REIT - REIT Earnings Preview: When The Tide Goes Out

2023-04-25 10:00:00 ET

Summary

- Real estate earnings season kicks into gear this week, and over the next month, we'll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies.

- This report discusses the major high-level themes and metrics we'll be watching across each property sector. We're particularly focused on commentary regarding cap rates, acquisition prospects, and dividend sustainability.

- The flat performance on the REIT Index this year hides some notably sharp bifurcations within the sector, with residential and industrial sectors posting notable outperformance, offset by weakness in office.

- Many well-capitalized REITs are equipped to "play offense" and take advantage of acquisition opportunities from weaker private players - but whether or not these typically-defensive REITs are ready to take a more aggressive tact remains a key focus.

- Most equity REITs still have a healthy buffer to protect current payout levels if macroeconomic conditions take a turn for the worse, but we'll be closely-monitoring dividend commentary in the office, mortgage, and healthcare REIT sectors.

Real Estate Earnings Preview

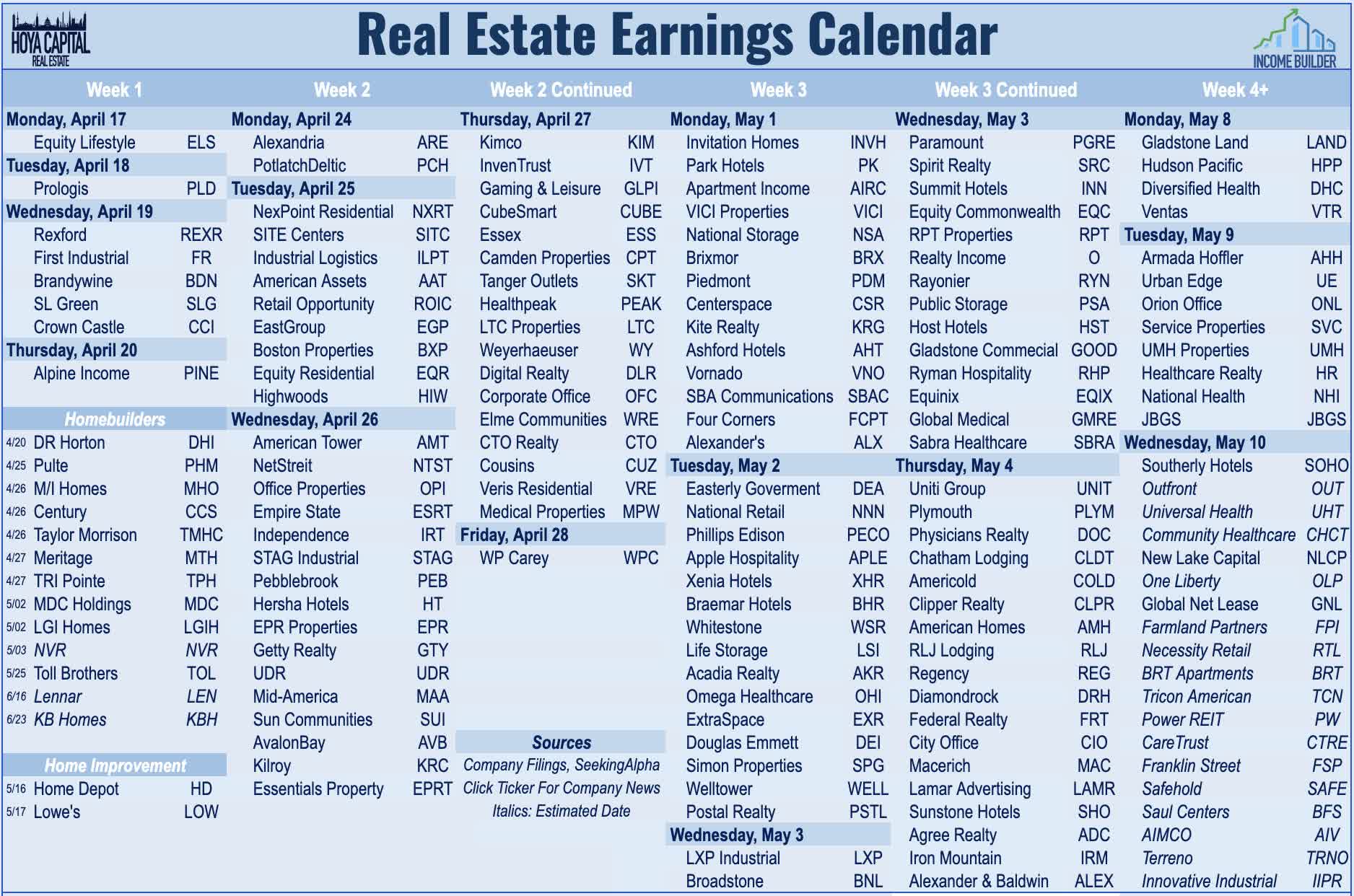

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on April 23rd.

{kind=link}

Hoya Capital

Real estate earnings season kicks into gear this week, and over the next month, we'll hear results from more than 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies which will provide key insights into how the real estate industry is adapting to the "new normal" of higher interest rates and to the tremors of instability felt across global financial markets during the quarter. This report discusses the major high-level themes and metrics we'll be watching across each of the real estate property sectors this earnings season. Below, we compiled the earnings calendar for equity REITs and homebuilders.

{kind=link}

Hoya Capital

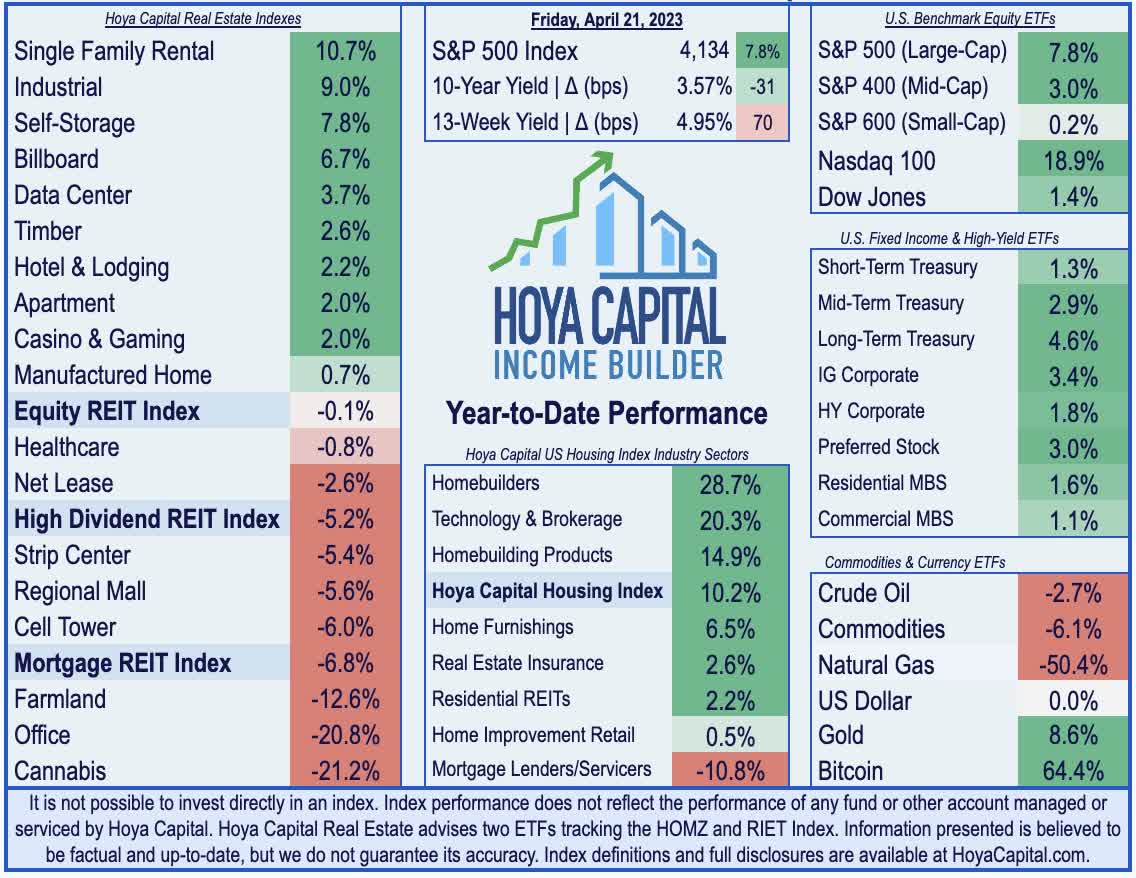

Real estate equities enter earnings season as one of the weaker-performing asset classes of 2023, with the Vanguard Real Estate ETF ( VNQ ) lower by 0.1% on the year, underperforming the 7.8% advance on the S&P 500 ( SPY ). The flat performance on the REIT Index this year hides some notably sharp bifurcations within the sector, however, with residential and industrial sectors posting notable outperformance, offset by weakness in the office and retail sectors. The sluggish start to the year follows the sector's second-worst year on record in 2022, in which the REIT benchmark slid by more than 25%, pressured by stiff headwinds from higher interest rates and elevated inflation. Despite the pull-back in interest rates in the wake of the banking turbulence in early March, however, REITs still haven't fully regained their footing amid concern over credit availability and higher cost of capital.

{kind=link}

Hoya Capital

Before diving into the specific sector-by-sector metrics we're focused on this earnings season, we discuss the four higher-level themes that we're focused on this earnings season:

- Cap Rates, Valuations, and Credit Conditions

- Acquisition Plans & Distress Opportunities

- Balance Sheets & Variable Rate Debt Exposure

- Full-Year 2023 Guidance Updates

1) Cap Rates, Valuations, & Credit Conditions

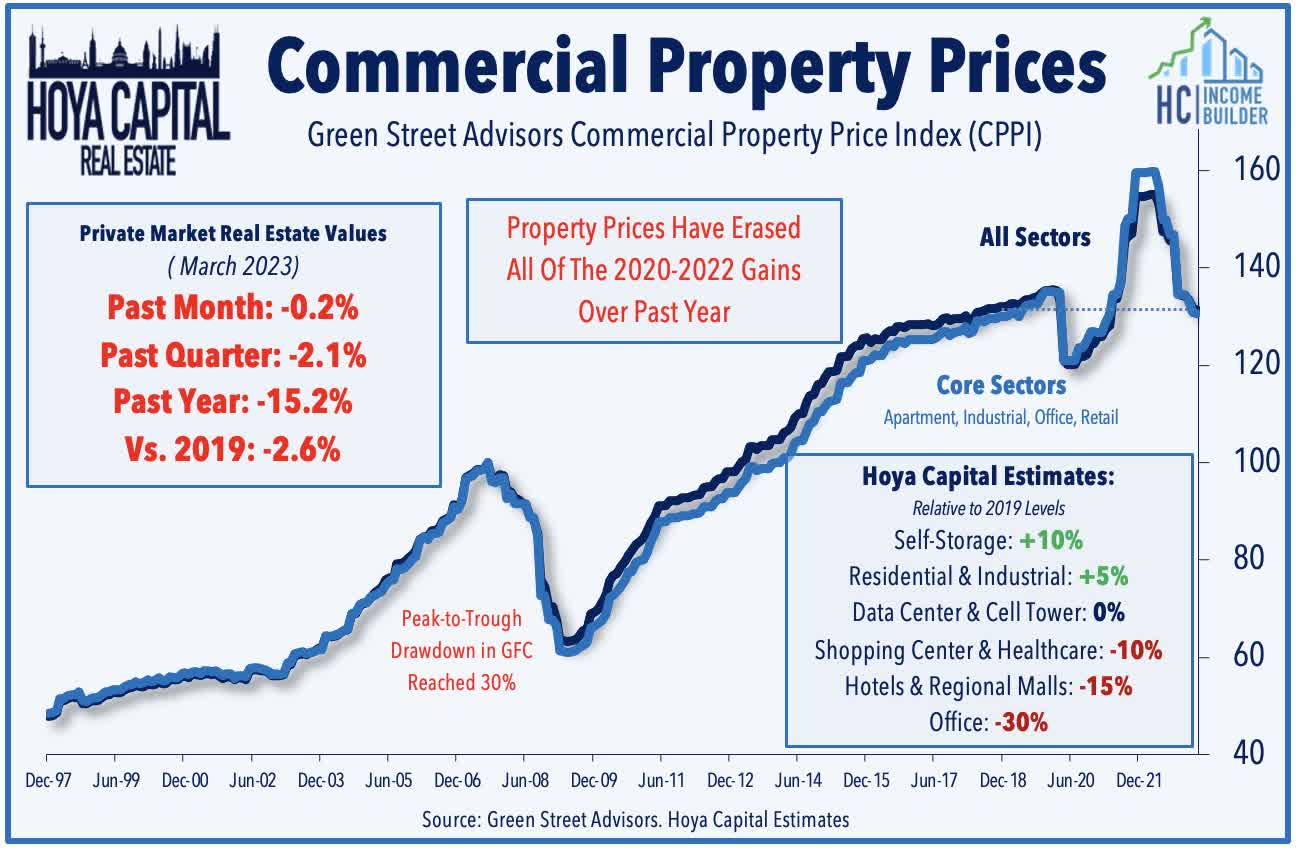

This active debate has been playing out across the U.S. real estate industry - a unique "dual market" structure with both an active public and private market. Private real estate markets are finally "catching up" to the reality of sharply higher interest rates - and expectations that rates may be "higher for longer" - which have been reflected in public real estate markets since mid-2022. Recent Green Street Advisors data shows that private market real estate values have declined about 15% from their peak in 2022 and now sit about 3% below pre-pandemic levels at the end of 2019. While transactions have been few-and-far-between given the wide bid-ask spread in commercial real state markets, commentary regarding estimated capitalization rates ("Cap Rates") - and by extension, real estate valuations - will be closely watched.

{kind=link}

Hoya Capital

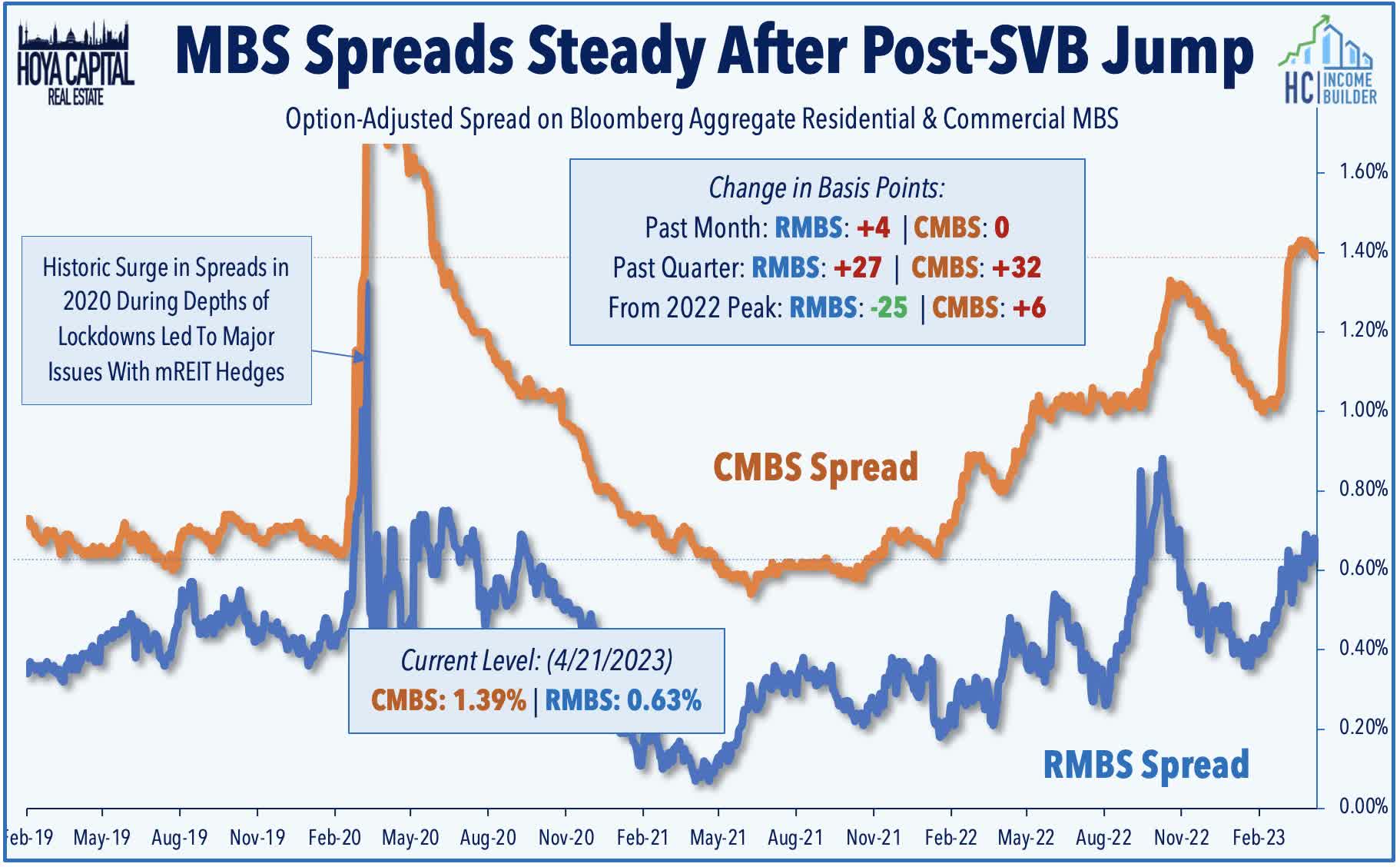

We've kept our eyes on the underlying Residential MBS ( MBB ) and Commercial CMBS ( CMBS ) markets throughout the recent banking crisis. These indexes remain in positive territory for the year - a surprise for some, considering the amplified media focus in recent months - as downward pressure from wider spreads and an uptick in office delinquency rates has been offset by tailwinds from lower benchmark interest rates and relative strength in the residential sector. CMBS spreads widened from 1.16% at the end of Q4 to 1.42% at the end of Q1 (26 basis points) and have held steady through the first three weeks of Q2, while RMBS spreads widened from 0.50% to 0.63% during the quarter (13 basis points) and have also held steady over the past three weeks. Ratings agency Fitch reported last week that the overall real estate delinquency rates remained near historically-low levels in March at 1.76%, but office delinquency rates have continued to tick higher throughout 2023 amid a recent wave of loan defaults on highly-levered portfolios owned by private equity firms.

{kind=link}

Hoya Capital

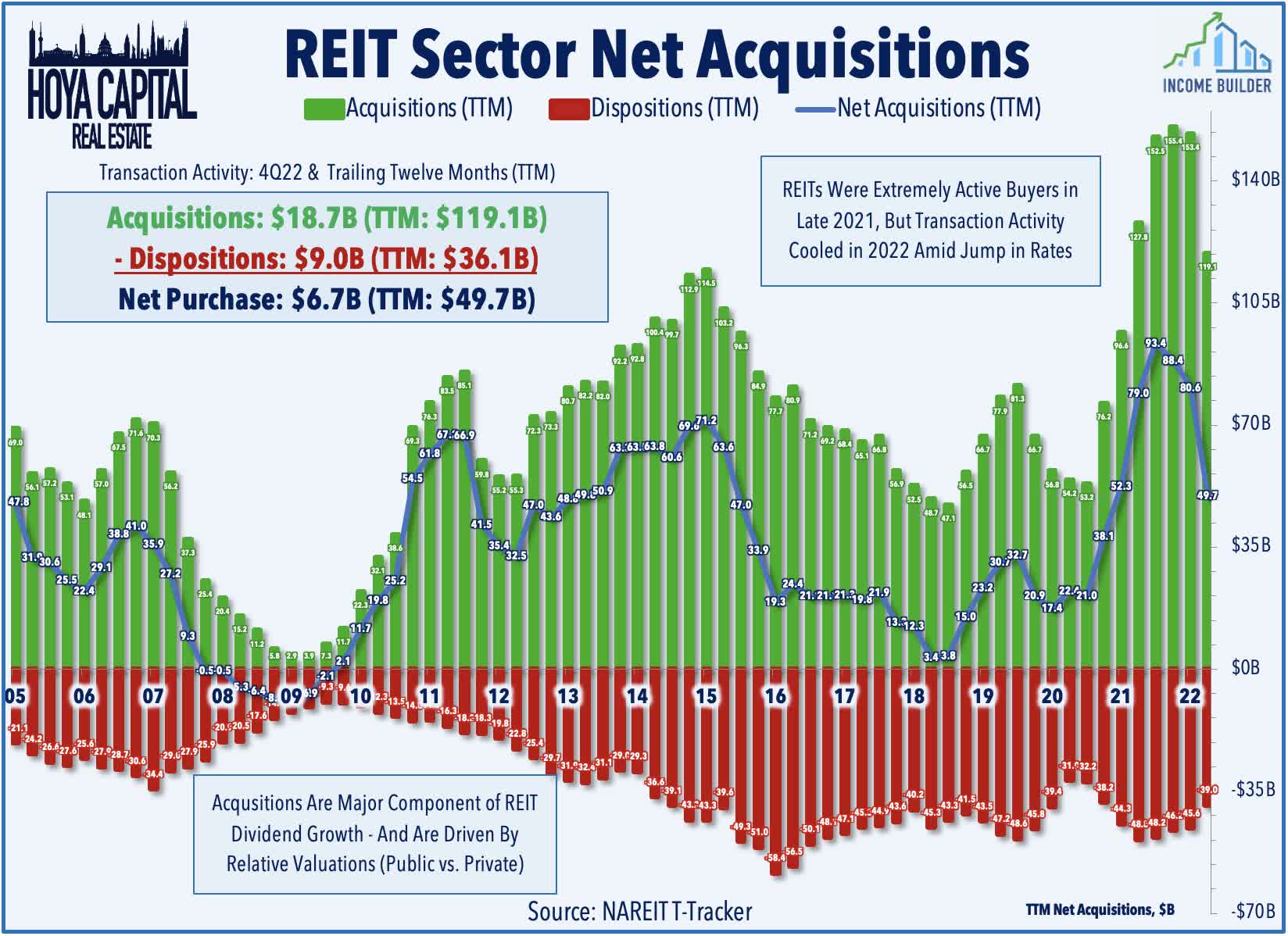

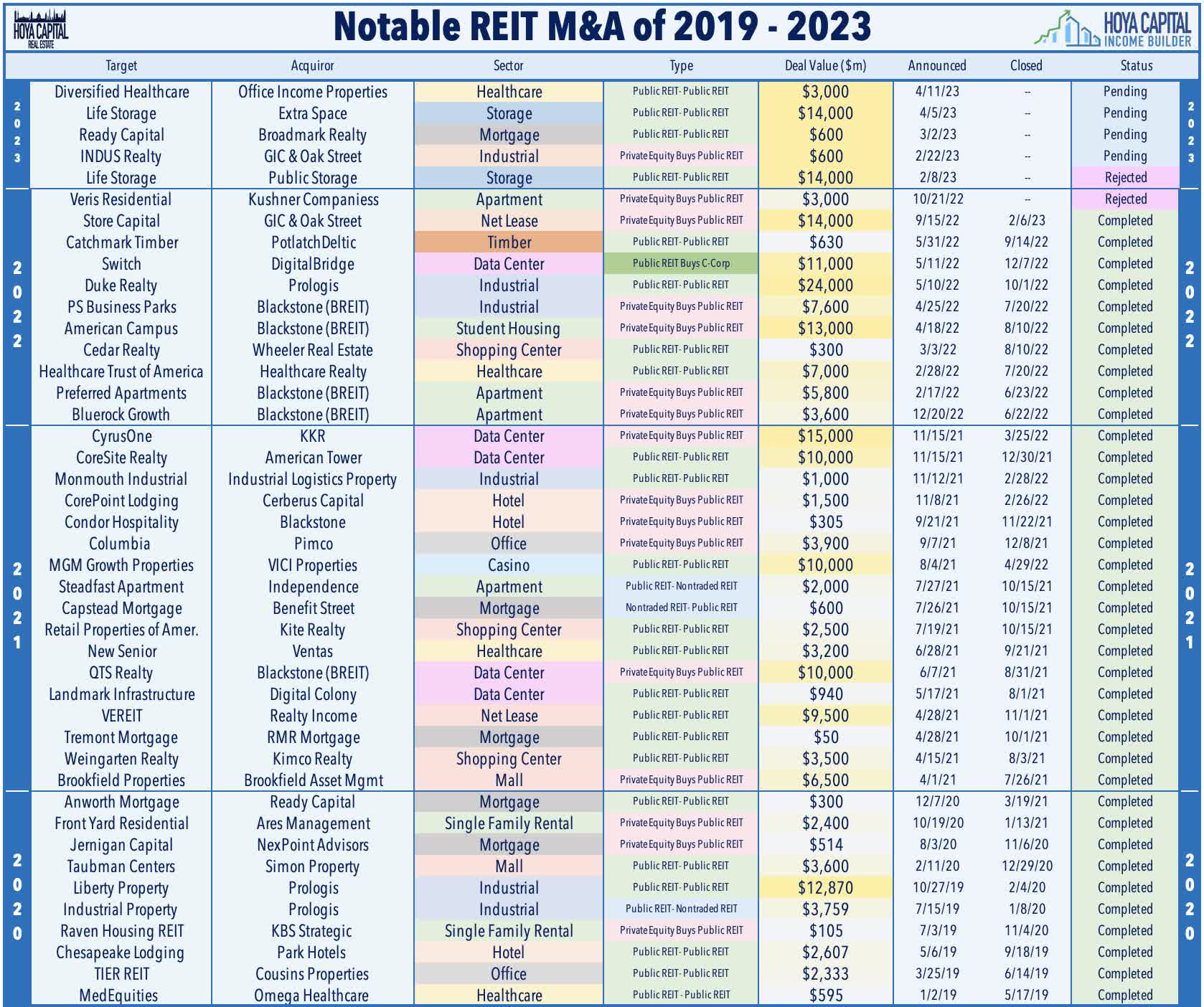

2) Acquisition Plans & Distress Opportunities

This commentary is particularly pertinent given the recent focus on the non-traded REIT ("NTR") platforms - including those offered by Blackstone ( BX ), Starwood , and KKR ( KKR ) - which have come under scrutiny in recent months after limiting investor redemptions at valuations that were seemingly still based on 2021 market conditions. Blackstone's non-traded real estate platform - BREIT - estimated that its Net Asset Value has increased about 30% since the end of 2019, but we discussed last week that some analysts believe that BREIT's actual NAV is 50% lower than its self-reported NAV. Publicly-traded REITs, by contrast, trade at an estimated 10-15% discount to consensus Net Asset Value ("NAV") estimates. Naturally, investors have seized on the opportunity to redeem NTR shares at these premium valuations, and outflows are likely to continue until this valuation gap narrows. We're interested to hear if public REITs are content to watch from the sidelines or if they're looking to become more opportunistic on the acquisitions front.

{kind=link}

Hoya Capital

What goes around comes around? These non-traded REIT platforms were on a "buying spree" from late 2020 into mid-2022 - paying "top dollar" for many of these large portfolio transactions - including the acquisition of more than a half-dozen public REITs. Foreshadowed by Blackstone's deal with VICI Properties ( VICI ) to sell its $5.5B stake in the MGM Grand Las Vegas and the Mandalay Bay Resort to VICI , we see these NTR platforms as "ripe for the picking" for opportunistic public REITs if redemption requests remain elevated. Even without "forced selling" in the near-term, we believe that the recent redemption limits exposed a key deficiency in the NTR structure compared with the far-more investor-friendly and efficient publicly-traded REITs and foresee many of these assets eventually returning to the public markets.

{kind=link}

Hoya Capital

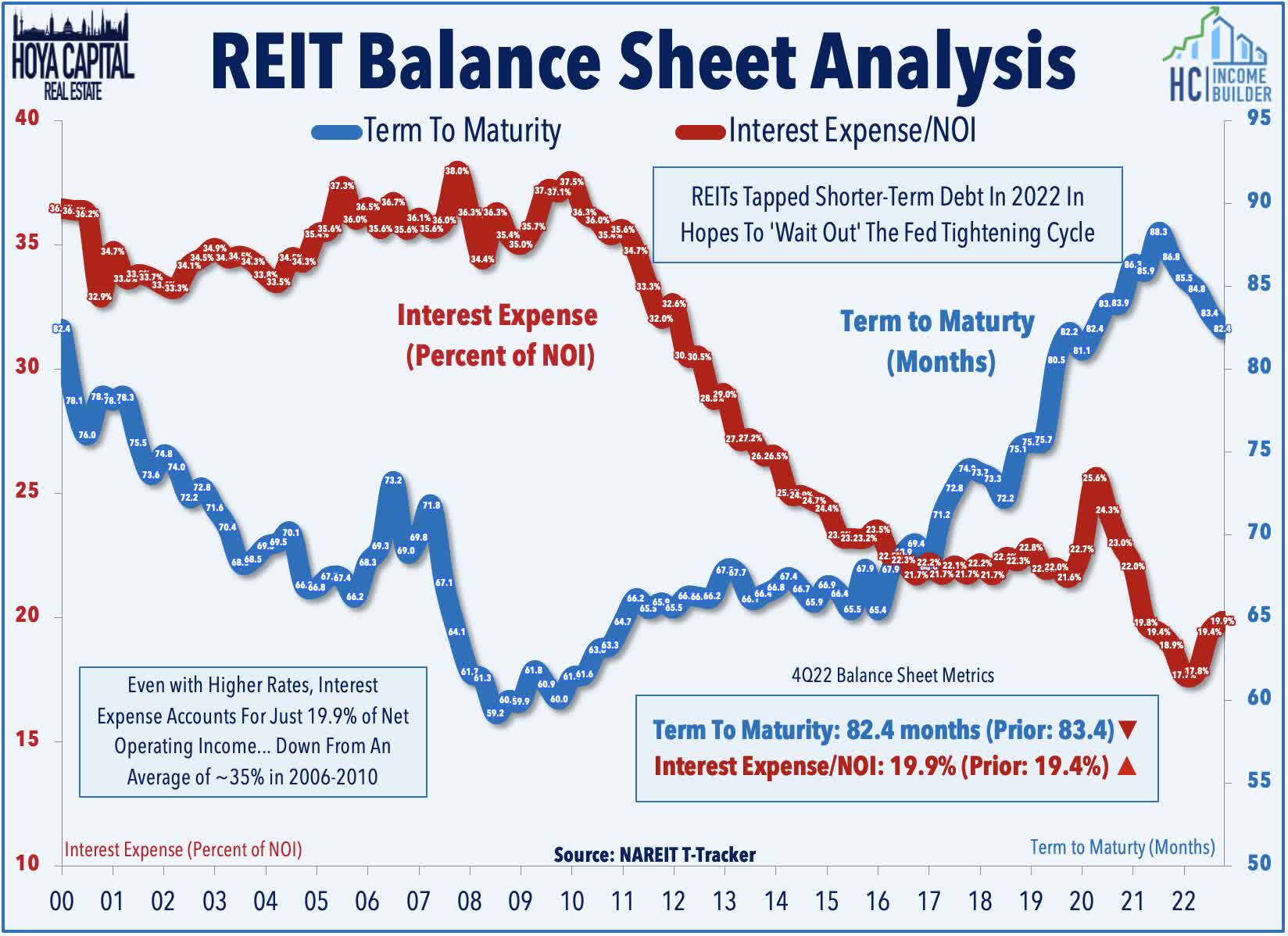

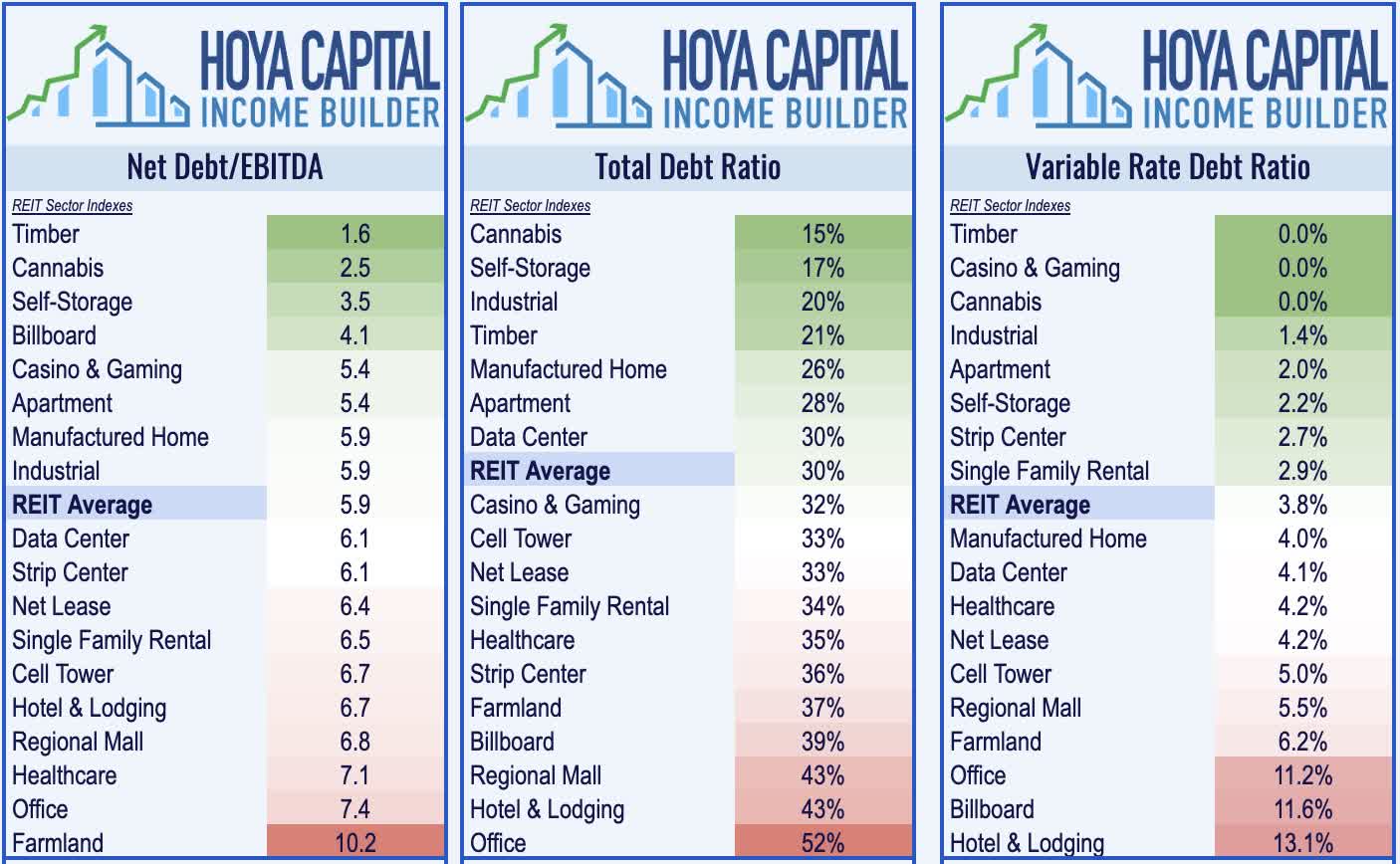

3) Balance Sheets & Variable Rate Exposure

Given the historic surge in interest rates in 2022, REITs have largely "hunkered down" over the last year - a benefit that was “earned” through their cautious balance sheet management over the past decade. As noted in our State of the REIT Nation report, following several years of robust capital-raising activity and balance sheet deleveraging, REITs raised less capital in 2022 than in any year of the prior decade and leaned more heavily into shorter-term credit facilities for funding needs, hoping to "wait out" the Fed and avoid locking in these higher rates on longer-term capital. We're interested in hearing which REITs are seeking to take advantage of the recent pull-back in benchmark lending rates and rebound in equity market valuations - and how the overall balance sheet strategy has evolved in the "new normal."

{kind=link}

Hoya Capital

Unlike the post-GFC period, there is no looming "wall of maturity" this time around as public REITs' access to long-term bond markets has allowed them to push their average maturity to nearly 7 years - but incremental external growth would almost surely require additional long-term capital. While most REITs remain on very solid footing with no immediate capital needs, the same can't necessarily be said about many private market players that rely on more short-term borrowing and continuous equity inflows to keep the wheels spinning. Much the opposite of their role during the GFC, many well-capitalized REITs are equipped to "play offense" and take advantage of acquisition opportunities from these private players - but whether or not these typically-defensive REITs are ready to take a more aggressive tact remains a key focus.

{kind=link}

Hoya Capital

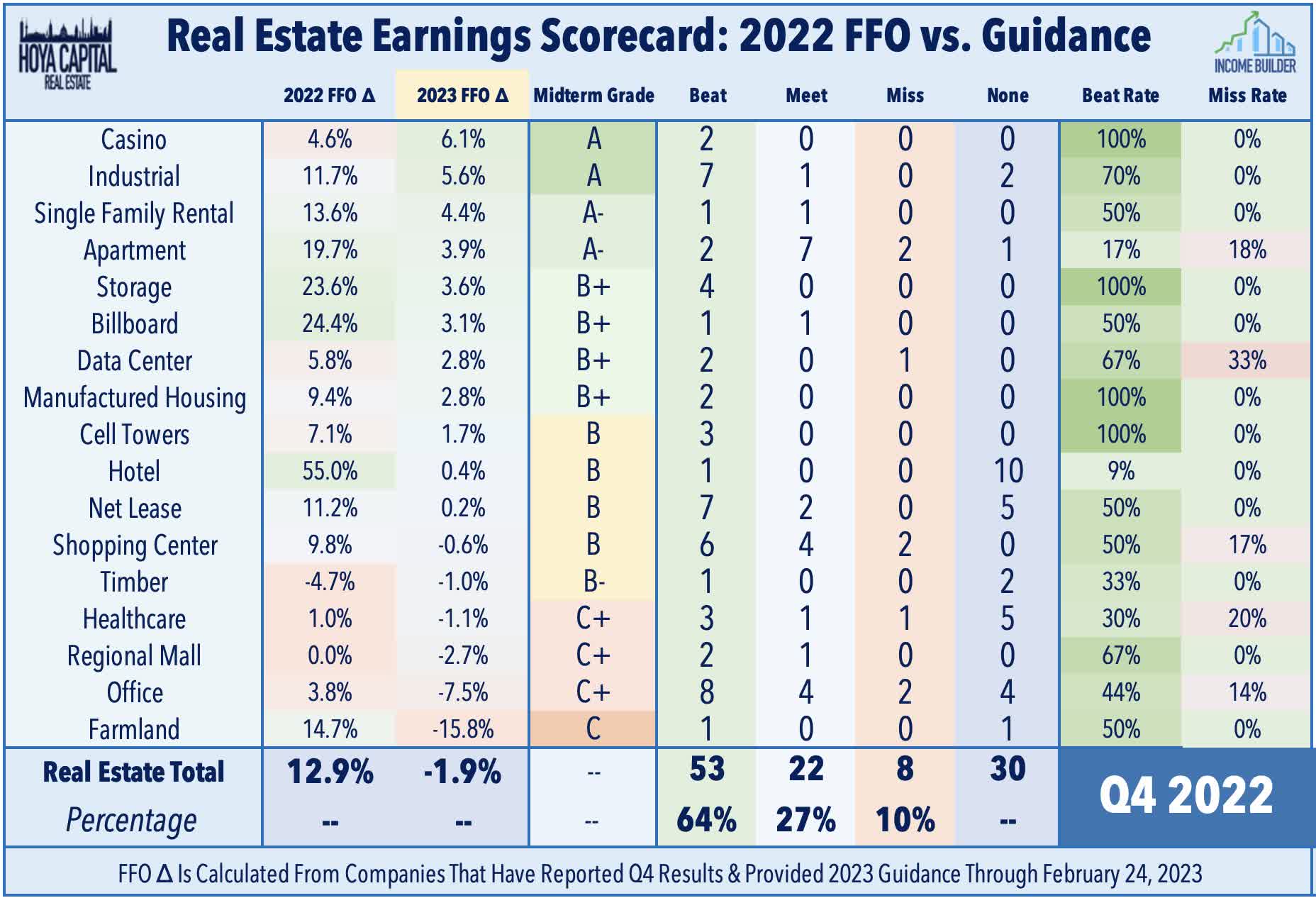

4) Full-Year 2023 Guidance Updates

All eyes will be on these REITs' updated full-year outlook - the key set of metrics that we monitor - with nearly 100 REITs expected to provide their updated FFO and/or NOI guidance for the year. Among the major property sectors, Residential and Industrial REITs were upside standouts on their initial outlook for 2023 provided last quarter, forecasting mid-single-digit FFO growth for 2023. Technology REITs see 2-3% growth - a bit disappointing given their lofty valuations - while retail REITs see flat-to-slightly-negative growth. Many Office REITs, several Healthcare REITs, and a handful of REITs across other property sectors forecast more significant double-digit FFO declines as industry-specific headwinds combine with expense pressures from elevated debt burdens.

{kind=link}

Hoya Capital

REIT FFO/share ("Funds From Operations") ended 2022 at levels that are about 15% above pre-pandemic levels - led by relative outperformance from residential, industrial, and technology REITs. Consensus expectations call for 2-3% FFO growth in 2023 for the sector average, but REITs typically provide a relatively conservative outlook early in the year with room to raise in subsequent quarters. Dividend commentary will also be in focus following a record pace of hikes in 2021 and 2022. With a historically low dividend payout ratio, most equity REITs still have a healthy buffer to protect current payout levels if macroeconomic conditions take a turn for the worse. Below, we discuss the specific metrics we're watching across each sector.

{kind=link}

Hoya Capital

Residential REITs Earnings Preview

Apartments : The state of the U.S. housing market will be a critical focus throughout earnings season - the industry that felt the most direct effects from the historically swift monetary tightening cycle that began in mid-2022. Consensus sentiment around apartment REITs has remained distinctly negative despite recent "green shoots" in forward-looking housing metrics as multifamily markets have an additional headwind from supply growth. Investors remain split on whether rental rate weakness seen in late 2022 is the beginning of a sharper downtrend, or whether the recent softness is more symptomatic of a normalization back toward "trend levels." Recent data from Apartment List and Zillow points more towards the "normalization" thesis, with rental rates showing some seasonal reacceleration in early 2023. We'll be closely-watching rent growth metrics on new and renewed leases and commentary regarding the timing and potential impact of looming supply headwinds.

{kind=link}

Hoya Capital

Single-Family Rentals : Cooling home price appreciation and tightening credit conditions is indeed bad news for many new “start-up” entrants into the single-family rental ("SFR") scene that are learning the hard way that the SFR game is a capital-intensive business that requires significant scale to operate profitably. While residential rent growth has moderated over the past nine months, the recent gloomy narrative on SFR REITs appear particularly unwarranted given the still-strong labor markets, lack of new single-family housing supply, and affordability conditions that still remain heavily skewed towards renting over owning. In addition to rent growth metrics, we're interested in commentary about external growth prospects - specifically, whether these REITs are seeing signs of distress in private markets that could create discounted buying opportunities in the quarters ahead.

{kind=link}

Hoya Capital

Retail REITs Earnings Preview

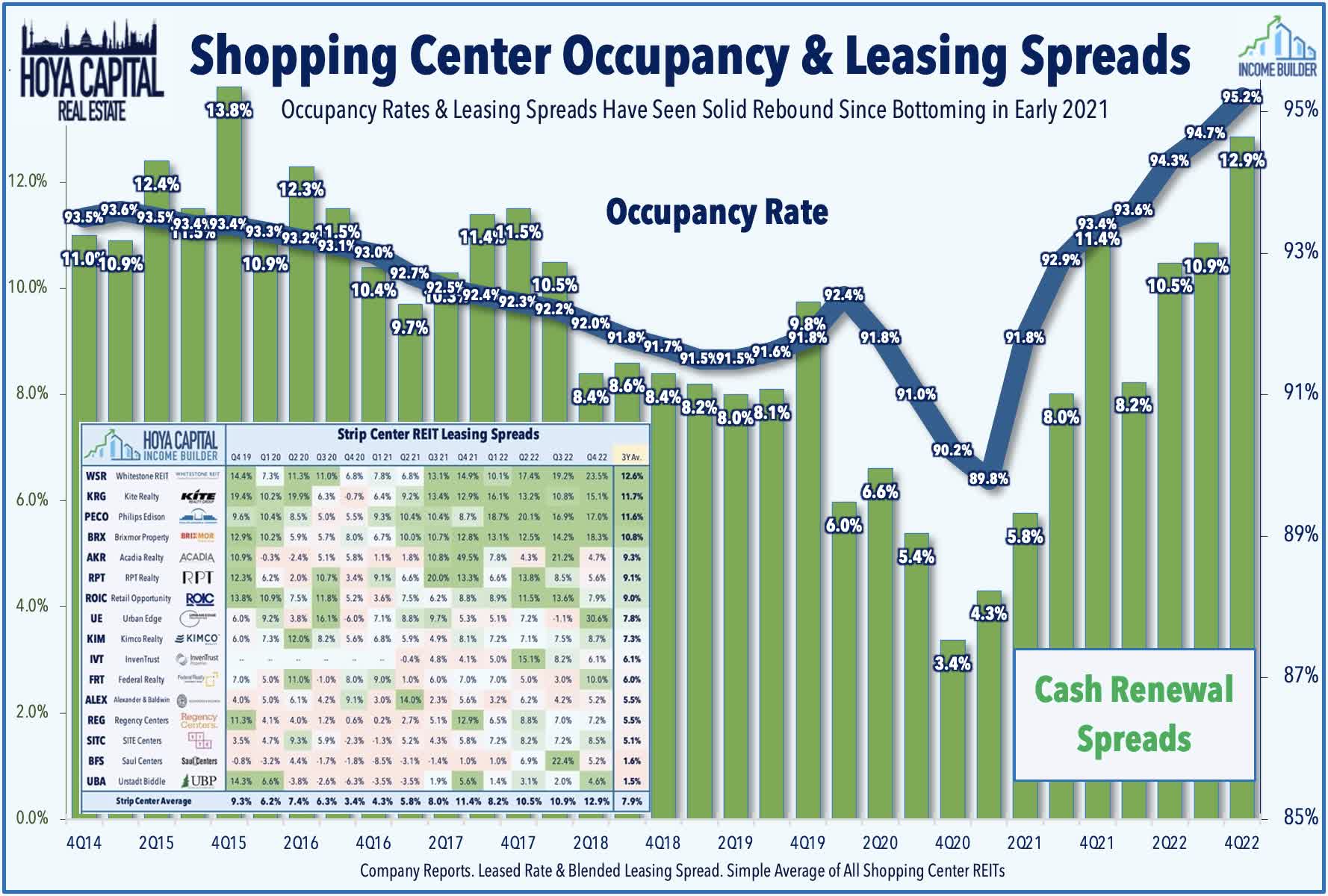

Strip Centers : Flying under the radar amid recession concerns and the looming shadow cast by their persistently-troubled mall peers, the outlook for Strip Center REITs has improved considerably over the past year. The combination of near-zero new development and positive net absorption since early 2021 has driven occupancy rates to record highs and allowed Strip Center REITs to enjoy some long-awaited pricing power. The recent bankruptcy of Bed Bath Beyond ( BBBY ) this week and Party City ( OTCPK:PRTYQ ) earlier this year, however, has cast some doubt over these REITs' ability to maintain the positive momentum. Commentary last quarter indicated that most of these locations - representing about 1-2% of the sector's NOI - have a "waiting list" of retailers eyeing the space, but we'll be listening closely to hear if any of these discussions have fizzled after the SVB collapse and subsequent credit crunch. We'll again be focused again on leasing spreads and occupancy rate trends - which have been quite impressive of late.

{kind=link}

Hoya Capital

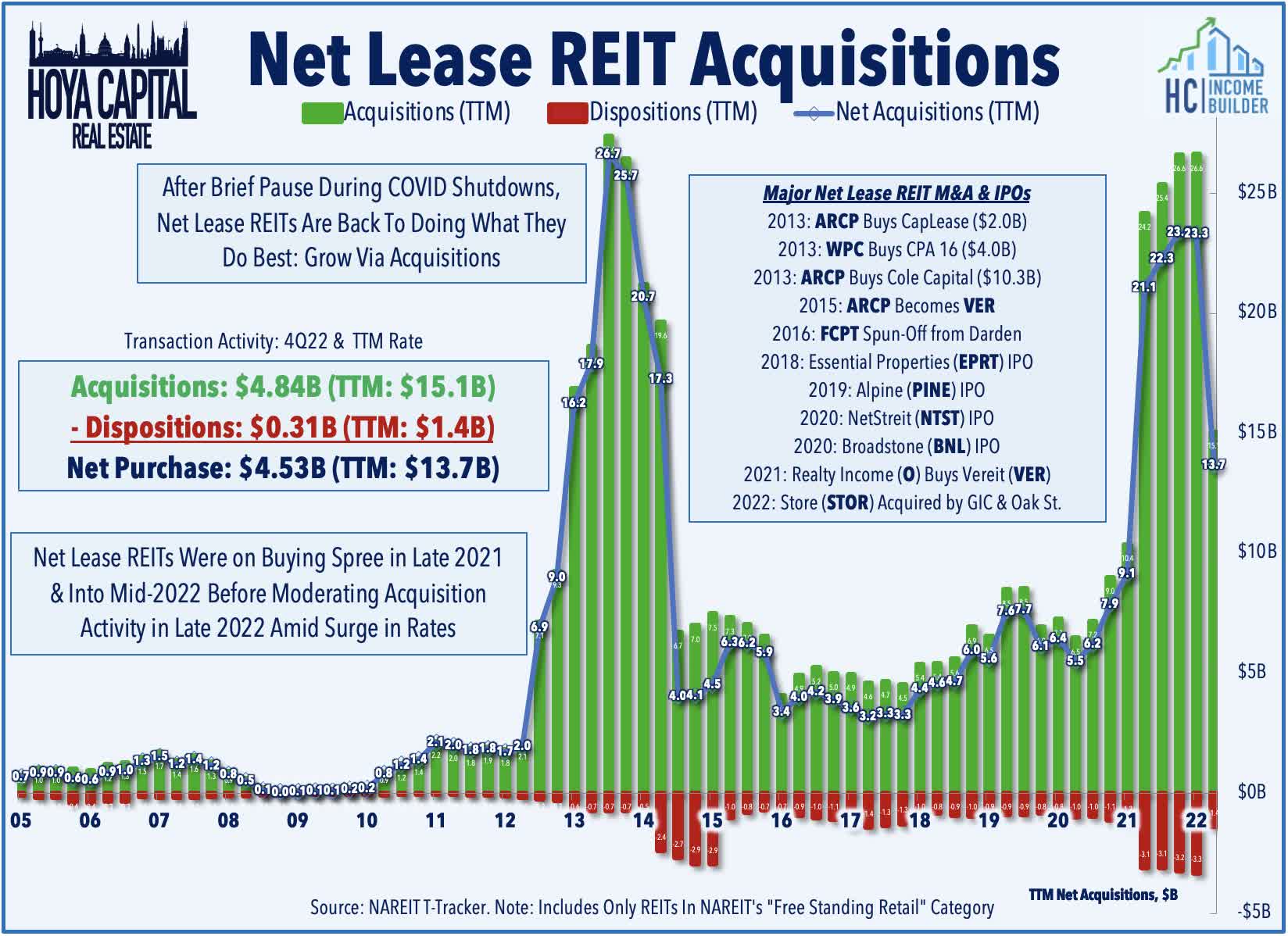

Net Lease : Historically one of the most "rate-sensitive" property sectors, net lease REITs have surprisingly been the best-performing major property sector since early 2021 despite the significant rise in interest rates. Private market values remained far "stickier" than comparable public market assets through much of 2022, but despite the tighter investment spreads, the pace of acquisition activity for some REITs slowed only modestly in late 2022, a strategy that could prove costly if rates remain persistently elevated. Strong balance sheets and lack of variable rate debt exposure have positioned net lease REITs to be aggressors as over-levered private players seek an exit, but these REITs can afford to wait until the price is right. We're keyed in on commentary regarding cap rate movements in early 2023 for a read on whether private market asset owners are holding tight or ready to adjust price expectations to the reality of higher benchmark rates.

{kind=link}

Hoya Capital

Tech and Industrial REITs Earnings Preview

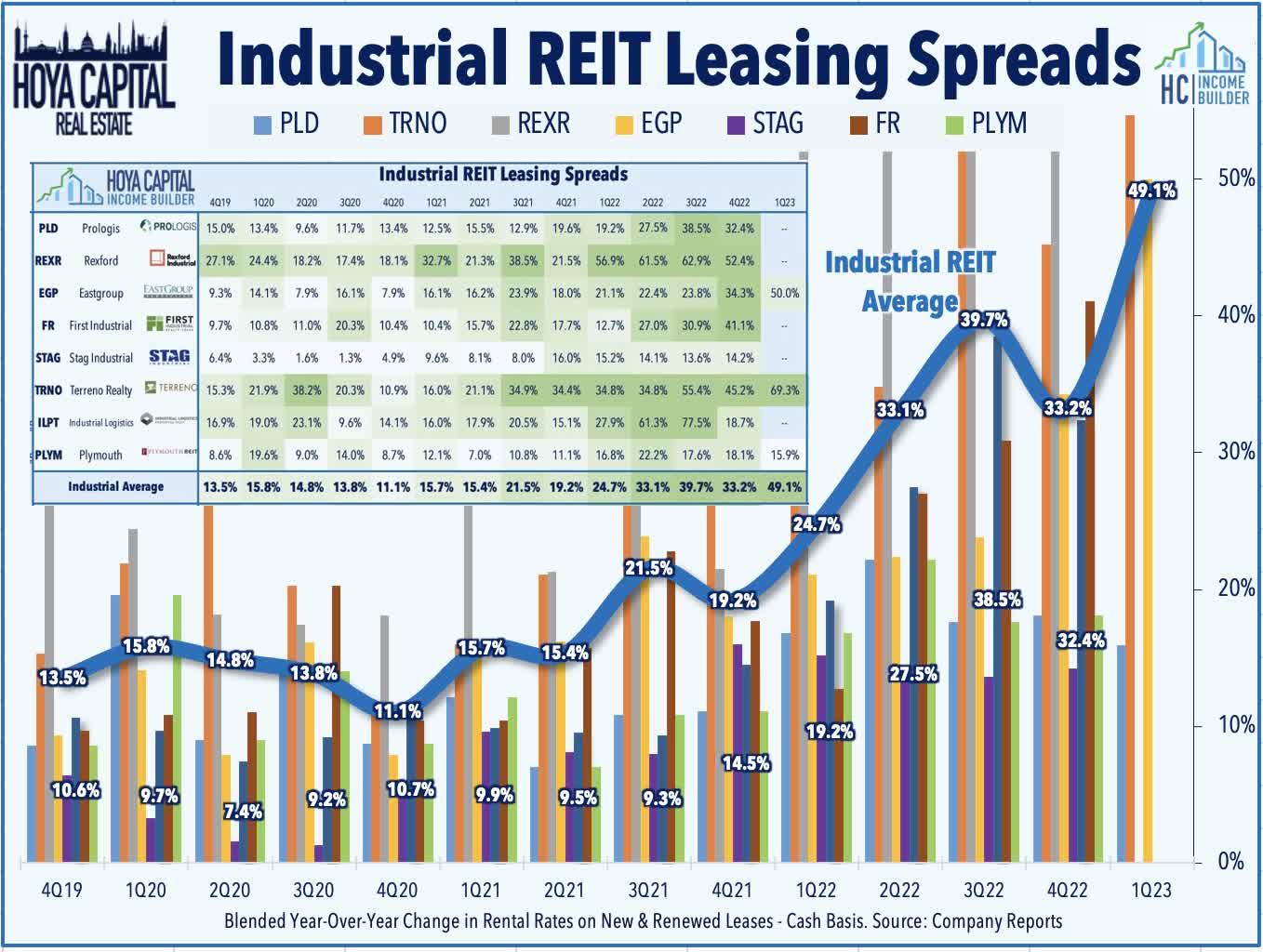

Industrial : A trio of "beat and raise" reports from industrial REITs last week showed that demand for well-located logistics space continues to significantly outstrip supply. Prologis ( PLD ) - the largest industrial REIT - reported fresh records across several critical operating metrics, including a record-high 11.4% same-store NOI growth for Q1 and record-highs for GAAP and cash leasing spreads at 68.8% and 41.9%, respectively. Rexford ( REXR ) raised its full-year FFO growth outlook to 8.7% - up 150 basis points from its prior outlook, driven by incredible rental rate growth of 80% on a GAAP basis and 60% on a cash basis - an acceleration from Q4. First Industrial ( FR ) reported that it achieved cash rental rate increases of 58.3% in the first quarter - its strongest on record - fueling a 175 basis point boost to its full-year FFO growth outlook to 4.4%. Industrial REITs aren't entirely immune from post-pandemic demand normalization, but supply remained inherently capped by land constraints. We expected rent growth to begin to normalize in early 2023, but have so far been pleasantly surprised by strengthening pricing power.

{kind=link}

Hoya Capital

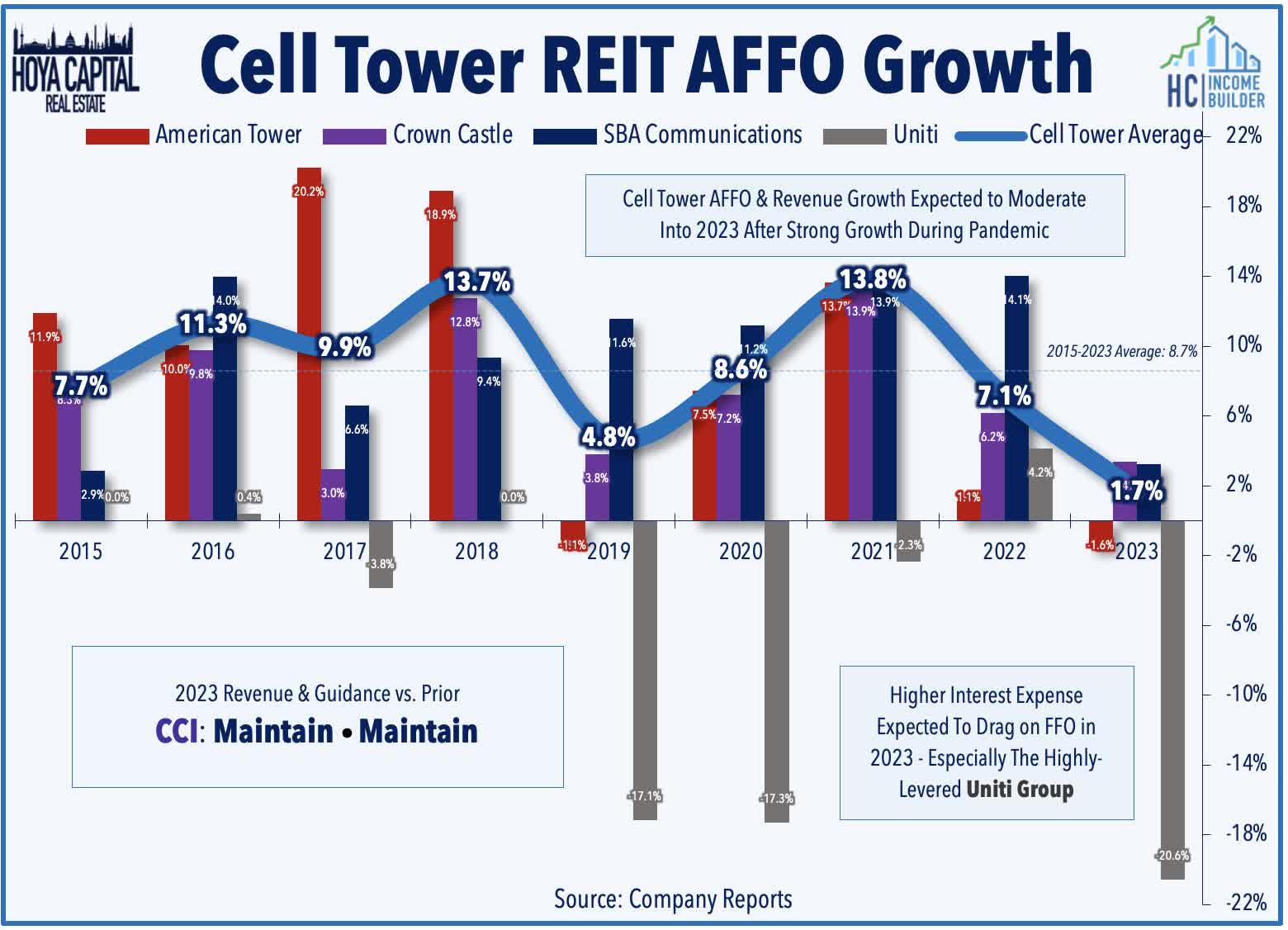

Cell Towers : Similar to their industrial REIT peers, Cell Tower REITs uncharacteristically lagged in 2022, weighed down by tech-related weakness and concerns of disruptive threats to the long-term competitive positioning. Crown Castle ( CCI ) reported decent results last week but provided cautious commentary in which it noted that near-term impacts from higher interest rates will result in "minimal dividend growth in 2024 and 2025" after recently exceeding its target of 7-8% annual dividend growth set in 2017. CCI quantified the headwind from higher interest rates and the near-term hit from lower Sprint revenues at $350M over the next two years - representing a roughly 10% drag on FFO. Nevertheless, CCI maintained its full-year outlook, which calls for site rental revenue growth of 3.5% at the midpoint of its range and AFFO/share growth of 3.4% - the highest among the four cell tower REITs based on current guidance. We're focused on updated full-year guidance from American Tower ( AMT ) and SBA Communications ( SBAC ) and on commentary about potential M&A following a relatively quiet year.

{kind=link}

Hoya Capital

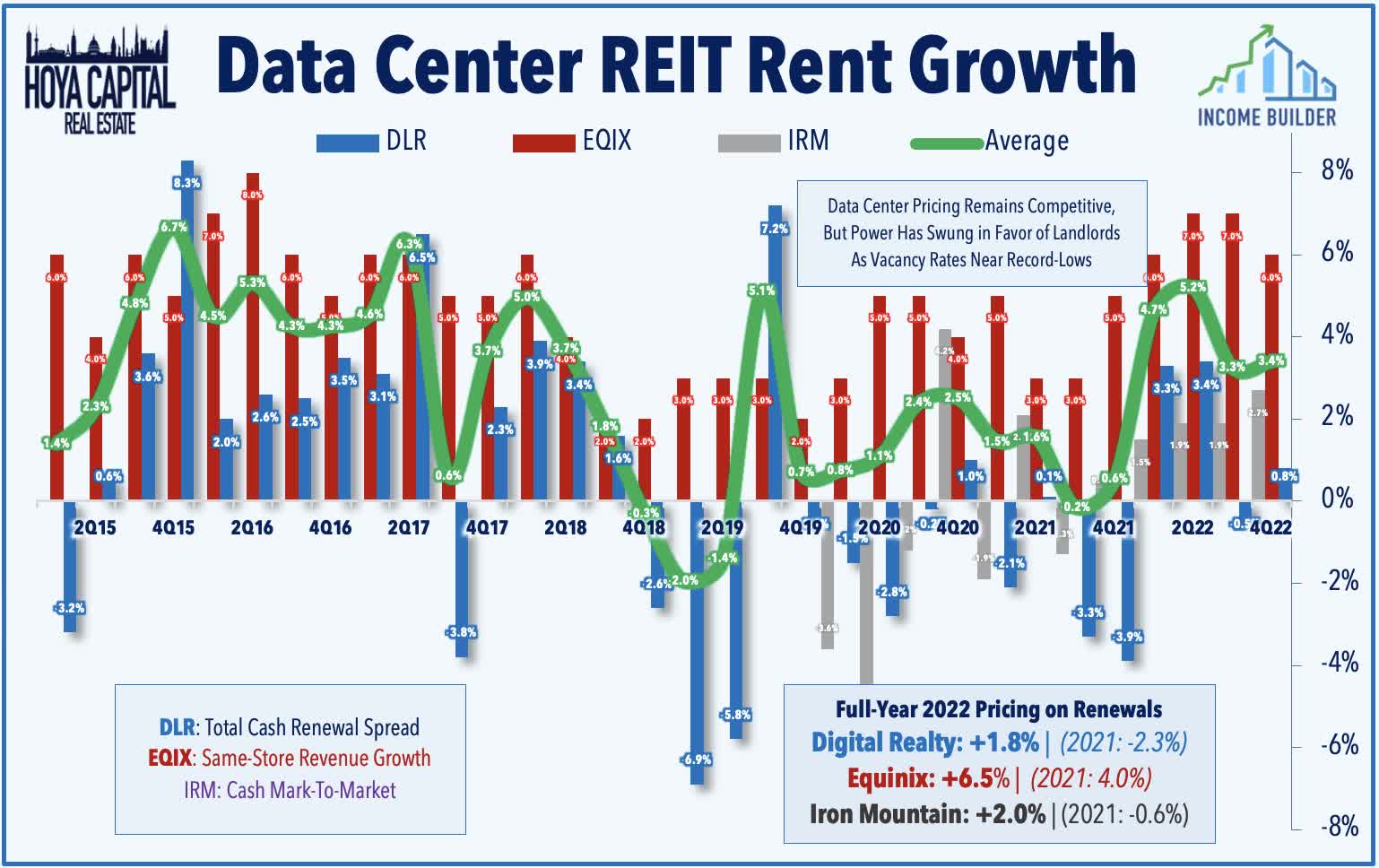

Data Center : Data Center REITs have been one of the better-performing property sectors over the past six months as property-level fundamentals have strengthened despite a downshift in cloud-related spending. Ironically, just as Data Center REITs became a trendy “short” idea last year centered on a thesis of weak pricing power and competition from hyperscalers, rental rate meaningfully improved in the back-half of 2022. While property-level fundamentals are not as compelling as the cell tower space where REITs have effectively corned the market, the concentration of data center REITs shouldn’t be discounted either as Equinix ( EQIX ) and Digital Realty ( DLR ) have built relatively dominant platforms. While DLR's initial FFO outlook for 2023 was soft, DLR does expect an upward inflection in property-level fundamentals, projecting same-capital NOI growth of 3-4% for full-year 2023 - a notable improvement from the -5.8% decline in 2022. We'll again be watching renewal pricing trends and leasing volumes closely watched this quarter.

{kind=link}

Hoya Capital

Hotel & Casino REIT Earnings Preview

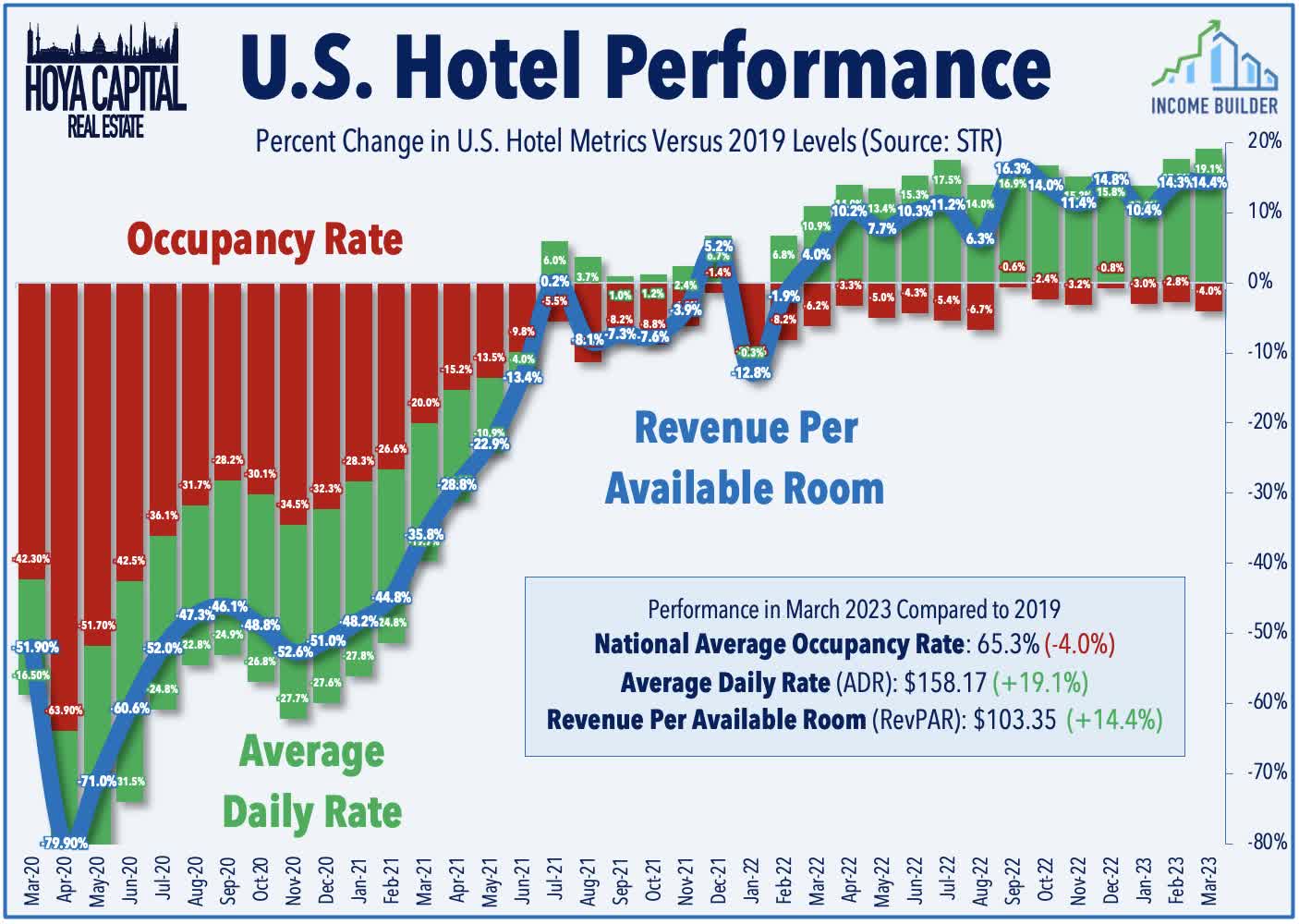

Hotels : Despite lingering recession concerns, Hotel REITs have been among the better-performing sectors over the past several quarters, buoyed by steady post-pandemic operating improvement and a much-anticipated return of dividends. Several years of pent-up leisure demand helped to offset a sluggish business and group travel recovery - and relatively strong pricing power has enabled hotel owners to achieve record-high Revenue Per Available Room ("RevPAR") metrics in 2022 despite a 5-10% occupancy rate drag compared to 2019-levels. STR reported last week that the national average RevPAR was 14.4% above the comparable 2019-level in March, fueled by a 19.1% increase in Average Daily Rates. Recent TSA Checkpoint data shows relatively strong demand trends in early 2023 with both January and February exceeding pre-pandemic throughput levels, but March saw a slight downshift in demand to about 2% below comparable 2019-levels, consistent with STR data showing a mid-single-digit comparable occupancy drag in March. We're hoping to see additional hotel REITs provide full-year guidance after several years of limited disclosures amid COVID-related uncertainty.

{kind=link}

Hoya Capital

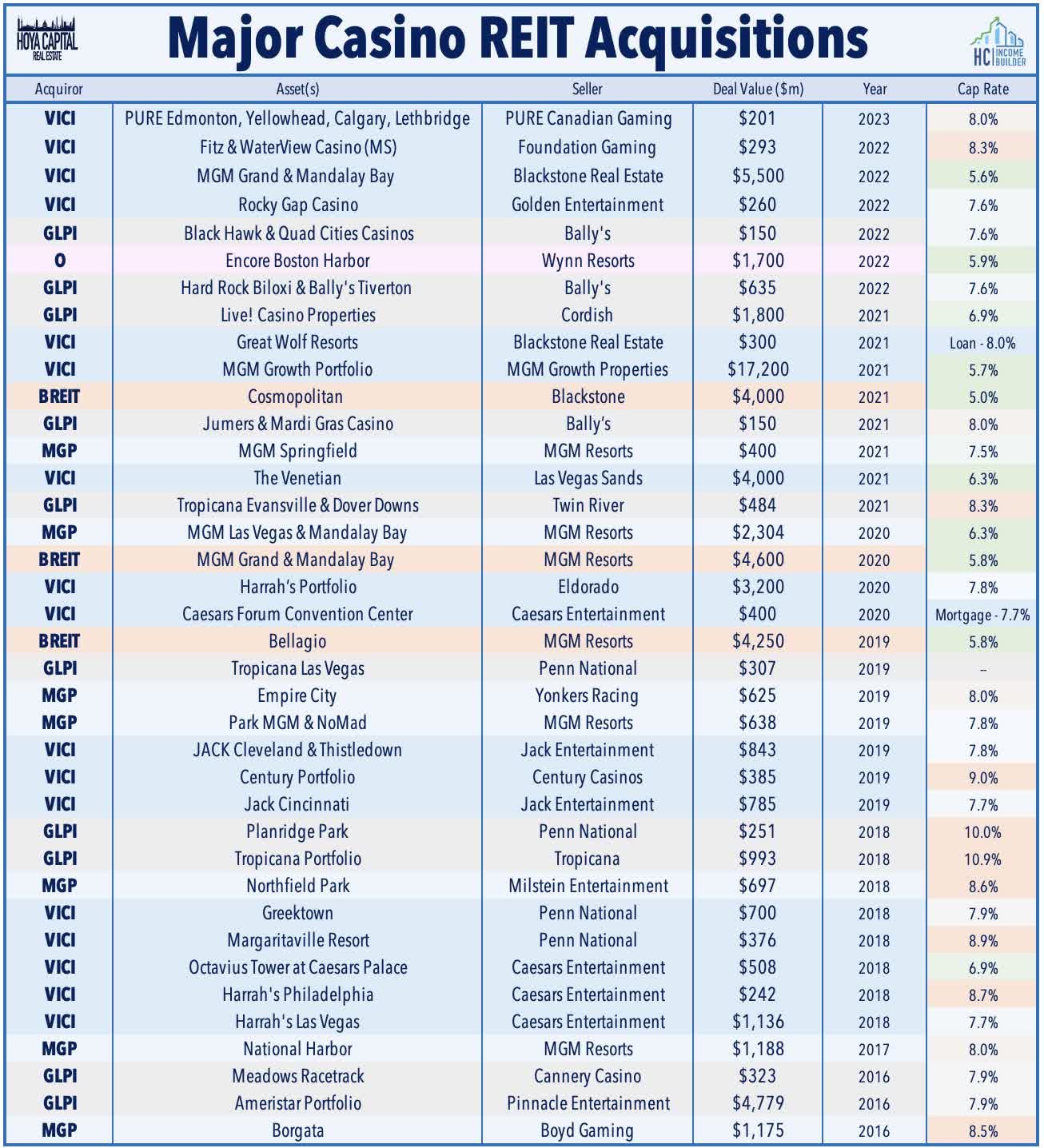

Casinos : Casino REITs were the lone property sector to finish in positive territory in 2022, benefiting from their attractive “inflation-hedging” lease structure, strength in Las Vegas travel demand, and broader institutional investor acceptance. A success story of the "Modern REIT Era," Casino REITs have been the best-performing property sector since their emergence in the mid-2010s, honing the competitive advantages of the public REIT model. Fittingly, Casino REITs - exemplars in shareholder-friendly governance - have been beneficiaries of distress felt across the darker underbelly of the real estate industry, including Blackstone’s ( BX ) non-traded REIT ("NTR") platform. M&A will again be the focus of earnings season, and we're focused specifically on whether any REITs have had discussions about acquiring BREIT's interest in the Bellagio and Cosmopolitan.

{kind=link}

Hoya Capital

Office & Healthcare REIT Earnings Preview

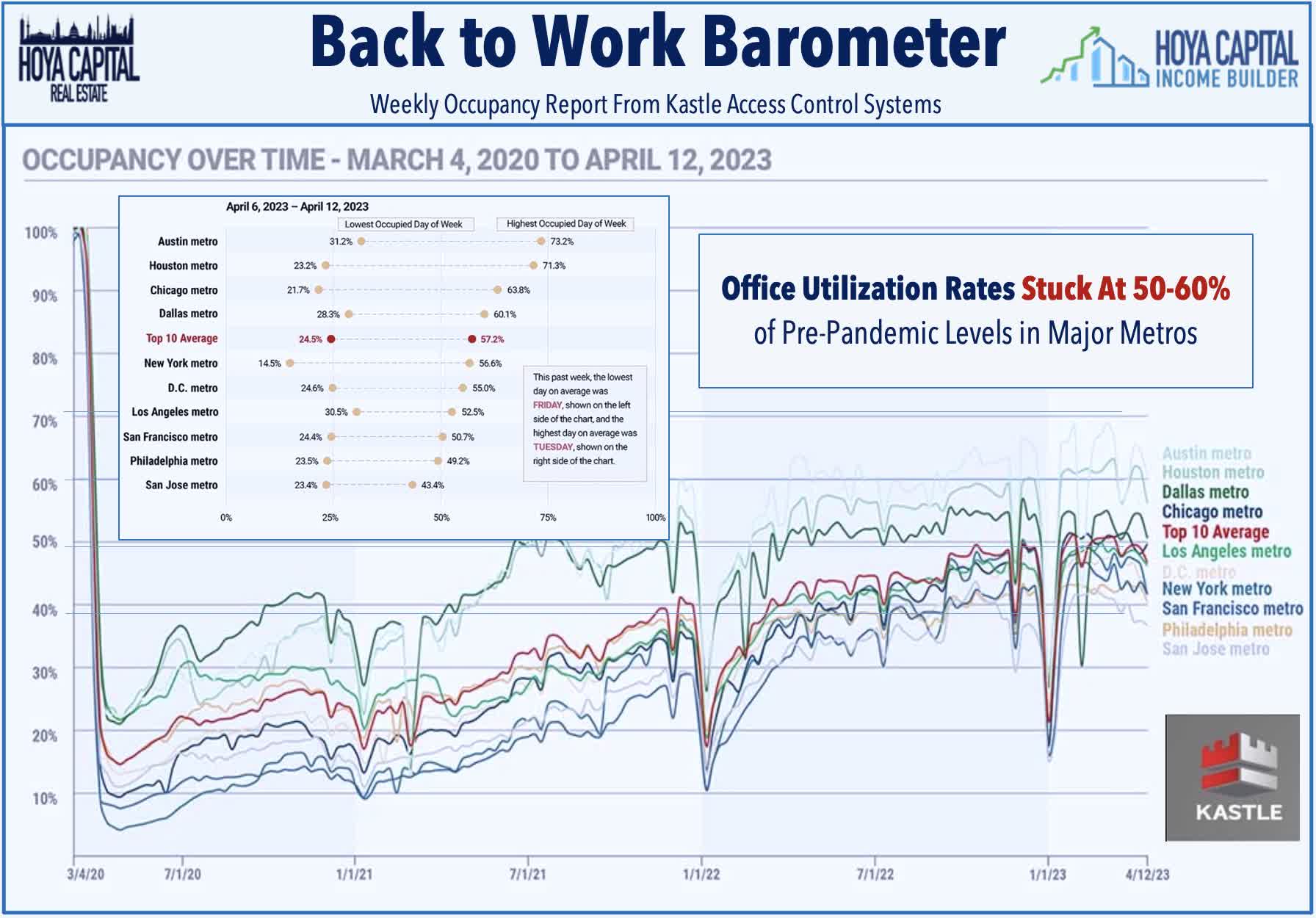

Office : Three years into the pandemic, data from Kastle Systems still shows that office utilization rates remain 40-60% below pre-pandemic levels and have trended more-or-less sideways since late 2021. Office valuations have dipped by nearly that much - 30% by some measures - which, combined with the rise in interest rates, has prompted a wave of loan defaults on portfolios owned by some of the more highly-levered private equity firms, including Brookfield, Blackstone , Pimco , Brookfield , and RXR - each of which shares a common theme: high loan-to-value ratios that are roughly twice as high as the typical office REIT. Results from a pair of office REITs last week showed that conditions for well-capitalized public REITs aren't nearly as dire as conditions faced by their more-highly-levered private market peers, but the question is whether there's any value in being the best house in a bad neighborhood or whether the downward inertia and spiraling effect on prices eventually drag even the better-capitalized players into the sinkhole.

{kind=link}

Hoya Capital

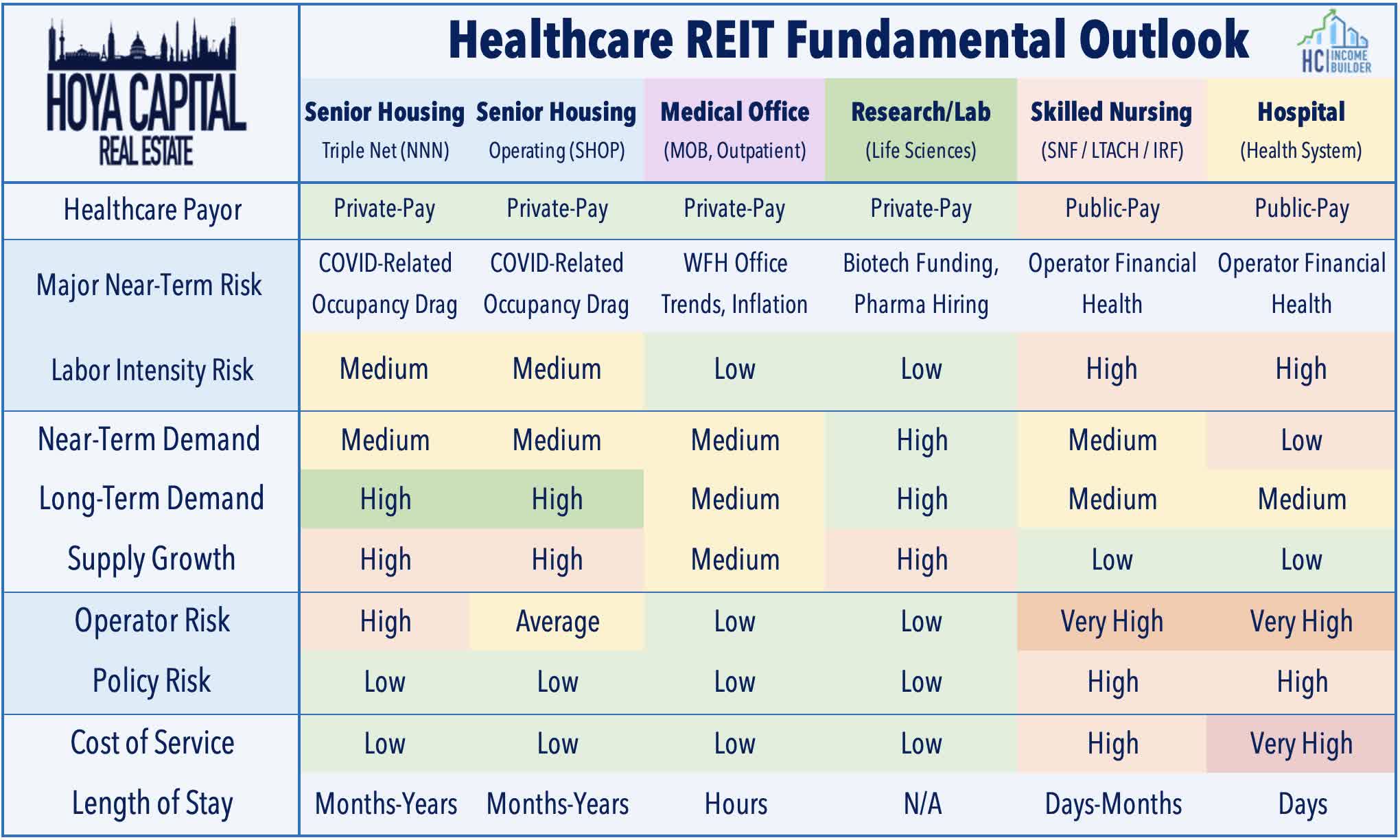

Public-Pay Healthcare : We segment the healthcare space along the private/public pay divide given the divergent fundamentals between the public-pay sub-sectors - hospitals and skilled nursing - and the private-pay sub-sectors - senior housing, medical office, and lab space. On the public-pay side, we've seen an intensification of tenant rent collection from struggling tenant operators. Gibbins Advisors reported early this year that bankruptcy filings for healthcare companies nearly doubled in 2022 compared to the prior year, which it attributes to this “COVID hangover” resulting from waning government support and higher labor costs. Medical Properties Trust ( MPW ) - which remains in the cross-hairs of short-sellers - has been a laggard this year, with tenant concerns still in focus. Skilled nursing REIT Omega Healthcare ( OHI ) also reported ongoing rent collection difficulties from a handful of struggling operators, but also highlighted some progress in restructurings and reiterated its confidence in its ability to cover its dividend. Tenant health - and resulting dividend sustainability is the primary focus of earnings season for these public-pay healthcare REITs.

{kind=link}

Hoya Capital

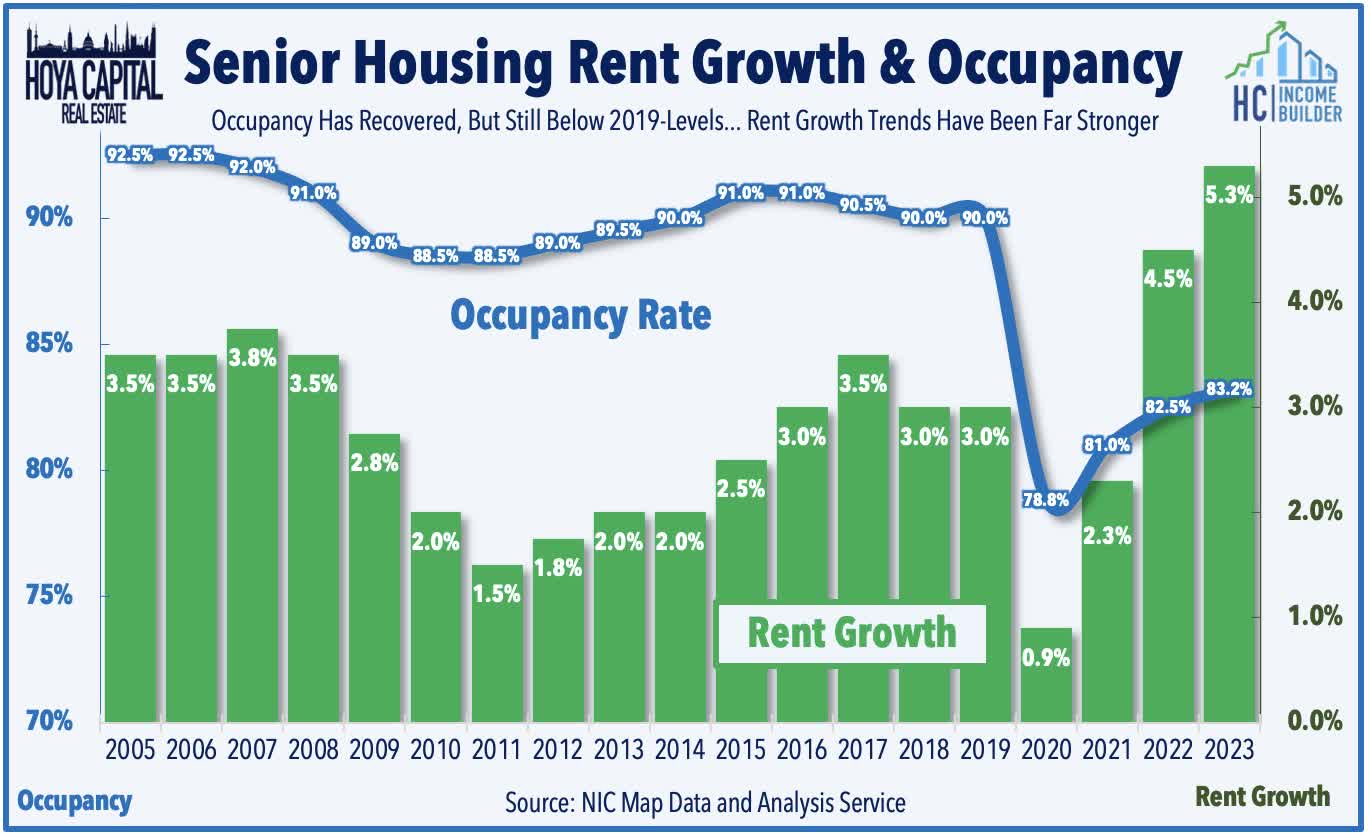

Private-Pay Healthcare : Conditions are far more stable on the private-pay side. Senior Housing ("SH") REITs Welltower ( WELL ) and Ventas ( VTR ) have been among the better performers in recent weeks, lifted by NIC data showing that senior housing occupancy increased for a seventh-straight quarter to 83.2% in Q1 - up 5.4% from the pandemic occupancy low of 77.8% in 2Q21 - but still below the pre-pandemic levels of roughly 90%. Despite the reduced occupancy levels, SH operators have exhibited strong pricing power with annual rent growth climbing to 5.3% in Q1 - the largest increase on record - and we expect the nearly 9% cost-of-living adjustment (COLA) to Social Security benefits to further support SH rent growth in 2023. Results from lab space owners Alexandria ( ARE ) and Healthpeak ( PEAK ) will be closely watched for updates on tenant health, many of which were clients of SVB.

{kind=link}

Hoya Capital

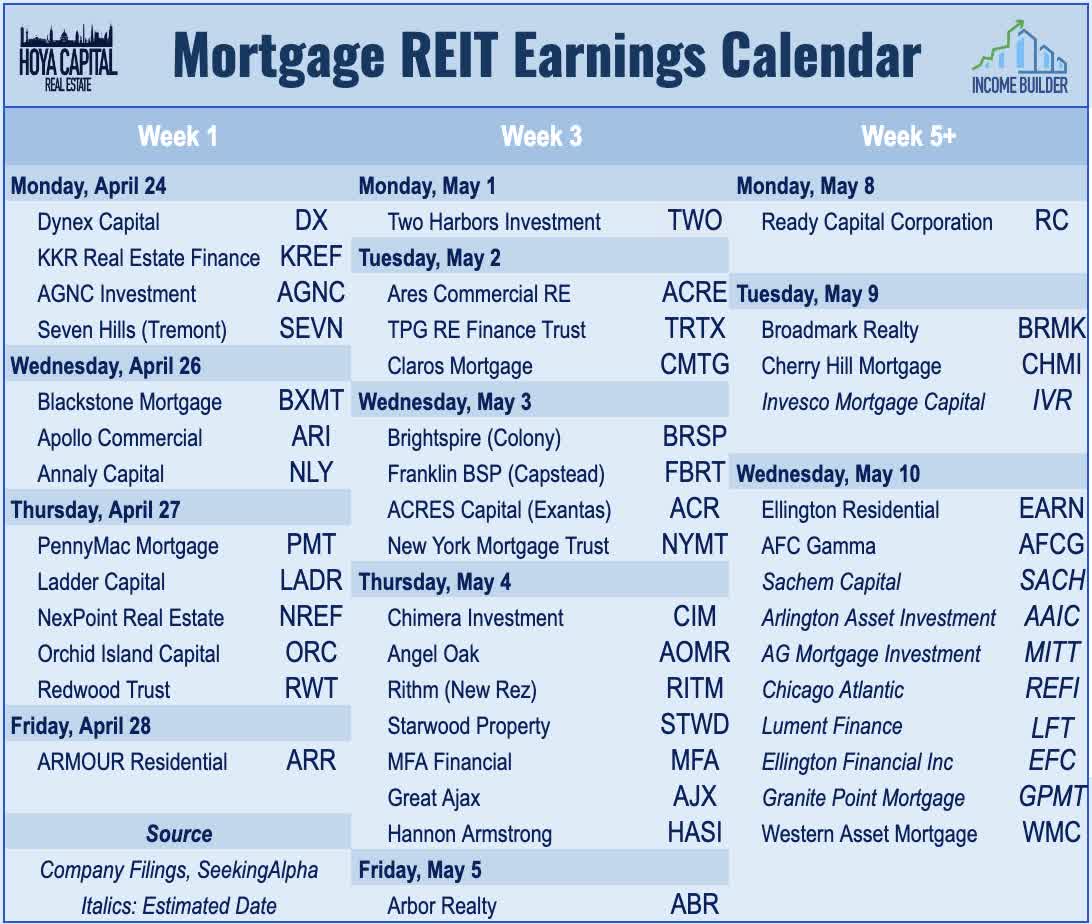

Mortgage REITs Earnings Preview

"Here we go again" was the attitude for a brief period last month in the wake of the Silicon Valley Bank collapse, as sharp changes in benchmark rates and/or spreads in either direction can wreak havoc on mortgage REITs that are caught over-levered or improperly hedged. Conditions have stabilized in April, however, which has lifted the iShares Mortgage REIT ETF ( REM ) higher by nearly 10% from its March 23rd lows. As noted above, the RMBS and CMBS benchmarks were about flat in Q1 as a decline in benchmark rates offset a widening of spreads. For residential mREITs, book values and dividend commentary will be the major focus. For commercial mREITs, we're more closely focused on loan performance and changes in Current Expected Credit Loss ("CECL") allowance - particularly for mREITs with significant office exposure. We note that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but there remains a handful of mREITs with payout ratios above 100% of EPS.

{kind=link}

Hoya Capital

Key Takeaways: Real Estate Earnings Preview

Real estate earnings season kicks into gear this week, and over the next month, we'll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies. This report discussed the major high-level themes and metrics we're watching across each property sector. We're particularly focused on commentary regarding cap rates, acquisition opportunities, and dividend sustainability. Many well-capitalized REITs are equipped to "play offense" and take advantage of acquisition opportunities from weaker private players - but whether or not these typically-defensive REITs are ready to take a more aggressive tact remains a key focus. Most equity REITs still have a healthy buffer to protect current payout levels if macroeconomic conditions take a turn for the worse, but we'll be closely-monitoring dividend commentary in the office, mortgage, and healthcare REIT sectors. We'll provide real-time commentary throughout earnings season for Income Builder members on our Real Estate Daily Recap .

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

REIT Earnings Preview: When The Tide Goes Out