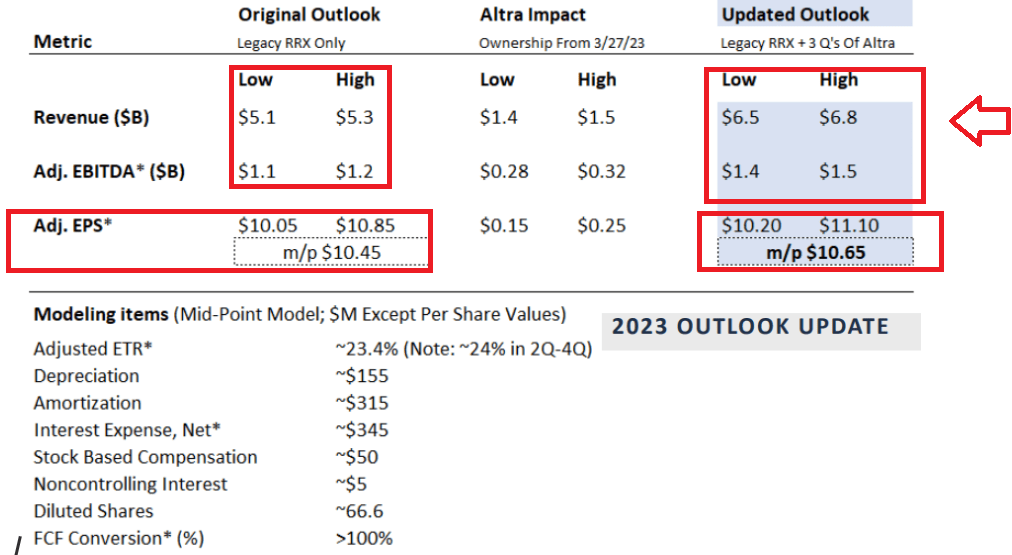

Finally, I am interested in the increase in outlook reported for the year 2023. Both the revenue growth and the Adjusted EBITDA expected for 2023 are a bit better than that in previous reports. We would be talking about revenue of close to $6.5 billion and Adjusted EBITDA close to $1.4 billion. It is also quite favorable that management offered a lot of information about future D&A, stock based compensation, and interest expense among other financial figures. DCF modelers will likely appreciate the substantial amount of information given by management.

Source: 2023 1st Quarter Earnings Presentation

{kind=link}

Regal Rexnord Reports A Considerable Amount Of Debt

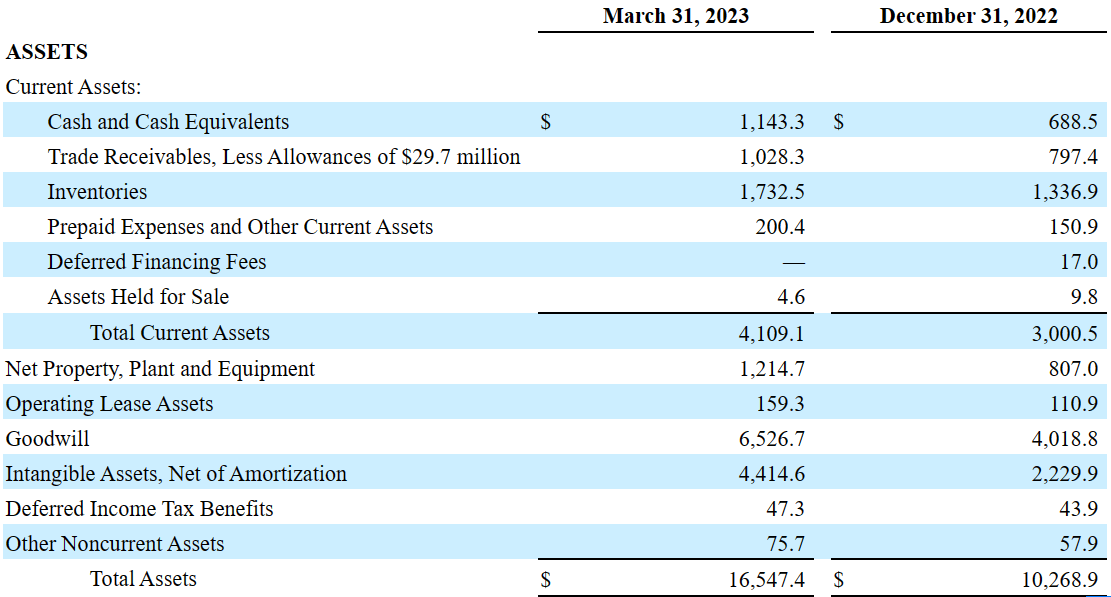

As of March 31, 2023, management reported cash and cash equivalents worth $1.143 billion, trade receivables worth $1.028 billion, and inventories of $1.732 billion.

Also, with prepaid expenses and other current assets around $200 million, total current assets are close to $4.109 billion, about 3x the total amount of current liabilities. I am not concerned about the liquidity inside Regal, however I think that long-term debt may be monitored by investors.

Non-current assets include net property, plant and equipment worth $1.214 billion, operating lease assets close to $159 million, goodwill of $6.526 billion, and intangible assets of $4.414 billion.

{kind=link}

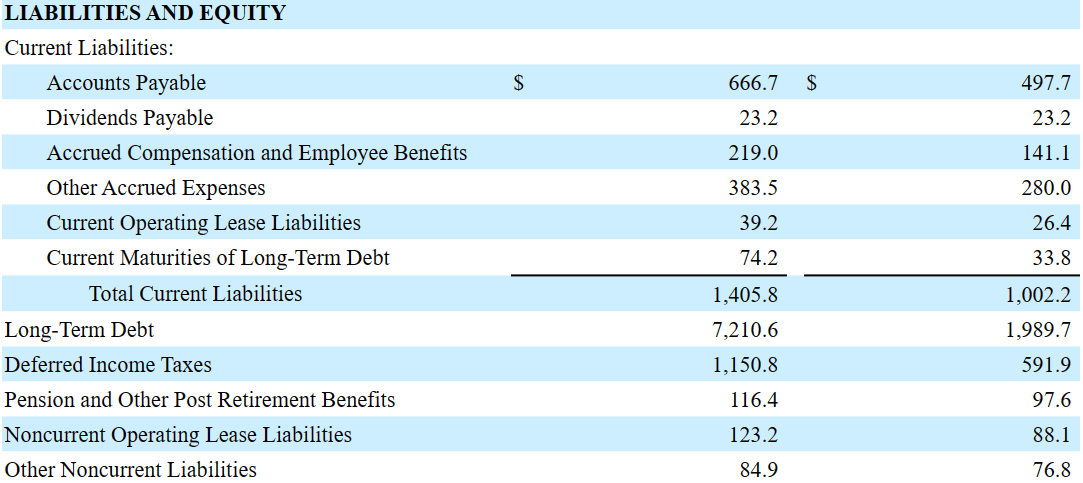

The list of liabilities includes accounts payable close to $666 million, dividends payable worth $23 million, accrued compensation and employee benefits worth $219 million, current operating lease liabilities close to $39 million, and current maturities of long-term debt of $74 million.

Long-term debt stands at close to $7.210 billion, which does not seem small. Besides, the company accumulated deferred income taxes of $1.150 billion and pension and other post-retirement benefits worth $116 million.

{kind=link}

The list of contractual obligations includes due payments of close to $1.5 billion in 3 to 5 years. I believe that the FCF may be sufficient to pay some of these obligations. I also believe that management may have to renegotiate with debt holders, or look for other types of financing sources.

{kind=link}

Competitors

In the commercial, industrial, and climate solution systems segments, the company participates in a market made up of both international manufacturers and domestic and regional developers. Due to its wide range of products and the variety of customers it serves, competition is given in a fragmented way. In some cases, it competes with companies that have a wide and similar product offering. It also competes with manufacturers of specific or niche products that create pressure in a given market.

Specifically, in the manufacture of electric motors, the competition is significant. A large number of manufacturers located in Europe, China, India, and Japan intend to penetrate more deeply into international markets and the local market of the United States, where Regal Rexnord Corporation has led the initiative in this regard in recent years.

With regard to mobility systems and solutions, competition occurs in an even more fragmented manner, by large companies and local service providers, thanks to the development of technology in this regard and the large number of applications in different phases of the processes.

Under My Cash Flow Model, I Obtained A Valuation Of $163 Per Share

According to the last annual report, Regal seeks to transform the business into a faster-growing business, increasing margins and generating greater amounts of return for its shareholders. Under my cash flow model, Regal Rexnord will successfully reach these objectives.

I believe that Regal Rexnord will likely be able to improve its gross margin and operating margin as well as to accelerate earnings growth. If the company successfully manages to control an eventual increase in commodity prices, salaries, or components, I believe that we can expect that economies of scale may bring further EPS growth.

Our cost of sales consists of costs for, among other things raw materials, including copper, steel and aluminum; components such as castings, bars, tools, bearings and electronics; wages and related personnel expenses for fabrication, assembly and logistics personnel; manufacturing facilities, including depreciation on our manufacturing facilities and equipment, insurance and utilities; and shipping. Source: 10-Q

In line with the previous words, it is worth noting that Regal Rexnord successfully manages to increase prices to customers, and signs long-term contracts with clients. I assumed that management will be able to do the same in the future.

When we experience commodity price increases, we have tended to announce price increase to our customers who purchase via purchase order, with such increases generally taking effect a period of time after the public announcements. For those sales we make under long-term contracts, we tend to include material price formulas that specify quarterly or semi-annual price adjustments based on a variety of factors, including commodity prices. Source: 10-Q

I also believe that Regal Rexnord will be able to get more exposure to markets with secular growth as it is one of the number one initiatives of management. Further investments in these markets will most likely accelerate exposure to the rising energy efficiency requirements, which, in my view, could represent a revenue catalyst.

We are focused on growing our position in prioritized secular growth markets, including some with strong regulatory tailwinds tied to rising energy efficiency requirements. These markets include the food and beverage, alternative energy, aerospace, water, warehouse/eCommerce, pharmaceutical and data center markets. We plan to direct a significant portion of our growth investments to end markets with secular growth characteristics. Source: 10-Q

Source: 2023 1st Quarter Earnings Presentation

The objectives of the company include keeping a portfolio of products with brands that remain in the long term, providing a greater offer of growth subsystems, using to its advantage the capacities and flexibility of its production and manufacturing capacity at an international level, and the growth of assets in its portfolio.

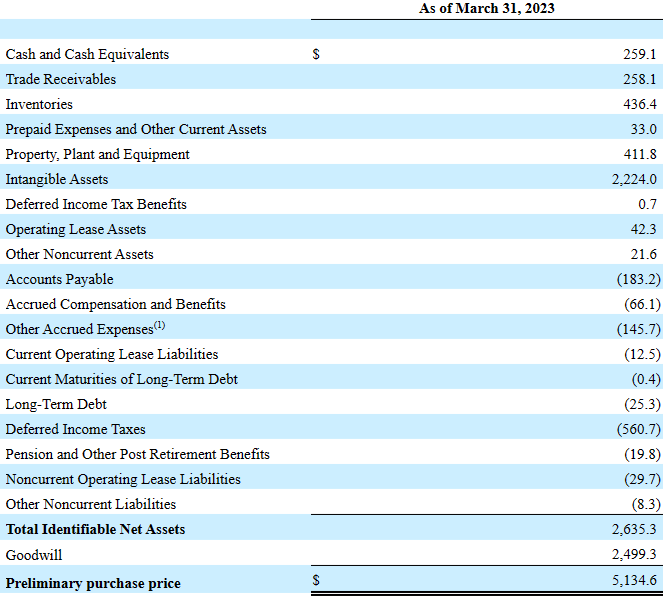

In addition, I assumed that Regal Rexnord will continue to conduct an exhaustive search for emerging acquisition and merger opportunities, always keeping in mind the main objectives of expanding operations based on improving the margin, achieving faster growth, and increasing the cash return of the operations. Besides, if the company successfully integrates Altra, I believe that future synergies could represent a lot of FCF growth for Regal Rexnord. It is worth noting that among the assets acquired in the transaction, management noted goodwill worth $2.49 billion, which is close to 49% of the total amount of assets acquired.

{kind=link}

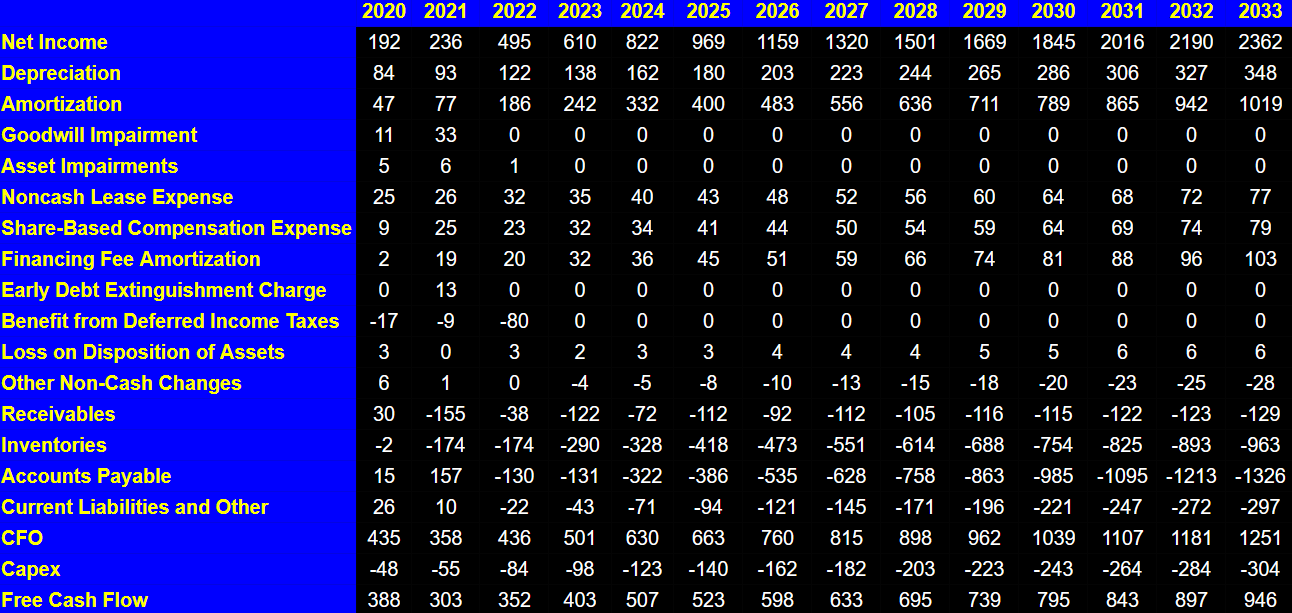

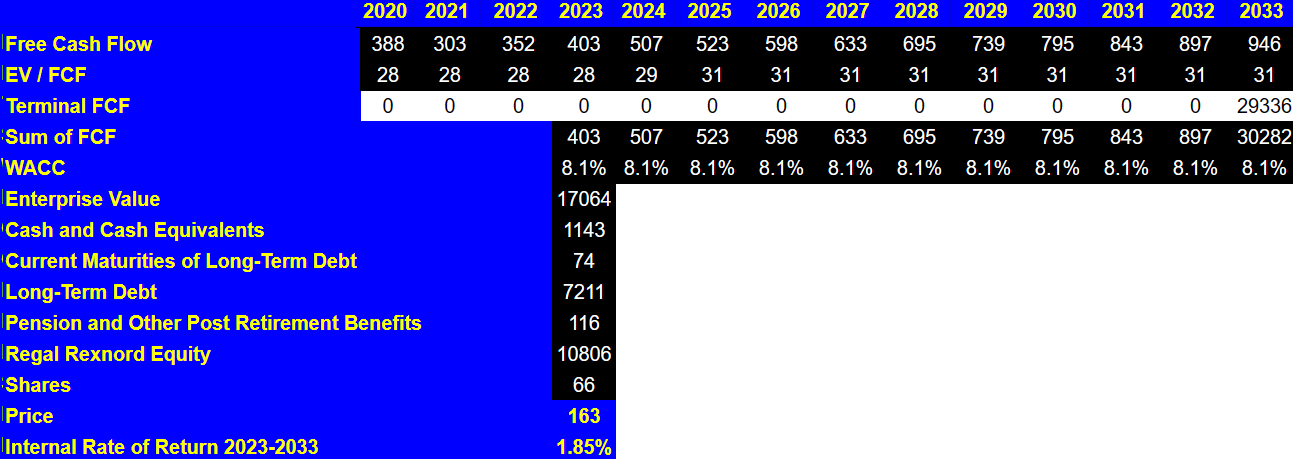

My cash flow model includes 2033 net income close to $2.361 billion, depreciation of $348 million, and amortization of around $1.018 billion. Also, with share-based compensation expenses close to $78 million and financing fee amortization of around $102 million, I included changes in receivables of -$129 million. Assuming inventories close to -$963 million and changes in accounts payable of -$1.327 billion, 2033 CFO would be close to $1.250 billion. Finally, if we include capex of -$305 million, the free cash flow would be around $946 million.

{kind=link}

By assuming an EV/FCF of close to 31x, which appears a conservative ratio, I obtained 2033 terminal FCF close to $29.336 billion. If we also assume a WACC of 8.1%, the enterprise value would stand at $17.064 billion.

If we also add cash and cash equivalents worth $1.143 billion, current maturities of long-term debt of $74 million, long-term debt worth $7.210 billion, and pension and other post-retirement benefits worth $116 million, the price would stand at close to $163 per share.

{kind=link}

Risks

Regal Rexnord depends on the prices of certain raw materials and the ability to maintain and improve contracts with its suppliers. The elements of risk at the operational level for the company include the factor that production volumes are high and may not match the needs of available demand as well as the fact that most of the sales are destined to specific industries.

It is also necessary to consider the exposures to international trade, such as variations in exchange rates, regulations, and tariffs for the export and import of products, or the conditions of the global and local economy that may affect the production chain in certain territories.

In addition, the restructuring of the business model may mean a risk factor in case of not having the capacity to do so or the inability to adapt to the operational demands. Besides, I believe that we could expect some complications coming in the process of integration of Altra. In my view, reduction in the total amount of goodwill may bring lower book value per share, and may affect FCF expectations and the stock price dynamics.

Finally, I believe that drastic changes in the credit markets may affect the ability of management to refinance the debt. As a result, I believe that Regal may have to pay more for financing, or may not find financing at all. In the worst case scenario, I believe that we may see a deterioration in the FCF margins and lower stock valuation.

Conclusion

Regal Rexnord recently increased its outlook for the year 2023 thanks to the acquisition of Altra. Even if the market does not seem to appreciate the recent quarterly report, I believe that management is smart. Increasing exposure to markets with secular growth is beneficial. Besides, if management continues to successfully increase prices to customers, and signs long-term contracts, in my view, inflation may not harm FCF generation. Even considering risks from the total amount of debt, M&A failures, or failed restructuring, I believe that the stock could trade at higher marks.

For further details see:

Regal Rexnord: Risky, But Guidance, And Secular Growth Imply Undervaluation