CA - Reitmans: 24% Price Difference Between The Share Classes Is A Buying Opportunity

Summary

- The company has successfully restructured its business and its TTM operating income stands at $29.9 million.

- Reitmans also had a $50.1 million cash balance as of October and I think it can increase by around $30 million in the near future.

- The company has two classes of shares which are almost the same yet a 24% premium has emerged over the past month.

- In my view, the price gap between the two classes is likely to close in the coming weeks.

- Considering the stock has strong momentum and Reitmans still looks cheap, I expect this to happen through an increase in the price of Class A shares.

Investment thesis

On January 25, I revealed in my MP service that I’d taken a position in a Canadian women’s clothing retailer named Reitmans ( RET.A.CA ) ( OTCPK:RTMAF ) ( RET.CA ) ( OTCPK:RTMNF ). It’s been a wild ride as the market valuation of the company has almost doubled since then which made this my second-largest position by far. Something unusual has happened over the past weeks as the price difference between the two classes of shares of the company has grown to 24%. In my view, Reitmans is still undervalued and there is very little difference between the two classes of shares which is why I switched my position to Class A shares. Let’s review.

Overview of the opportunity

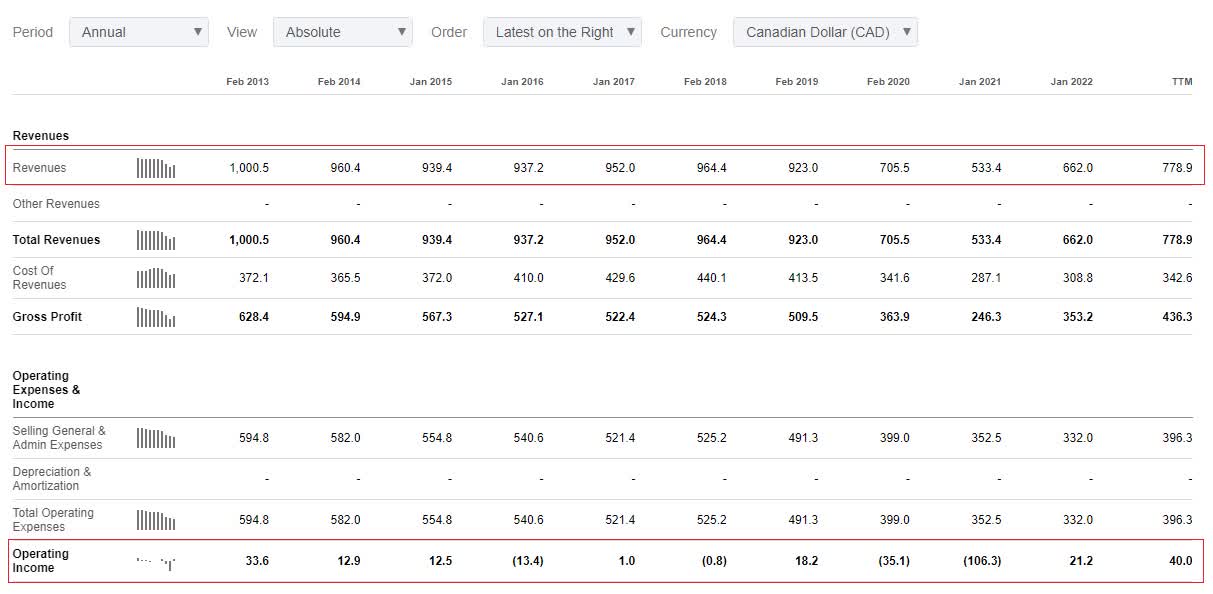

Reitmans is a family-owned clothing retailer with a 96-year-old history, and it currently has just over 400 stores in Canada under the Reitmans, Penningtons, and RW&Co brands. Looking at the financial performance for the past decade, Reitmans has been struggling to remain profitable and COVID-19 lockdowns forced the company to embark on a restructuring that resulted in the closure of the Thyme Maternity and Addition Elle banners, the shutdown of 140 stores as well as the firing of a quarter of all employees or about 1,600 people.

However, this restructuring can be viewed as a blessing in disguise as it enabled Reitmans to renegotiate retail leases at lower price levels and close unprofitable stores. In addition, the company paid only around 50 cents on the dollar to settle debt and liabilities. With COVID-19 lockdowns ending and Reitmans stores reopening, the business seems to be in excellent health as TTM operating income stands at C$40 million ($29.9 million). The operating income margin is 5.1% which is a decent level for a clothing retailer.

{kind=link}

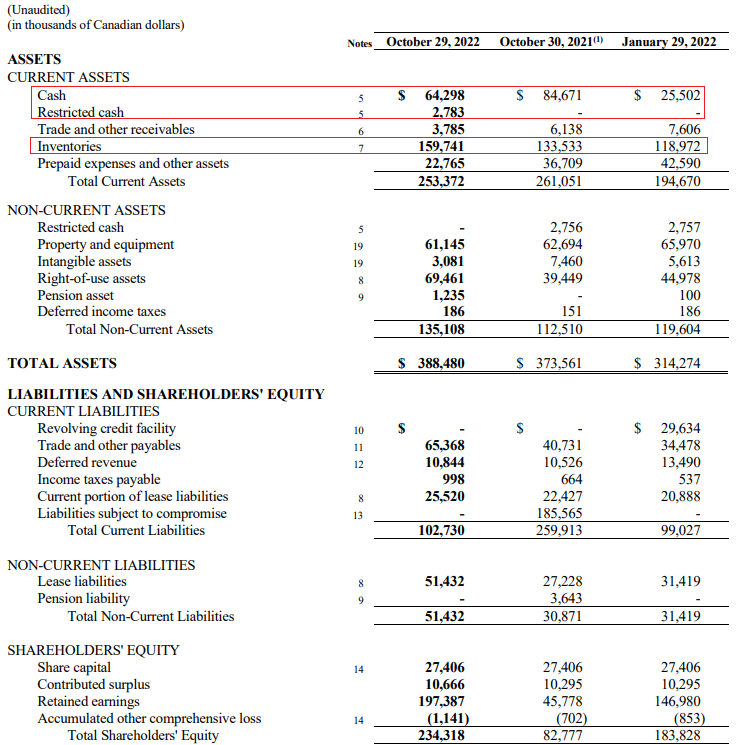

Turning our attention to the balance sheet, we can see that Reitmans had no debts as of October 29. The cash balance stood at C$67.1 million ($50.1 million) and I expect it to have increased significantly by January 29. There are two reasons for this. First, the holiday season is usually marked by destocking, and you can see that inventories fell by C$14.5 million ($10.9 million) in Q4 FY22. Second, inventories in Q3 FY22 were increased further to counter the effects of supply chain issues. If inventories fall back to C$119 million ($88.9 million), the cash balance would be around C$107 million ($79.9 million).

{kind=link}

Reitmans has a market capitalization of C$241.7 million ($180.5 million) as of the time of writing, which puts the enterprise value ((EV)) at C$174.6 million ($130.4 million). If you include the expected C$40 million ($29.9 million) decrease in inventories, we get C$134.6 million ($100.5 million). Reitmans should publish its FY23 financial report around the middle of April and I expect the annual operating income to decrease to around C$35-C$37 million ($26.1-$27.6 million) considering the whole sector is dealing with cost inflation.

In my view, a profitable business in a cyclical industry like clothing retail should be trading at about 8x EV/operating income. Taking into account the expected inventory decrease, Reitmans is trading at just 3.9x as of the time of writing which is why I think the company is undervalued by a wide margin. In addition, Canadian asset management firm Donville Kent recently said that the real estate assets of Reitmans in Montreal could be worth C$240 million ($179.2 million).

Looking at the catalysts for the share price that we can expect in the near future, I think that the company is likely to reinstate its dividend and could attract more institutional investor interest from firms like Donville Kent. In my view, asset sales are unlikely.

Turning our attention to the share price structure of Reitmans, the company has two classes of shares. The difference between them is that Class A shares have no voting rights. Otherwise, they are pretty much the same and have historically had the same dividend payments.

{kind=link}

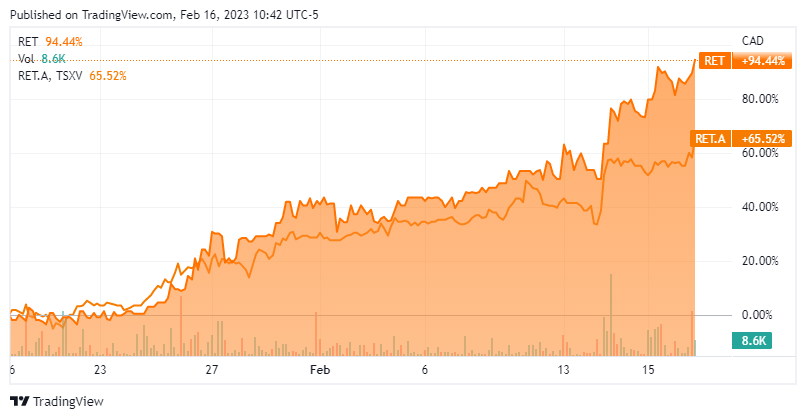

You could argue that the common shares should be priced higher, but I disagree as their free float is just 42.5% as the Reitmans family still has a majority stake. One month ago, the two classes of shares were trading at almost the same level at around C$3.00 ($2.24) but their prices have diverged significantly over the past few days. The common shares are 24% more expensive as of the time of writing.

{kind=link}

So, what’s the reason behind this situation? Well, I think the most likely explanation is that Donville Kent or another institutional investor has been focusing on building a position through the common shares. On February 14, Canadian digital newspaper La Presse reported that Donville Kent Senior Vice President & Portfolio Manager Jesse Gamble revealed in a phone interview that the company had just over a million Reitmans shares and that it made purchases as late as last week.

In my view, there is no justifiable reason why common shares should continue trading at a premium to Class A shares and I expect the gap to close in the coming weeks. Considering both classes of shares have strong momentum and Reitmans still looks cheap, I expect this to happen through an increase in the price of Class A shares. In view of this, I’ve sold my common shares and bought Class A shares for a similar total price.

Looking at the risks for the bull case, I think that the major one is share price volatility as Reitmans is a microcap company and the trading volume rarely exceeds 50,000 shares. For example, the share price reached C$3.00 ($2.24) in March 2022 and then went down below C$1.00 ($0.75) by June despite a lack of major news. I could also be underestimating the inflation pressure on costs and Q4 FY22 results are weaker than my expectations.

Investor takeaway

I like a good business turnaround story and I think that institutional investors are finally starting to take notice of the improvement in the fundamentals of Reitmans. I expect dividend payments to be reinstated in the near future and I’ve switched my position to Class A shares as I think that they offer better value at the moment. In my view, the difference in the price between the common and Class A shares makes no sense and I expect this difference to decline significantly in the near future.

For further details see:

Reitmans: 24% Price Difference Between The Share Classes Is A Buying Opportunity